-

- Here Comes The Santa Claus Rally

- When Presidential & Decennial Cycles Collide

- New: Financial Planning Corner

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Here Comes Santa Claus (Rally)

On Friday, the market rallied sharply on the back of a much better than expected employment report and comments from Larry Kudlow that a “trade deal” is near. Given we are now at the last stages of the year where mutual, pension, and hedge funds need to “window dress” for year-end reporting, we removed our small equity hedge from the portfolio for the time being.

A quick word about that employment report.

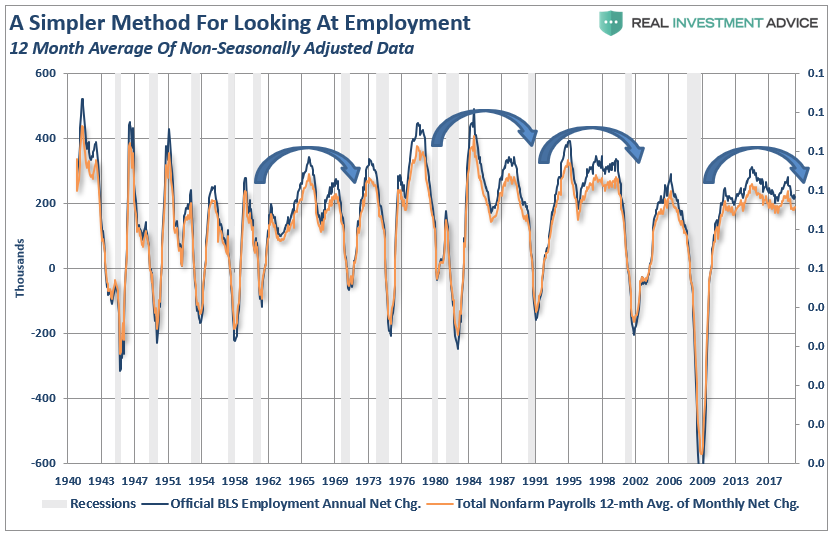

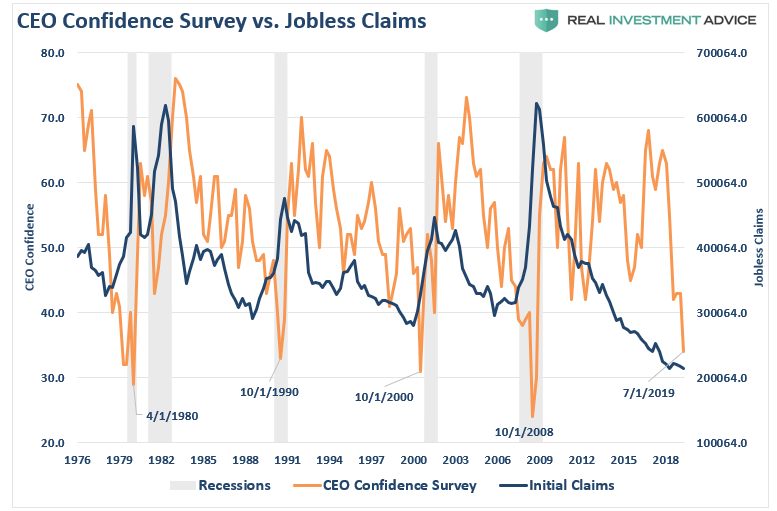

While the headline number was good, it remained primarily a story of auto workers returning to work and continued increases in lower wage-paying jobs and multiple jobholders. Such has been the story of the bulk of this recovery. However, more importantly, the bump did not change the overall dynamics of the job market cycle, which is clearly deteriorating as shown in the chart below.

The key to trend change is CEO confidence which is extremely negative and coincident with employment cycle turns. Note that the end of employment cycles, when compared to CEO confidence, looks very similar at the end of each decade.

Nonetheless, in the short-term, the market dynamics are positive suggesting the market can indeed rally into the end of the year. As noted above, we have removed our equity hedge for now to allow our long-positions to fully benefit from the expected “Santa Claus” rally. (Or if you prefer the more PC version then it would be the expected “Jovial Full-Figured Holiday Person” rally.)

