-

- The “QE, Not QE” Rally Is ON

- How To Play It

- What Happens Next

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

The “QE, Not QE” Rally Is On

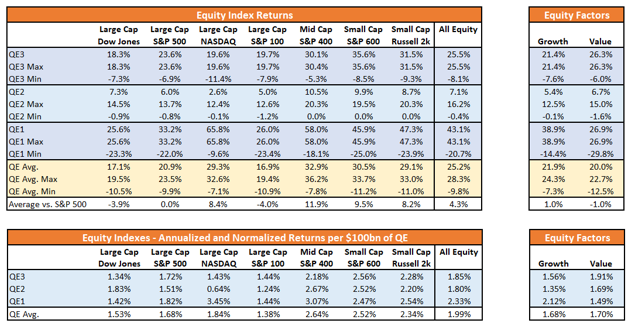

Just recently, we released a study for our RIAPro Subscribers (30-Day Free Trial) on historical QE programs and what sectors, markets, and commodities perform best. (If you subscribe for a 30-day Free Trail you can read the entire report “An Investor’s Guide To QE-4.”)

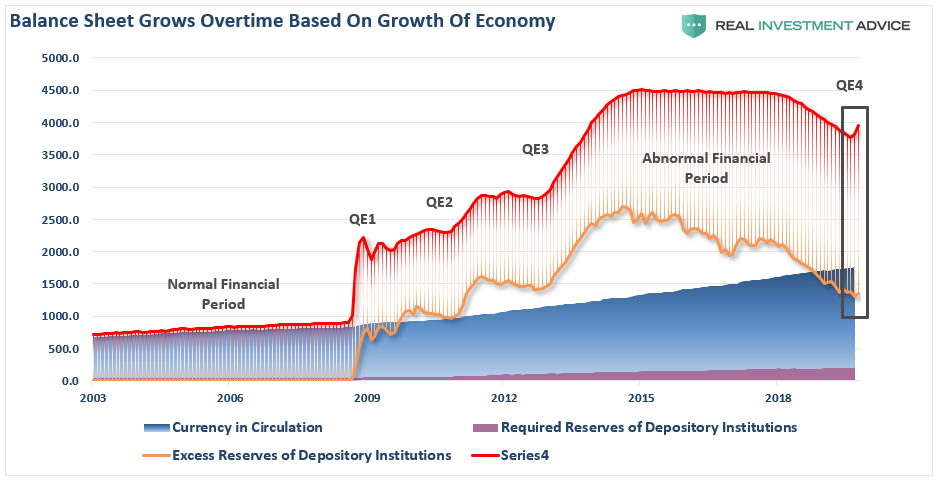

“On October 9, 2019, the Federal Reserve announced a resumption of quantitative easing (QE). Fed Chairman Jerome Powell went to great lengths to make sure he characterized the new operation as something different than QE. Like QE 1, 2, and 3, this new action involves a series of large asset purchases of Treasury securities conducted by the Fed. The action is designed to pump liquidity and reserves into the banking system.

Regardless of the nomenclature, what matters to investors is whether this new action will have an effect on asset prices similar to prior rounds of QE. For the remainder of this article, we refer to the latest action as QE 4.

To quantify what a similar effect may mean, we start by examining the performance of various equity indexes, equity sectors, commodities, and yields during the three prior QE operations. We then normalize the data for the duration and amount of QE to project what QE 4 might hold in store for the assets.”

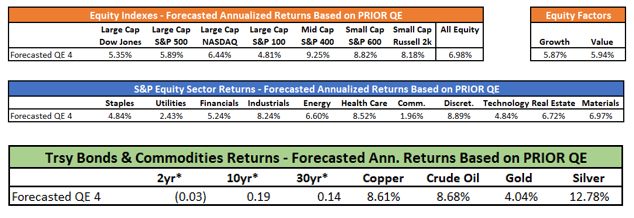

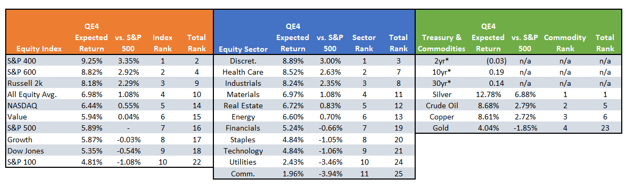

The following is one of the tables from article.

