- Trade Deal Done

- QE, Not QE, But It’s QE

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Trade Deal Done

On Thursday and Friday, the market surged on hopes that a “trade deal” was coming to fruition. This was not a surprise to us, as we detailed this outcome two weeks ago:

“‘For Trump, he can spin a limited deal as a ‘win’ saying ‘China is caving to his tariffs’ and that he ‘will continue working to get the rest of the deal done.’ He will then quietly move on to another fight, which is the upcoming election, and never mention China again. His base will quickly forget the ‘trade war’ ever existed.

Kind of like that ‘Denuclearization deal’ with North Korea.’”

As we discussed in that missive, a limited “trade deal” would potentially set the markets up for a run to 3300. To wit:

Assuming we are correct, and Trump does indeed ‘cave’ into China in mid-October to get a ‘small deal’ done, what does this mean for the market.

The most obvious impact, assuming all ‘tariffs’ are removed, would be a psychological ‘pop’ to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year.”

This is not the first time we presented our analysis for a “bull run” to 3300.

Every week, we review the major markets, sectors, portfolio positions specifically for our RIA PRO subscribers (You can check it out FREE for 30-days). Here was our note for the S&P 500 previously.

- We are still maintaining our core S&P 500 position as the market has not technically violated any support levels as of yet. However, it hasn’t been able to advance to new highs either.

- There is likely a tradeable opportunity approaching for a reflexive bounce given the depth of selling over the last couple of weeks.

This is the outcome we expected.

- There is no “actual” deal.

- The “excuse” will be this deal lays the groundwork for a future deal.

- No one will discuss a trade deal ever again.

It is almost as if Bloomberg read our work:

“The U.S. and China reached a partial agreement Friday that would broker a truce in the trade war and lay the groundwork for a broader deal that Presidents Donald Trump and Xi Jinping could sign later this year.

As part of the deal, China would agree to some agricultural concessions and the U.S. would provide some tariff relief. The deal under discussion, which is subject to Trump’s approval, would suspend a planned tariff increase for Oct. 15. It also may delay — or call off — levies scheduled to take effect in mid-December.”

So, who won?

China.

- China gets to buy agricultural and pork products they badly need.

- The U.S. gets to suspend tariffs.

Who will like the deal?

- The markets: the deal removes a potential escalation in tariffs.

- Trump supporters: Fox News will “spin” the “no deal” into a Trump “win” for the 2020 election.

- The Fed: It removes one of their concerns potentially impacting the economy.

By getting the “trade deal” out of the headlines, this clears the way for the market to rally potentially into the end of the year. Importantly, it isn’t just the trade deal providing support for higher asset prices short term:

- There now seems to be a pathway forward for “Brexit”

- The Fed is injecting $60 billion a month in liquidity into 2020 (More on this below)

- The Fed has cut rates and is expected to cut again by year end.

- ECB back into easing mode and running negative rates

- Fed and ECB loosening capital requirements for banks (Because they are so healthy after all.)

This is also a MAJOR point of concern.

