The term “Bond Vigilantes” is a nostalgic twist on an old-west theme. In the nineteenth century, the American West formed self-appointed groups, or committees, to seize the duties of law enforcement and judicial authority in situations when citizens found law enforcement lacking or inadequate.

In the bond market, the term “Bond Vigilante” was first coined by Ed Yardeni in 1980 when bond traders sold Treasurys in response to the growing power of the Federal Reserve and its policies on the U.S. economy. (Sound familiar?) According to Investopedia:

“A bond vigilante is a bond trader who threatens to sell, or actually sells, a large number of bonds to protest or signal distaste with policies of the issuer. Selling bonds depress their prices, pushing interest rates up and making it more costly for the issuer to borrow.”

If the “Sheriff” in town isn’t doing their job, the premise is that holders will become “Bond Vigilantes” and “take the law into their own hands.”

Over the last couple of years, the fear of “Bond Vigilantes” has returned with the surge of inflation since 2022. Even Ed Yardeni, the economist who coined the term “Bond Vigilantes” and has regularly predicted their return to the investment landscape ever since, says they’re “saddling up.”

The problem is that the expected return of the “Bond Vigilantes” is flawed as it is based on the premise that those vigilantes have the power to “take the law of monetary policy into their own hands.”

“Shorting government bonds when the central bank is politically aligned with the Treasury is a sure-fire way to lose lots of money. The consolidated government’s balance sheet consists of IOU liabilities that it can manufacture in infinite quantities. Why would anyone think they can win that game? It’s like my writing IOUs for blog points. Maybe I write more than I can ever cover for. But I create the points. I can always create more. if I write too many, their value depreciates.” – Credit Writedowns, circa 2011.

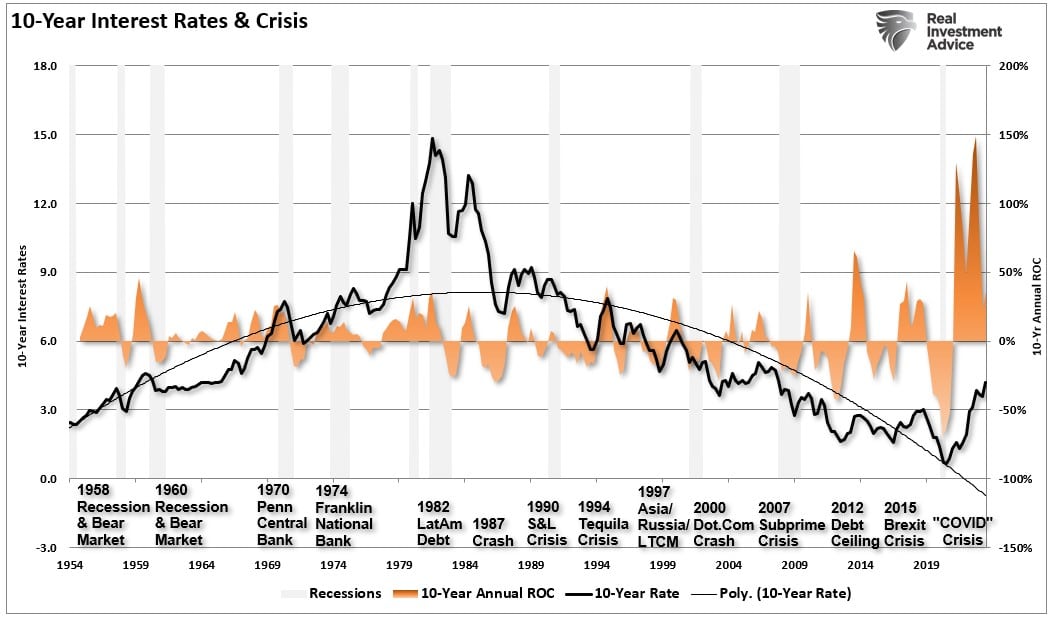

As shown in the chart below, since 1980, betting on the return of the vigilantes has been a losing bet. (It is worth noting that previous spikes in the annual rates of change in rates preceded either financial events or recessions. The current episode is magnitudes more significant than any prior event since 1954)