As you will notice, all major markets increased in value during QE-1, 2, and 3.

Since the market increased each time the Fed engaged in monetary programs, it should not be surprising investors now have a “Pavlovian” response to the Fed “ringing the bell.”

Over the last month, we have been discussing the end of the year rally which would be supported by both the Fed, and a “trade deal.”

This past week, as expected, headlines were floated which suggested that tariffs would be reduced in exchange for essentially nothing, This is precisely the case we laid out in September:

“Trump can set aside the last 20%, drop tariffs, and keep market access open, in exchange for China signing off on the 80% of the deal they already agreed to.

For Trump, he can spin a limited deal as a ‘win’ saying ‘China is caving to his tariffs’ and that he ‘will continue working to get the rest of the deal done.’ He will then quietly move on to another fight, which is the upcoming election, and never mention China again. His base will quickly forget the ‘trade war’ ever existed.

Kind of like that ‘Denuclearization deal’ with North Korea.”

We followed that in early October by laying out the case for the “trade deal” to push the markets to 3300:

“Assuming we are correct, and Trump does indeed ‘cave’ into China in mid-October to get a ‘small deal’ done, what does this mean for the market.

The most obvious impact, assuming all ‘tariffs’ are removed, would be a psychological ‘pop’ to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year.”

Then, just two week’s ago, as the Fed went into action:

“Clearly, the Fed is concerned about something other than the impact of ‘Trump’s Trade War’ on the economy. In the meantime, the injection of liquidity continues to support asset prices as the litany of ‘algo’s’ which drive -80% of the trading on Wall Street, respond to more liquidity.”

That is where we are today.

The questions now are:

- How do you play it; and,

- What happens next?

How To Play It

As we have been noting over the last month, with the Fed’s more accommodative positioning, we continue to maintain a long-equity bias in our portfolios currently. We have reduced our hedges, along with some of our more defensive positioning. We are also adding opportunistically, to our equity allocations, even as we carry a slightly higher than normal level of cash along with our fixed income positioning.

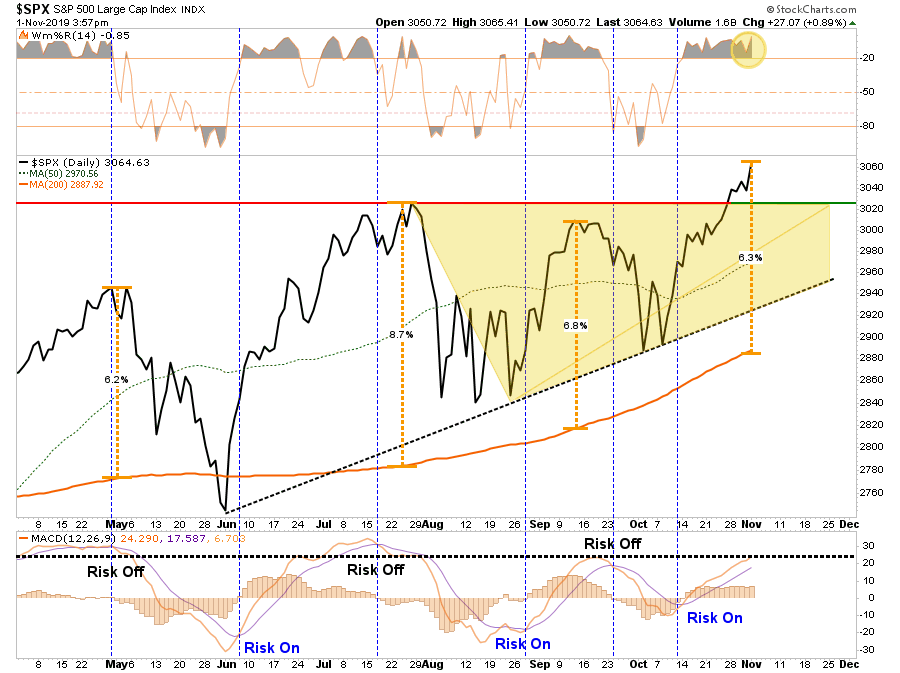

Currently, it will likely pay to remain patient as we head into the end of the year. With a big chunk of earnings season now behind us, and economic data looking weak heading into Q4, the market has gotten a bit ahead of itself over the last two weeks.

