-

When I was growing up, my father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books but through experience. One of my favorite pieces of “wisdom” was:

“A sure-fire ‘no lose’ proposition is doing exactly the opposite of whatever ‘no lose’ proposition is being proposed.”

Of course, back then, he was mostly giving me “life advice” about not following along with my stupid-ass friends who were always up elbows deep in mischief.

However, that advice also holds true with the financial markets currently. As I have noted over the last couple of weeks (read this and this) the “bulls” certainly seem to regained control of the markets as new highs were reached on Monday. As I stated, between the Fed cutting rates, reigniting “not-QE,” and the President following our script of putting the “trade war” to rest, “what is there NOT to love if you are a bull.”

While we have begun to opportunistically increase our the equity exposures in our portfolios, we are cognizant there are currently several warning signs investors should consider before buying into the “bullish view.”

Here are four to consider.

Warning 1: Conflicting Confidence

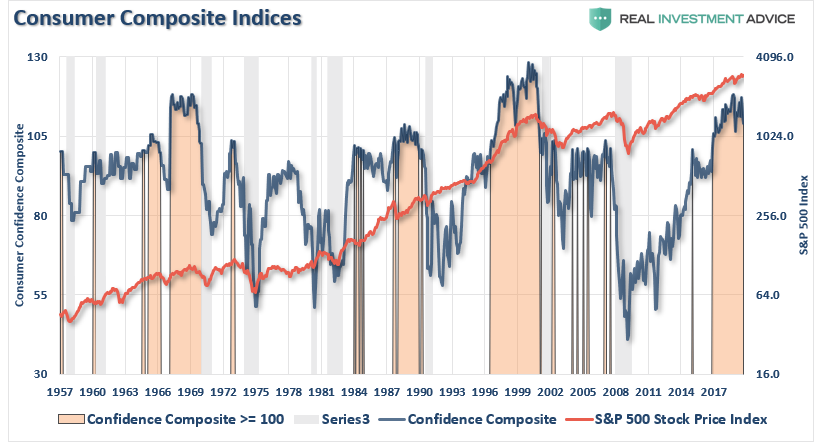

There are several different surveys of confidence, which all currently show the same thing. Individuals are extremely optimistic on just about everything. Recently, I discussed our composite confidence indicator:

“The latest release of the University of Michigan’s consumer sentiment survey rose to a three-month high of 96, beat consensus expectations, and remains near record levels. The chart below shows our composite confidence index, which combines both the University of Michigan and Conference Board measures. The chart compares the composite index to the S&P 500 index with the shaded areas representing when the composite index was above a reading of 100.”

“On the surface, this is bullish for investors. High levels of consumer confidence (above 100) have correlated with positive returns from the S&P 500.”

As I have discussed many times previously, the stock market rise has NOT lifted all boats equally. More importantly, the surge in confidence is a coincident indicator and more suggestive, historically, of market peaks as opposed to further advances.

As David Rosenberg, the chief economist at Gluskin Sheff previously wrote:

‘For an investment community that typically lives in the moment and extrapolates the most recent experience into the future, it would only fall on deaf ears to suggest that peak confidence like this and peak market pricing tend to coincide with each other.”

