In August of last year, I wrote an article entitled “As Good As It Gets“ which discussed the record levels being set by a broad swath of economic indicators. To wit:

“First, “record levels” of anything are records for a reason. It is where the point where previous limits were reached. Therefore, when a ‘record level’ is reached, it is NOT THE BEGINNING, but rather an indication of the MATURITY of a cycle. While the media has focused on employment, record stock market levels, etc. as a sign of an ongoing economic recovery, history suggests caution.”

In the “rush to be bullish” this a point often missed. When data is hitting “record levels” it is when investors get “the most bullish.” Conversely, they are the most “bearish” at the lows.

But as investors, such is exactly the opposite of what we should do. It is just our human nature.

“What we call the beginning is often the end. And to make an end is to make a beginning. The end is where we start from.” – T.S. Eliot

There currently seems to be a very high level of complacency that the economy will continue its current cycle indefinitely. Or should I say, there seems to be a very large consensus the economy has entered into a “permanently high plateau,” or an era in which economic recessions have been effectively eliminated through monetary and fiscal policy.

Interestingly, it is that very belief on which the Fed is dependent. They have voiced some minor concerns over a slowing in some of the data, yet they remain committed to trailing economic data points which suggest the economy remains robust.

But herein lies “the trap” for investors.

With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, “instability of stability” is now the biggest risk.

The “stability/instability paradox” assumes that all players are rational and such rationality implies avoidance of complete destruction. In other words, all players will act rationally and no one will push “the big red button.”

Again, the Fed is highly dependent on this assumption to provide the “room” needed, after a decade of the most unprecedented monetary policy program in U.S. history, to extricate themselves from it.

The Fed is dependent on “everyone acting rationally.” However, as was seen in the last two months of 2018, such may not actually be the case.

That market rout, and pressure from the White House, has caused the Fed to tilt a bit more “dovish” as of late. However, it should not be mistaken that their views have substantially changed or that they are no longer committed to the reduction of their balance sheet and hiking rates, albeit at a potentially slower pace.

“There is good reason to expect that this strong [economic] performance will continue. I believe that this gradual process of normalization remains appropriate.“

But that may be a mistake as I pointed out recently:

“But the cracks are already starting to appear as underlying economic data is beginning to show weakness. While the economy ground higher over the last few quarters, it was more of the residual effects from the series of natural disasters in 2017 than “Trumponomics” at work. The “pull forward” of demand is already beginning to fade as the frenzy of activity culminated in Q2 of 2018.