On a short-term basis, the market is now more than 6% above its 200-dma. These more extreme price extensions tend to denote short-term tops to the market, and waiting for a pull-back to add exposures has been prudent.

Also, the majority of our indicators are back to more extreme overbought readings, which have typically denoted short-term tops at a minimum.

As I noted last week:

“Given the markets tend to pullback just before Thanksgiving, and during the second week of December, we will have a better opportunity increase allocations if we are patient.“

Once we see that pullback, or even a slight consolidation of the recent advance, we can increase allocations in portfolios towards more equity related exposure.

This begs the question of “what to buy,” which brings us back to our recent RIAPRO.NET article:

“If we assume that assets will perform similarly under QE 4, we can easily forecast returns using the normalized data from above. The following three tables show these forecasts. Below the tables are rankings by asset class as well as in aggregate. For purposes of this exercise, we assume, based on the Fed’s guidance, that they will purchase $60 billion a month for six months ($360 billion) of U.S. Treasury Bills.

The expected top five performers during QE4 on a normalized basis from highest to lowest are: Silver, S&P 400, Discretionary stocks, S&P 600, and Crude Oil.

I would highly suggest reading the whole article.

What Happens Next?

Michael Lebowitz, CFA recently penned:

“A Honus Wagner baseball card from 1909 was recently auctioned for over $3 million. While that may seem like a lot of money, it is not necessarily expensive. A baseball card is nothing more than paper and ink with no real value. Its street value, or price, is based on the whims of collectors. “Whim” is impossible to value.

Stocks are not baseball cards. Stocks represent ownership in a corporation, and therefore, their share prices are based on a future series of expected earnings and cash flows. Further, there are many other types of investments that serve not only as alternatives, but provide a means to assess relative value.

Today, investors are trading stocks on a “whim,” with scant attention to their value. Unlike a baseball card, when a stock’s street value rises much more than its real value, an inevitable correction will occur. The only question is not if but when will investors realize what they are truly buying.”

There is an important distinction to be made here between “investing” vs. “speculating.”

Benjamin Graham, in his seminal work Security Analysis (1934) defined investing as:

“An operation in which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

The problem is that today, the term “investor” is now being applied ubiquitously to anyone who participates in the stock market. As Graham noted later in “The Intelligent Investor:”

“The newspaper employed the word ‘investor’ in these instances because, in the easy language of Wall Street, everyone who buys or sells a security has become an investor, regardless of what he buys, or for what purpose, or at what price, or whether for cash or on margin.”

To understand “what happens next,” one must understand the difference between “investment” and “speculation.”

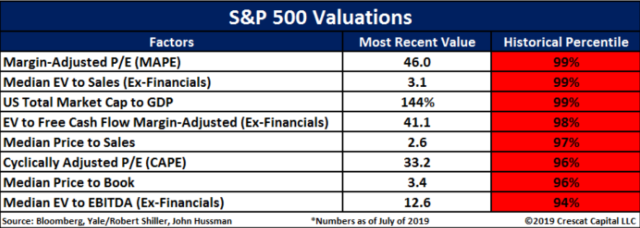

While QE-4 may be driving stocks higher today based on a “whim,” there are two very important difference between QE-4 and QE-1 or 2; 1) stocks are no longer undervalued or 2) under-owned.

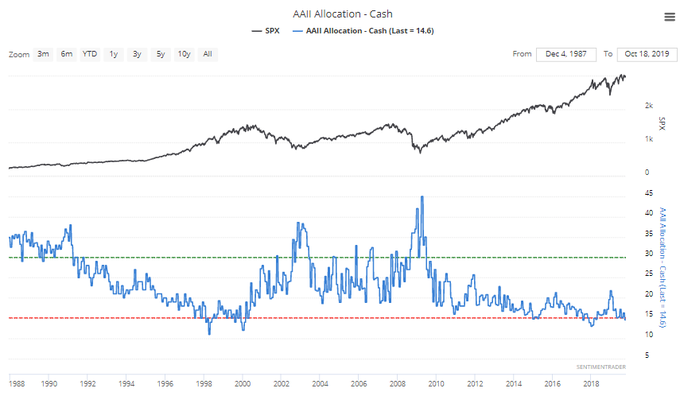

“With cash levels at the lowest level since 1997, and equity allocations near the highest levels since 1999 and 2007, it suggests investors are now functionally ‘all in.’”

