-

With the market breaking out to all-time highs, the media has started to once again reach for their party hats as headlines suggest clear sailing for investors ahead.

After all, why not?

- The Federal Reserve cut rates for the 3rd time this year.

- The Fed is also back in the “QE” game of buying bonds.

- President Trump has “surrendered” to China in order to end the “trade war.”

- Corporate stock buybacks are on track for the second largest year on record.

- Earnings, due to buybacks, are beating lowered estimates,

- Consumer sentiment remains near record highs; and,

- Economic data is weak, but not terrible.

With those supports in place, markets are pushing new highs as we discussed would likely be the case last month:

“Assuming we are correct, and Trump does indeed ‘cave’ into China in mid-October to get a ‘small deal’ done, what does this mean for the market.

The most obvious impact, assuming all ‘tariffs’ are removed, would be a psychological ‘pop’ to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year. “

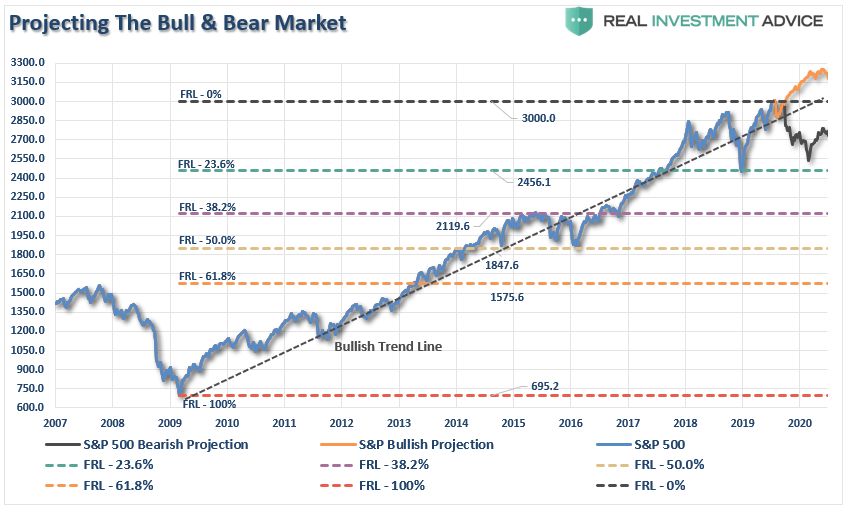

This is not the first time we presented analysis for a “bull run” to 3300. To wit:

“The Bull Case For 3300

- Momentum

- Stock Buybacks

- Fed Rate Cuts

- Stoppage of QT

- Trade Deal”

All the boxes have been checked.

Even more important than these supports, is the overall psychology of the markets. As Doug Kass recently noted, investors “want to believe.”

“’Price has a way of changing sentiment.’ – The Divine Ms M.

- They want to believe that the trade talks between the U.S. and China will be real this time.

- They want to believe that there is no ‘earnings recession’ even though S&P profits through the first half of 2019 are slightly negative (year over year) and that S&P EPS estimates have been regularly reduced as the year has progressed.

- They want to believe that stocks are cheap relative to bonds even though there is little natural price discovery as central banks are artificially impacting global credit markets and passive investing is artificially buoying equities.

- They want to believe that technicals and price are truth – even though the markets materially influenced by risk parity and other products and strategies that exaggerates daily and weekly price moves.

- They want to believe that today’s economic data is an “all clear” – forgetting the weak ISM, the lackluster auto and housing markets, the U.S. manufacturing recession, and the continued overseas economic weakness.

- They want to believe that, given no U.S. corporate profit growth, that valuations can continue to expand (after rising by more than three PEs year to date).

- They want to believe though that the EU broadly has negative interest rates and Germany is approaching recession (while the peripheral countries are in recession) – that the Fed will be able to catalyze domestic economic growth through more rate cuts.

- They want to believe that the U.S. can be an oasis of growth even though the economic world is increasingly flat and interconnected and the S&P is nearly 50% dependent on non U.S. economies.”