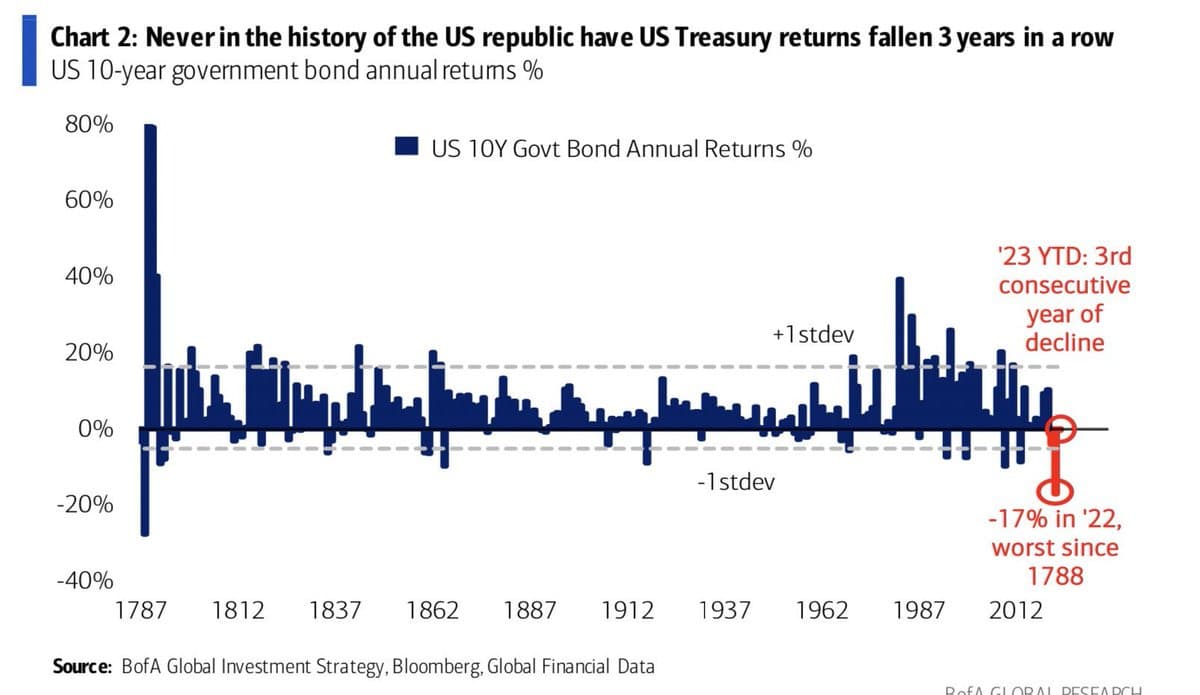

Lastly, if you are betting on the return of the vigilantes, the track record of betting against the bond market since 1787 remains quite dismal.

The biggest flaw in the “return of the Bond Vigilantes” theory remains the “Town Sheriff.”

The Central Bank Sheriffs

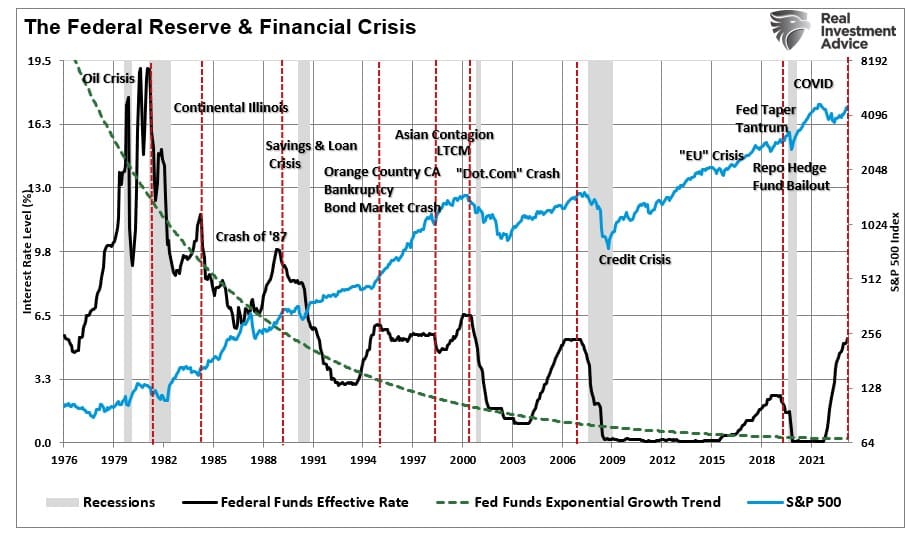

As noted above, since 1980, the Federal Reserve has been a critical player in the bond market. Either through monetary policy changes, raising or lowering interest rates, or, as seen since 2008, directly intervening in the bond market. Those actions by the Federal Reserve were always in response to a financial event, crisis, or recession.