With investors paying exceptionally high prices for equity ownership, expected forward returns becomes much more problematic. As we addressed on Thursday:

“The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to ‘remain irrational longer than logic would predict,’ but it never lasts indefinitely.

‘Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.’” – Jeremy Grantham

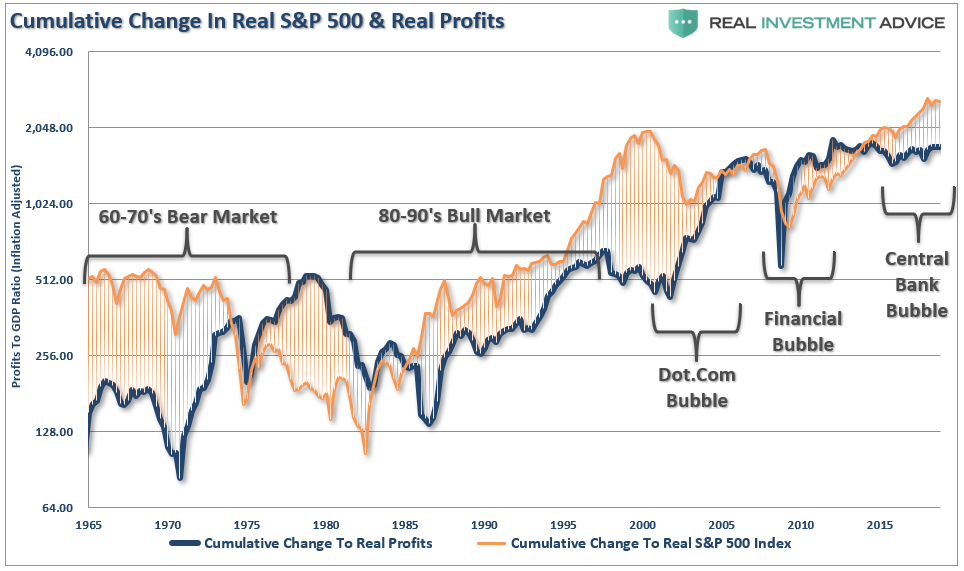

Another way to look at the issue of profits as it relates to the market is shown below. When we measure the cumulative change in the S&P 500 index as compared to the level of profits, we find again that when investors pay more than $1 for a $1 worth of profits there is an eventual mean reversion.

With investors paying more today than at any point in history for each $1 of profit, the next mean reversion will be a humbling event.

That is just math.

However, in the meantime, individuals are “speculating” within the markets based solely on the premise that a “greater fool” will be there when the time comes to sell.

Unfortunately, that is rarely the case.

There are virtually no measures of valuation which suggest making investments today, and holding them for the next 20-30 years, will work to any great degree.

This is the difference between “investing” and “speculation.”

When you think about QE-4, as it relates to your portfolio, you have to consider the premise of valuations, margin of safety, and risk. Yes, the markets are indeed bullish by all measures, and holding risk will likely pay off in the short-term. (speculation) However, over the long-term, the “house will always win.” (investing)

If you need help or have questions, we are always glad to help. Just email me.

See you next week.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now!

