With the year 2018 in the books, we know the S&P 500, including dividends, has produced a meager 4.86% annualized return from the year 2000. That return has beaten inflation, but I call it meager because it’s not the 10% or so that many stock brokers, financial advisors, and market historians have taught much of the public to expect for such a long period of time. The return is way below its long term average, even if our starting point is a bit arbitrary and convenient (the start of the technology stock meltdown).

But there is another lesson to be learned from the past 19 years besides subpar annualized returns. The fact is those returns are radically bifurcated or back-loaded. In other words, they have accumulated recently or in the second half of the nearly two-decade period, not the first. And that means people in the age range of, say, 45-55, who have been investing by contributing steadily to work-sponsored savings plans like 401(k)s and 403(b)s for the past couple of decades, have been the beneficiaries of an amazing sequence of returns. It also means they may be unprepared for a less beneficial sequence in the future.

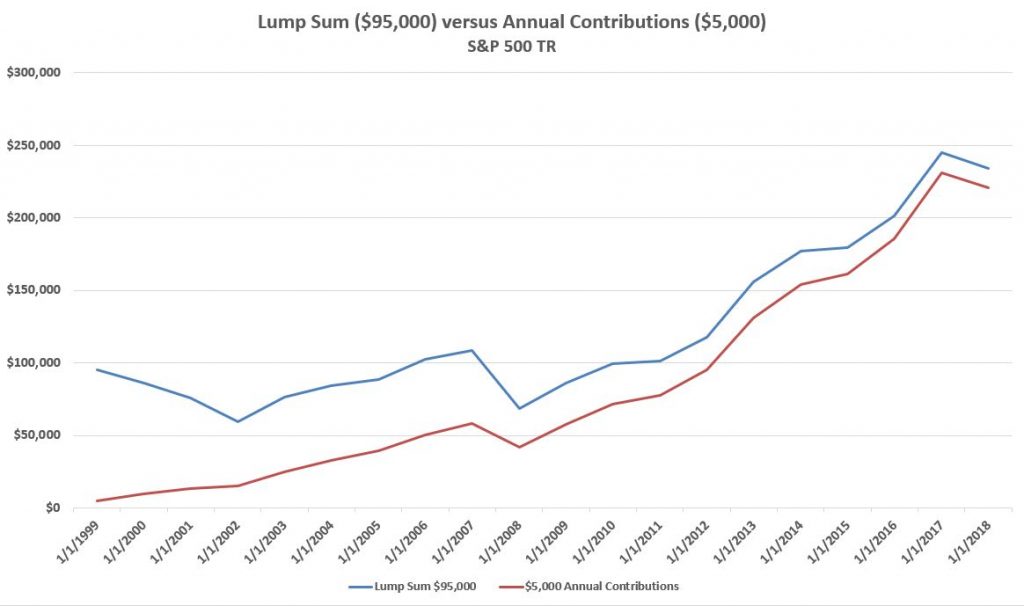

A way to illustrate this point is to compare a $95,000 lump sum investment in the S&P 500 TR Index in 2000 to a series of $5,000 annual investments from 2000 through 2018. Amazingly, the final dollar value of the periodic investments nearly equals the dollar value of the initial large lump sum.

If the compounding is steadier a large lump sum should outstrip periodic contributions because only a few of the contributions are getting the benefit of compounding for a long time. Only if the compounding is completely lop-sided, with positive returns occurring overwhelmingly in later years (which is what has happened), should these investments be nearly at the same dollar level. Another way of saying this is that, assuming reasonably even compounding, you should always want to invest a large lump sum immediately rather than dribble money into an investment over time. But the sequence of compounding over the last two decades has been anything but even or steady.

Volatility doesn’t matter for a one-time, lump sum investment. It makes no difference when, over the investment period, the returns come to the final amount. But when you get the returns matters a lot in cases of periodic contributions or withdrawals. When you’re saving periodically, you want the big returns, if possible, after you’ve accumulated some money. And you’d like to get the inevitable bad years out of the way in the beginning of a periodic saving or investment period when you don’t have a lot invested. That’s exactly how it’s worked out for middle aged people today who have been lucky enough to work steadily and earn enough to save periodically for the past two decades. The bad years came early when very little was at stake, and the good years came much later when much more was at stake.