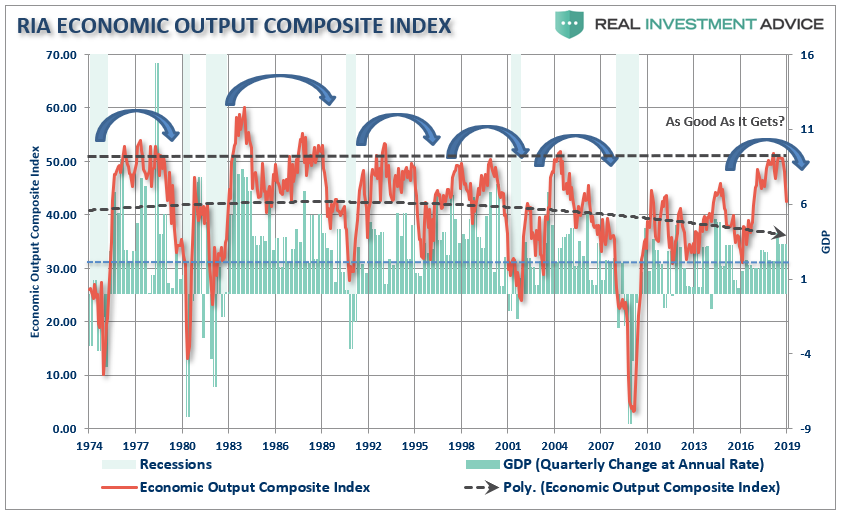

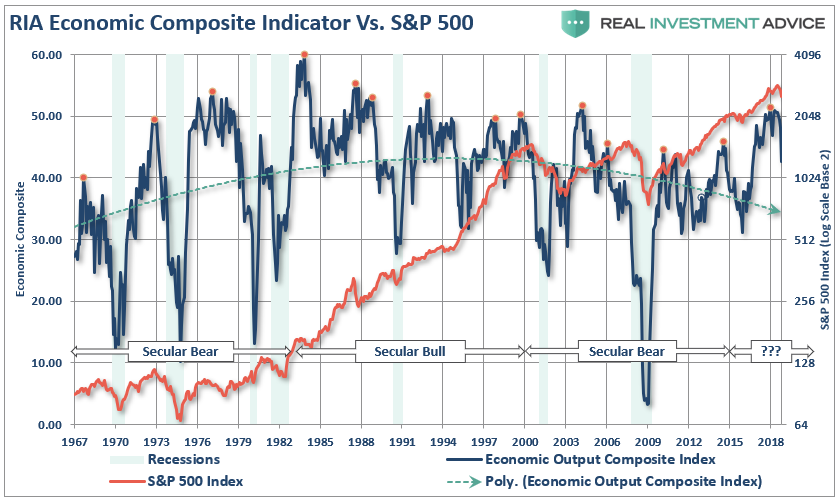

To see this more clearly we can look at our own RIA Economic Output Composite Index (EOCI) which is an extremely broad indicator of the U.S. economy. It is comprised of:

- Chicago Fed National Activity Index (an index comprised of 85 subcomponents)

- Chicago Purchasing Managers Index

- ISM Composite Index (composite of the manufacturing and non-manufacturing surveys)

- Richmond Fed Manufacturing Survey

- New York (Empire) Manufacturing Survey

- Philadelphia Fed Manufacturing Survey

- Dallas Fed Manufacturing Survey

- Markit Composite Manufacturing Survey

- PMI Composite Survey

- Economic Confidence Survey

- NFIB Small Business Index

- Leading Economic Index (LEI)

All of these surveys (both soft and hard data) are blended into one composite index which, when compared to U.S. economic activity, has provided a good indication of turning points in economic activity.

As shown, the slowdown in economic activity has been broad enough to turn this very complex indicator lower.

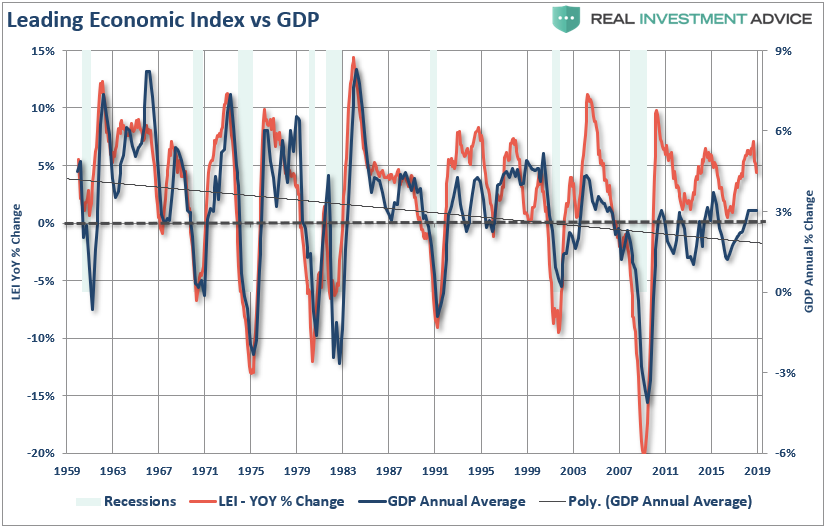

One of the components of the EOCI is the Leading Economic Index (LEI) which is a strong leading indicator of the economy as shown below.

