- Analysts cut profit expectations for S&P discretionary sector

- ‘Revenue estimates are tumbling’ on demand doubts, BI says

Analysts are growing increasingly doubtful that US consumer spending will hold up into next year, even as American shoppers continue to be surprisingly resilient despite lingering inflation and elevated borrowing costs.

Over the past 12 weeks, sell-side analysts have trimmed profit projections for the S&P 500 consumer discretionary sector through the third quarter of next year, according to Bloomberg Intelligence equity strategists Gina Martin Adams and Michael Casper. The cuts, which were primarily driven by slumping revenue estimates, were enough to push the expected pace of consumer discretionary earnings growth below the S&P 500 Index’s anticipated pace of earnings growth before the middle of 2024.

“While margin forecasts have held up well, revenue estimates are tumbling as the consensus doubts discretionary demand in the year ahead,” they wrote in a note to clients on Thursday.

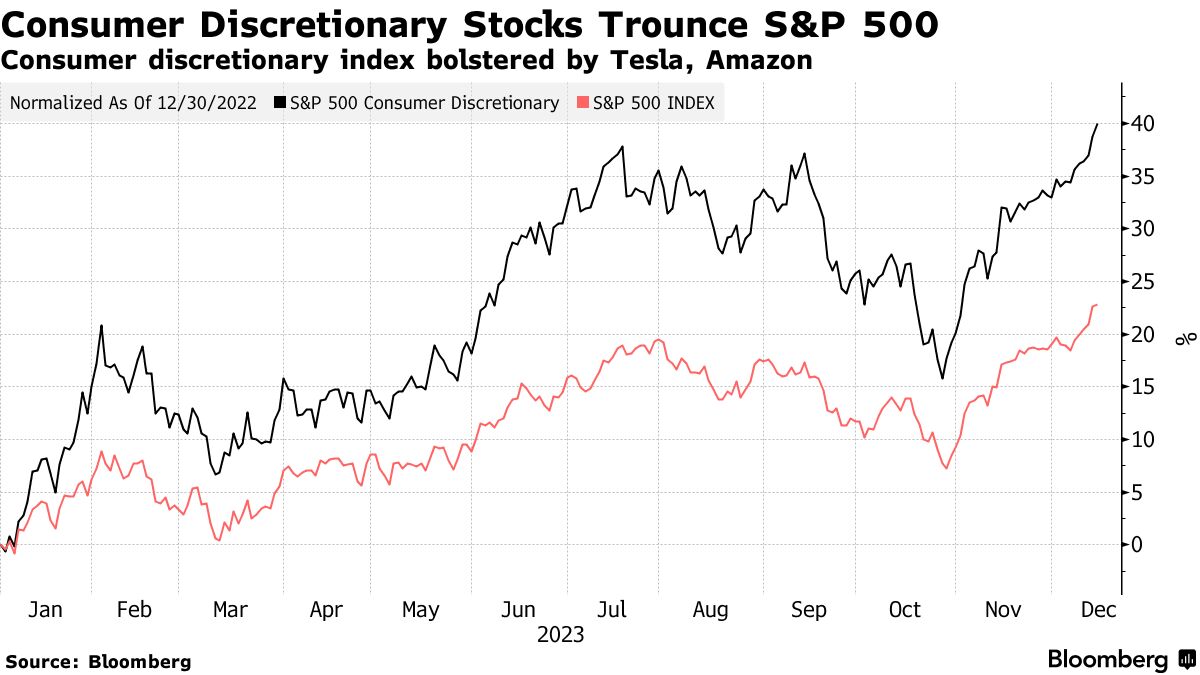

The S&P 500 Consumer Discretionary Index has soared 40% this year, almost twice the S&P 500’s 23% gain, though technology heavyweights Tesla Inc. and Amazon.com Inc. have powered much of the advance. Carnival Corp. and Nike Inc. will offer the latest read on consumer demand when they report earnings next week.

Consumer discretionary stocks extended their recent streak of gains on Thursday, trading around the highest level since April 2022, after Commerce Department data showed US retail sales unexpectedly picked up in November, pushing toward the highest level since April 2022. The index climbed the most in nearly a month on Wednesday, fueled by bets that the Federal Reserve will soon begin cutting interest rates, which would ease pressure on household budgets.

Strategists at Wells Fargo & Co. said the retail sales figures signal decent consumer strength for the holiday season. But they still expect some moderation in 2024 due to dwindling household savings, deteriorating credit conditions and signs of moderation in the labor market.

“While today’s data don’t necessarily paint a picture of a consumer that is about to lose its footing, we still anticipate some moderation to take hold as the calendar flips to 2024,” wrote economists Tim Quinlan and Shannon Seery Grein.

Michael Pearce, the lead US economist at Oxford Economics, cautioned that the November reading comes on the heels of a weak retail sales reading in October, meaning real consumption growth is still tracking lower in the fourth quarter than the previous period.

While the sell side has cut discretionary sector revenue projections for every industry, Hasbro Inc., VF Corp. and Tesla Inc. are seeing some of the steepest reductions over the next four quarters, according to Martin Adams and Casper. Meanwhile, Lennar Corp., Wynn Resorts Ltd. and AutoZone Inc. are among those that have seen the biggest boosts in expected fiscal-year revenue growth.

The mounting negativity signals that Wall Street has already priced in a fair bit of downside for much of the sector, calling into question how much of a hit individual stocks will take even if consumer demand weakens.

“Excluding Amazon and Tesla, the rest of discretionary is discounted,” Casper said. “The risk that analysts have cut too much is a possibility with valuations so low.”

Written by: Katrina Compoli and Carly Wanna — With assistance from Jess Menton @Bloomberg

The post “Wall Street Is Skeptical That Shoppers Can Keep Spending in 2024” first appeared on Bloomberg.com

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.