Over the past couple of weeks, we have been discussing a “sellable rally” following the sell-off during the month of May. To wit:

“This week we are going to look at the recent sell-off and the potential for a short-term ‘sellable’ rally to rebalance portfolio risks into.

The markets only need some mildly positive news at this point to spur a ‘short-covering’ rally. I would encourage you to use it to reduce risk, rebalance holdings, and raise cash until the ‘trade war smoke’ clears.

The market did indeed rally last week. While the initial sell-off in the market was attributed to potential tariffs on Mexico, which were indefinitely suspended on Friday, the real reason was the dismal employment report of just 75,000 jobs.”

As I said, there was more room to go on the upside, and yesterday the market continued its rally to start the week.

“In the very short-term the markets are oversold on many different measures. This is an ideal setup for a reflexive rally back to overhead resistance. The markets have only reversed about half of the previously oversold condition which leaves some ‘fuel in the tank’ for a continuation of the rally this coming week.”

But here is the real question for this week:

Is it still just a “sellable rally” or “is the bull market back?”

That’s the answer we all want to know.

Each week on RIA PRO we provide an update on all of the major markets for trading purposes.

(See an unlocked version here. We also do the same analysis for each S&P 500 sector, selected portfolio holdings, and long-short ideas. You can try RIA PRO free for 30-days)

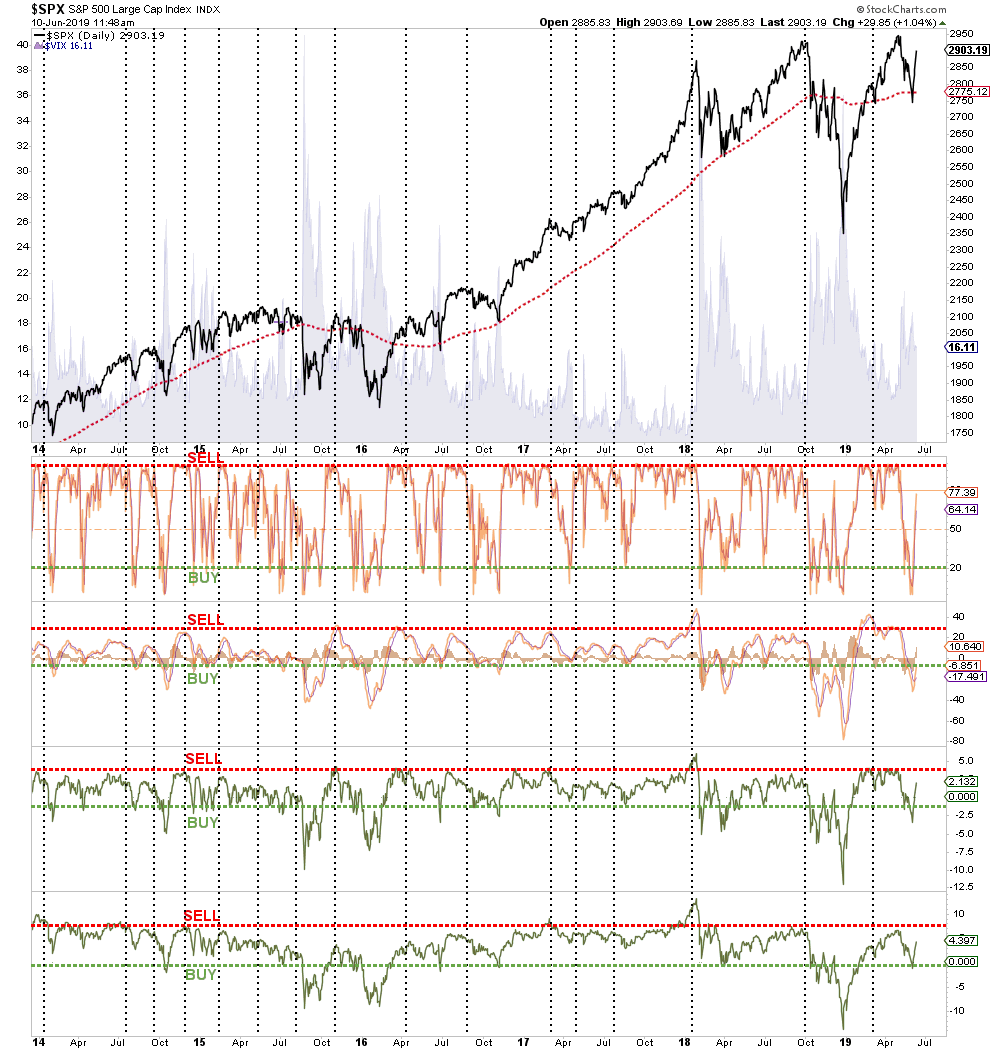

- Last week we noted that SPY had corrected the overbought condition and is testing the 200-dma.

