Gen Zers, according to a recent Magnify Money survey, are overly optimistic about being wealthy. In fact, according to the survey, they are THE most financially optimistic generation. To wit:

“Nearly three-quarters (72%) of Gen Zers believe they’ll become wealthy one day, making them the most financially optimistic generation.”

But, interestingly, that optimism, as noted by the firm’s executive editor, is “more than just youthful optimism.”

“We are surrounded by extremes of wealth and poverty, and I think younger folks naturally gravitate to the more positive extremes. What’s more, the concept of investing is so much more accessible today, and I know many Gen Zers believe they can harness the power of the market to build wealth.” – Ismat Mangla

Interestingly, Gen Zers are optimistic they can use the stock market to build wealth. Unfortunately, that hasn’t worked out well for the generations before them.

Since 1980, there have been three major bull market cycles. The first started in the mid-80s and culminated in the Dot.com bust at the turn of the century. The early 2000s saw the inflation of the “real estate” bubble heading into the 2008 “financial crisis.“ We live in the third “everything bubble” fueled by a decade-long push of monetary and fiscal interventions.

However, 80% of Americans are still not “wealthy after these three major bull markets.”

That is according to some of the most recent surveys and Government statistics:

- 49% of adults ages 55 to 66 had no personal retirement savings, according to the U.S. Census Bureau’s Survey of Income and Program Participation (SIPP).

- The latest Federal Reserve Survey of Consumer Finances found that the median savings in Americans’ retirement accounts were $65,000.

- Less than half of those surveyed saved $100,000. Not enough to support a median retirement income of around $40,000 a year.

- One in six say they have saved nothing. A third currently makes NO contributions.

- 80% of people expected to see their living standards fall in retirement. 10% feared they wouldn’t be able to retire at all.

Will it be different for Gen Zers in the future? Unfortunately, it likely won’t be for the same reasons that using the stock market to build wealth didn’t work for the generations before them.

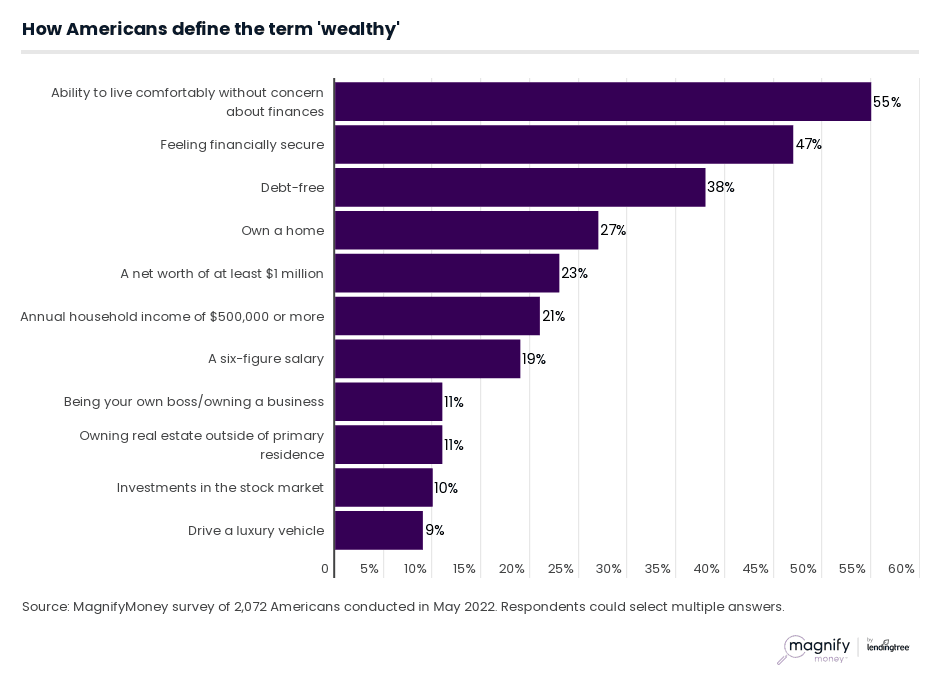

80% Of Americans Aren’t Wealthy

According to the Magnify survey, Gen Zers defined “being wealthy” by several measures:

Most surveyed define “wealthy” as living comfortably without concern about their finances. As shown below, that goal has eluded all but the top 20% of income earners.