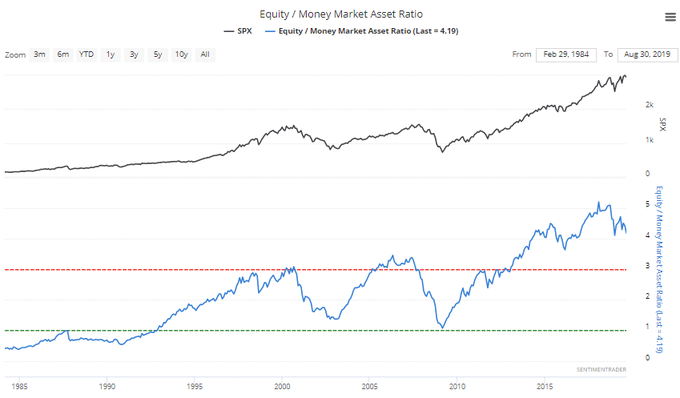

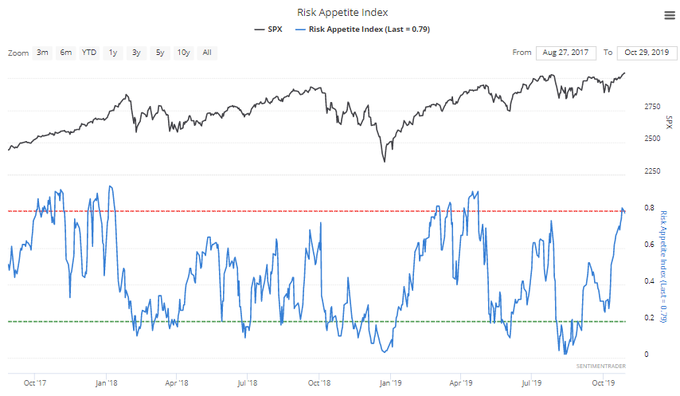

The “need to believe” is a powerful force which has lured investors back into the “warm waters of complacency.” The sentiment is certainly understandable given the market’s advance which has triggered investor’s “Pavlovian” response to the ringing of “the bell.” This was shown recently by a series of charts from Sentiment Trader.

Everyone Back In The Pool

As asset prices have escalated, so have individual’s appetite to chase risk. The herding into equities suggests that investors have thrown caution to the wind.

With cash levels at the lowest level since 1997, and equity allocations near the highest levels since 1999 and 2007, it suggests investors are now functionally “all in.”

With net exposure to equity risk by individuals at historically high levels, it suggests two things:

- There is little buying left from individuals to push markets marginally higher, and;

- The stock/cash ratio, shown below, is at levels normally coincident with more important market peaks.

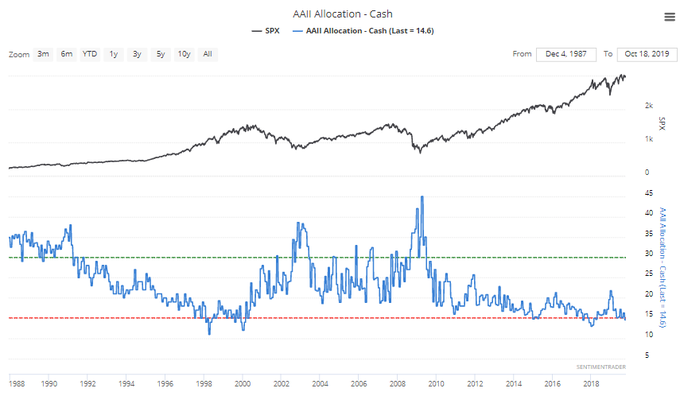

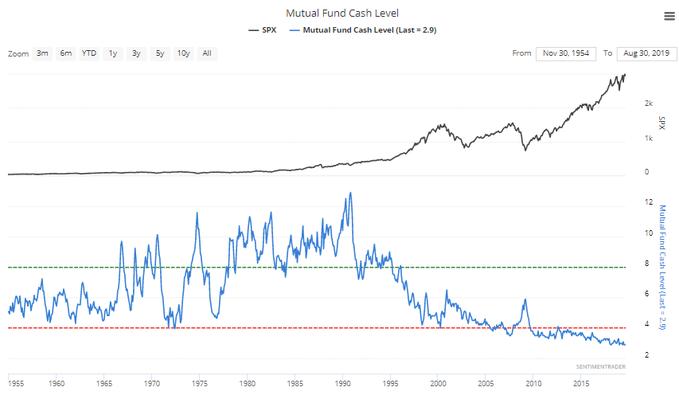

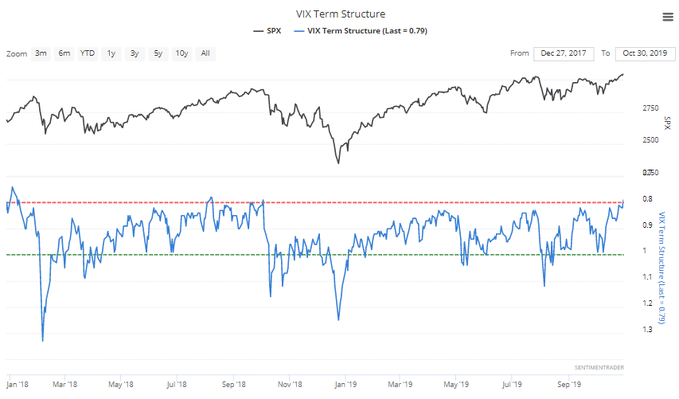

But it isn’t just individual investors that are “all in,” but professionals as well.