- The “buy” signal in the lower panel was massively extended, as noted several weeks ago, which as we stated, suggested the reversal we have seen was coming. The signal is almost fully reversed.

- As stated last time:

- “The correction last week has set up a tradeable opportunity into June.”

- That tradeable rally is in process and we are approaching our initial target of $290

- Short-Term Positioning: Bullish

- Last Week: Hold full position with a target of $290.

- This Week: Sell 1/2 of position on any rally next week that hits our target.

- Stop-loss moved up to $280

On Monday, our initial target was hit which, for traders, suggests trimming positions and reaping some decent short-term profits. However, the current momentum of the rally does suggest the rally could be sustained through the end of the month with previous highs attainable.

With the markets back to very overbought levels, as noted above, there are reasons to remain cautious as there are signs the current rally is likely not sustainable longer-term.

Let’s Review Some Important Charts

Dow Theory

Dow Theory suggests that when the Transportation index does not confirm the Industrial components, rallies should be treated with caution. Since the Dow Jones Industrial Average is really no longer just industrial companies, I compare the industrials the S&P 500 for some measure of confirmation. Currently, transportation stocks continue to suggest the economy is weaker than the markets currently believe and the current rally is likely somewhat limited.

![]()

Notice the vertical red lines correspond with a non-confirmation of transportation to the S&P 500. In most cases, that non-confirmation resulted in lower market prices. While this is not an absolute signal, it does suggest some caution with respect to excessive risk taking.

