I noted in this past weekend’s newsletter the pick up in volatility over the last few weeks has made investing in the market difficult.

On Friday, the market plunged on new Trump was going to increase tariffs on China. Then on Monday, the markets rallied on comments from President Trump that China was ready to talk.

“China called last night our top trade people and said ‘let’s get back to the table’ so we will be getting back to the table and I think they want to do something. They have been hurt very badly but they understand this is the right thing to do and I have great respect for it. This is a very positive development for the world.” – President Trump, via CNBC

You simply can’t trade that kind of volatility. This was a point made to our RIAPRO subscribers last week:

When you are ‘unsure’ about the best course of action, the best course of action is to ‘do nothing.’”

As we discussed previously, the President has learned that his comments will move markets. Given the shellacking of the markets on Friday, and what was looking to be a dismal open Monday morning, Trump’s comments to boost the markets weren’t surprising.

What the market disregarded were the comments from China:

Based on what I know, Chinese and US top negotiators didn't hold phone talks in recent days. The two sides have been keeping contact at technical level, it doesn't have significance that President Trump suggested. China didn't change its position. China won't cave to US pressure.

— Hu Xijin 胡锡进 (@HuXijin_GT) August 26, 2019

As I penned last week, the markets have now been “trained” by Trump.

“Ring the bell. Investors salivate with anticipation.”

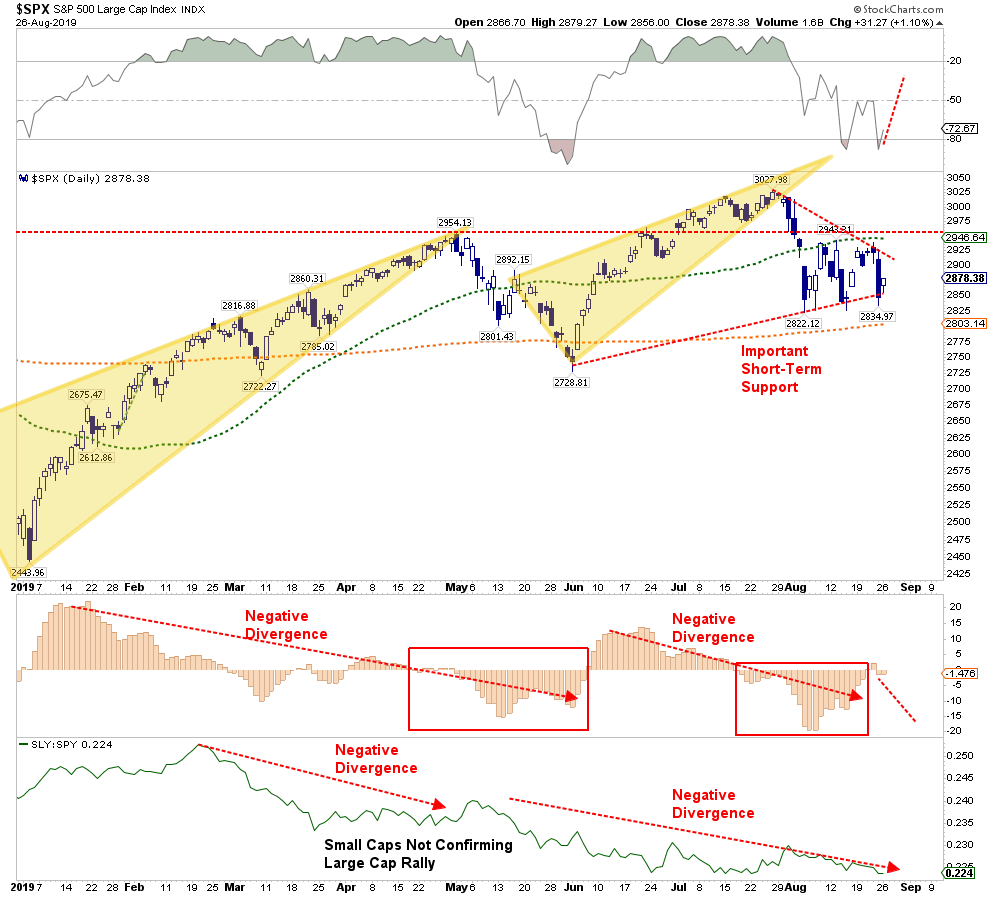

However, despite the rally yesterday, the markets are still well confined in a very tight consolidation range.