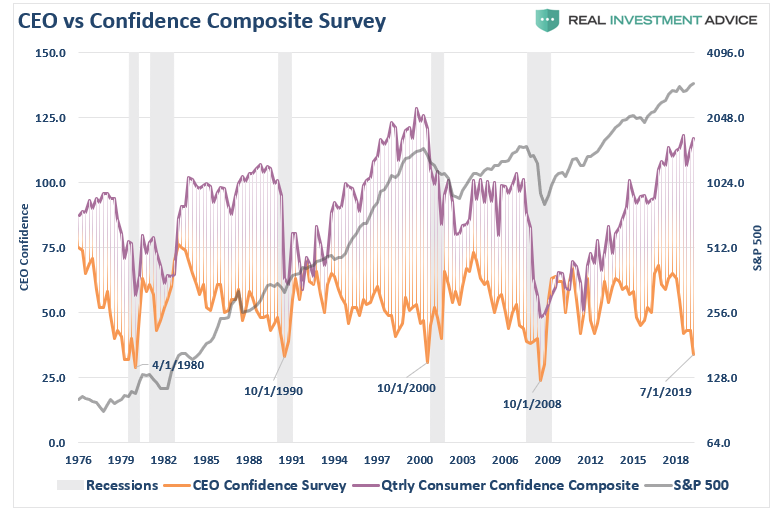

However, that confidence may be short-lived as “CEO Confidence” is near historic lows. As we covered in our previous analysis, this divergence should not be dismissed. A quick look at history shows this historical relationship between these two measures of confidence. The divergence is seen every time prior to the onset of a recession.

Notice that CEO confidence leads consumer confidence by a wide margin. This lures bullish investors, and the media, into believing that CEO’s really don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

“I’m sorry, we think you are really great, but I have to let you go.”

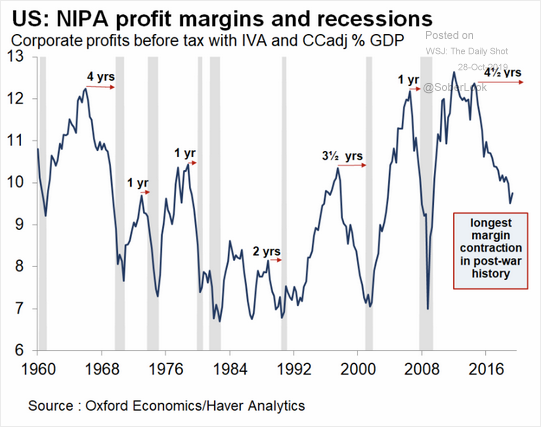

Warning 2 – All Hat, No Cattle

For those of you unfamiliar with Texas sayings, “all hat, no cattle” means that someone is acting the part without having the “stuff” to back it up. Just wearing a “cowboy hat,” doesn’t make you a “cowboy.”

One of the problems for the “bulls” currently is that while asset prices are hitting record highs, profit margins aren’t.

In other words, investors, in their rush to “be long the market,” are paying ever-higher prices for each dollar of profit being produced. The problem, of course, is falling profit margins, not surprisingly, have preceded recessions and bear markets.

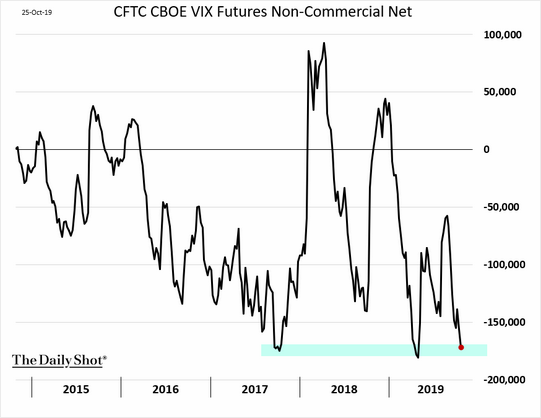

We will discuss valuations more in a moment, but the important point here is that investors are increasingly taking on “risk,” without consideration for the consequences. As shown, below speculators are now extremely “short volatility” which suggests there is no fear of a correction. Unfortunately, for the bulls, this has typically been a pretty reliable contrarian indicator.