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

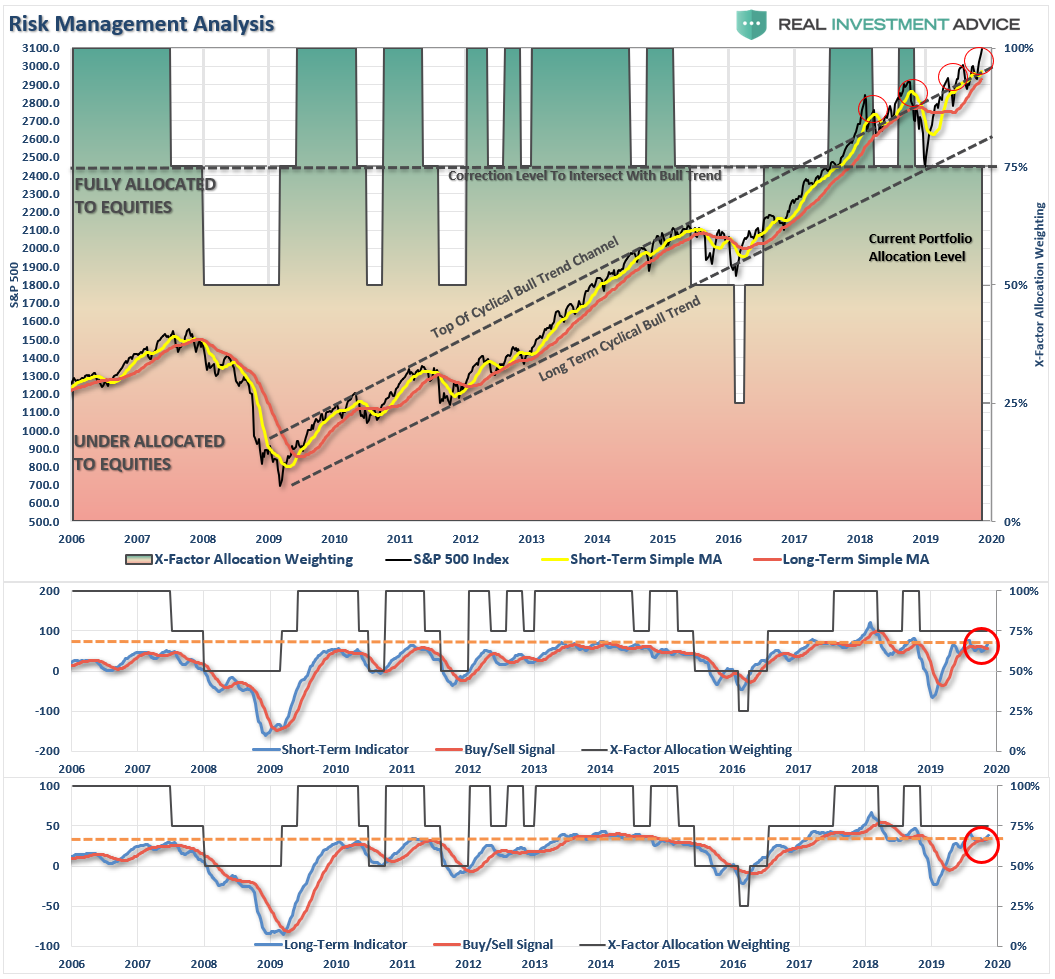

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Watch Your Step Getting On The Bull

Last week we noted:

“Given the ‘bulls’ upper-hand heading into the end of the year, we looking to increase our equity exposure slowly. Given the markets tend to pullback just before Thanksgiving, and during the second week of December, we will have a better opportunity to increase allocations if we are patient.

We need to see a bit of a pullback to reduce the rather excessive extension of the market above the 200-dma, but a pullback that doesn’t break back below the previous highs. Such action will confirm the breakout and suggest our target of 3300 is attainable.”

Please review the chart above. While we are indeed looking to increase equity allocations, thre are reasons to remain cautious.

With the market once again pushing above it’s cyclical bullish trend line, and testing the cycle trend highs from 2007, the risk of a short-term correction action is elevated. Such a correction will provide a much better entry point to add risk to portfolios accordingly.

This week, continue making adjustments to prepare to opportunistically increase equity exposure on a pullback which doesn’t fail at support levels.

- If you are overweight equities – Hold current positions.

- If you are underweight equities – rebalance portfolios to target weights

- If at target weight equities, hold positioning and look for a pullback to increase exposure.

Understand this increase could well be short-lived. The markets have been in a very long consolidation process and the breakout to the upside is indeed bullish. However, we must counter-balance that view with the simple reality we are VERY long in the current economic and market cycle which is where “unexpected” events have destroyed capital in the past.

If you need help after reading the alert; do not hesitate to contact me.

