NYCB was downgraded to junk by Moody’s, PBB and Aareal saw bonds plummet on their US CRE exposure

Second Chapter

The collapse of Credit Suisse in March 2023 seemingly marked the nadir of a flash banking crisis that began only a few weeks earlier with the downfall of Silicon Valley Bank and Signature Bank in the US. But what looked like a momentary blip that authorities on both sides of the Atlantic had managed to contain is now increasingly looking like the opening chapter of a much longer saga.

This time the focus is on commercial real estate debt. The loan books of lenders from New York to Munich are showing rising levels of stress because of a slump in property values, triggered by a mix of interest rates hikes over the last two years and the shift to remote working.

New York Community Bancorp, which had acquired part of Signature Bank in 2023, was the first to rattle markets when it announced a surprise loss tied to its credit book last week. Even if its commercial real estate portfolio is relatively small, its rating has now been downgraded to junk by Moody’s and the bank is looking to shed risk on a $5 billion mortgage portfolio.

In Japan, Aozora Bank recorded its first loss in 15 years due to bad loans in US commercial property.

Alarm bells are now ringing in Europe, with the ECB signaling to lenders that they may face higher capital requirements if they fail to grasp the risks they face from commercial real estate.

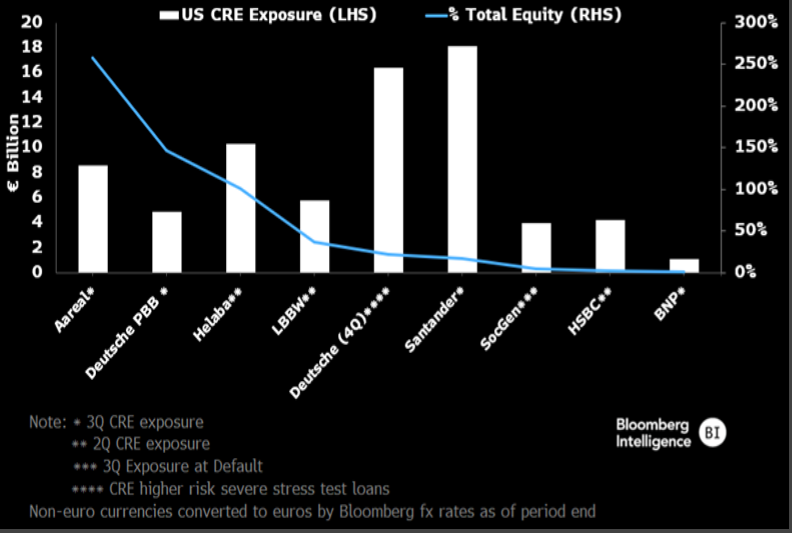

“You’ve got more banks that are coming under scrutiny, more banks falling casualty, and potentially some banks defaulting on both sides of the Atlantic,” said Jonathan Golan, a portfolio manager at Man Group. In Germany and Scandinavia there are banks with a large exposure to commercial real estate, and if they take a 15-cent writedown for every dollar they lend “not only are these banks not investment grade, they’re insolvent.”

Deutsche Bank bolstered provisions for its US commercial real estate portfolio, but it’s smaller banks that are hurting the most. Deutsche Pfandbriefbank, a Bavarian lender specializing in commercial real estate finance with a large exposure to the US, saw its bonds collapse this week after Morgan Stanley held a call with clients recommending they sell PBB’s senior notes.

Its tier 2 bonds lost about a third of their value this week and are now trading at less than 50 cents on the euro. The sudden drop forced the bank to issue an unscheduled statement that it had increased provisions and described the turmoil as the “greatest real estate crisis since the financial crisis.”

Bonds issued by Aareal Bank, another German specialized bank, and LBBW, which acquired a Berlin-based lender in 2022 with large exposure to German developers, also sank.

“In 2023, most banks were not willing to take a haircut,” said Anke Johann, a partner at law firm Goodwin Procter in Munich. “This strategy of amend and extend will likely end in 2024.”

Notes From the Brink

Amid the turmoil in the property market, real estate investment trust Office Properties Income Trust managed to sell a $300 million bond to repay debt coming due later this year, Sri Taylor and Gowri Gurumurthy report.

The move was a bold one — the firm saw its credit rating cut deeper into junk just a day before tapping the market — and it paid out to extinguish upcoming debt. It sold the new 9% bond at a discount to yield nearly 10.7%. It’s using proceeds from the sale to help repay notes with a 4.25% coupon.

