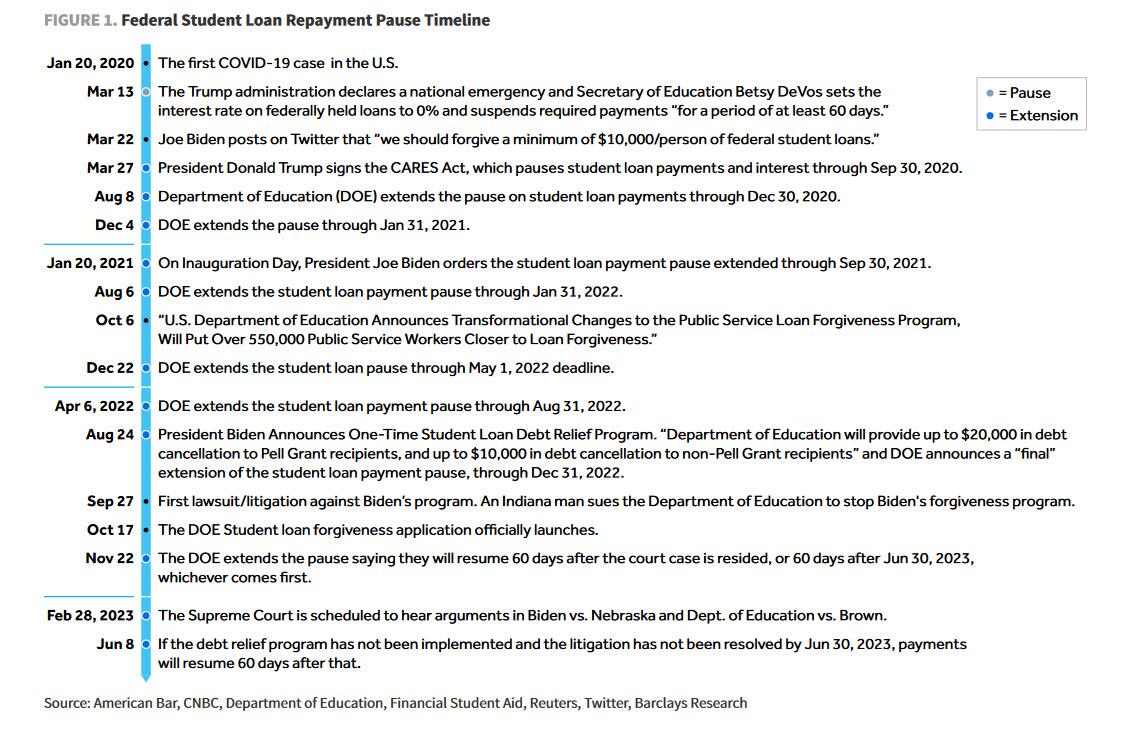

Millions of young Americans will face the end of the student loan payment moratorium this summer. Why is this happening now, after a three-year break from payments? It is the result of the recent passage of the “Fiscal Responsibility Act” to raise the debt ceiling. Under that act, the Biden Administration is prohibited from extending the pause on student loan repayments which have remained in place since March 2020.

“Student loan payments are set to resume in the coming months. For more than 40 million Americans carrying student loan debt, the timeline to resume making payments is now on the horizon. The debt ceiling deal passed earlier this month paves the way for student loan payments to resume as early as August 29, 2023, per the latest update from the U.S. Department f Education: Federal Student Aid. For most, this will be the first time making payments since the early days of the pandemic in March 2020.” – Zerohedge

“So what? Some students with tuition debt now have to pay their loans.”