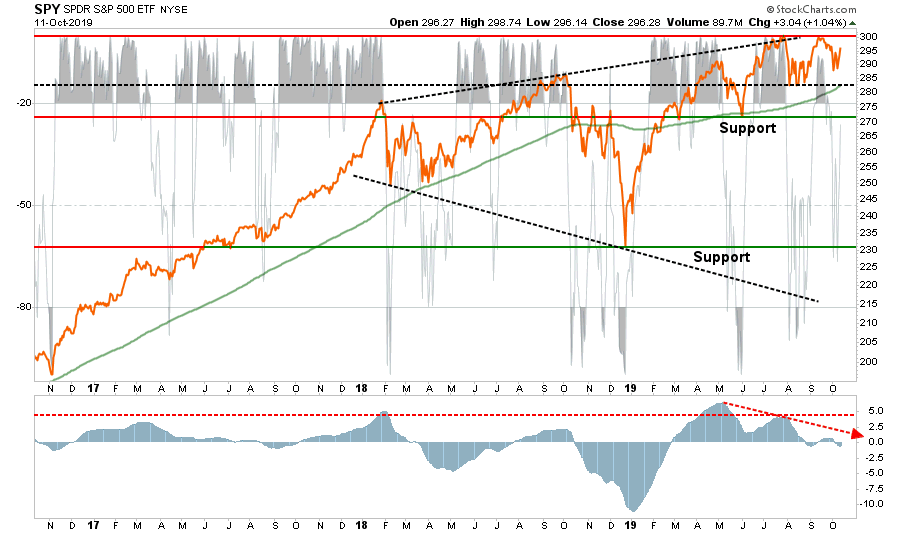

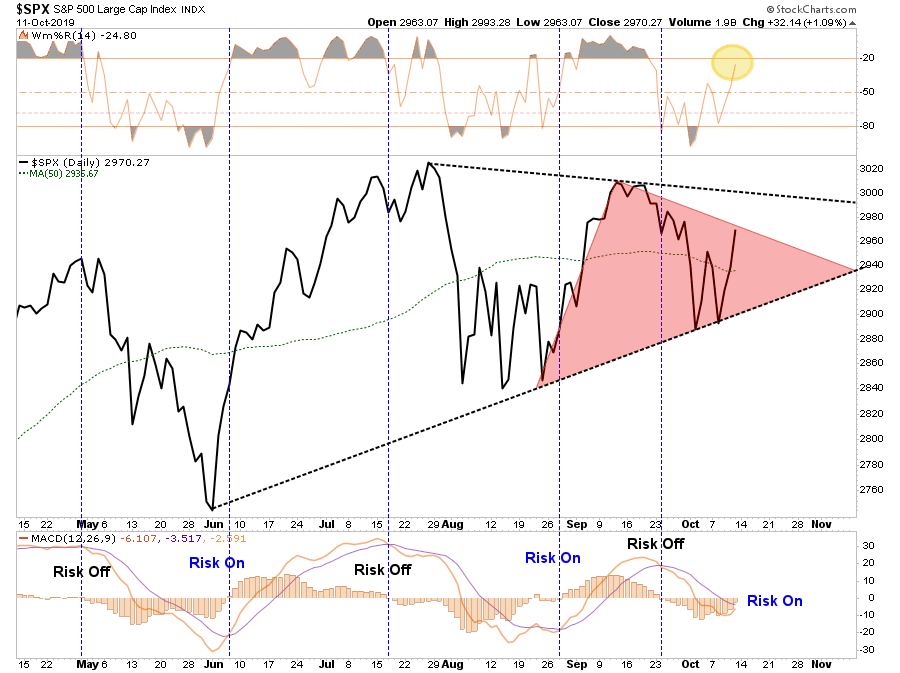

Despite all of this liquidity and support, the market remains currently confined to a downtrend from the September highs. The good news is there is a series of rising lows from June. With a “risk-on” signal approaching and the market not back to egregiously overbought, there is room for the market to rally from here.

Let me repeat what we wrote back in July:

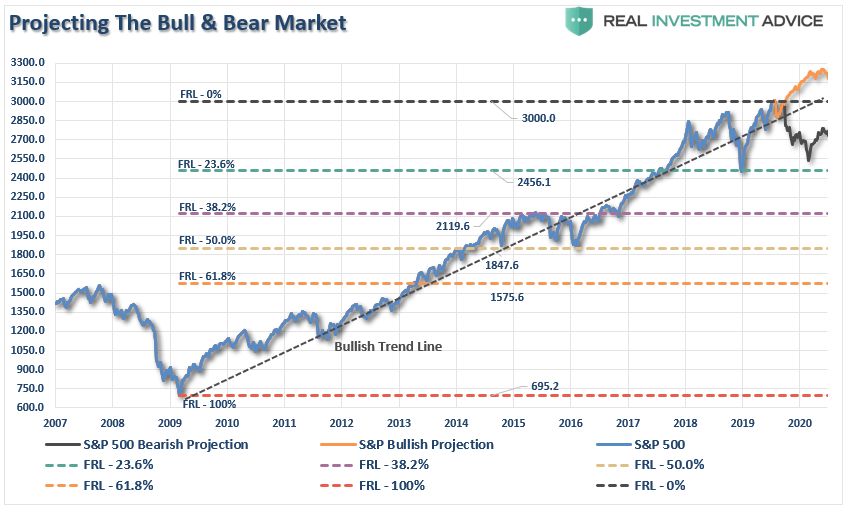

“As we face down the last half of 2019, we can once again run some projections on the bull and bear case going into 2021, as shown in the chart below:”

The Bull Case For 3300

- Momentum

- Stock Buybacks

- Fed Rate Cuts

- Stoppage of QT

- Trade Deal

However, while the case for a push higher is likely, the risk/reward still isn’t great for investors over the intermediate term. A failure of the market to make new highs, given the amount of monetary support, will be a very bearish signal.