While Central Banks have always been the “Sheriff” in town, the “Bond Vigilantes” can run amok for a while before finding themselves on the wrong end of the hangman’s noose. Such has mainly been the case following the Financial Crisis in 2008.

“Earlier this year, the world’s most famous bond investor, Bill Gross, was short U.S. government debt. He was hailed as THE VIGILANTE by Megan McArdle at The Atlantic. At long last, it seemed, the long-dormant bond vigilantes had arrived on horseback, ready to force the U.S. government into austerity.” – Business Insider, 2011

Of course, that venture by Bill Gross backfired as Central Banks repeatedly stepped in. To quote the President of the European Central Bank, Mario Draghi.

“We will do whatever it takes to preserve the continent’s common currency.”

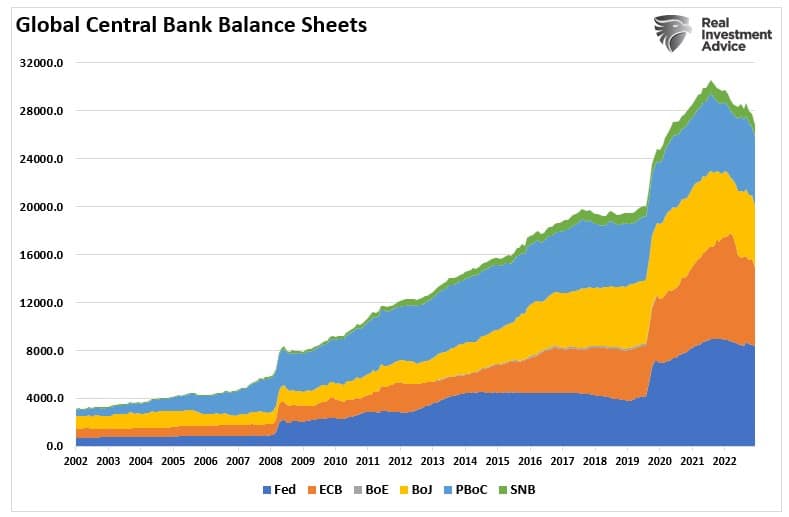

Doing “whatever it takes” has not been just the stance of the ECB “Sheriff,” but every major Central Bank since 2008. As discussed in “Deficit Surge:”

“Many ‘bond bears’ suggest that rates must rise as deficits increase and more debt is issued. The theory is that at some point, buyers will require a higher yield to buy more debt from the U.S. Such is perfectly logical in a normally functioning bond market where the only players are the individual and institutional bond market players. In other words, as long as ‘all else is equal,’ rates should rise in such an environment.“

All Else Is Not Equal

However, all else is not equal in a global economy where government debt yields are controlled by Central Banks colluding with Governments to maintain economic growth, control inflation, and avoid financial crises.