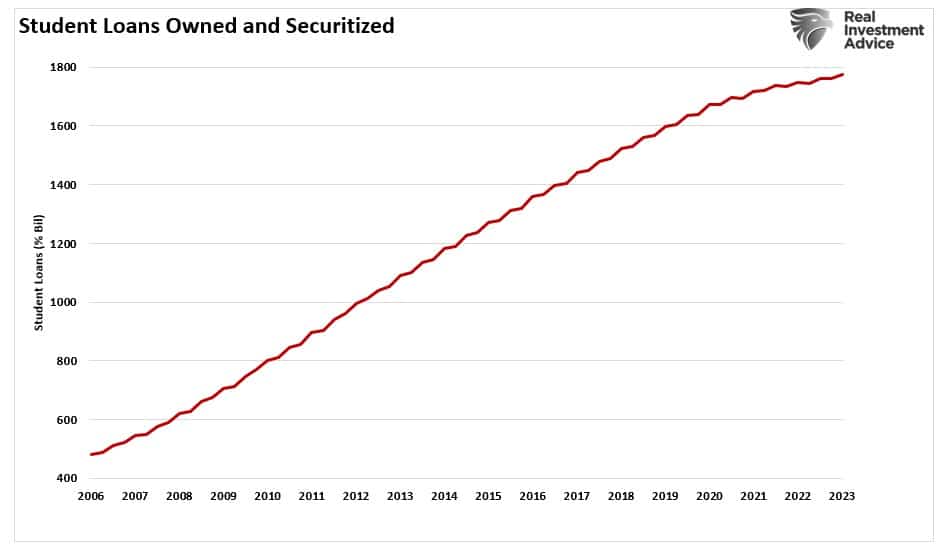

While, on the surface, the restarting of payments does not sound like a “big deal,” it is. As of the end of Q1-2023, almost $1.8 Trillion in student loan debt is outstanding. That debt carries a substantially higher interest rate than current bank loan rates.

“About 92 percent of student loan debt is federal, with interest rates ranging from 4.99 percent to 7.54 percent. Average private student loan interest rates, on the other hand, can range from just under 4 percent to almost 15 percent.” – Bankrate

When you account for the size of the debt outstanding, the impact on personal spending in the future is significant.

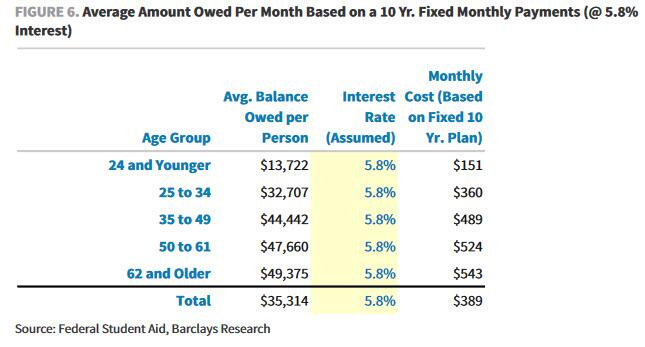

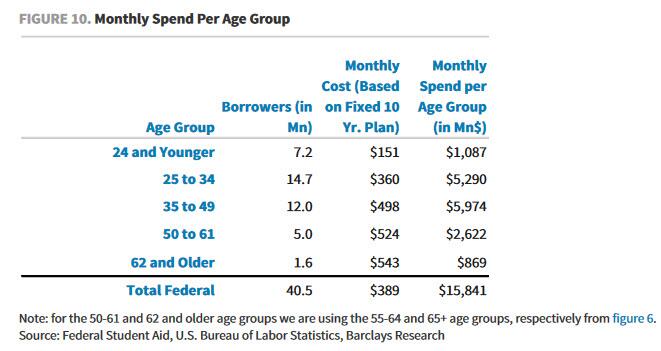

“The analysis is based on federal student loan data for the aggregate $1.4 trillion balance across the 40.5mn borrowers by age cohort. Utilizing a 10-year payment period and a 5.8% interest rate, the bank calculates an approximate $390/month payment across cohorts.

