- Galicia, Mariva and AdCap recommend unwinding positions

- Monthly CPI seen falling below 10% by mid-year on Milei plan

Banks and funds in Argentina are telling clients to ease off short-term bonds with interest payments linked to inflation as early signs fuel market optimism about President Javier Milei’s pledge to crush runaway price increases.

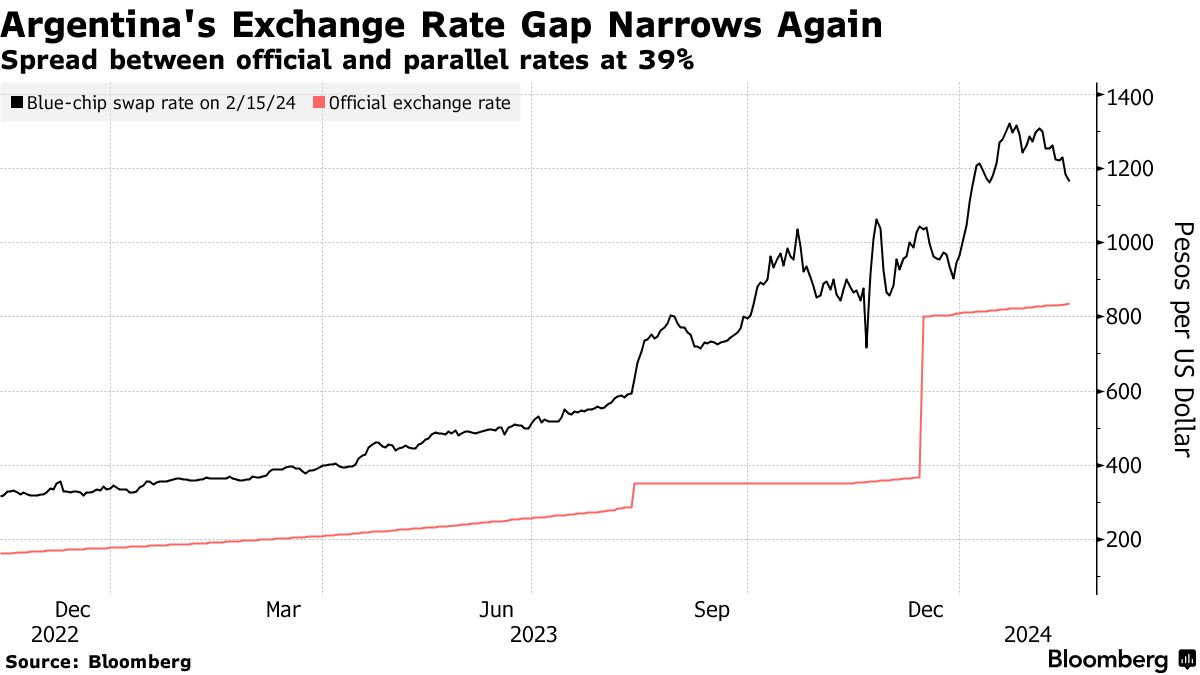

Recession forecasts and a shrinking amount of money in circulation, as well as a narrowing gap between Argentina’s exchange rates and cooling inflation expectations, are driving investors to ease off inflation bonds that until recently became a popular investment to shield peso portfolios from triple-digit price hikes.

“The inflation decline is much faster than we expected and this forces a portfolio rebalancing,” said Mariano Calviello, head portfolio manager at Fima, the investment wing of Banco Galicia, which is the main holder of inflation-linked bonds, according to data compiled by Bloomberg. “The inflation-linked bonds have to readjust to this new reality.”

Argentina has been reporting lower-than-expected inflation for two months now, albeit still at crisis levels. Cumulative price increases in Milei’s first two months were 51.3% versus the 57.3% forecast in a Bloomberg survey. The new president anticipates data could surprise again in February, with gains of around 15% monthly, against market expectations of 18%.

“The short end of the inflation-linked curve has lost attractiveness,” Juan Carlos Barboza, chief economist at Buenos Aires-based Banco Mariva, said in a note to clients, referring to the inflation-adjusted bond coefficient. “Inflation data has been surprisingly downward and bond prices continue to remain strong.”

Besides Galicia and Mariva, AdCap Securities and local broker Neix have also told clients in Argentina to sell or take profits of CPI-linked bonds.

To be sure, Milei’s economic plan faces steep challenges on inflation and history has repeatedly shown that early investor hopes in Argentina later get dashed by the crisis-prone country. For example, market optimism imploded in 2019 after former President Mauricio Macri lost a primary election, ending his business-friendly agenda after Argentina’s inflation rate doubled in his final two years. A litany of factors — labor unions, utility bills, transport costs, education — could push inflation higher again in the coming months.

And not all investors are shifting strategy. Brokers Balanz Capital and TPCG Valores also see inflation cooling, but are not advising clients against inflation-linked notes because short term fixed rates and FX-linked bonds still provide worse returns.

Until recently, investors were comfortable positioning themselves in inflation-linked bonds with annual price gains topping 250%. Demand for this hedge was so high that the bonds offered a negative real interest rate. But economists surveyed by Argentina’s central bank last month expect monthly inflation to gradually cool from 21% last month to 8% in June.

“We recommend taking some profits in CPI-linked bonds and dollarizing part of the portfolio with more conservative bonds,” such as dual bonds, said Javier Casabal, a strategist at AdCap, another major investor of inflation-linked securities. “There is a flood of news showing an enormous conviction that everything is going in the same direction of lowering inflation, in whatever way.”

High-frequency inflation data shows monthly price hikes cooling, while the peso’s parallel exchange rate strengthened about 11% in the last 30 days to 1,100 per US dollar, diminishing the need for another sharp move. Consumer spending plummeted in December after Milei devalued the official peso rate 54% overnight and lifted years of price controls, cementing recession forecasts for 2024.

“Recession, adjustment of relative prices and zero deficit is what is needed for inflation to come down in Argentina. Milei is playing right into that,” said Alberto Bernal, chief strategist at XP Investments in Miami.

Written by: Ignacio Olivera Doll @Bloomberg

The post “Argentina Banks Warn Against Inflation Bonds as Price Hikes Cool” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.