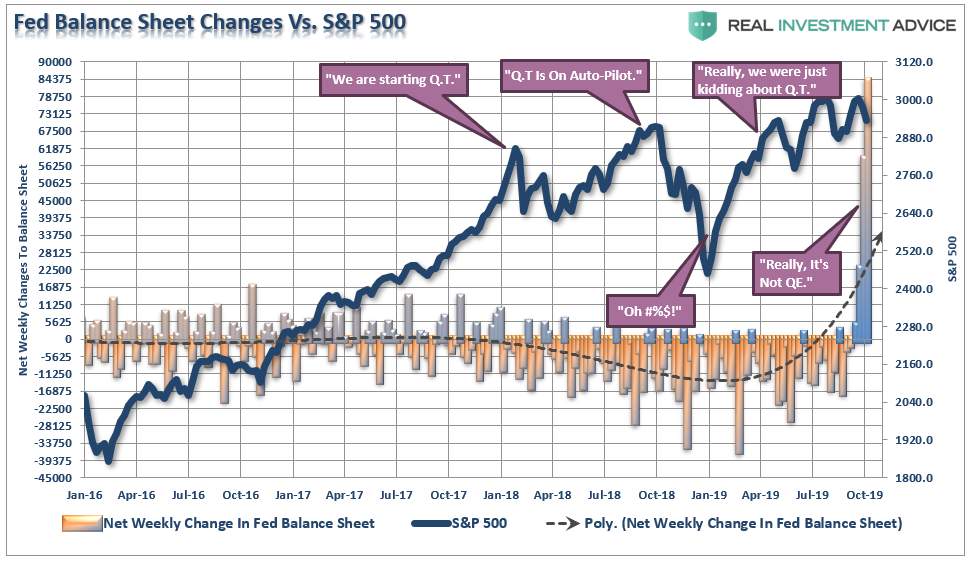

The Fed’s “Not QE”, “QE”

There is no systemic threat from a shortage of reserves or a weak banking system. Some (a few) firms got sideways with new bank liquidity regs. The Fed should let market deal with it, not inject low cost money to encourage this behavior! And, Fed should let us know who they are!

— Brian Wesbury (@wesbury) October 12, 2019

Sure thing, Brian.

As I noted previously:

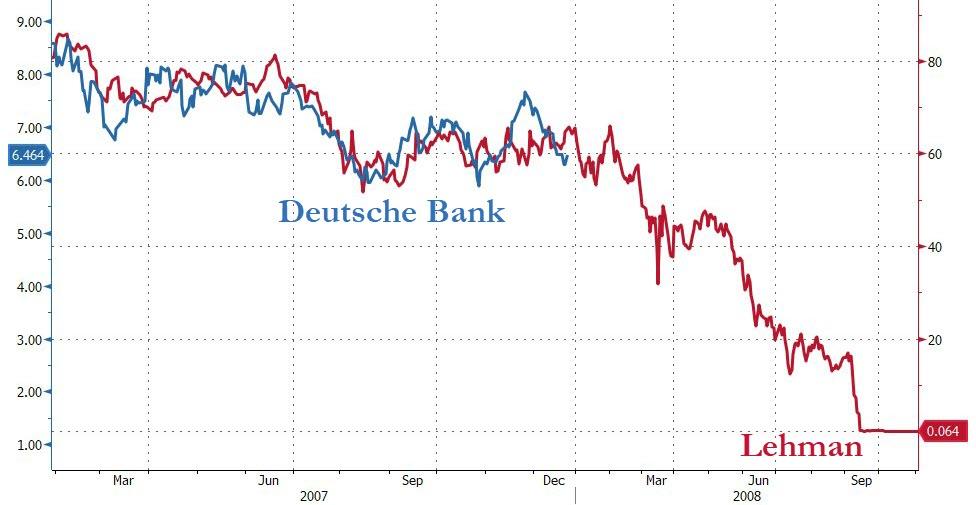

“Then there are the tail-risks of a credit-related event caused by a dollar funding shortage, a banking crisis (Deutsche Bank), or a geopolitical event, or a surge in defaults on “leveraged loans” which are twice the size of the “sub-prime” bonds linked to the “financial crisis.” (Read more here)

Just remember, bull-runs are a one-way trip.