“Compared to a median pre-tax personal annual income of ~$57k, this payment represents an approximate 8% headwind to monthly income. In aggregate, this amounts to an “additional” (or rather, original, as the payments were there and then three years ago, they just stopped) $15.8bn in monthly payment for federal student loans affecting approximately 15.5% of the U.S. adult population (and 32% of the 25- to 34-year-old cohort).” – Barclays

That is a significant amount of money consumers have retained to spend on other things. Such is likely why retail spending has remained surprisingly buoyant in the face of higher interest rates and slowing economic growth. However, the question is whether the return of tuition payments will weaken that economic support.

Retail Sales And Economic Growth

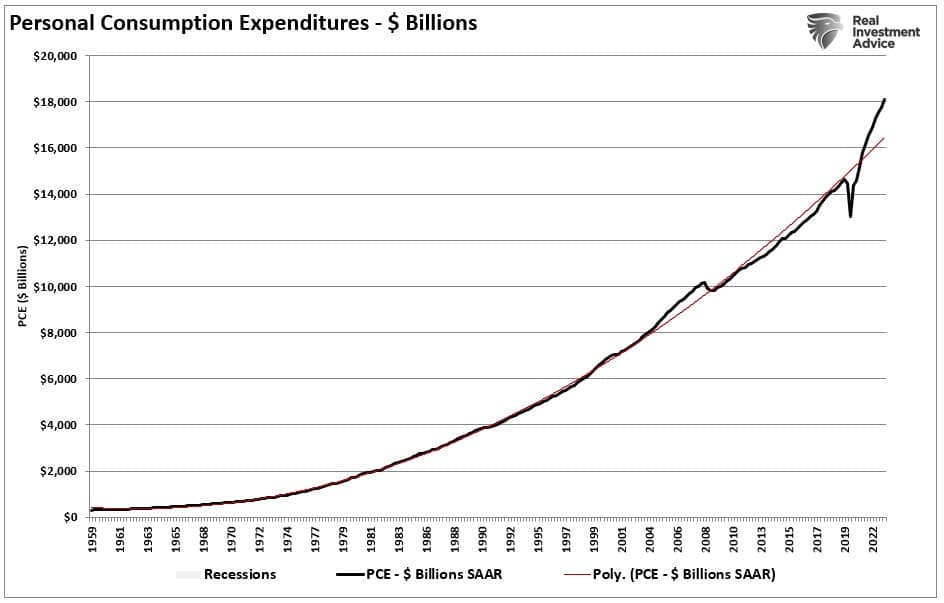

In Q1 of 2023, the U.S. economy totaled $26.5 Trillion. Of that, as shown, Personal Consumption Expenditures, what we spend in the economy, total $18 Trillion.