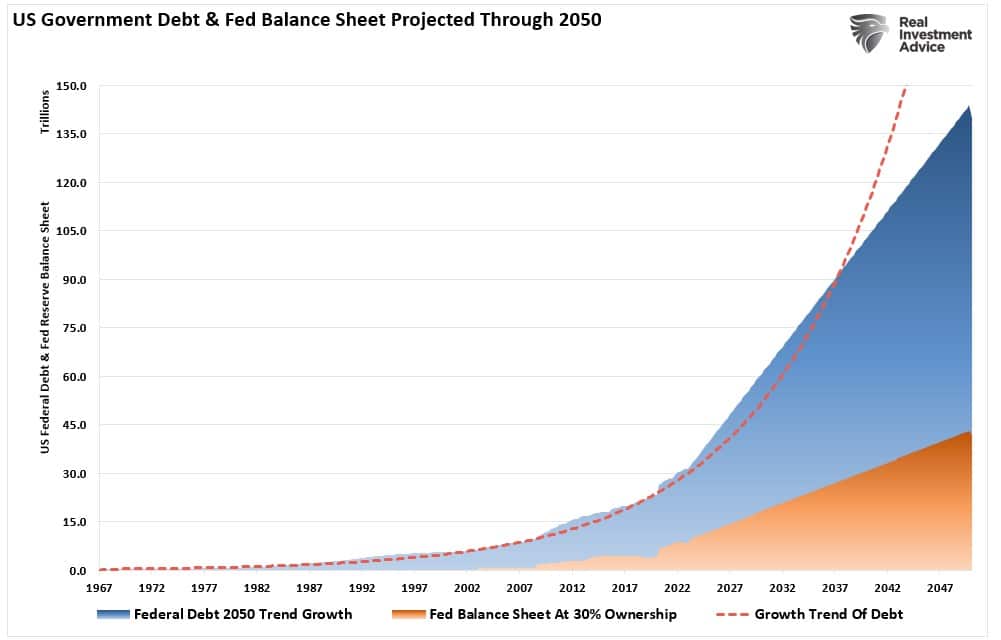

This monetization of debt issuance to support anemic economic growth, suppress inflationary forces, and depress borrowing costs will not change in the future. The biggest problem with the “Bond Vigilante” thesis is the inability of the economy to sustain higher rates due to mounting debt issuance and rising deficits. The chart below models the CBO analysis using the growth trend of debt but also includes the need for the Federal Reserve to monetize nearly 30% of the issuance.

At the current growth rate, the Federal debt load will climb from $32 trillion to roughly $140 trillion by 2050. Concurrently, assuming the Fed continues monetizing 30% of debt issuance, its balance sheet will swell to more than $40 trillion.

While you may think such is unsustainable, there is a clear example of why “Bond Vigilantes” keep getting arrested.

