“(Market) Predictions Are Difficult…Especially When They Are About The Future” – Niels Bohr

Okay, I took a little poetic license, but the point is that while we try, predictions of the future are difficult at best and impossible at worst. If we could accurately predict the future, fortune tellers would win all the lotteries, psychics would be richer than Elon Musk, and portfolio managers would always beat the index.

However, we can analyze what occurred previously, weed through the noise of the present, and discern the possible outcomes of the future. The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the unexpected and random events they inevitability occur.

We have seen plenty, from trade wars to Brexit, to Fed policy and a global pandemic in recent years. Yet, before each of those events caused a market downturn, Wall Street analysts were wildly bullish that wouldn’t happen.

For example, on December 7th, 2021, we wrote an article about the predictions for 2022.

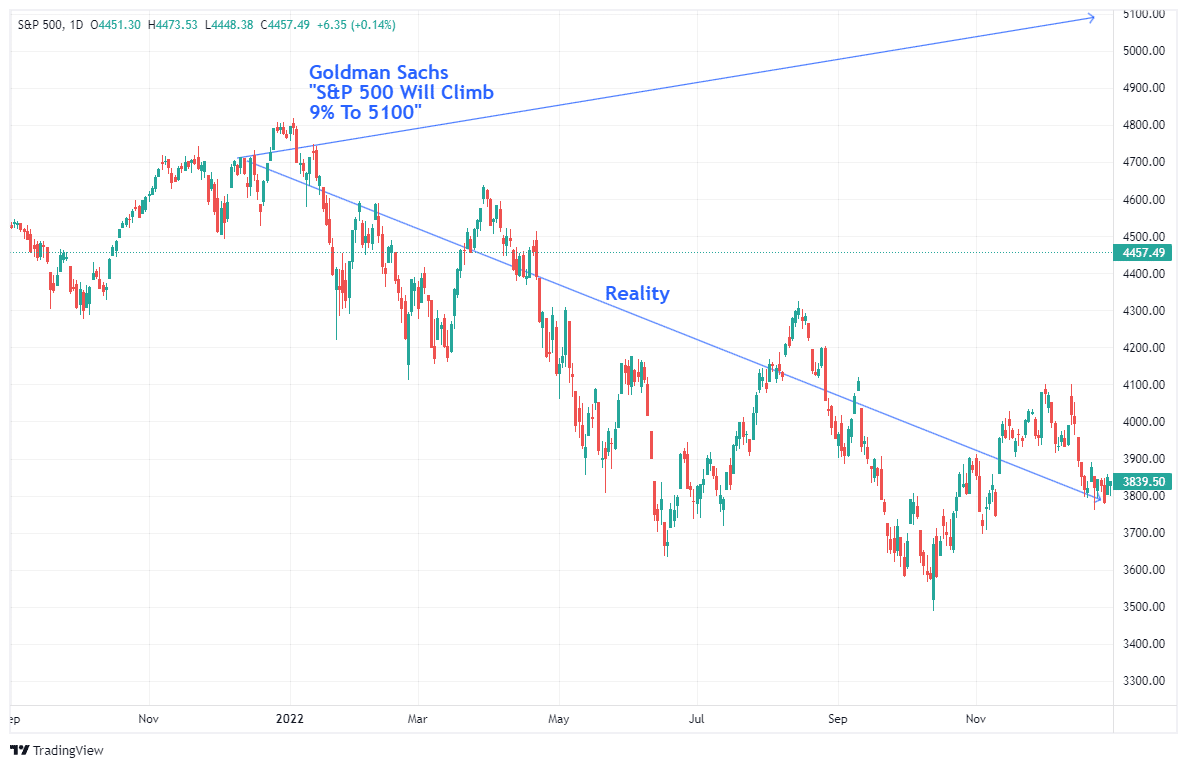

“There is one thing about Goldman Sachs that is always consistent; they are ‘bullish.’ Of course, given that the market is positive more often than negative, it ‘pays’ to be bullish when your company sells products to hungry investors.

It is important to remember that Goldman Sachs was wrong when it was most important, particularly in 2000 and 2008.

However, in keeping with its traditional bullishness, Goldman’s chief equity strategist David Kostin forecasted the S&P 500 will climb by 9% to 5100 at year-end 2022. As he notes, such will “reflect a prospective total return of 10% including dividends.”

The problem, of course, is that the S&P 500 did NOT end the year at 5100.