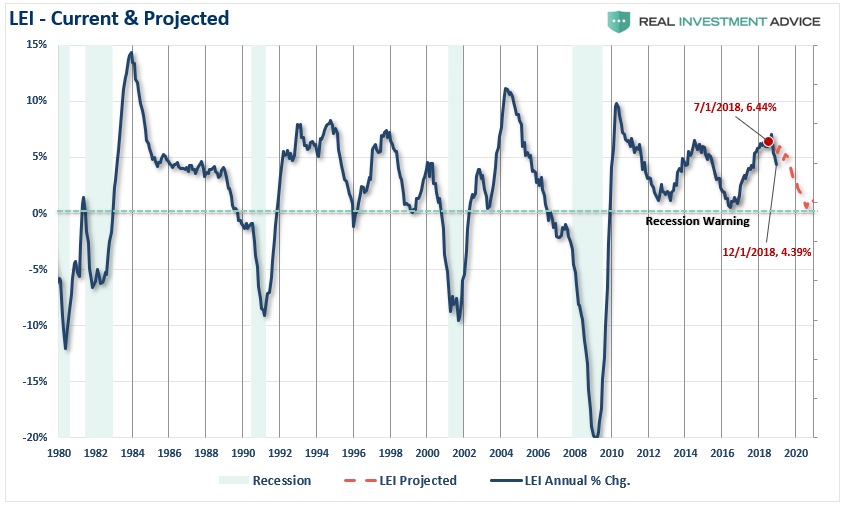

The recent downturn in the LEI suggests economic data will likely be weaker in the quarters ahead. However, this downturn wasn’t a surprise and was something I showed would be the case in July of 2018.

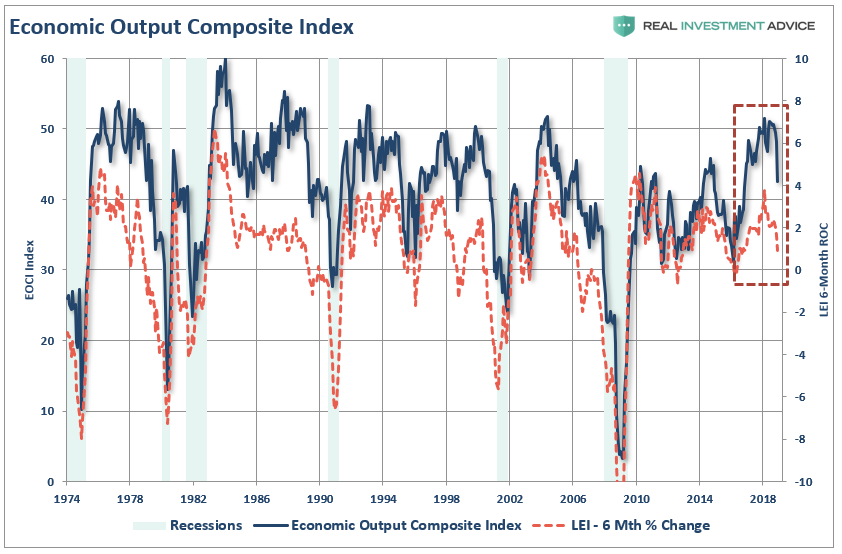

As shown, over the last six months, the decline in the LEI has actually been sharper than originally anticipated. Importantly, there is a strong historical correlation between the 6-month rate of change in the LEI and the EOCI index. As shown, the downturn in the LEI predicted the current economic weakness and suggests the data is likely to continue to weaken in the months ahead.