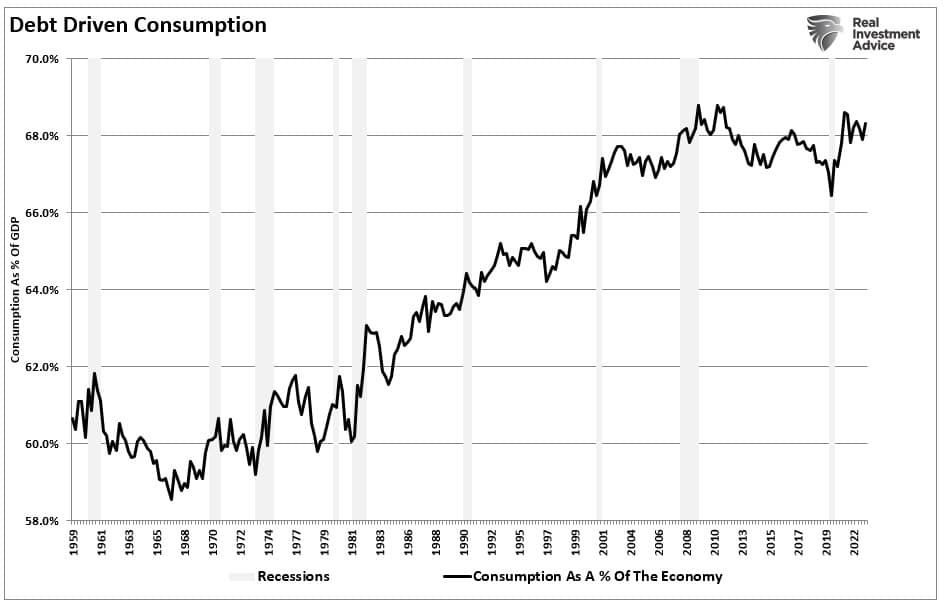

In other words, nearly 70% of the economy is a function of consumer spending.

Logically, the concern is that when student loan payments restart, that will divert spending from the economy into debt service. (This is the same concern the U.S. faces with $32 Trillion in debt.)

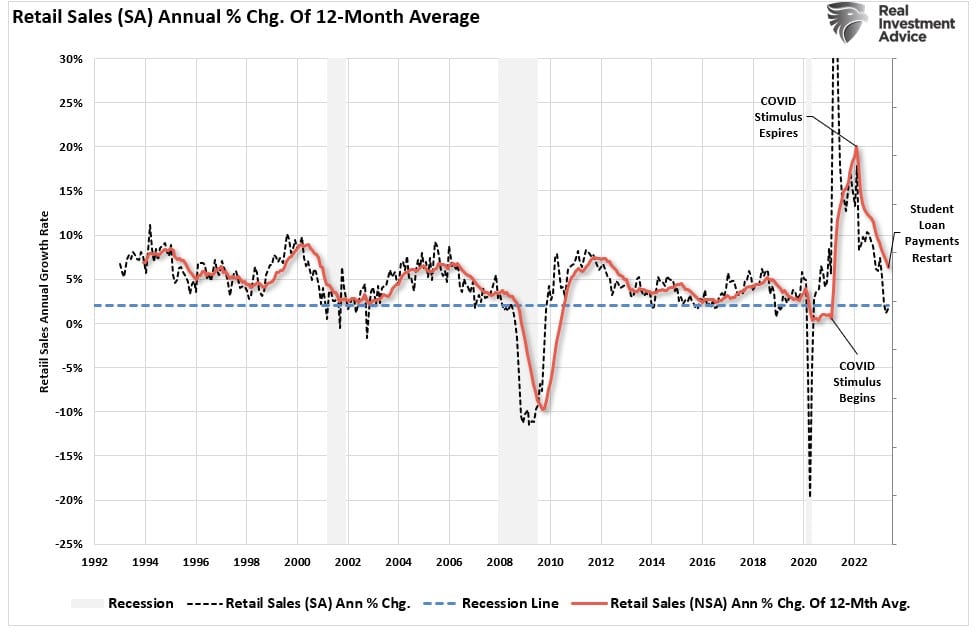

In the U.S., retail sales comprise about 40% of personal consumption expenditures. When student loan payments restart, the most immediate impact will be felt in retail sales as consumers have less money to spend on discretionary items and services. Since 1992, retail sales, on a seasonally adjusted basis, have grown at an average rate of $1.4 billion monthly. The chart below shows the annual rate of change in seasonally adjusted retail sales versus the 12-month moving average of the annual rate of change.