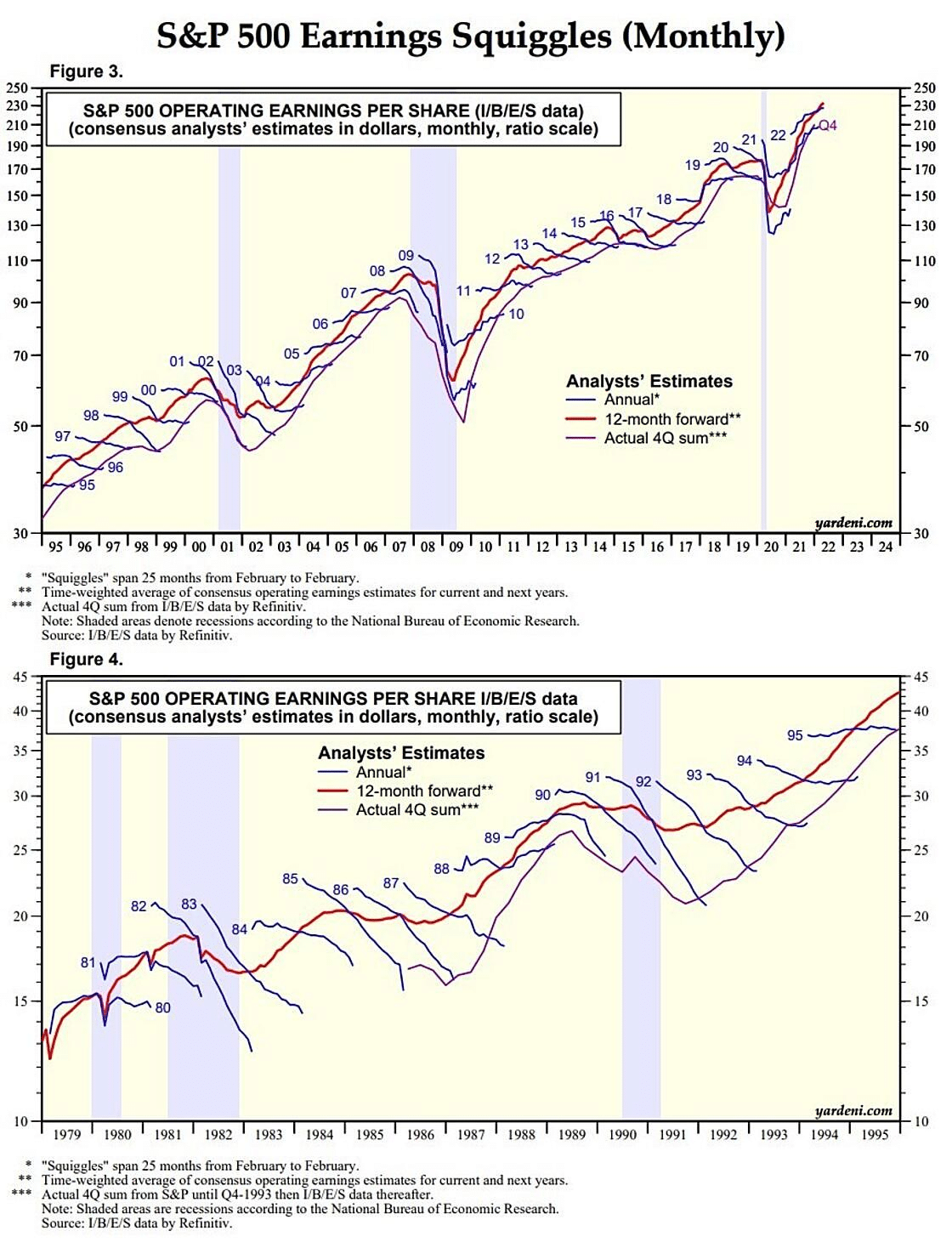

It isn’t just Goldman Sachs always making bullish and erroneous forecasts but the vast majority of Wall Street analysts. Such errors in predictions are most evident in expectations for forward earnings. Ed Yardeni tracks the historical earnings forecast and changes for each year. Analysts’ expectations are clearly wrong by about 30% on average.

Despite increasing signs of recessionary risk, analysts are once again becoming increasingly optimistic about earnings growth into 2024. Of course, such would require substantially stronger economic growth to generate those earnings.

So, the question becomes how much faith should we have in Wall Street estimates when it comes to our investing?

