- Chinese consumers and central banks have bolstered gold market

- Timing of Fed pivot to cutting rates remains key gold driver

This week’s gold rush may have been triggered by bets on the US Federal Reserve’s long-anticipated pivot to looser monetary policy, but the foundations for the record rally were laid in China.

After months of mostly treading water, the gold market suddenly sprang to life last Friday. Prices breached December’s record on Tuesday and have jumped to successive daily highs ever since.

The rally itself was peculiar: gold tends to spike in response to globe-shaking geopolitical or economic developments, and nothing particularly noteworthy had happened to justify the surge. The sharp climb higher has left many analysts and other market watchers casting around for explanations, from big investment funds taking a renewed interest in gold, to the role of algorithmic traders that follow momentum in the market, fueling volatility.

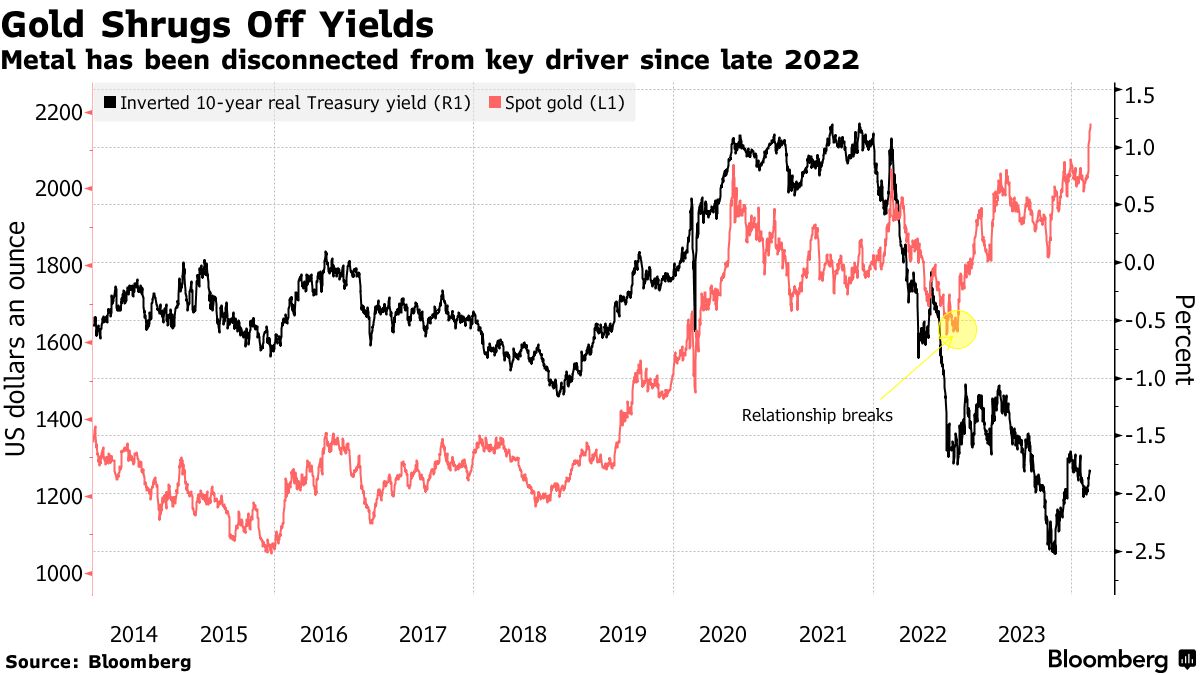

But the reality is that prices didn’t actually have that far to go before hitting record territory. Gold has been trading for months around the $2,000 mark — a level that would have been viewed as stratospheric just a few years ago, and which was only breached for the first time in 2020 as the global pandemic raged. Even more unusually, prices have traded at such elevated levels despite sky-high real interest rates that are typically bad for gold, which doesn’t pay interest.

Why were prices so high in the first place? That’s where China comes in.

While many western investors did indeed dump gold holdings as rates soared last year, global demand was underpinned instead by massive purchases by central banks in emerging market countries, led by China. And regular people are buying too — consumers in China have been stocking up on coins, bars and jewelry despite the high prices, to protect their wealth against turmoil in the country’s stock market and property sector.

“The gold market hasn’t been driven by western investors,” said Bernard Dahdah, a commodity analyst at Natixis. “China, so far this year and through last year has been the engine behind gold prices — but not necessarily behind this spike.”

While Chinese and other emerging market buying helped set the stage for this week’s records, the focus has turned to investors and their bets on when the Fed will start cutting interest rates. The initial leap higher on March 1 came after disappointing US factory data and a drop in consumer sentiment appeared to bolster the case for cutting. Fed Chairman Jerome Powell’s comments reiterating the likelihood of a cut this year drove further gains, helping to propel prices to fresh records.

In the latest sign of funds having helped supercharge the recent rally, fresh data out Friday from the Commodity Futures Trading Commission showed that money managers were buying strongly in the week through March 5 — the day when gold jumped through its previous record.

Still, bullion has far to go to reach its inflation-adjusted peaks set more than a decade ago. Gold has risen more than 600% since the turn of the millennium, though adjusted for inflation it remains below the high of $850 touched in January 1980, equivalent to more than $3,000 in today’s dollars.

This week’s high offers some echoes with that peak 44 years ago. In 1979, bullion more than doubled in value as the overthrow of the Shah in Iran and the Soviet invasion of Afghanistan highlighted the precious metal’s role as a haven asset. This year, attacks by Iran-backed Houthis on Red Sea shipping and Russia’s grinding war in Ukraine are raising geopolitical risks.

“The sabre-rattling from Putin, conflict in Ukraine and Gaza, all of that adds to the background noise,” said Adrian Ash, director of research at BullionVault. “The mood music is bullish for gold now from the safe haven perspective.”

But recent gains have still been relatively modest compared with some record-notching rallies of the past. That’s partly because prices were already elevated thanks to buying by central banks seeking to diversify their reserves away from a dependency on the dollar.

Central bank demand “puts a buffer on gold,” said Max Belmont, a portfolio manager on the First Eagle Gold Fund, which had $2.3 billion in assets under management at the end of 2023. “And it’s not the western central banks that are accumulating, it’s the eastern,” with China the largest buyer in 2023, he said.

If Chinese buying has been a pillar of the gold market, Fed policy is likely to remain the key market mover. Signs that a pivot is getting closer have supported gold since mid-February, with traders now pricing in 67% chance of a rate cut in June, a higher probability than early last month. Lower borrowing costs are typically positive for gold, which doesn’t offer the holder any interest.

That means US data, including the latest inflation figures due Tuesday, will be closely watched.

In the short term, some investors may choose to cash in their recent profits, which would weigh on prices, said BullionVault’s Ash.

But overall, the backdrop means the rally could have further to go. And despite the many parallels between the latest record-breaking run and previous gold peaks, the role played by central banks and Asian buying sets it apart.

“The current market behavior, characterized by daily record highs, is unprecedented in my experience,” said Alexander Zumpfe, senior trader at German gold refiner Heraeus Group. “This uniqueness underscores the complexity of the current market dynamics and the variety of factors influencing gold prices.”

Written by: Yvonne Yue Li and Jack Ryan — With assistance from David Marino and Eddie Spence @Bloomberg

The post “Chinese Buying Set the Stage for Gold’s Latest Record Run” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.