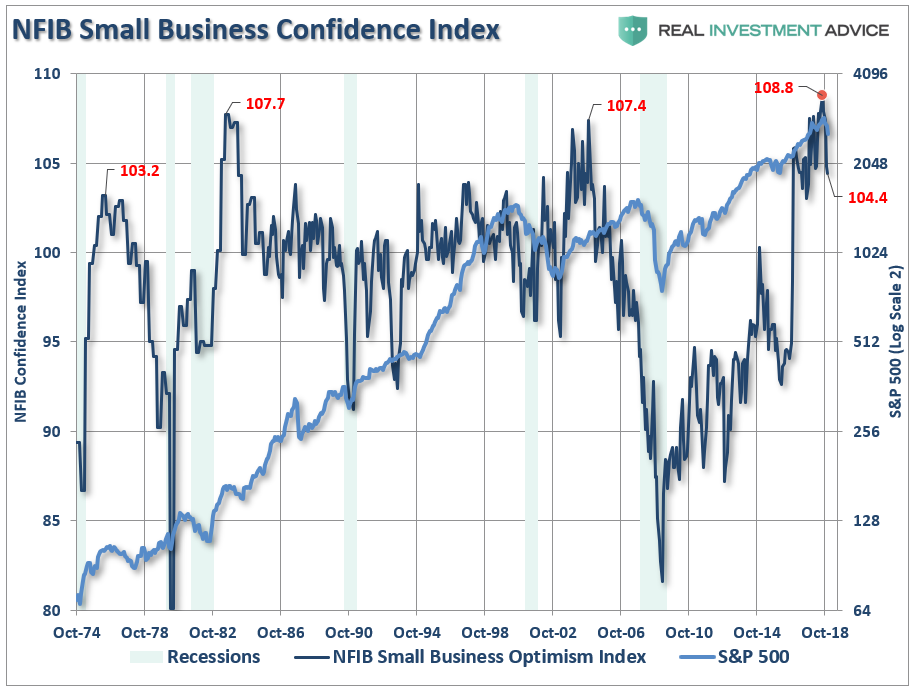

Another component of the EOCI is the National Federation of Small Business index. In 2018, that index peaked at a record of 108.8 and has since fallen more than 4-points in recent months. While it has been of little concern to the media, it should be noticed that at no point in history did the index peak at a record and not substantially decline over the coming months.

More importantly, notice that peaks in the optimism have previously always occurred shortly after a recession ended, not nearly a decade into an economic upturn. Such suggests the time between the current peak and the next recessionary spat could be closer than seen previously.

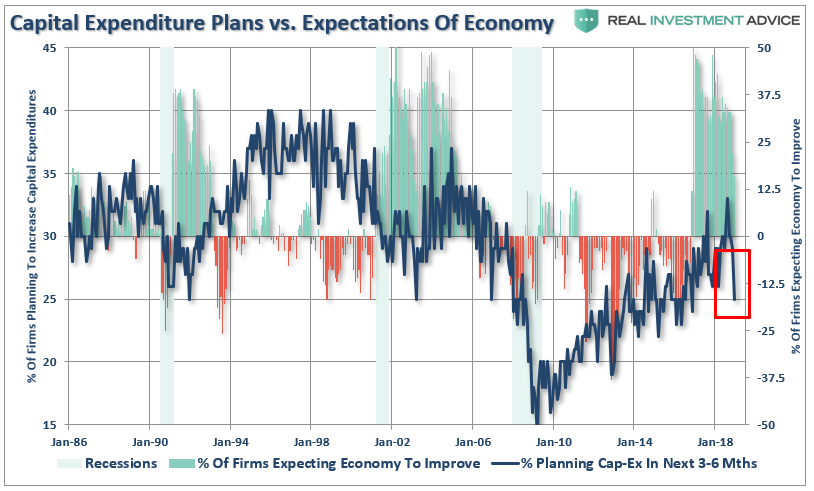

However, while small business owners are still “saying” they are optimistic, they are not necessarily acting that way. A look at their level of economic confidence versus their capital expenditures suggests a much more cautious stance relative to their level of “optimism.”

Currently, their level of capital expenditures has plunged back to levels more often seen during a recessionary period than a burgeoning economic upswing.

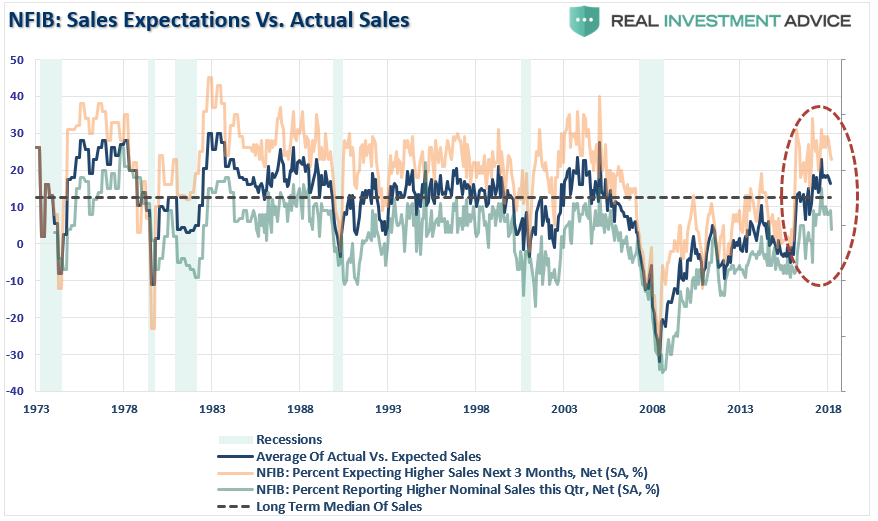

The same goes for the difference between the “expectation of sales” versus their “actual sales.”