REITs that are heavily exposed to commercial real estate are feeling the pain of the latest property jitters. The KKR Real Estate Finance Trust earlier this week lowered its dividend by nearly half after realizing a $59 million loss on an office loan. Its shares sunk, falling by the most since March 2020 on Wednesday, and deepening losses through Friday.

Amid rising interest rates, properties will have to be refinanced at higher prices when their debt comes due. More than $1 trillion in commercial mortgage loans are maturing over the next two years, at a time when valuations for assets like office buildings have dropped.

The Latest on… Cevdet Caner

In a London court this week, more junior-ranking creditors opposed a planned debt restructuring of a major Berlin development of Aggregate Holdings, the real estate investment company run by Cevdet Caner. These creditors, which are considered out-of-the-money, would be all but wiped out.

A footnote in the restructuring plan made them balk: the proposal includes a consultancy agreement with a firm some creditors contend is owned solely by Caner. Company filings show the firm, NIU Real Estate GmbH, is indirectly owned by an entity of which Caner was the sole shareholder when it was registered in Luxembourg in 2022.

The consultancy agreement includes a €300,000 monthly fee for its services, and also instruments that entitle the firm to a cut of potential profits after debt is repaid, according to court documents.

“There can be no possible justification for this payment,” lawyers for Bank J Safra Sarasin, which is representing some investors opposing the restructuring plan, said in a filing. Safra has created its own alternative arrangement, which would be undertaken in Luxembourg.

The majority of senior creditors, including London-based fund Fidera, support the plan. A London judge said he would aim to provide a judgment on the case in around three weeks.

High Alert

- Genesis Global has settled a lawsuit brought by New York’s top law enforcement official alleging the bankrupt crypto lender defrauded customers of its now-terminated Gemini Earn program, which was run jointly with Gemini Trust.

- Retail investors are pulling more than €1 billion a month from real estate funds in Europe. The redemptions meant total net assets held by European open-ended and exchange-traded property funds fell more than 10% to €180.7 billion from December 2022 through the end of last year, data compiled by Morningstar show.

- KKR and Macquarie are among suitors that have been shortlisted in the bidding for French fiber company XpFibre, part of Altice France. The company’s bonds jumped on Friday.

- Kenya’s eurobonds maturing in June surged after the East African nation offered to buy back its $2 billion of debt and announced plans to sell new securities.

- The number of distressed charter schools rose to a record in the beginning of 2024 as the sector struggles with the end of pandemic assistance and rising costs.

By the Numbers

Investors are expressing newfound optimism toward US budget carrier Spirit Airlines after the company reported a smaller-than-expected loss and gave an upbeat revenue projection for this quarter, Alicia Clanton reports.

The company said it expects its revenue to range from $1.25 billion to $1.28 billion this quarter, more than the $1.22 billion predicted by analysts. It also said it has the cash it needs to survive without combining with JetBlue Airlines.

Spirit’s 8% bonds jumped 4.75 cents on the dollar to 72 cents following the earnings announcement, and advanced further on Friday. Meanwhile, the company and a group of bondholders have organized with advisers ahead of anticipated debt talks. The 8% bondholders are working with Akin Gump Strauss Hauer & Feld, while Spirit has tapped Perella Weinberg Partners and Davis Polk & Wardwell.

Spirit Chief Financial Officer Scott Haralson said on a call to discuss quarterly results that “the company is aware of its 2025 and 2026 debt maturities and is assessing options to address those maturities when the time is appropriate.”

More from the Terminal and Bloomberg Law

- London House on Sale for $34 Million After Bankruptcy of Emirati

- Children’s Place Hires Centerview to Help Bolster Cash Reserves

- Silver Point, Bracebridge Back McDermott Restructuring Overseas

- China Developer to Sell London Project for HK$1 Plus Dollar Debt

- Hedge Fund Seeks Early Redemption of SBB Bonds in UK Court Claim

- Intrum Offers to Buy Back Bonds as Prices Fall Into Distress

- Subscribe here to our Americas, EMEA and APAC distressed debt channels on the Terminal

Written by: Luca Casiraghi and Libby Cherry — With assistance from Tasos Vossos, Giulia Morpurgo, Greg Ritchie, Carmen Arroyo, Matthew Monks, Sri Taylor, Gowri Gurumurthy, Alicia Clanton, and Nicholas Comfort @Bloomberg

The post “The ‘Greatest Real Estate Crisis’ Since 2008 Starts to Hit Banks” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.