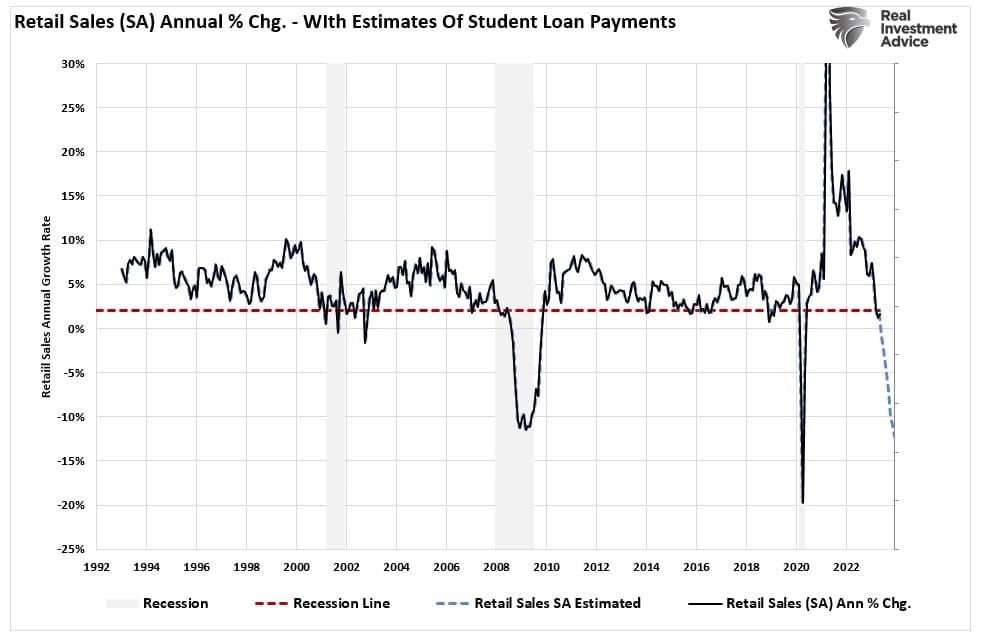

If Barclay’s Bank is correct in its assumptions, removing the student loan moratorium on payments will significantly impact retail sales. The chart below projects the average retail sales growth less the student loan payments. If Barclay’s is correct in its assumptions, the impact on retail sales could be significant.

A Recession Risk

Given the importance of retail sales on overall economic growth, it is difficult to avoid a recession.

“According to a New York Fed study, the average student loan payment is $393 monthly. For consumers taking advantage of the program, they have deferred 39 months’ worth of payments, resulting in more than $15,327 in additional discretionary income during the period, much larger than the amount most consumers received from other COVID stimulus programs.

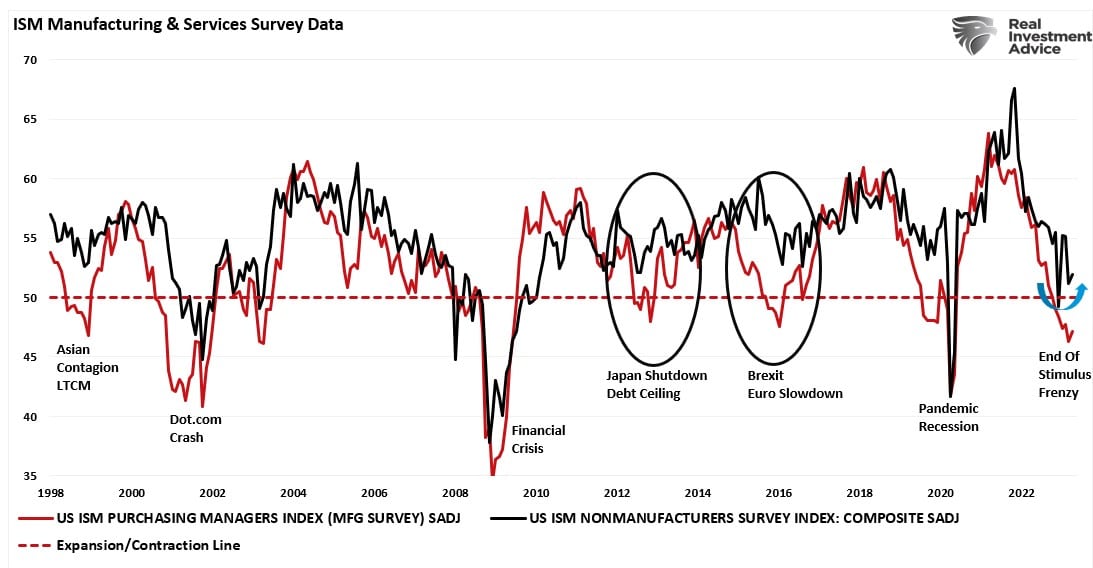

That sudden increase of $393 per month in loan repayments will force prime-age consumers (those aged 18-44 years) to cut back on discretionary spending. Since portions of that particular demographic tend to prioritize experiences over goods consumption, we will likely see a more significant impact on services which, as discussed previously, has been the one support keeping the economy out of recession.

