Economic growth in the US is still good, but it has shown some deterioration of late. GDP growth in the third quarter of 2018 was up 3.5% q/q, off from the 4.2% advance recorded in Q2. The increase in real GDP reflected contributions from personal consumption expenditures, private inventory investment and local government spending. Non-residential investment also added to GDP growth.

The GDP deflator in the third quarter increased to 110.65 index points from 110.27 index points in the second quarter of 2018, or by 0.3%. Inflation, therefore, remains very subdued despite strong growth.

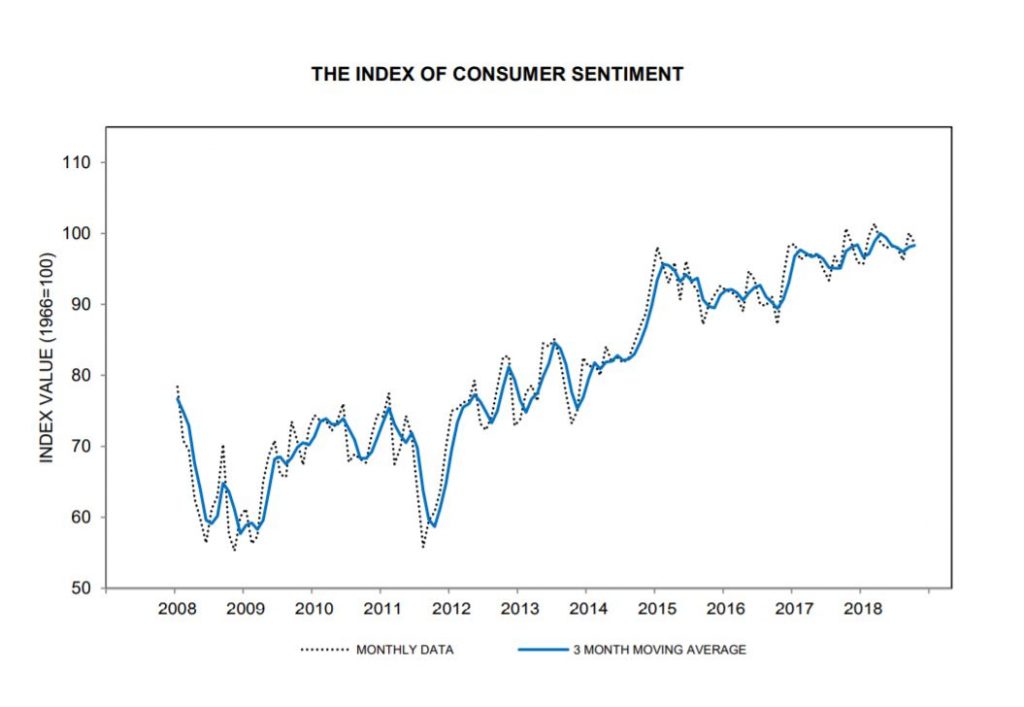

GDP growth, as reported by the government, narrowed slightly and the University of Michigan consumer sentiment index for October declined to 98.6 from 100.1. The two indicators together clearly point to a slowdown in the economy. How deep the downturn will be is still hard to say, but the stock market’s sharp declines in the past few weeks does not bode well for the economy.

The decline in home sales, both new houses and pre-owned ones, has certainly contributed to the weaker GDP growth. This trend is unlikely to reverse soon, which means that GDP growth in Q4 will be just as weak as it has been in Q3. Adding to the softer economy could be the Fed’s decision November 6-7 to boost interest rates by a quarter point.