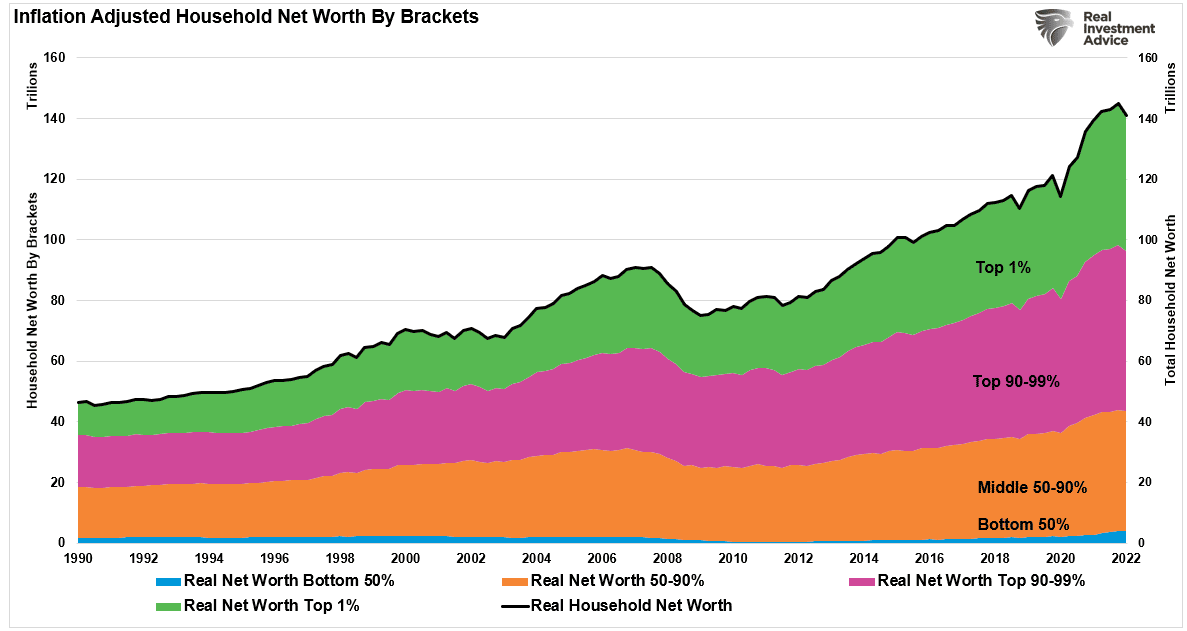

While 72% of Gen Zers believe they will be wealthy, the net worth of the bottom 50% of Americans has remained relatively unchanged since 1990. While the middle 50-90% of Americans have seen an increase in net worth, it has not been enough to keep up with the “standard of living,” which, as discussed previously, continues to push Americans further into debt.