Most likely, this is the final run-up before the next bear market sets in. However, where the “top” is eventually found is the big unknown question. We can only make calculated guesses.”

Think about this logically for a moment.

- The yield curve inverts which puts pressure on bank loans and funding.

- The Fed cuts rates, which puts pressure on banks net interest margins.

- The banks are chock full of leverage loans, risky energy-related debt, subprime auto loans, etc.

- The Fed begins reducing excess reserves.

- All of a sudden, banks have a problem with overnight funding.

- Fed reduces liquidity regulations (put in place after Lehman to protect the financial system)

- Fed now has to commit to $60 billion in funding through January 2020 to increase reserves.

The last point was detailed in a recent FOMC release:

“In light of recent and expected increases in the Federal Reserve’s non-reserve liabilities, the Federal Open Market Committee (FOMC) directed the Desk, effective October 15, 2019, to purchase Treasury bills at least into the second quarter of next year to maintain over time ample reserve balances at or above the level that prevailed in early September 2019. The Committee also directed the Desk to conduct term and overnight repurchase agreement operations (repos) at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation.

In accordance with this directive, the Desk plans to purchase Treasury bills at an initial pace of approximately $60 billion per month, starting with the period from mid-October to mid-November.”

NOTE: If you don’t understand what has been happening with overnight lending between banks – READ THIS.

The Fed is in QE mode because there is a problem with liquidity in the system. Given the Fed was caught “flat-footed” with the Lehman bankruptcy in 2008, they are trying to make sure they are in front of the next crisis.

The reality is the financial system is NOT healthy.

If it was, then we would:

- Not still be using “emergency measures” to support banks for the last decade. (QE, LTRO, Etc.)

- Not be pushing $17 trillion in negative interest rates on a global basis.

- Have reinstated FASB Rule 157 in 2012-2013 requiring banks to mark-to-market the assets on their books. (A defaulted asset can be marked at 100% of value which makes the bank look healthy.)

- Not be needing to reduce liquidity requirements.

- Not be needing $60 billion a month in QE.

Oh, but that’s right, Jerome Powell denies this is “QE.”

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis. Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy. In no sense, is this QE,” – Jerome Powell

It’s QE.

Just so you can understand the magnitude of the balance sheet increase over the last couple of weeks, the largest single week increase from 2009 to September 20th, 2019 was $39.97 billion.

The last two weeks were $58.2 and $83.87 billion respectively.

But, it’s not Q.E.

So, what was it then?

This was not about covering unexpected cash draws to pay quarterly taxes, which was one of the initial excuses for the funding shortfalls.

So true – remember the whole #REPO crisis started because it was just a demand for cash for #tax #payments. Apparently, companies are paying taxes daily until sometime in 2020.

Amazing the #media continually buys into the #narratives as if they were the truth. #ThinkPeople https://t.co/Y3cxdK9AWe— Lance Roberts (@LanceRoberts) October 12, 2019

Nope.

This was bailing out a bank that is in serious financial trouble. It started with the ECB a month ago loosening requirements on banks, then proceeded to the Fed reducing capital reserve requirements and flooding the system with reserves.

Who was the biggest beneficiary of all of these actions? Deutsche Bank.

Which is about 4x as large as Lehman was in 2008 and is currently following the same price path as well. Let me repeat, the Fed is terrified of another “Lehman Crisis” as they do not have the tools to deal with it this time.