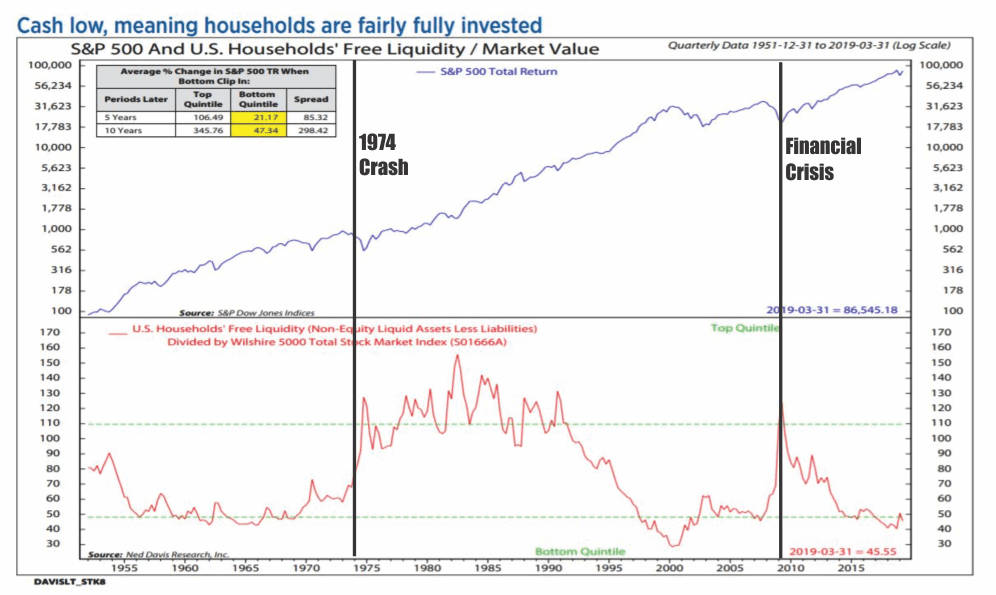

Much of the existing “complacency” stems from the belief the Fed will continue to lower interest rates and provide ongoing support for asset prices. After all, this is what happened as the Federal Reserve kept interest rates suppressed after the financial crisis. However, the difference between now and then is that individuals are currently fully invested in the financial markets.

“Cash is low, meaning households are fairly fully invested.” – Ned Davis

In other words, the “pent up” demand for equities is no longer available to the magnitude that existed following the financial crisis which supported the 300% rise in asset prices.

While investors may want to believe asset prices can only go higher, this is the very basis of the “Greater Fool Theory.” At some point, someone, is going to be left holding the bag.

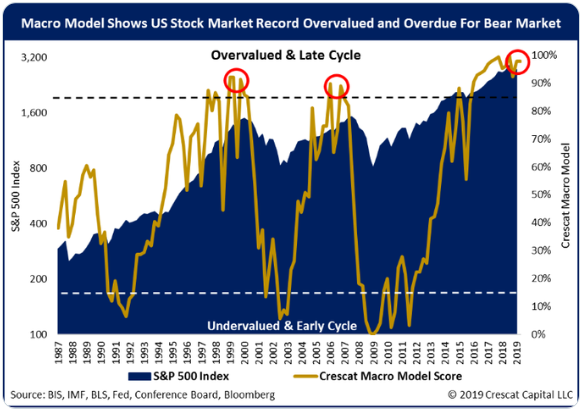

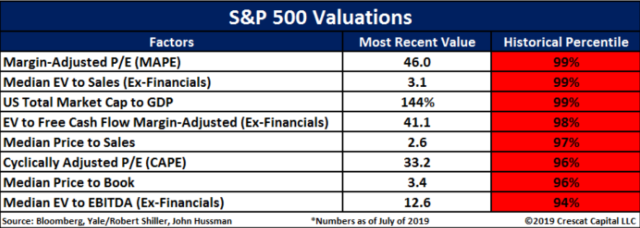

Warning 3 – Valuations

With the global levels of over-valuation of stocks and bonds, combined with excessive optimism, and leverage as noted above, such has set the stage for exceedingly low returns over the next decade, or longer. As our friends over at Crescat Capital recently noted, valuations are anything but “cheap.”

What happens next should be obvious: unless one assumes that the laws of economics and finance are irreparably broken; a deep recession and a market crash are inevitable, especially after the longest central bank-sponsored bull market in history.

However, in the short-term, valuations, as discussed previously, are a poor market timing device for investors. However, from a long-term investment perspective, valuations mean a great deal as it relates to expected returns.

With earnings estimates being revised lower, economic growth remaining weak, and high levels of complacency, the importance of valuations should not be readily dismissed.