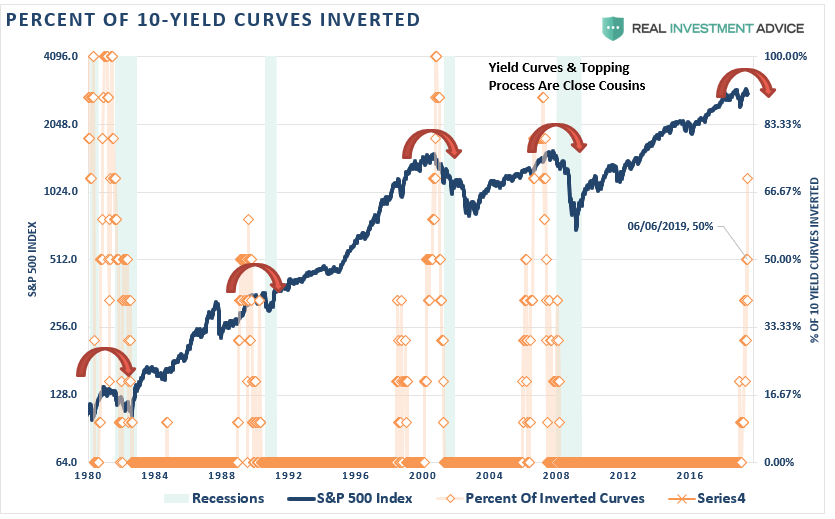

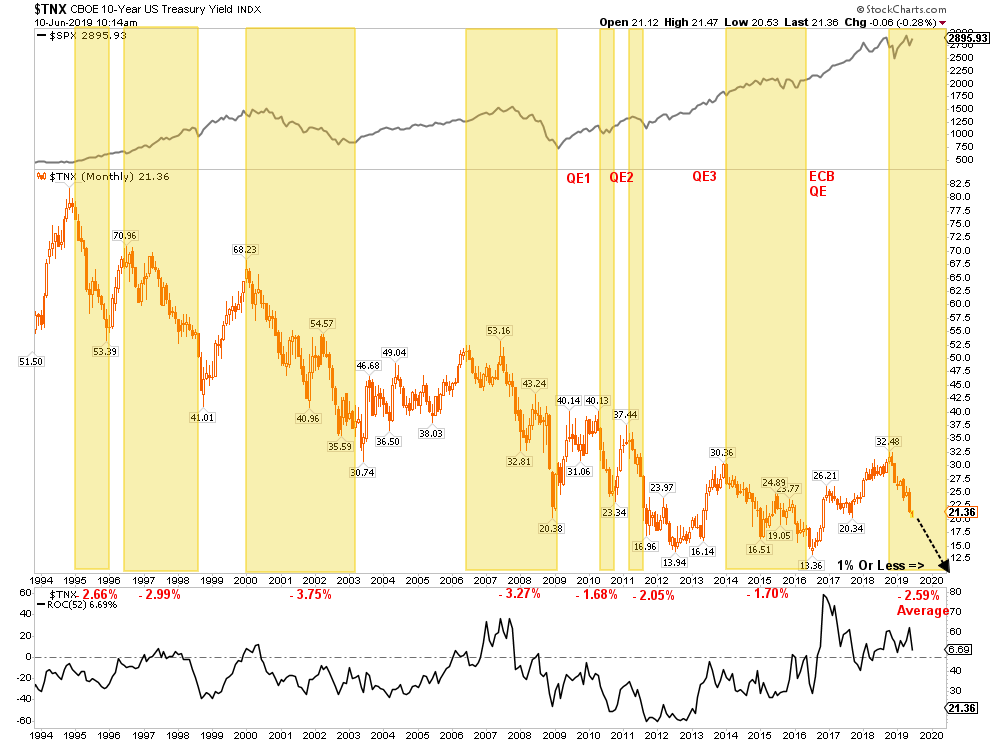

Yields

Yields also continue to suggest that investors should proceed with at least of a modicum of caution.

As noted this past weekend, the yield spreads across various maturities have continued to invert. These inversions are not just a theoretical market indicator but rather has real world impacts on a variety of areas which affect real economic growth such as lending, capital investment, and financially engineered products.

“Interest rates are the best predictor of the economic strength, and the yield curve has been screaming both ‘deflation’ and ‘economic weakness’ for months. (We have repeatedly warned on this issue – see here)”

Importantly, as shown in the chart below, yields typically fall 2-3% on average during periods of economic weakness and recessions.

The important thing to notice is that during each period of falling rates, going back to 1980, each successive low has been lower along with the subsequent high during each cycle. With yields currently at just a bit more than 2%, as of this writing, the next low in interest rates, most likely coincident with a recession, will be close to zero.

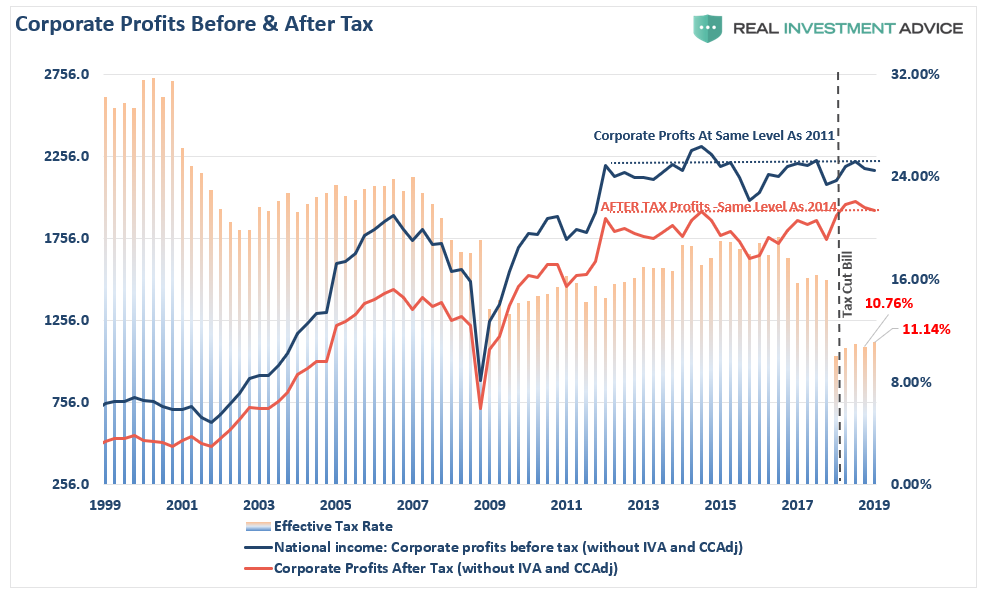

Corporate Profits

Ultimately, the market is a “weighing machine,” to quote Warren Buffett, based on the expected cash flows and profits from companies in the future. While in the short-term prices can, and do, deviate from the underlying value, ultimately prices will revert to the underlying fundamentals. Since the December 24th lows, prices have risen sharply while earnings, and subsequently corporate profits, have deteriorated. The chart below shows corporate profits before and after tax.

It is important to note that investors are paying a very high price for earnings which have not risen since 2011 on a pre-tax basis. (Also, the effective tax rate rose in the last quarter.)