Importantly, while investors are holding very little “cash,” they have taken on a tremendous amount of “risk” to chase the market. It is worth noting the current levels versus previous market peaks.

Importantly, what these charts clearly show is there is nothing wrong with aggressively chasing the markets, until there is.

As Doug Kass often states: “Risk happens fast.”

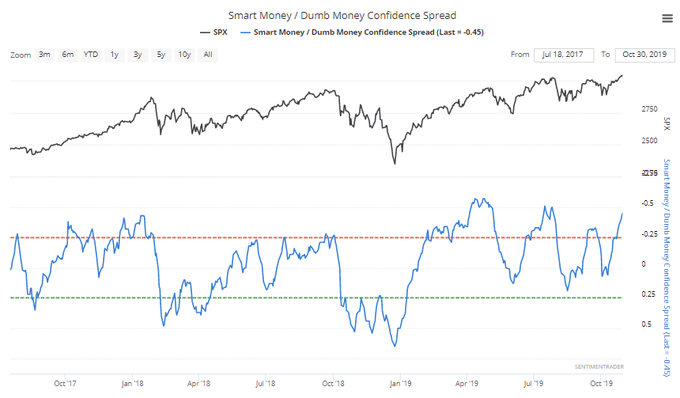

Which brings me to something Michael Sincere’s once penned:

“At market tops, it is common to see what I call the ‘high-five effect’ — that is, investors giving high-fives to each other because they are making so much paper money. It is happening now. I am also suspicious when amateurs come out of the woodwork to insult other investors.”

Michael’s point is very pertinent, particularly today. As shown in the two charts below, investors are clearly “high-fiving” each other as risk aversion hits near record lows.

While the fundamental backdrop of the market has materially weakened, the confidence of individuals has surged. Of course, as the markets continue their relentless rise, investors feel “bullet proof” as investment success breeds overconfidence.

As Sentiment Trader shows, retail investors (dumb money) are currently pushing levels which have typically denoted short-term market peaks, This should not be surprising as individuals, with regularity, “buy tops and sell bottoms.”

Strongly rising asset prices, particularly when driven by emotional exuberance, “hides” investment mistakes in the short term. Poor, or deteriorating, fundamentals, excessive valuations and/or rising credit risk is often ignored as prices increase. Unfortunately, it is after the damage is done that the realization of those “risks” occurs.

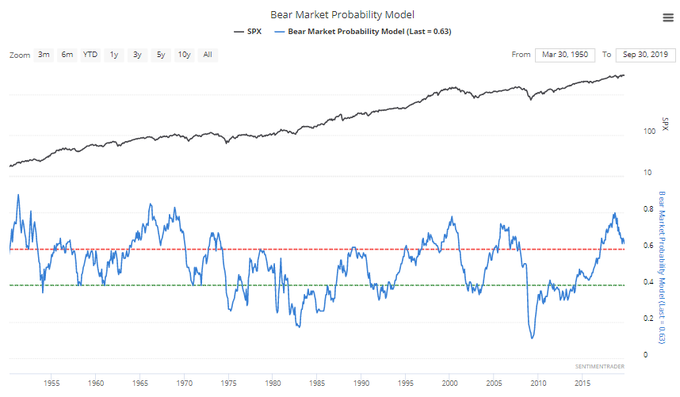

Regardless of what you believe, a “bear market” will eventually come. We don’t/won’t know what will trigger it, but some unforeseen exogenous event will start a “flight to safety” by investors. The chart below is the “bear market” probability model from Sentiment Trader. Importantly, note the index peaks a couple of years before the onset of a “bear market.” (The last peak was in 2015)

Here is the point, despite ongoing commentary about mountains of “cash on the sidelines,” this is far from the case. This leaves the current advance in the markets almost solely in the realm of Central Bank activity.

Again…there is nothing wrong with that, until there is.

Which brings us to the ONE question everyone should be asking.

“If the markets are rising because of expectations of improving economic conditions and earnings, then why are Central Banks pumping liquidity like crazy?”

