Kevin Wilson recently penned a piece for Seeking Alpha that made a great point about where the markets are currently. To wit:

“Famous market observer Art Cashin mentioned a metaphor in October 2017 that resonated with me. He said (words to the effect that) at that moment, market players had only the protection provided by pictures of lifeboats, not the lifeboats themselves. This is just like the Titanic, whose measly 16 lifeboats looked nice, but left many hundreds on board with no means of escape when the ship sank. That is the current market situation in a nutshell. Players seem to believe that their positions are diversified enough to protect them in a downturn, and in any case, many appear to expect no major drawdown in spite of many months of extreme volatility. I would argue that the risk is far greater than perceived by many, and the protections most have in place are quite inadequate.”

Indeed, that is the case. As I noted in this past weekend’s newsletter, while the S&P 500 has declined only marginally for 2018, the devastation across markets has been dramatically worse.

In other words, traditional diversification, which is considered the “defacto” portfolio protection strategy by the mainstream media, has not worked.

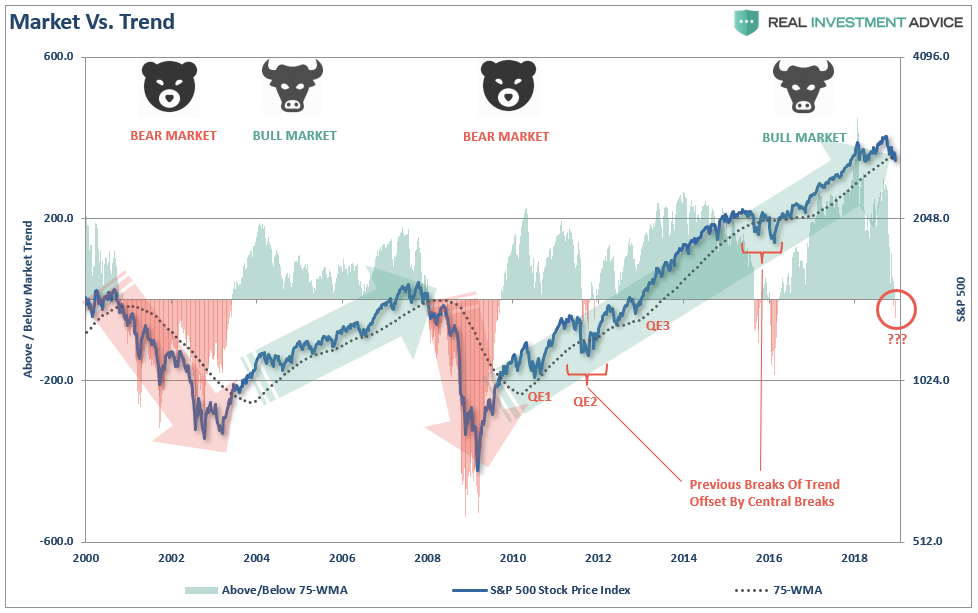

Over the last several weeks, I have been discussing the transition of the market from “bullish” to “bearish.”

“The difference between a ‘bull market’ and a ‘bear market’ is when the deviations begin to occur BELOW the long-term moving average on a consistent basis.”

“For only the third time in the last decade, the market has now slipped below that longer-term trend.

The difference, this time, is there are no Central Banks talking about coming to the markets rescue – at least not yet.

Currently, it is still too early to know for sure whether this is just a ‘correction’ or a ‘change in the trend’ of the market. As I noted previously, there are substantial differences which suggest a more cautious outlook. To wit:

- Downside Risk Dwarfs Upside Reward.

- Global Growth Is Less Synchronized

- Market Structure Is One-Sided and Worrisome.

- Higher Interest Rates Make It Hard for the Private and Public Sectors to Service Debt

- Trade Tensions With China Are Intensifying

- Any Semblance of Fiscal Responsibility Has Been Thrown Out the Window

- Peak Buybacks.

- China, Europe, and the Emerging Market Economic Data All Signal a Slowdown

- The Democrats won control of the House in the Mid-term elections which will effectively nullify fiscal policy agenda moving forward.

- The leadership of the market (FAANG) has faltered.

Here is the important point.

Understanding that a change is occurring, and reacting to it, is what is important. The reason so many investors ‘get trapped’ in bear markets is that by the time they realize what is happening, it has been far too late to do anything about it.”