- The “bulls” are hoping for a break to the upside which would logically lead to a retest of old highs.

- The “bears” are concerned about a downside break which would likely lead to a retest of last December’s lows.

- Which way will it break? Nobody really knows.

This is why we have been suggesting raising cash on rallies, and rebalancing risk until the path forward becomes clear.

“The reason we suggest selling any rally is because, until the pattern changes, the market is exhibiting all traits of a ‘topping process.’ As the saying goes, a market-top is not an event; it’s a process.”

Let me restate from this past weekend’s missive where we are positioned currently:

“Over the past few months, we have reiterated the importance of holding higher levels of cash, being long fixed income, and shifting risk exposures to more defensive positions. That strategy has continued to work well.”

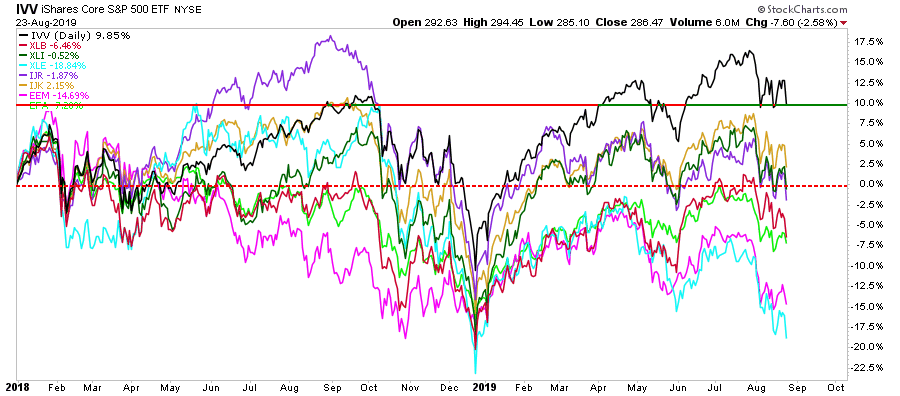

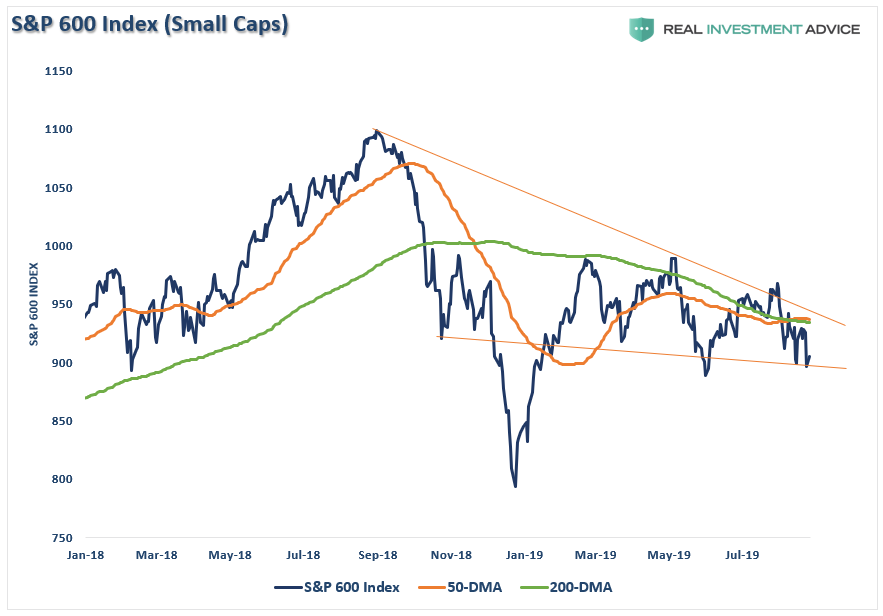

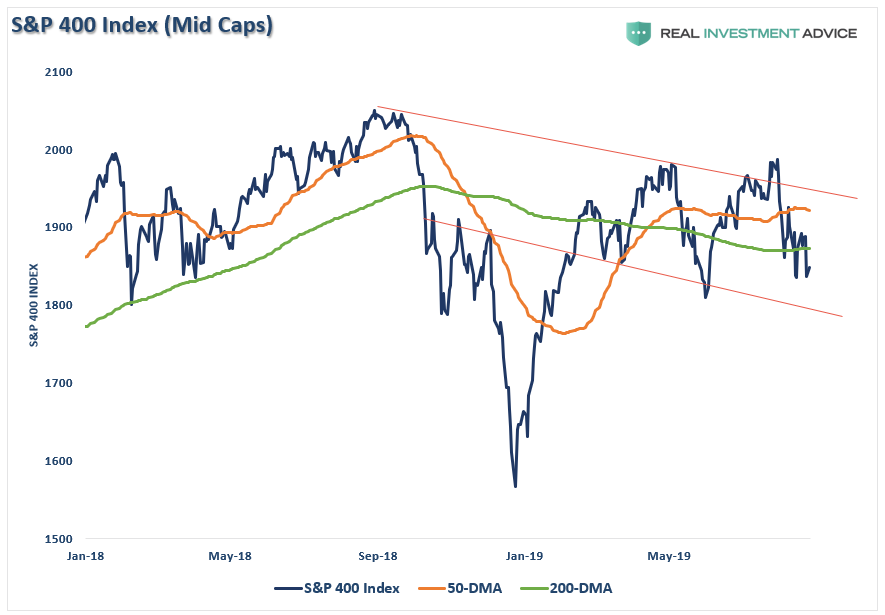

- We have remained devoid of small-cap, mid-cap, international and emerging market equities since early 2018 due to the impact of tariffs on these areas.

- For the same reasons we have also reduced or eliminated exposures to industrials, materials, and energy

- With the trade war ramping up, there is little reason to take on additional risk at the current time as our holdings in bonds, precious metals, utilities, staples, and real estate continue to do the heavy lifting.”

As I noted previously, if you are told you have to “buy and hold” a little of everything to be diversified, then what are you paying an advisor for? There are plenty of “robo-advisors” that will gladly clip a fee from you to do something you can easily do yourself.

However, be warned. There are currently high correlations between asset classes, which suggests that when the next bear market ensues there will be few places to hide. What goes up together, will come down together as well. Being “diversified,” in the traditional sense, isn’t going to help you.