Notice that actual sales are always less than expectations, but the current gap is one of the largest on record. More importantly, both actual and expected sales have turned lower in recent months which was during the seasonally strong Christmas shopping period.

All of this underscores the single biggest risk to your investment portfolio.

In extremely long bull market cycles, investors become “willfully blind,” to the underlying inherent risks. Or rather, it is the “hubris” of investors they are now “smarter than the market.”

However, while the Fed is focused on what has happened in the past, the market is focused on what will happen in the future. What the current trend of economic data suggests is that the global economic weakness, which we have been discussing for the last few months, has now come home to roost. As shown below, the EOCI index has provided a leading indication historically to market weakness. The difference between small corrections and larger declines was determined by the secular period of the market.

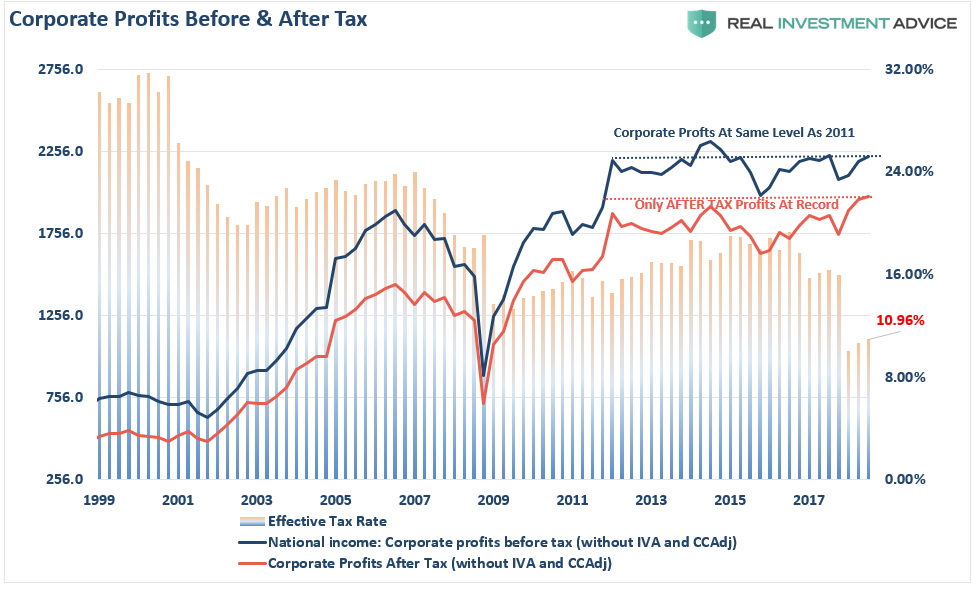

What shouldn’t be overlooked, is that the risk to investors is a negative impact to corporate profitability in the quarters ahead. Valuations are still a major issue for investors as corporate profits have not grown over the last 8-years. (They have only set a record recently on an “after tax” basis due to recent legislative changes.)

Of course, changing profits on the bottom line of the corporate balance sheet is not what drives the economy. That comes from consumption, and if pretax corporate profits aren’t growing, neither is revenue which is consistent with the modest rates of economic growth seen over the last decade.

This is why both the Fed, and the markets, are very dependent on “stability.” As long as no one asks the “tough questions,” the bullish thesis can continue as momentum and psychology remain intact.

Unfortunately, as seen in the last quarter of 2018, “instability” can happen very quickly leaving investors with little time to react. The recent market rout was likely a warning sign that investors should not dismiss as a “one-off” event.

- The Federal Reserve is still looking to increase rates.

- They are also committed to continuing the reduction of their balance sheet which is extracting liquidity from the financial markets.

- Even if the Fed doesn’t hike rates further, rates are still materially higher than they were two-years ago which is impinging consumers discretionary incomes.

- Earnings estimates are still too high

- China is becoming a bigger problem.

- Debt remains a substantial problem as default risks increase

- Domestic economic weakness, as shown, is gaining traction

- The Global economy is weakening at a faster pace than the US economy, and;

- Markets have begun to show their vulnerabilities.

What happens next is anyone’s guess, but erring to the side of caution currently will likely turn out to be a good decision.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.