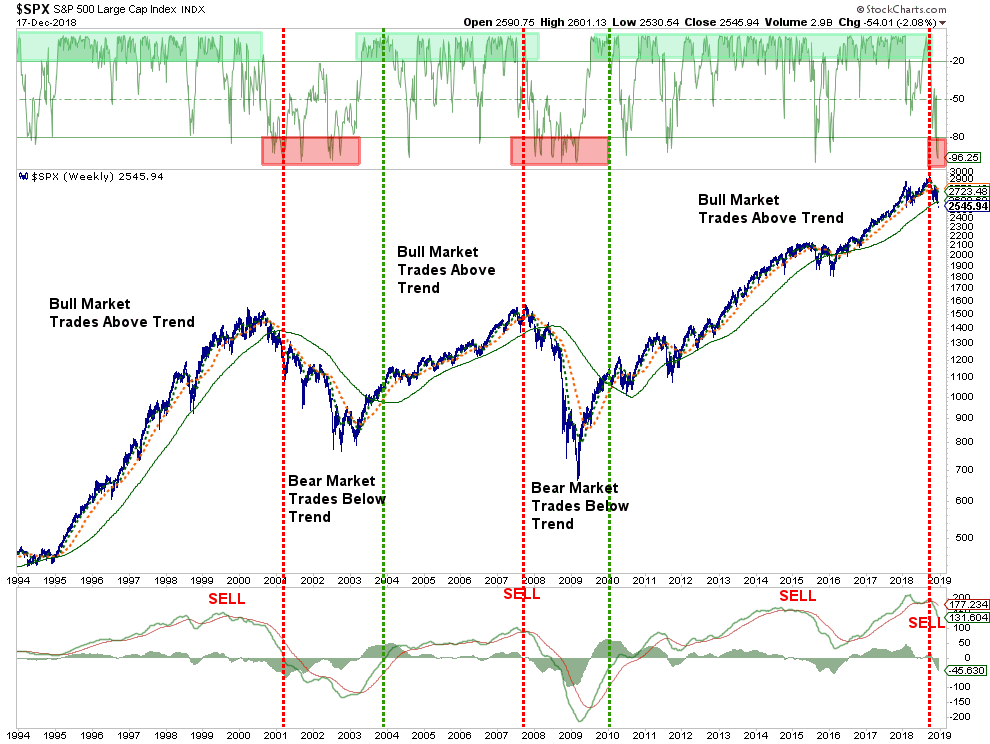

More importantly, as I have shown previously, the long-term technical backdrop has now substantially eroded. John Murphy at Stockcharts.com had an important note on this:

“There’s a reason why every short-term rally attempt over the past couple of months has failed. That’s because longer-range indicators have turned bearish and remain so. It’s more difficult for bounces on daily charts to get very far when the trends on weekly and monthly charts have turned down.”

He is absolutely correct and today we are going to go through some of the longer-term charts to show the risk currently at hand.

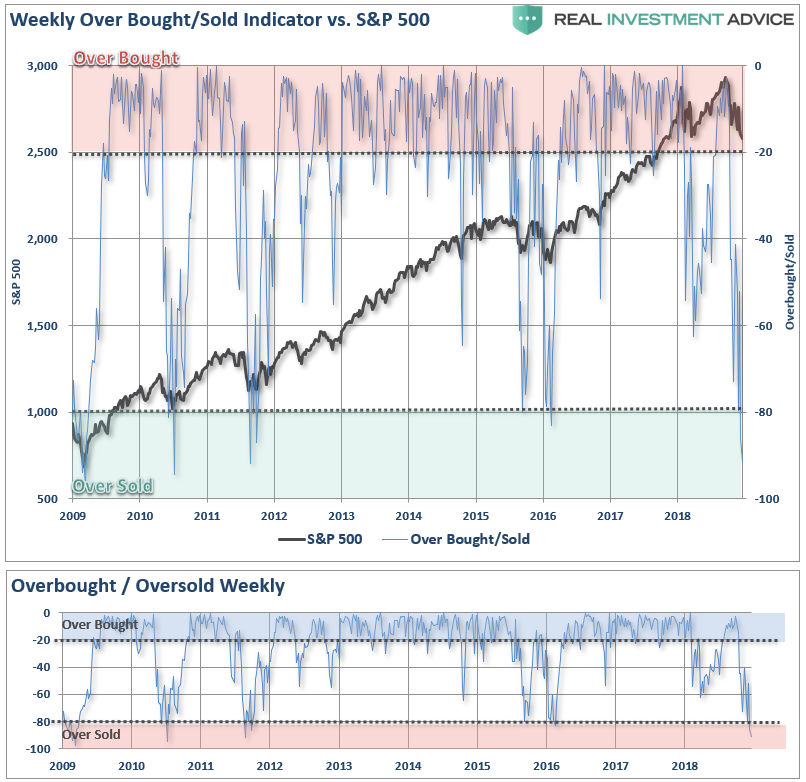

On a weekly basis, the market is clearly oversold and, historically speaking, such conditions have led to reflexive bounces.