Markets Send Warning Signals

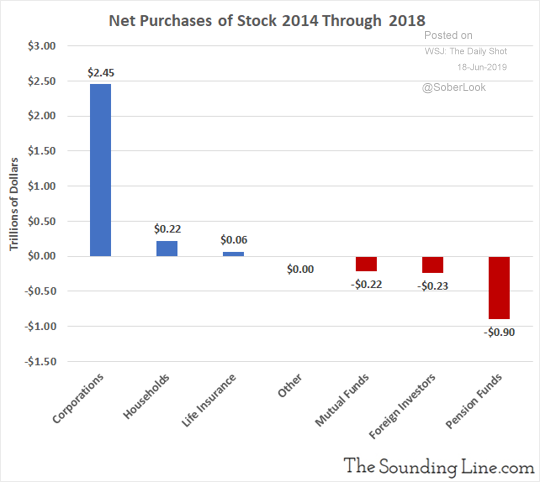

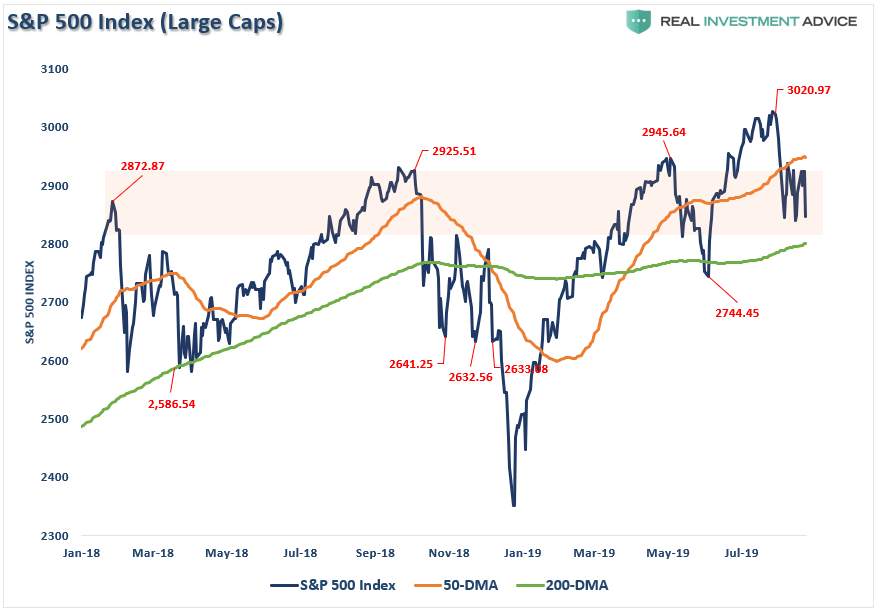

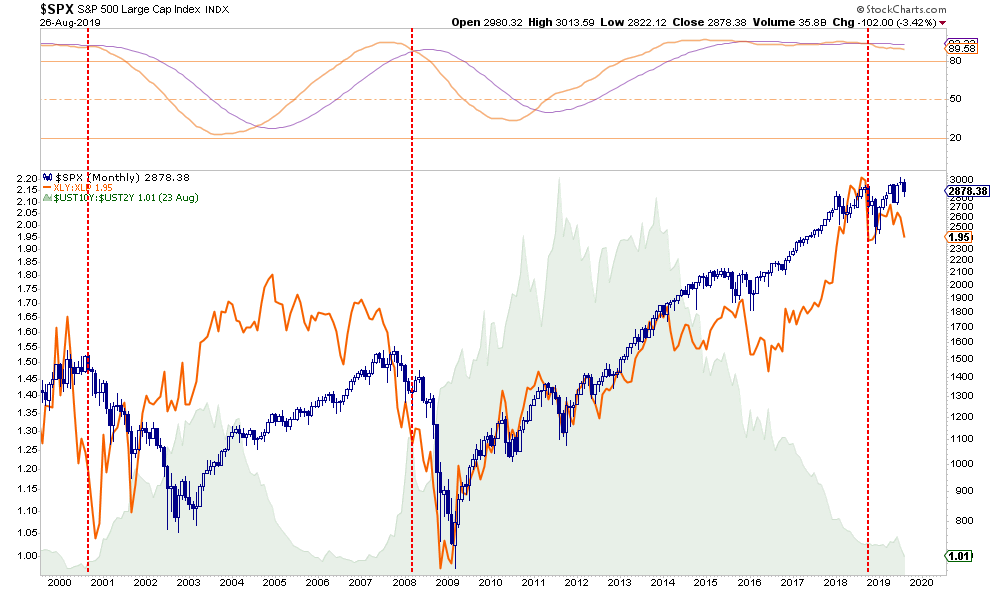

While large-cap stock indexes (S&P 500, Dow Jones, and Nasdaq) have maintained a reasonably steady state over the past 18-months, such is not the case across the broader market. As I noted previously, share repurchases have provided much of the lift for large-capitalization stocks over the last couple of years.

“Corporate share buybacks currently account for roughly all ‘net purchases’ of U.S. equities in recent years. To wit:“

“It is likely that 2018/2019 will be the potential peak of corporate share buybacks, thereby reducing the demand for equities in the market. This ‘artificial buyer’ explains the high degree of complacency in the markets despite recent volatility. It also suggests that the ‘bullish outlook’ from a majority of mainstream analysts could also be a mistake.

If the economy is weakening, as it appears to be, it won’t be long until corporations redirect the cash from ‘share repurchases’ to shoring up operations and protecting cash flows.”

