- Core PCE picked up in March when drawn to two decimal places

- Compounding effects are large for year-over-year figures

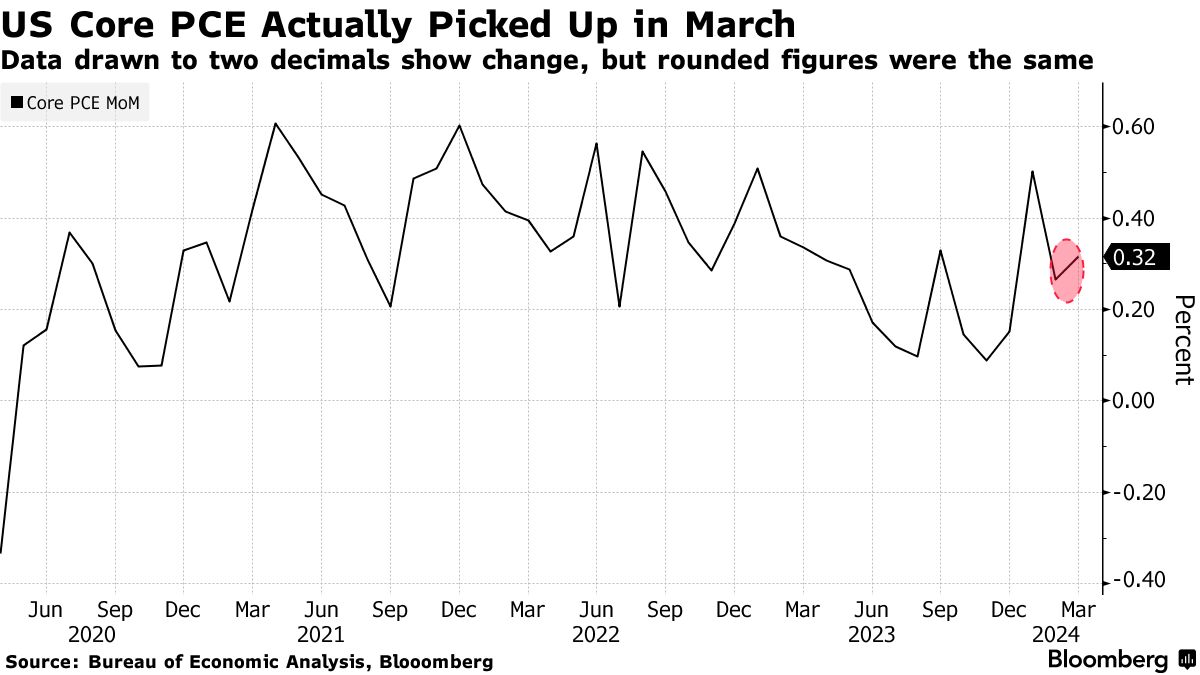

To the naked eye, a key US inflation metric held steady in March. But look a little closer at two or three decimal places and you’ll see that it actually picked up.

The difference matters because the personal consumption expenditures price index is an inflation gauge favored by Federal Reserve policymakers — one that ultimately will shape their views on when to cut interest rates.

The core PCE, which excludes food and energy costs, came in at 0.3% for a second month in March, according to Bureau of Economic Analysis data rounded to one decimal. Digging a little deeper, the pace accelerated to 0.32% from 0.27%, and both January and February figures were revised higher.

The difference may look minor on a monthly basis, but the implications for annualized rates — which the Fed targets — are much greater. For example, monthly gains of 0.25% and 0.34% are both rounded to 0.3%. But over 12 months, the two rates would produce inflation of 3.04% and 4.16%, respectively.

Those annualized figures would have significantly different implications for monetary policy, and especially now, said EY Chief Economist Gregory Daco.

“The Fed is so data dependent, arguably excessively focused on making policy on a play-by-play basis, that the nature of any report is excessively interpreted, just based on the headline figure,” he said. “The increased focus on every single data release makes it that much more important to know what the data is showing and the direction of travel for inflation.”

Recent data have indicated that inflation is moving sideways at best, or possibly rearing back up again. The core PCE figure on an annual basis rose 2.8% for a second month in March.

But a report Thursday showed that core PCE in the first quarter jumped to 3.7% from 2% in the prior period. That was higher than economists forecast and sent Treasuries plunging as traders pushed out bets for a cut in interest rates even further. When the March data came as expected, Treasuries rebounded somewhat.

Economists didn’t always scrutinize the inflation prints to this degree, said Chris Low, chief economist at FHN Financial, who’s been in this line of work for 35 years. He and his colleagues started forecasting PCE as well as the consumer price index — another closely watched inflation gauge — to two decimal places in late 2022, which he says was the first time the CPI data became more important than the jobs report.

While the Fed bases its inflation target on the PCE data, the CPI is also important because it comes out a few weeks earlier and is linked to Treasury Inflation-Protected Securities, or TIPS. That means it’s more important to read CPI out to three decimal points, whereas PCE “can probably get away with two,” said Omair Sharif, founder of Inflation Insights LLC.

“I don’t wake up for anything under three decimal spots,” said Sharif, adding he’s been estimating inflation to that degree for at least a decade, if not longer. “That makes a big difference for how you view the forecasts and the risks around the forecasts.”

Low says the focus on decimals was prompted by follow-up questions from traders who wondered how one month’s reading compared to the prior print. That information is crucial at a time like now, when the expected timing of the Fed’s first interest-rate cut is changing seemingly every day.

“It’s not enough to tell them that inflation is high or inflation is low — they need to know what the momentum is doing,” Low said. “If you don’t go to two decimal places, frequently you can’t tell.”

Written by: Molly Smith and Christopher Condon @Bloomberg

The post “Squint Your Eyes and US Inflation Data Actually Looks Worse” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.