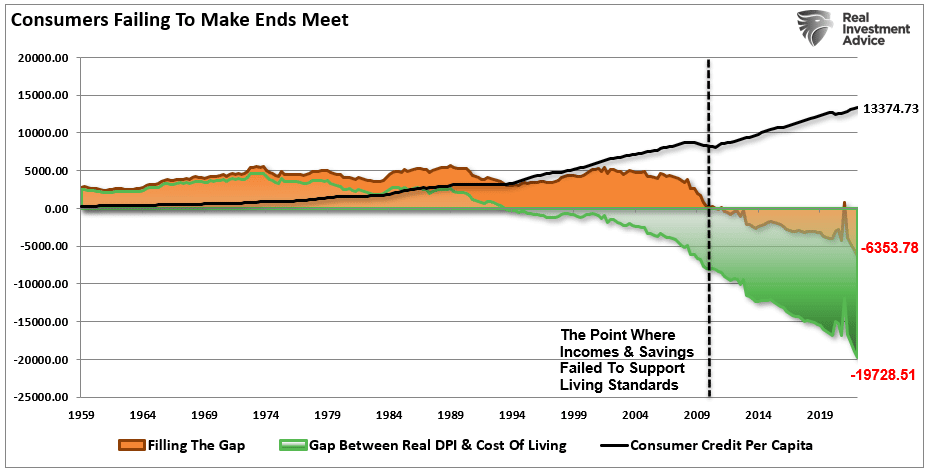

“The current gap between savings, income, and the cost of living is running at the highest annual deficit on record. It currently requires roughly $6,300 a year in additional debt to maintain the current standard of living. Either that or spending gets reduced which is the likely outcome as a recession becomes more visible.” – The One Chart To Ignore

Another Magnify Money survey supports this bit of analysis by showing that roughly 50% of working Americans live “paycheck-to-paycheck,” meaning they have no money left after expenses. While that was common among those making less than $35,000 annually (76%), 31% of those making more than $100,000 experienced the same.

The critical point is that it is hard to count on the stock market to build wealth when you don’t have excess savings with which to invest.

The Stock Market Won’t Make You Wealthy

Generation Z, born between 1992 and 2002, was between 5 and 16 years old during the financial crisis. Such is important because they have never truly experienced a “bear market.” Any advice they might have received from financial advisors suggesting caution, asset allocation, or risk management was repeatedly proven to underperform the market.

“Ha….Boomers just don’t get it.”

However, since they became old enough to open an investment account, they have only seen a “liquidity-driven” bull market that fostered a generation of “Buy The F***ing Dip “ers.

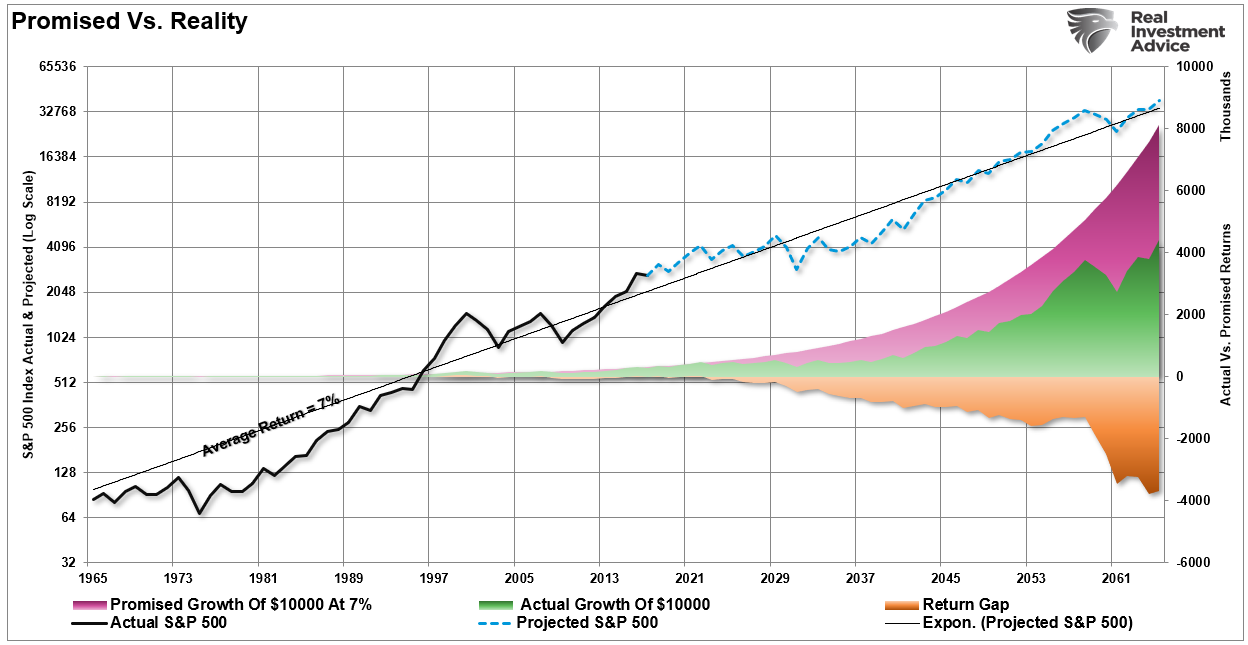

However, while the lack of savings was one of the key points in “The One Chart To Ignore,” the other key point, and why 80% of Americans didn’t build wealth, is that “markets don’t compound returns.“