Despite the best of intentions, Central Bank interventions, while boosting asset prices may seem like a good idea in the short-term, in the long-term it harms economic growth. As such, it leads to the repetitive cycle of monetary policy.

- Using monetary policy to drag forward future consumption leaves a larger void in the future that must be continually refilled.

- Monetary policy does not create self-sustaining economic growth and therefore requires ever-larger amounts of monetary policy to maintain the same level of activity.

- The filling of the “gap” between fundamentals and reality leads to consumer contraction and ultimately, a recession as economic activity recedes.

- Job losses rise, wealth effect diminishes, and real wealth is destroyed.

- The middle-class shrinks further.

- Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

- Wash, Rinse, Repeat.

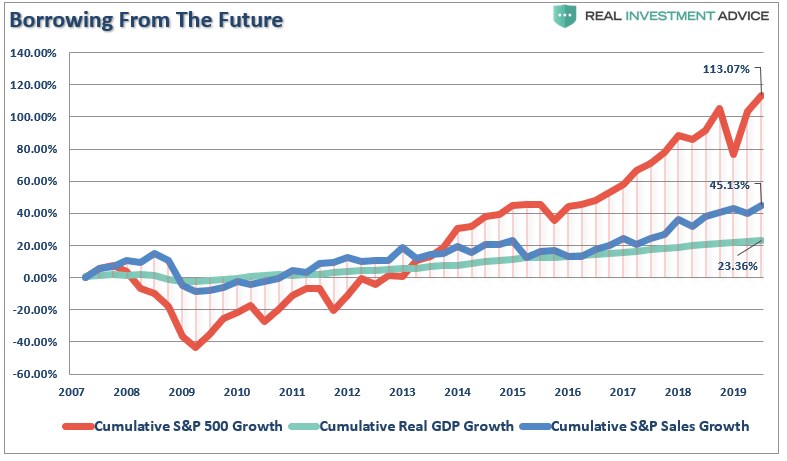

If you don’t believe me, here is the evidence.

The stock market has returned more than 100% since the 2007 peak, which is more than 2.5x the growth in corporate sales and almost 5x more than GDP. The all-time highs in the stock market have been driven by the $4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP.

What could possibly go wrong?

However, whenever there is a discussion of valuations, it is invariably stated that “low rates justify higher valuations.”

Maybe.

But the argument suggests rates are low BECAUSE the economy is healthy and operating near full capacity.

The reality is quite different.

The main contributors to the illusion of permanent prosperity have been a combination of artificial and cyclical factors. Low interest rates, when growth is low, suggests that no valuation premium is “justified.“’

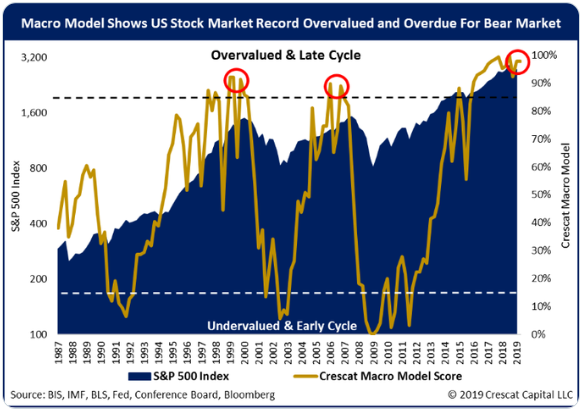

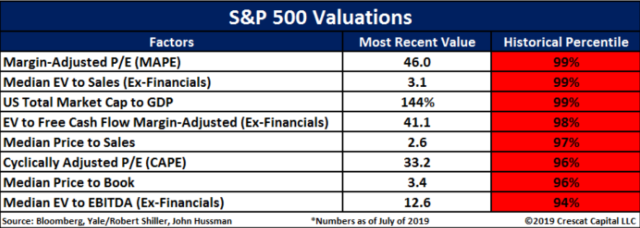

Currently, investors are taking on excessive risk, and thereby virtually guaranteeing future losses, by paying the highest S&P 500 price/revenue ratio in history and the highest median price/revenue ratio in history across S&P 500 component stocks. This valuation problem was discussed last week by our friends at Crescat Capital. To wit:

There are virtually no measures of valuation which suggest making investments today, and holding them for the next 20-30 years, will work to any great degree.

That is just the math.

The markets are indeed bullish by all measures. From a trading perspective, holding risk will likely pay off in the short-term. However, over the long-term, the “house will win.”

Just remember, at market peaks – “everyone’s in the pool.”

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.