Japan Is A Good Example

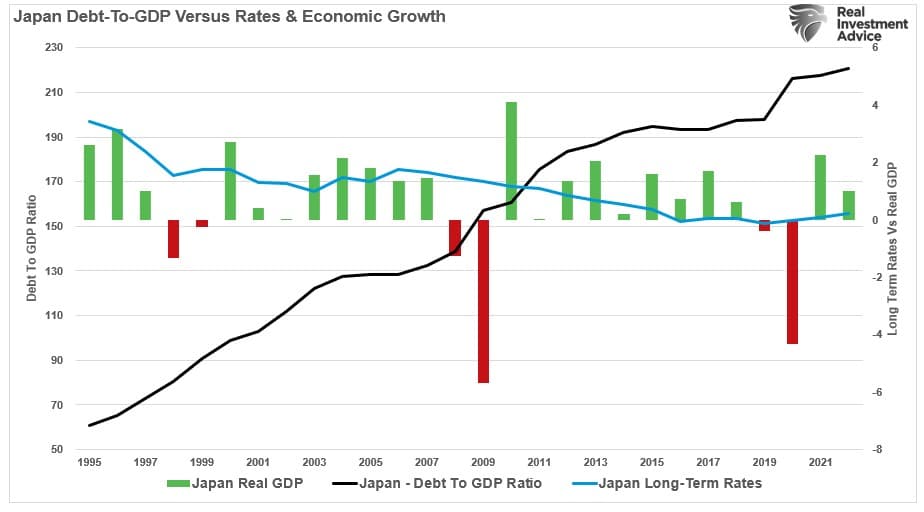

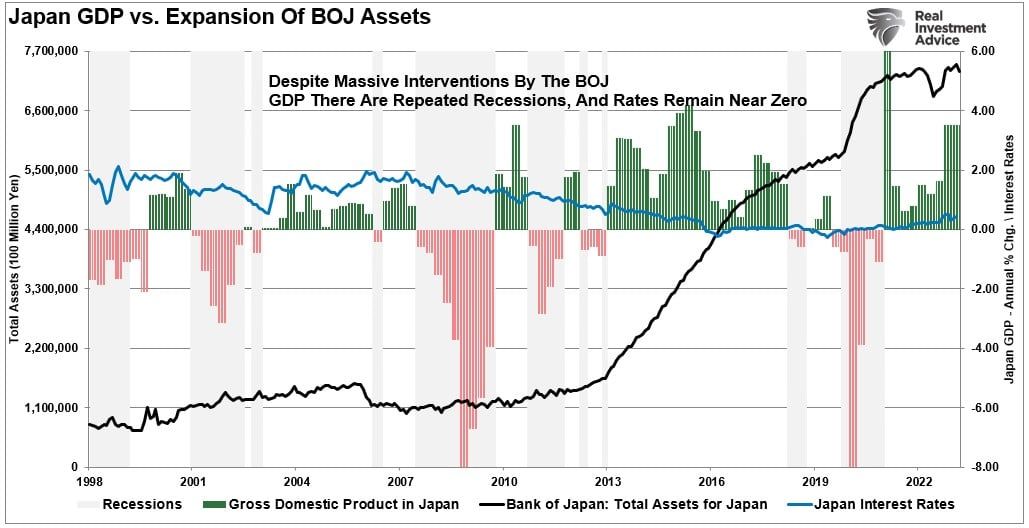

Since 2008, Japan has run a massive “quantitative easing” program. That program, on a relative basis, is 3-times more extensive than in the U.S. Not surprisingly, economic prosperity is only marginally higher since the turn of the century. Nonetheless, if the thesis of “Bond Vigilantes” is valid, and if they exist, then Japan should be fighting significantly higher interest rates and inflation, given a debt-GDP ratio of more than 210%.

Surprisingly, there is no evidence of such. Maybe the situation would be markedly different if the Bank of Japan (BOJ) didn’t own most ETF, corporate, and government debt markets. However, such is also why Japan continues to be plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time recently.)

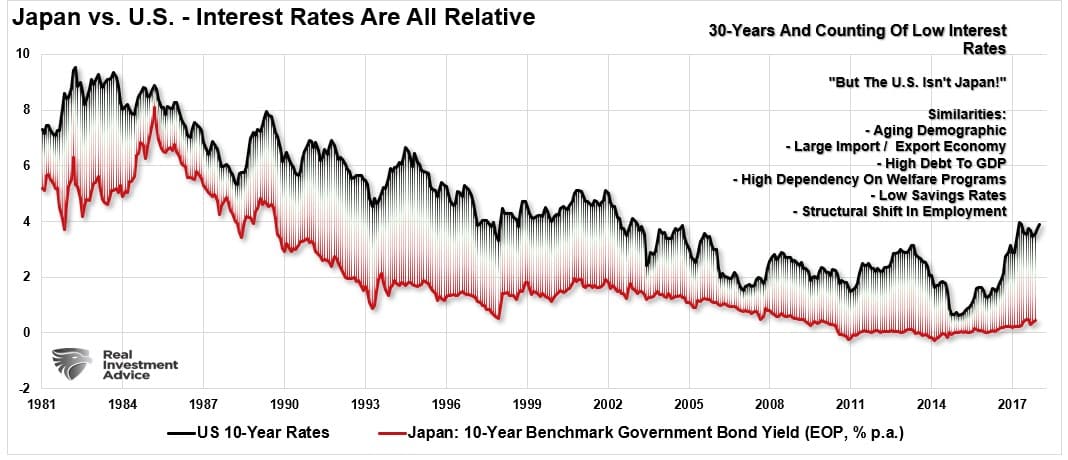

While many argue the U.S. economy will eventually “grow” its way out of debt, there is no evidence such a capability exists. We know that interest rates in the U.S. and globally are telling us economic growth will remain weak in the future. While the recent surge in U.S. interest rates resulted from massive one-time liquidity injections, the similarities between the U.S. and Japan remain a stark reminder of where interest rates will ultimately be.

The reality is that each time interest rates tick higher, the rumors of the return of the “Bond Vigilante” surface. In the short term, it may seem like they are moving markets. However, eventually, the “Sheriff” will arrive to reassert its force on the markets. This isn’t a good thing, as noted by my colleague Doug Kass:

“The fact is that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.”

Japan is a microcosm of what the U.S. will face in the coming years.

As in the play by Samuel Beckett, those waiting for the “Bond Vigilantes” to arrive may just as well be waiting on Godot.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.