“There is a significant difference between the AVERAGE and ACTUAL returns received. As I showed previously, the impact of losses destroys the annualized ‘compounding’ effect of money. (The purple shaded area shows the “average” return of 7% annually. However, the differential between the promised and “actual return” is the return gap.)“

While 26% of Gen Zers think that investing in the stock market and 19% in Cryptocurrencies will be their ticket to financial wealth, a lot of financial history suggests this will not be the case.

While Gen Zers are very optimistic they will be wealthy in the future, a mountain of statistical and financial evidence argues to the contrary. Will some Gen Zers attain a high level of wealth? Absolutely. Roughly 10% of them. The remainder will likely follow the exact statistical breakdown of the generations before them.

The reasons for that disappointing outcome remain the same. If investing money worked as the mainstream media suggests, as noted above, then why, after three of the most significant bull markets in history, are 80% of Americans so woefully unprepared for retirement?

The crucial point to understand when investing money is this: the financial market will do one of two things to your financial future.

- If you treat the financial markets as a tool to adjust your current savings for inflation over time, the markets will KEEP you wealthy.

- However, if you try and use the markets to MAKE you wealthy, the market will shift your capital to those in the first category.

Experience tends to be a brutal teacher, but it is only through experience that we learn how to build wealth successfully over the long term.

How Money Really Works

It isn’t just about investing money. There are also vital points about the money itself.

1. Your career provides your wealth.

You most likely will make far more money from your business or profession than from your investments. Only very rarely does someone make a large fortune from investments, and it is generally those that have a business investing wealth for others for a fee or participation. (This even includes Warren Buffett.)

Focus on your career, or business, as the generator of your wealth.

2. Save money. A lot of it.

“Live on less than you make and save the rest.” Such sounds simple enough but is exceedingly difficult in reality. Given that 80% of Americans have less than $500 in savings tells the real story. However, without savings, we can’t invest to grow our savings into future wealth.

3. The true goal of investing money is to adjust savings for inflation.

As investors we get swept up into the “casino” called the stock market. However, the true goal of investing is to ensure that our “savings” adjust for future purchasing power parity in the future. While $1 million sounds like a lot today, in 30-years it will be worth far less due to the impact of inflation. Our true goal of investing is NOT to beat some random benchmark index by taking on excess risk. Rather, our true benchmark is the rate of inflation.

4. Don’t assume you can replace your wealth.

The fact that you earned what you have doesn’t mean that you could earn it again if you lost it. Treat what you have as though you could never earn it again. Never, take chances with your wealth on the assumption that you could get it back.

5. Don’t use leverage.

When someone goes completely broke, it’s almost always because they used borrowed money. Using margin accounts, or mortgages (for other than your home), puts you at risk of being wiped out during a forced liquidation. If you handle all your investments on a cash basis, it’s virtually impossible to lose everything—no matter what might happen in the world—especially if you follow the other rules given here.

6. Whenever you’re in doubt, it is always better to err on the side of safety.

If you pass up an opportunity to increase your fortune, another one will be along soon enough. But if you lose your life savings just once, you might never get a chance to replace it. Always err on the side of caution. Always ask the question of what CAN go “wrong” rather than focusing on what you “HOPE” will go right.

Investing money in our future is not as simple as much of the media makes it seem. We all want to be able to under-save today for tomorrow’s needs by hoping the markets will make up the difference. Unfortunately, there is no magic trick to building wealth.

The process of saving diligently, investing conservatively, and managing expectations will build wealth over time.

It’s boring. But it works.

No matter your age, it’s not too late to start making better choices.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.