(Courtesy of ZeroHedge)

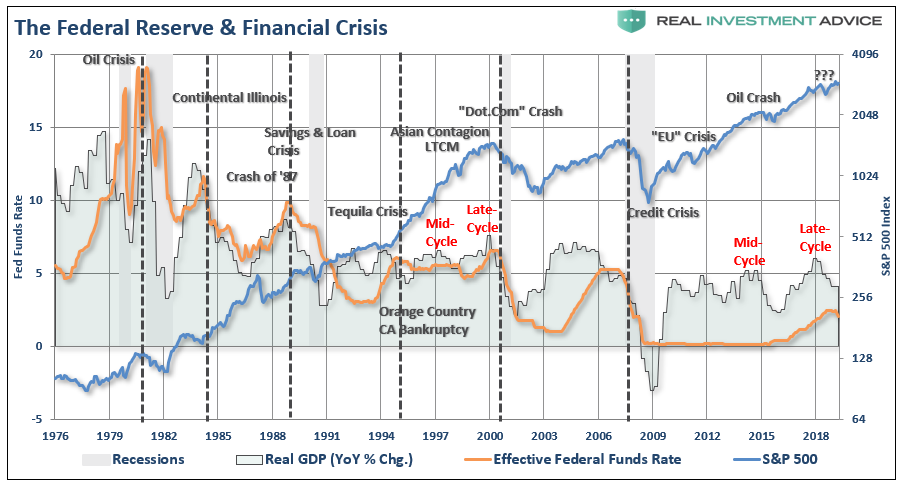

The problem for the Fed, is that while they insist recent rate cuts are “mid-cycle” adjustments, as was seen in 1995 to counter the risk of the Orange County bankruptcy, the reality is the “mid-cycle” has long been past us.

With the Fed cutting rates, injecting weekly records of liquidity into the system, at a time where economic data has clearly taken a turn for the worse, the situation may “not be in as good of a place” as we have been told.

Being a little more cautious, taking in some profits, and rebalancing risks continues to be our recipe for navigating the markets currently.

If you need help or have questions, we are always glad to help. Just email me.

See you next week.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now!

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

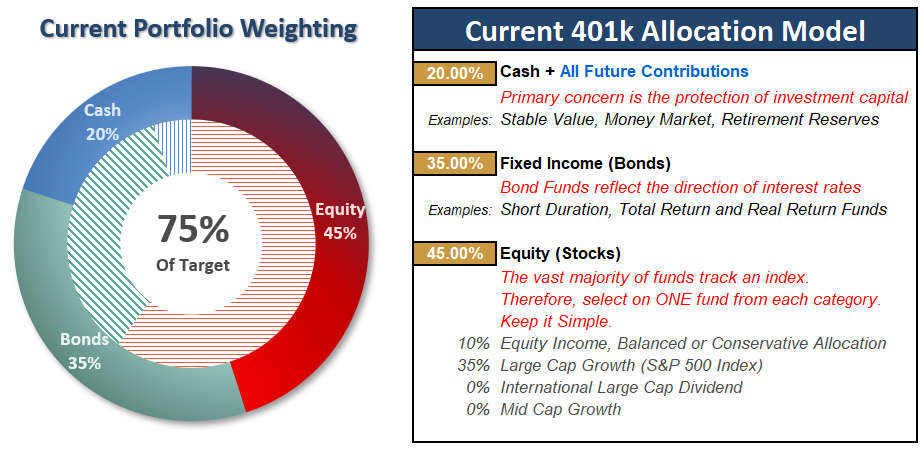

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Trade Deal Done?

As we stated last week:

“The market rallied on at the end of last week on “bad news” which gave the market “hope” the Fed would more aggressively cut rates. This is a short-term boost with a long-term negative outcome. Low rates are not conducive to economic growth, and the Fed cutting rates aggressively cuts financial incentive in the economy and leads to recessions in the economy.

We advise caution, but suggest remaining weighted toward equity exposure for now. Despite the rally this week, there is some risk heading into the ‘trade deal’ next week. As noted, we expect a deal to be completed which will provide a lift to equities but we recommend weighting for the news before adding to risk.”

Once we get a handle on how the markets are going to react to all of the news, please read the main body of the missive above, we will look to increase overall equity exposure accordingly. In the meantime, you can prepare for the next moves by taking some actions if you haven’t already.

- If you are overweight equities – Hold current positions but remain aware of the risk. Take some profits, and rebalance risk to some degree if you have not done so already.

- If you are underweight equities or at target – rebalance risks and hold positioning for now.

If you need help after reading the alert; do not hesitate to contact me.

401k Plan Manager Beta Is Live

Become a RIA PRO subscriber and be part of our “Break It Early Testing Associate” group by using CODE: 401 (You get your first 30-days free)

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

I have gotten quite a few plans, so keep sending them and I will include as many as we can.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.