With portfolio managers needing to chase performance, the easiest, and safest, place to allocate capital is in highly liquid, large capitalization companies which are being supported by share repurchases. Despite trade turmoil, Fed disappointment, and weaker economic, and earnings growth, stocks still remain elevated and confined within the longer-term bullish trend.

However, once you step outside the large-capitalization universe, a very different picture emerges.

Since small and mid-capitalization companies don’t engage in massive share repurchase programs, and are directly impacted by early changes to consumer spending and tariffs. As such, it is not surprising that performance has been lagging that of its large-cap brethren.

Small-Cap 600 Index

Mid-Cap 400 Index

Mid-Cap 400 Index

The same issue applies to international markets as well, where economic growth has been markedly weaker than in the U.S.

MSCI All-World (Ex-US) Index

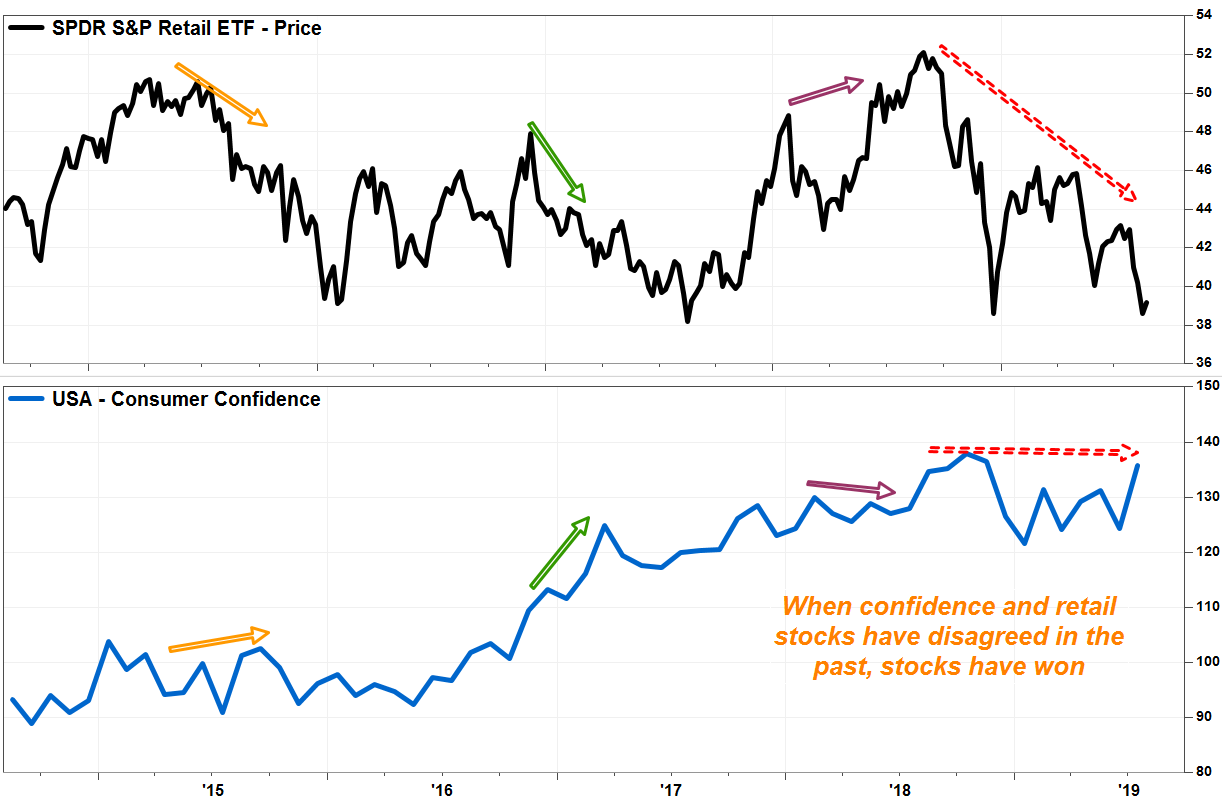

Given the consumer makes up about 2/3rds of the U.S. economy, low unemployment, and retail sales data is often cited as reasons to be “bullish” on equities. However, as shown in the chart below, the ratio between consumer “discretionary” and “staples” companies suggests there is an emerging weakness in the retail sector.