However, it is important to note the difference between “bull” and “bear” markets.

During bull markets, markets trade above their longer-term moving averages and can remain overbought for extended periods of time. During “bear” markets, the opposite is true as markets tend to trade below their long-term means and remain oversold.

So, while it is very likely the current oversold condition will lead to a short-term bounce, it is likely an opportunity to reduce risk into.

John also highlighted similar concerns in his missive as well:

“Chart 1 plots weekly price bars for the SPX since the start of 2016 when the last ‘up-leg’ of its nearly ten-year bull market started. And the chart strongly suggests that the nearly three-year rally has ended. First of all, the rising trendline starting in early 2016 was broken during October. That previous support line has acted as a resistance line above short-term rallies since then. That’s a negative sign.

The SPX is now headed down for a retest of its early 2018 lows. That will be a major test of the market’s uptrend. Because a decisive close below that previous low would confirm that stocks are in the early stages of a bear market. In addition, the blue 10-week moving average crossed below the red 40-week average this month (called a “death cross”) which is another bearish sign. [A TV anchor on FOX Business this week referred to the death cross as “gobbledygook”, which says a lot about the quality of its reporting]. Even stronger bearish signals are clearly seen on the weekly RSI and MACD lines.”

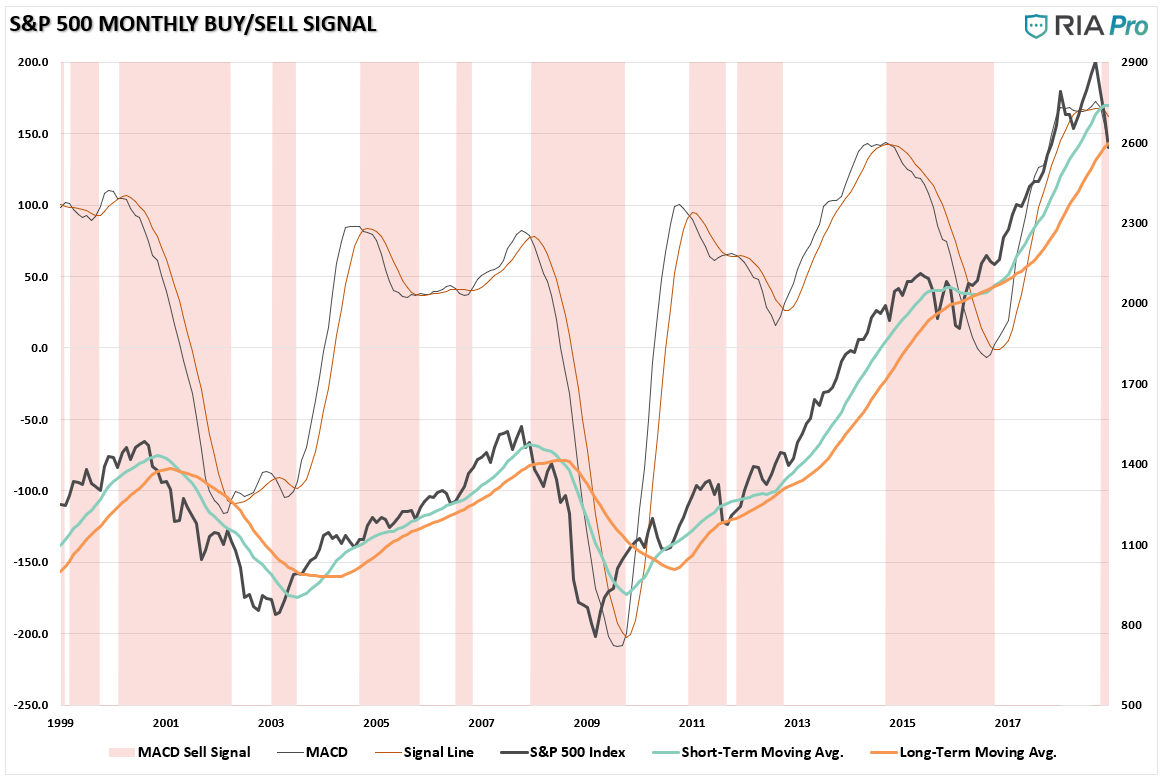

Most importantly, the long-term weekly sell signals have turned negative as well. This combined signals are rare in nature and historically have been worth paying attention to.