401k Plan Manager Beta Is Live

Become a RIA PRO subscriber and be part of our “Break It Early Testing Associate” group by using CODE: 401 (You get your first 30-days free)

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

I have gotten quite a few plans, so keep sending them and I will include as many as we can.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

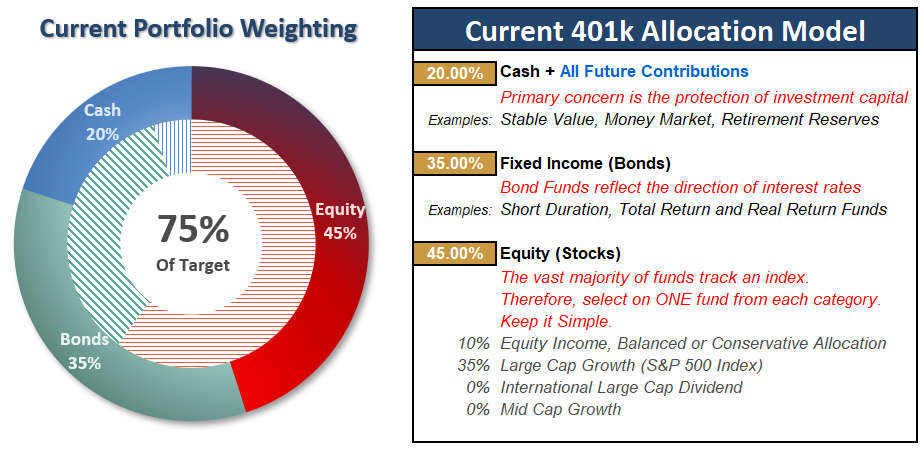

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

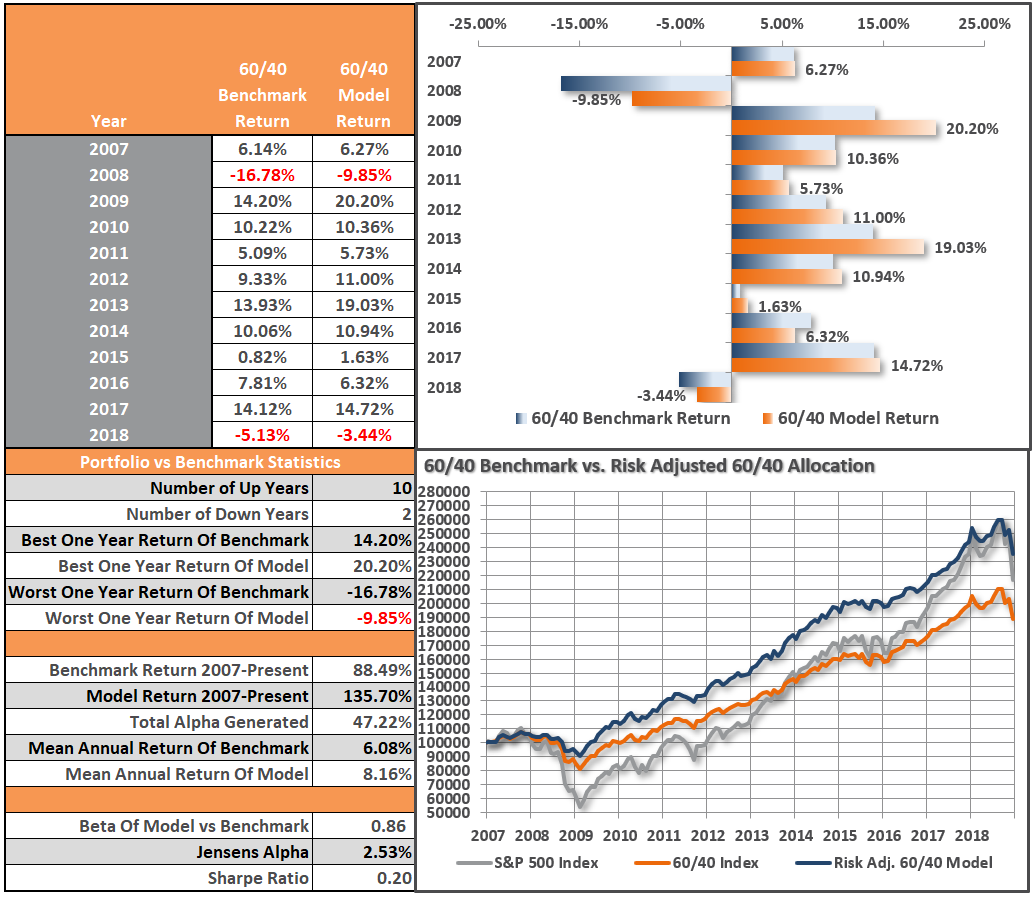

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.