“This isn’t the first time we have seen the manufacturing side of the economy contract, but services remained robust enough to keep the overall economy out of recession. The economy similarly avoided a “recession” in 1998, 2011, and 2015.”

If the data is correct, the economic and earnings risk is significant.

An Overlooked Risk

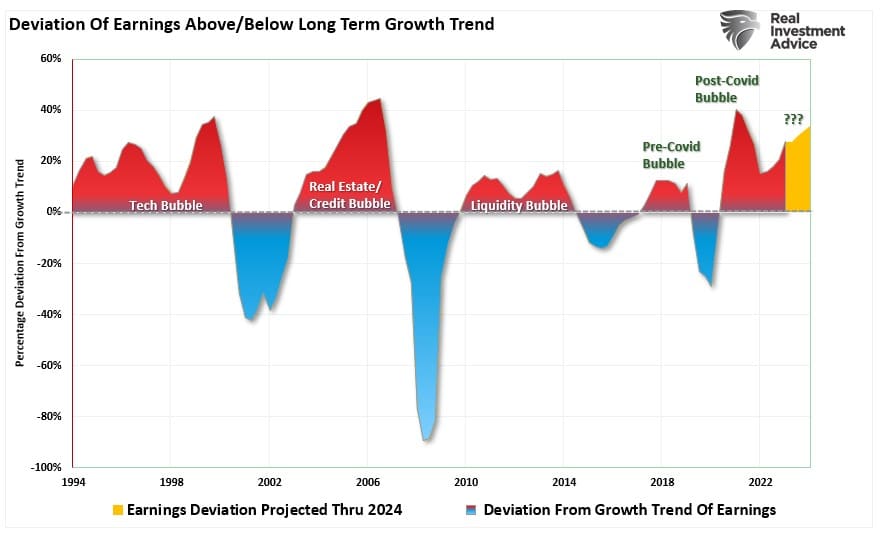

Since January, investors have been piling into cyclical stocks, assuming inflation would ease and the economy would avoid a recession. As noted, Wall Street analysts have become optimistic about accelerating earnings growth into next year.

“Analysts expect the first quarter of 2023 will mark the bottom for the earnings decline, and growth will accelerate into year-end. Again, this is despite the Fed rate hikes and tighter bank lending standards that will act to slow economic growth. The problem with these expectations is the detachment of earnings estimates above the long-term growth trend. The only two previous periods with similar deviations are the “Financial Crisis” and the “Dot.com” bubble.“

However, the restarting of student loan repayments may be the one thing Wall Street overlooked in its rush to trumpet the “return of the bull.” The problem is that cyclical stocks heavily depend on consumer spending, particularly in technology, where companies like Apple, Microsoft, and Amazon are direct-to-consumer companies. As those funds are redirected to student loan payments, a contraction in consumer spending will directly impact those companies’ sales, reducing bottom-line earnings.

Given that markets, and many of the high-flying names in 2023, are grossly overvalued, any negative impact on forward-earnings estimates could lead to a significant price correction. Most certainly, such a price reversion would accompany a recession in the economy caused by a contraction in spending.

While it is always unwise to bet against the U.S. consumer, the restarting of student loan payments is likely a hurdle the economy will struggle with. Furthermore, it is likely this is an impact the market has yet to factor into its assumptions for future economic and earnings growth rates.

We will find out later this year.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.