Predictions Of The Future Have An Expiration

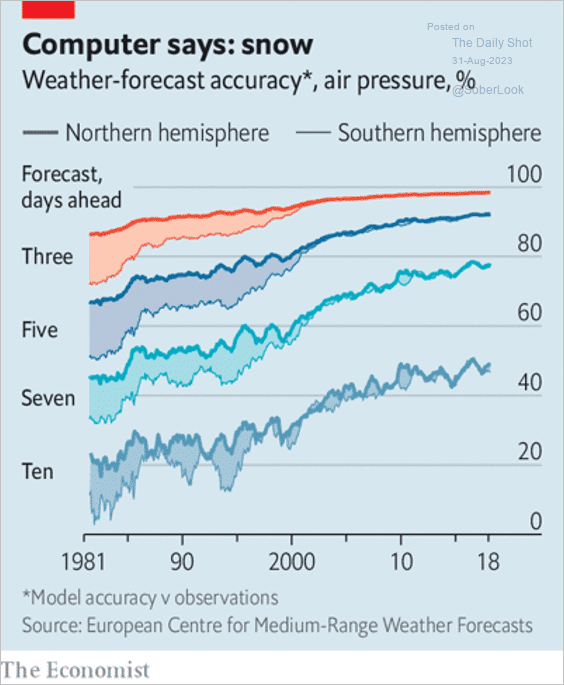

In the late 90s, there was a study on the accuracy of “predictions.” The study took predictions from various professions, including psychics and meteorologists. The study came to two conclusions.

- “Meteorologists” are the MOST accurate predictors of the future, and,

- The predictive ability was accurate to just 3-days.

Most importantly, once predictions stretch beyond 3-days, the accuracy is no better than a coin flip.

A quarter of a century later, the Economist magazine analyzed computer models and their weather-forecasting accuracy. Surprisingly, despite the massive increases in computer analysis capabilities, increased data collection, and improved models, the accuracy has failed to improve. Now, as it was then, the accuracy of weather forecasts is roughly 100% for 3-days into the future. However, at ten days, the accuracy is still no better than a coin flip.

Here is the critical point. When analyzing weather patterns, there is a tremendous amount of observable data. From surface temperatures to high and low-pressure zones, humidity, air quality, and numerous data points. That data, collected by Doppler radar, radiosondes, weather satellites, buoys, and other instruments, is fed into computerized NWS supercomputers where numerical forecast models go to work.

Still, with all that data, the predictions’ accuracy is only good for three to ten days.

Given the markets are affected by a broad spectrum of extremely variable inputs from economics to geopolitics, monetary policy, interest rates, financial events, and most importantly, human psychology, how accurate are predictions 12 months into the future?

As investors, how much weight should give to any prediction that extends for more than a week?

Navigating From Here

In the short term, all that really matters to investors is short-term market psychology. That psychology is easily seen in the technical analysis of market price data. This is why we spend each week discussing with you the technical support and resistance levels and the market’s overall trend – bullish or bearish.

In the long term, meaning over the course of the next decade, it is fundamentals and valuations that will determine the return on your investments.

With that in mind, my job as a portfolio manager is to navigate market risks as we see them. Making a “one-sided” bet on a potential outcome harbors an outsized risk of being wrong. Such would potentially impact client capital and damage financial outcomes.

Therefore, we approach risk management in the market by choosing to hedge risk and reduce potential liabilities. As such, given the market’s current structure, we have three options currently:

- Do Nothing – If the markets do correct, we destroy capital and time waiting for the portfolio to recover.

- Take Profits – Taking profits, raising cash, and reducing equity exposure before a correction helps mitigate the damage of a decline. However, if wrong, we can repurchase positions, add new ones, or resize portfolio holdings as needed.

- Hedge – We have also opted to hedge by adding a position to the portfolio that is the “inverse” of the market. Such allows us to keep existing positions intact. By “shorting against the portfolio,” we effectively reduce our equity risk (and related capital destruction) during a market correction.

As noted, we continued to use a combination of both #2 and #3 in the past. Doing nothing leaves us overly exposed to an unexpected “volatility shock” in the market or the reversal of bullish psychology.

In our view, we can either manage risk or ignore it.

The only problem with “ignoring risk” is that such has a long history of not working out well.

Investment Guidelines

When it comes to investing, we tend to repeat our mistakes by forgetting the past. Therefore, it is worth repeating investing guidelines to return your focus to what truly matters.

- Investing is not a competition. There are no prizes for winning but severe penalties for losing.

- Emotions have no place in investing. You are generally better off doing the opposite of what you “feel.”

- The ONLY investments that you can “buy and hold” are those providing an income stream and return of principal.

- Market valuations are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in.”

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.