The Bear Growls

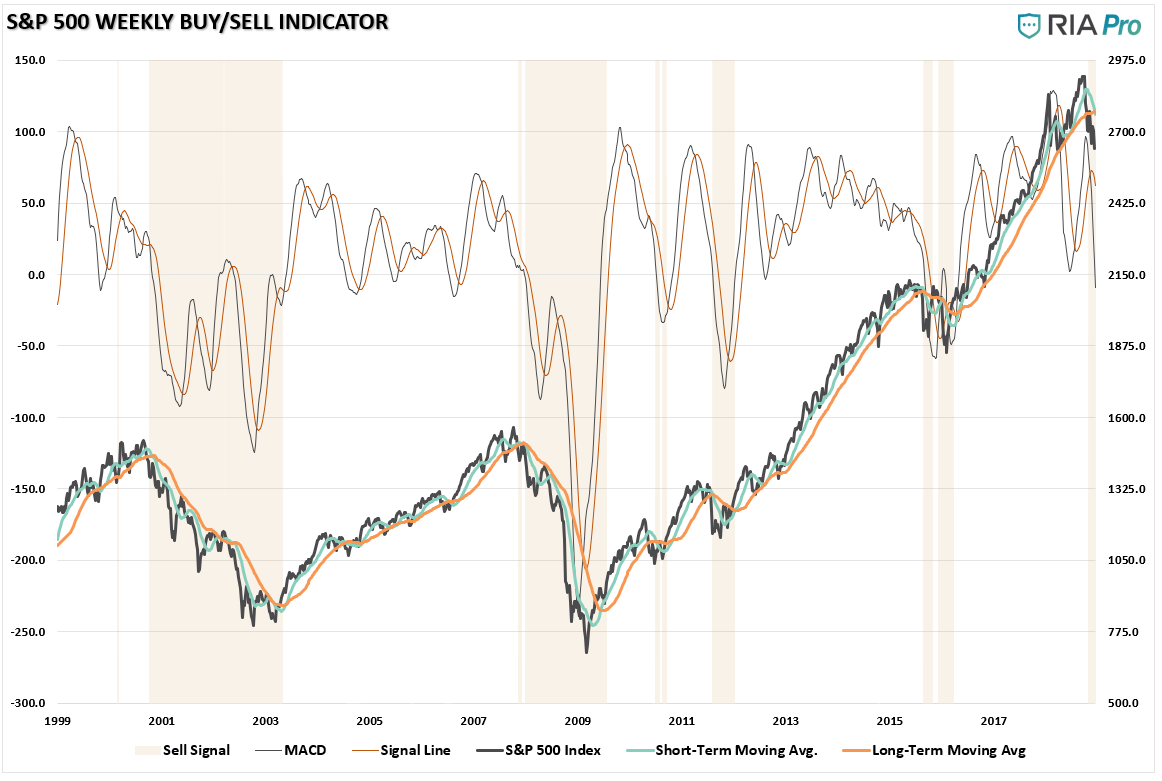

On a monthly basis, the data is also suggesting that a “bear” may indeed be stalking investors.

IMPORTANT NOTE: While we are discussing these technical issues today, monthly signals are ONLY VALID on the first day of the following month. So, if the markets were able to rally to all-time highs before the end of December, these signals would all be potentially reversed.