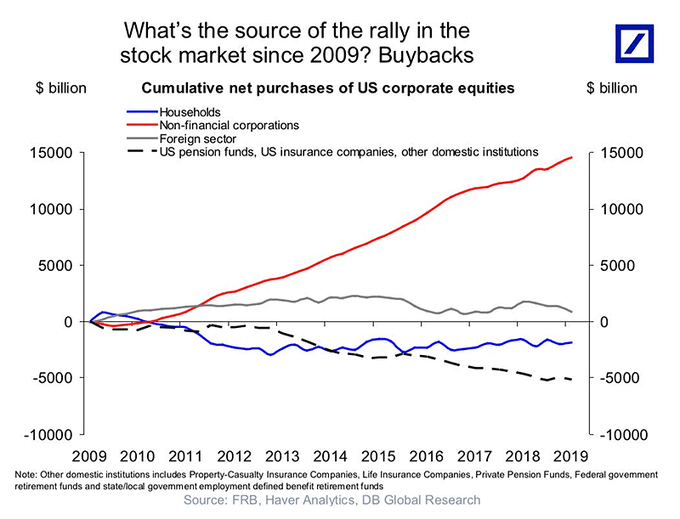

Warning 4 – Share Buy Backs

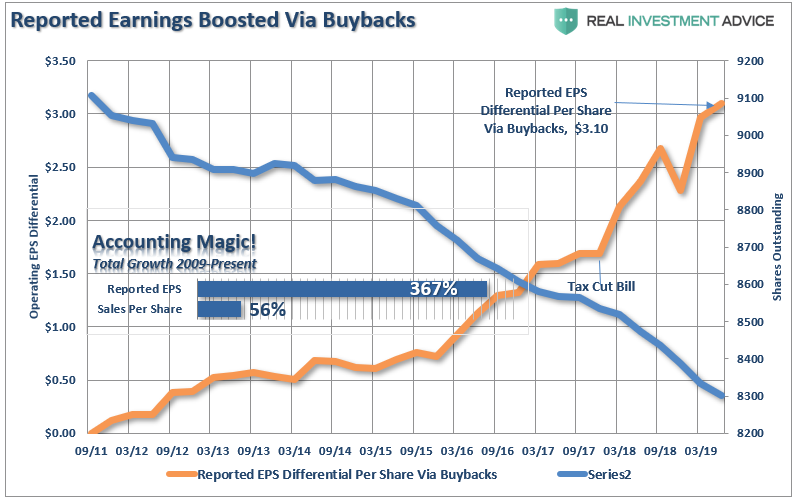

We have discussed the issue of “share buybacks” numerous times and the distortion caused by the use of corporate cash to lower shares outstanding to increase earnings per share.

“The reason companies spend billions on buybacks is to increase bottom-line earnings per share which provides the ‘illusion’ of increasing profitability to support higher share prices. Since revenue growth has remained extremely weak since the financial crisis, companies have become dependent on inflating earnings on a ‘per share’ basis by reducing the denominator. As the chart below shows, while earnings per share have risen by over 360% since the beginning of 2009; revenue growth has barely eclipsed 50%.”

The problem with this, of course, is that stock buybacks create an illusion of profitability. However, for investors, the real issue is that almost 100% of the net purchases of equities has come from corporations.

The problem is that corporate spending binge may be coming to an end. Via Goldman Sachs:

“Corporate buybacks are ‘plummeting’ as companies tighten their purse strings, and it could have a big impact on the market, Goldman Sachs warned in a note to clients.

In the second quarter, S&P 500 share buybacks totaled $161 billion, about 18% less than the first quarter, the firm found. The amount spent on buybacks this year is down 17% from a year earlier.

For 2019, total buybacks will drop 15% to $710 billion, and in 2020 they see a 5% decline to $675 billion.”

While this may not sound like much, it suggests that a primary support for higher asset prices is being removed. Of course, if a recession sets in, share repurchases could easily cease altogether.

If They Don’t “Buy & Hold” – Why Should You?

Of course, these are just “warning signs.” None them suggest that the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But they are warning signs nonetheless. Past experience suggests that future returns are likely to be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30 years, and whatever time you personally have left to your financial goals.

While much of the mainstream analysis suggests you should “invest for the long-term,” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple. No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If the professionals are looking at “risk,” and planning on how to protect their capital from losses when things go wrong, then why aren’t you?

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.