With the risk of a recession on the rise, the risk to profits, and ultimately valuation multiples, is worth carefully considering. As David Rosenberg noted on Monday:

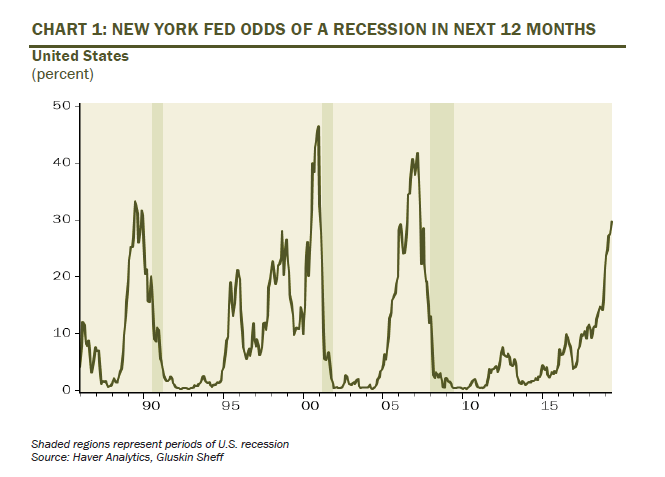

“It’s not like risks have not been on the rise either, as the New York Fed’s recession model increased again in May hitting its highest level in 12-years. Odds of a recession ticked higher to 29% from just 11% last year and 8% two years ago. Putting it all together means there is now more downside risk than upside potential in the stock market as investors have already overpriced equities for whatever good news there has been in the first 5-months of the year.”

(Importantly, the recession indicator is based on LAGGING economic data which is subject to very large revisions. It is for the reason that readings of 20-30% are indicative of recessions.)

Monthly Signals Remain Bearish

Given that monthly data is very slow moving, longer-term signals can uncover changes to the trend which short-term market rallies tend to obfuscate.

I can’t believe I actually have to write the next sentence, but if I don’t I invariably get an email saying “but if you sold out, you missed the whole rally.”

What should be obvious is that while the monthly “sell” signals have gotten you out to avoid more substantial destructions of capital, the reversal of those signals were signs to “get back in.” Investing long-term is about both deployment of capital and the preservation of it.

Currently, the monthly indicators have all aligned to “confirm” a “sell signal” which since 1950 has been somewhat of a rarity. The risk of ignoring the longer-term signal currently is the risk of a loss of what has been gained during the current reflexive rally. Yes, while waiting for the signal to reverse will equate to short-term underperformance, the long-term risk-adjusted returns have been more than enough to satisfy retirement planning goals which is why we invest to begin with.

The following chart is one of my favorites because it combines a litany of confirming signals all into one monthly chart. Despite the recent rally, which has pushed prices back above their longer-term moving average, the longer-term trends of the signals remain “non-confirming” of the recent rally.

The technical signals, which do indeed lag short-term turns in the market, have not confirmed the bullish attitude. Rather, and as shown in the chart above, the negative divergence of the indicators from the market should actually raise some concerns over longer-term capital preservation.

What This Means And Doesn’t Mean

What this analysis DOES NOT mean is that you should “sell everything” and “hide in cash.”

As always, long-term portfolio management is about “tweaking” things over time.

At a poker table, if you have a “so so” hand, you bet less or fold. It doesn’t mean you get up and leave the table altogether.

What this analysis DOES MEAN is that we need to use this rally to take some actions to rebalance portfolios to align with some the “concerns” as discussed above.

1) Trim Winning Positions back to their original portfolio weightings. (ie. Take profits)

2) Sell Those Positions That Aren’t Working. If they don’t rally with the market during a bounce, they are going to decline more when the market sells off again.

3) Move Trailing Stop Losses Up to new levels.

4) Review Your Portfolio Allocation Relative To Your Risk Tolerance. If you are aggressively weighted in equities at this point of the market cycle, you may want to try and recall how you felt during 2008. Raise cash levels and increase fixed income accordingly to reduce relative market exposure.

Could I be wrong? Absolutely.

If we are, and the market rallies and confirms new highs, and a resurrection of the bullish trend, then we will adjust our allocation models up and take on more equity risk.

But as I have asked before, what is more important to you as an individual?

- Missing out temporarily on the initial stages of a longer-term advance, or;

- Spending time getting back to even, which is not the same as making money.

For the majority of investors, the recent rally has simply been just recovery of previous losses from 2018.

Currently, there is not a great deal of evidence supportive of a longer-term bull market cycle. The Fed talking about cutting rates is “NOT” bullish, it actually correlates to much more negative long-term outcomes in the market.

If I am right, however, the preservation of capital during an ensuing market decline will provide a permanent portfolio advantage going forward. The true power of compounding is not found in “the winning,” but in the “not losing.”

As I quoted in our post on trading rules:

“Opportunities are made up far easier than lost capital.” – Todd Harrison

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.