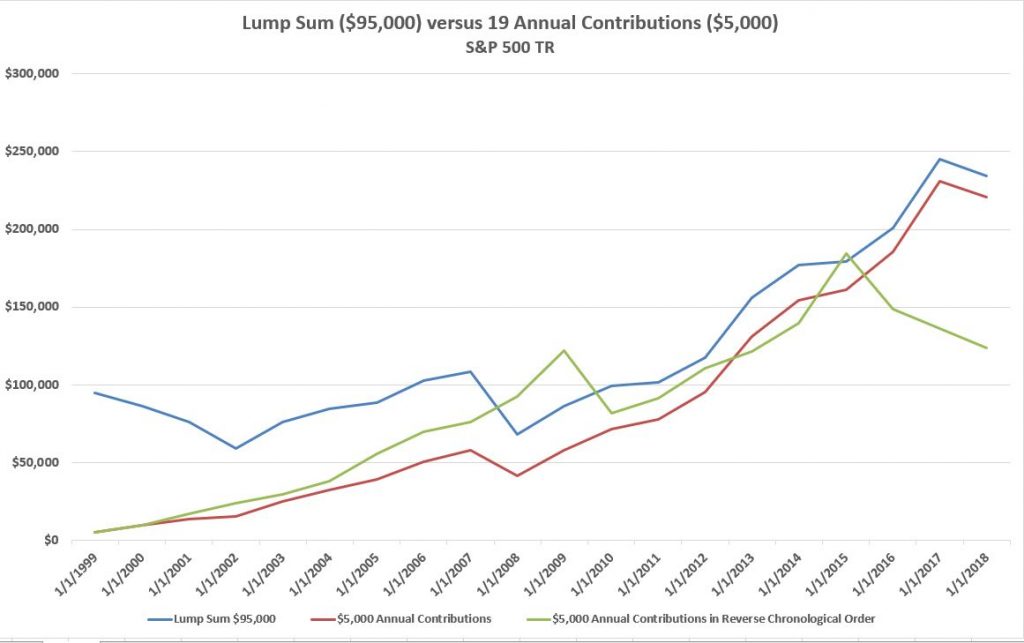

To illustrate the importance of sequence of returns further, the chart below repeats the first chart with an additional line showing contributions made in reverse chronological order (2018-2000). Clearly, getting the big returns in the beginning, and poor returns at the end of a contribution period matters a lot for the final result. The amount of savings decreased roughly $97,000 (or 43%), from around $221,000 to around $124,000.

If investors were also able to ramp up their savings in the second decade, that’s worked out even better for them than our charts show. It could also work out badly in the future if the larger contributions are buying stocks that, in retrospect, look like they might have been overpriced. Time will tell.

Last, it’s likely that those doing periodic investing likely haven’t realized how lucky they are in taking their lumps early and reaping benefits later. The poor overall return of the market is less apparent to them. It also might not be apparent to them how quickly their luck can change, and that it would matter a lot now that they have much more money saved. Middle-aged people who have now accumulated a significant amount of all the money they will ever save might be more vulnerable than they think. The poor returns of their early investing years could re-materialize, and that would be much worse for them now than it was when they first started saving money.

Target date funds might provide some protection to middle-aged investors in that they are surely less allocated to stocks for someone who’s 45, 50, or 55 than they were when the person was 30. But are they as conservative as they should be given today’s valuations, which the boffo returns of the past decade have produced?

Many financial pundits and advisors say you should just try to control the things you can. As an investor, that means the rate of savings and little else. You can’t know what your sequence of returns might be, according to the conventional advice. sometimes you’ll get lucky, and sometimes you won’t; either way, just keep investing in an allocation driven by age and distance to retirement. Maybe that’s true in the end, but if you’re not wondering about how lucky the past long sequence has been for middle-aged savers and whether the next one will be as favorable to people with more at stake than they had 15-20 years ago, you might not be thinking hard enough. Even if you make no moves in your portfolio or investment strategy, you should probably be girding yourself emotionally for a less benign environment.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.