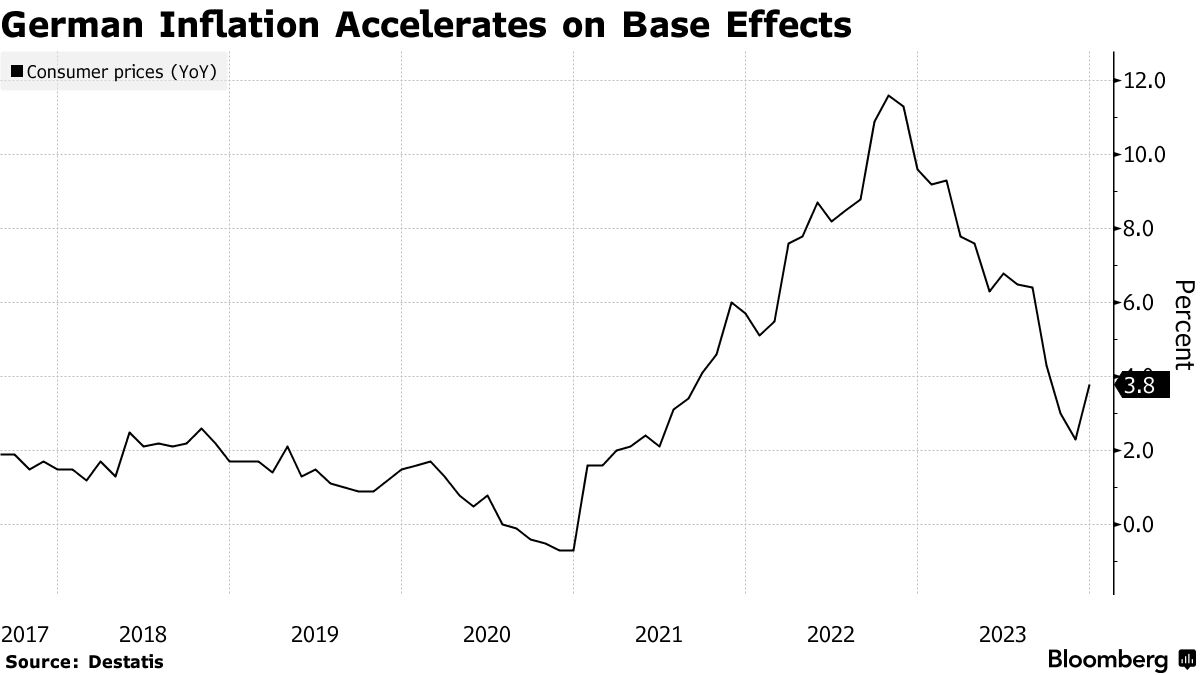

- Consumer prices rose 3.8% from year ago in December; est. 3.9%

- Surge largely due to one-time energy aid payments in late 2022

German inflation quickened less than anticipated in December — reflecting a more muted boost from energy that may help keep wage demands at bay and allow a faster return to the European Central Bank’s 2% target.

Consumer prices rose by an annual 3.8%, the statistics office said Thursday. That’s less than the 3.9% predicted by economists, though up from 2.3% in November. The reading for 2023 as a whole was 6%.

Last month’s surge is largely down to base effects: One-time state aid for natural gas and district heating bills depressed energy costs at the end of 2022, boosting inflation a year later. In recent months, though, prices for electricity, gas and fuels have sunk, with regional German data suggesting the trend continued in December.

Numbers earlier in the day from France showed a similar picture to that in Europe’s biggest economy as the withdrawal of government assistance helped push inflation up to 4.1% from 3.9%. Price gains in Ireland were also faster, while Spain last week reported them holding steady at 3.3%.

While euro-zone figures due Friday are set to show inflation bouncing back up to 3%, the slowdown that began in November 2022 is expected to resume as the year progresses.

What Bloomberg Economics Says…

“For the ECB, rising inflation in the euro area’s biggest economy is inconvenient, but the overall trend is down — we see the first rate cut in June, at the latest.”

—Martin Ademmer, economist. Click here for full REACT

The ECB remains cautious on inflation. President Christine Lagarde and her colleagues are carefully studying domestic drivers, particularly salaries. About half of workers covered under the ECB’s wage tracker will negotiate new deals in the first half of 2024, with the results key to determining the path for interest rates.

Money markets point to about six quarter-point reductions by year-end. But while even the Governing Council’s more hawkish members have conceded that rates won’t climb further — absent additional shocks — they’ve pushed back against the idea of cuts any time soon.

In a recent interview, Bundesbank President Joachim Nagel advised traders speculating on an imminent reduction in borrowing costs to be “careful” as “others have miscalculated before.”

A sluggish euro-area economy may aid the retreat in inflation, with the bloc likely to have endured a mild recession in the latter half of 2023 and Germany showing little indications of a strong rebound to follow.

The ECB’s most recent projections show inflation back at 2% in the second half of 2025. The Bundesbank doesn’t see Germany achieving that milestone before 2027. For this month, Bloomberg Economics’ nowcast points to an inflation reading of 3.1%.

“We had a clear message from Christine Lagarde at the last ECB meeting that domestic inflation pressures were a concern,” Sarah Hewin, head of Europe and Americas Research at Standard Chartered, said before the German data were released.

“Ultimately we think that by the second quarter and the next set of forecasts that we get for June, they’ll be signaling clearly that there’ll be inflation on target over their time horizon,” she told Bloomberg TV. “Possibly they get there a little bit earlier, but we do see a more cautious approach from the ECB. So we think second-quarter rate cuts.”

Written by: Jana Randow — With assistance from Kristian Siedenburg, Joel Rinneby, William Horobin, Tom Keene, Jonathan Ferro, Lisa Abramowicz, James Hirai, and Andrej Sokol @Bloomberg

The post “German Inflation Jumps Less Than Expected in Boost for ECB” first appeared on Bloomberg.com

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.