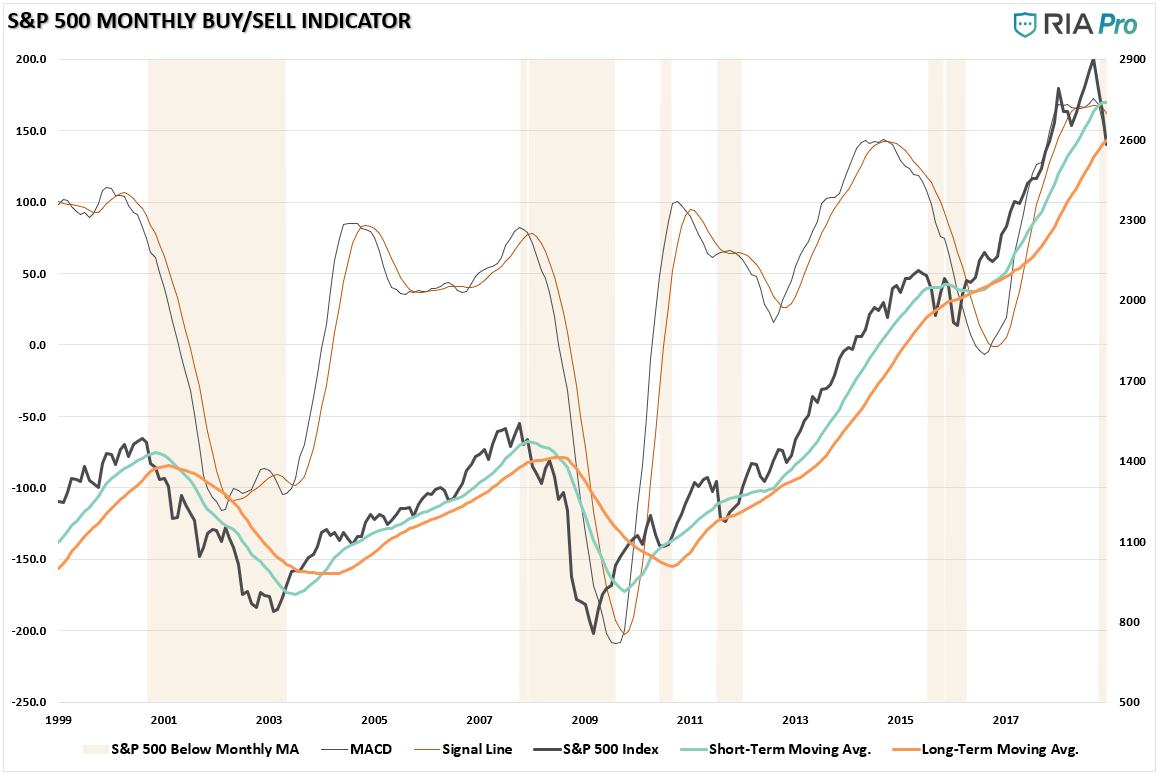

Of the monthly signals we follow, the shorter-term signals have all recently crossed back into “alert” territory suggesting the pressure on stocks remains lower for now. However, as shown, given this is a short-term signal, it issues alerts which do not always indicate the beginning of a bear market.

However, once we move to the longer-term indicator, the picture becomes substantially clearer.

There are two very important points to take away from the chart above.

- The long-term monthly signal has been triggered which suggests risk should be substantially reduced, and;

- The market has violated the long-term moving average which has only occurred 3-times previously: 2000, 2007, and 2015.

As John concluded in his article as well:

“That’s because a bull market usually has three ‘up-legs,’ and it’s just completed the third one.”

The Biggest Threat To The Bull Market

“Mike ‘Wags’ Wagner: ‘You studied the Flash Crash of 2010 and you know that Quant is another word for wild f***ing guess with math.’

Taylor Mason: ‘Quant is another word for systemized ordered thinking represented in an algorithmic approach to trading.’

Mike ‘Wags’ Wagner: ‘Just remember Billy Beane never won a World Series .’

– Billions, A Generation Too Late

While Billions is a hugely entertaining show, especially if you are in the business, the writers pull storylines straight from real life. As JP Morgan previously noted:

“Quantitative investing based on computer formulas and trading by machines directly are leaving the traditional stock picker in the dust and now dominating the equity markets.

While fundamental narratives explaining the price action abound, the majority of equity investors today don’t buy or sell stocks based on stock specific fundamentals. Fundamental discretionary traders’ account for only about 10 percent of trading volume in stocks. Passive and quantitative investing accounts for about 60 percent, more than double the share a decade ago.”

Herein lies the single biggest threat to the bull market.

As long as the algorithms are all trading in a positive direction, there is little to worry about. Algo’s were not a predominant part of the market prior to 2008 and, so far, they have behaved themselves by continually “buying the dips.” That support has kept investors complacent and has built the inherent belief “this time is different.”

But what happens when these algo’s reverse course and rather than “buying the f***ing dip,” they begin to “sell the f***ing rallies” instead?

It may have already started.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.