As Tomi Kilgore noted for MarketWatch,

“One way to gauge the real strength of the consumer is to measure how much they spend on what they want (discretionary items) relative to what they need (staples). The consumer discretionary sector is highly sensitive to what the overall stock market is doing, and to worries about economic growth and contraction.

To see this relationship in real time is through comparing consumer discretionary stocks, by way of the SPDR Consumer Discretionary Select Sector exchange-traded fund (XLY), to the consumer staples sector, as tracked by the SPDR Consumer Staples Select Sector ETF (XLP).”

Historically, when the S&P 500 is on a monthly sell signal, with an inverted yield curve, and discretionary stocks are underperforming staples, it has been a leading indicator of a recessionary economy and bear market.

As Tomi goes on to note:

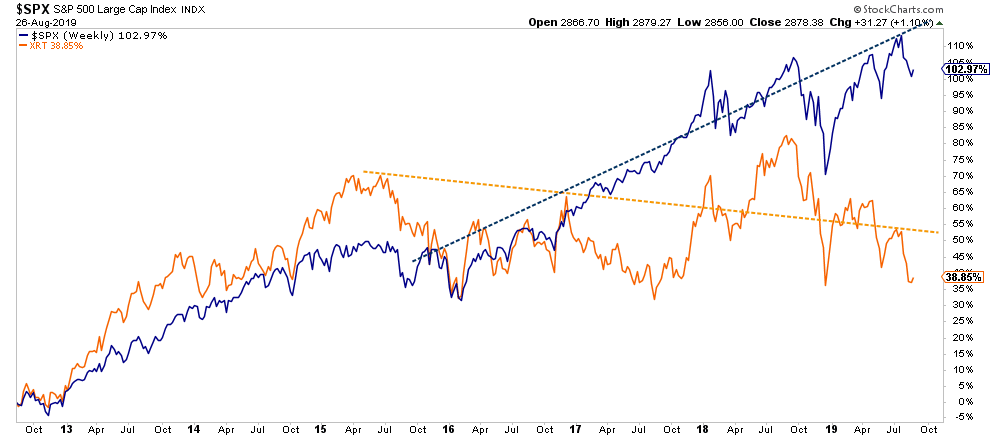

“That by itself might lead one to believe that worries about the economy are overdone, until a chart of consumer confidence is placed side-by-side with a chart of retail stocks, as tracked by the SPDR S&P Retail ETF (XRT).”

As one might expect, those charts usually move in tandem. But sometimes they move in opposite directions for short periods of time, and when they do, it’s the stocks that have been the leading indicator.

And the retail sector should still matter to investors, because when the XRT has diverged from the broader market at key turning points, it has been the XRT that has led the way.

Slow At First, Then All Of A Sudden

What all of this suggests is that “risk” is building in the markets.

However, risk builds slowly. This is why the investment community often uses the analogy of “boiling a frog.” By turning up the heat slowly, frogs don’t realize they are being boiled until its too late. The same is true for investors who make a series of mistakes as “risk” builds up slowly.

- Investors are slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late-cycle stages.

- Investors are ultimately driven by the “herding” effect. A rising market leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

- Lastly, as the markets turn, the “disposition” effect takes hold and winners are sold to protect gains, but losers are held in the hopes of better prices later.

The end effect is not a pretty one.

When the buildup of “risk” is finally released, the explosion happens all at once leaving investors paralyzed trying to figure out what just happened. Unfortunately, by the time they realize they are the “frog,” it is too late to do anything about it.

With President Trump on a warpath with China, increasing tariffs (a tax on businesses), at a time when economic growth and corporate profits are weakening, raises our concern over the amount of equity exposure we are carrying in the markets.

Given that markets still hovering within striking distance of all-time highs, there is no need to immediately take action. However, the continuing erosion of underlying fundamental and technical strength keeps the risk/reward ratio out of favor. As such, we suggest continuing to take actions to rebalance risk.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

We are closer to the end of this cycle than not, and the reversion process back to value has historically been a painful one.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.