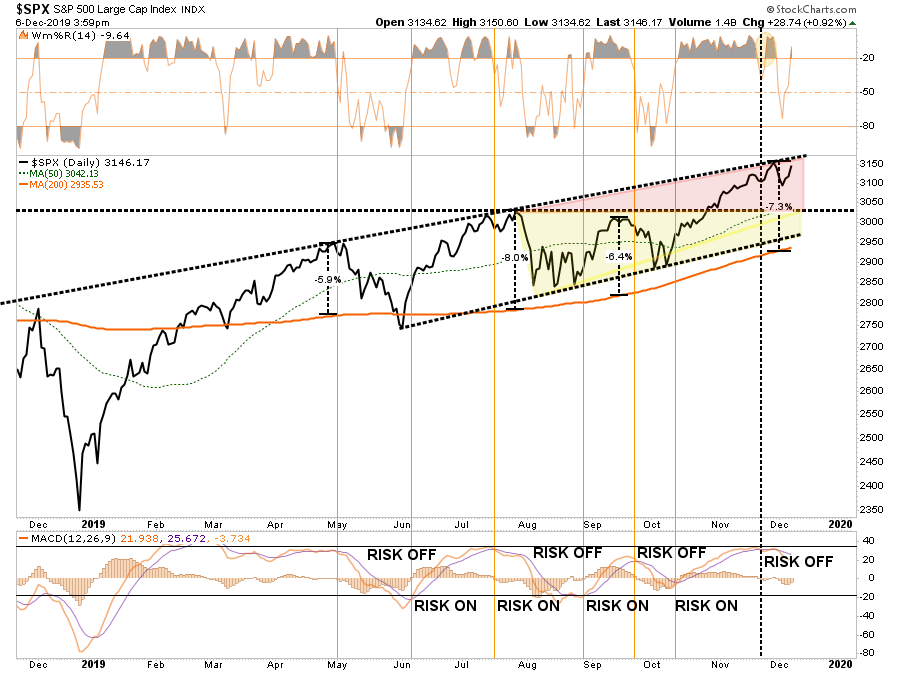

With the market back to short-term overbought, and the short-term “sell signal” still in place, it is possible we could see a bit of a correction next week. However, as we head into the last week of the year, a retest of highs is quite likely.

In the longer-term, as we will discuss more in a moment, the risk remains to the downside. It is highly unlikely there will be a “trade deal” anytime soon, and with the upcoming election, there will likely be increased volatility going into 2020.

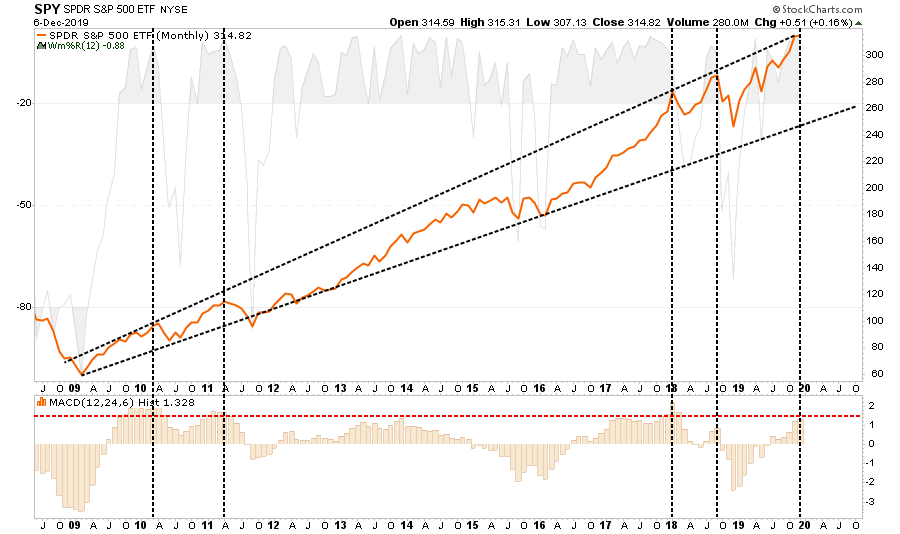

From a purely technical perspective, on a monthly basis, the market is exceedingly overbought and at the top of the long-term trend channel. When these two conditions have been filled previously, we have seen fairly sharp corrections within the confines of the bullish trend.

With QE-4 in play, the bias remains to the upside keeping our target of 3300 on the S&P 500 in place. This is particularly the case as we head further into the seasonally strong period combined with an election year cycle.

Currently, we are exploring the energy space in particular where there is value being generated after the long drought of interest in energy-related stocks.

We have just released a research report for our RIAPro Subscribers (30-Day Free Trial) where we are looking for an opportunity. Here is a snippet:

“A decline in the dividend yield to the norm, assuming the dividend payout is unchanged, would result in a price increase of 13.17% for AMLP. Alternatively, if oil declined about 20% in value, the current AMLP dividend yield would then be fairly priced. We consider this a significant margin of safety should the price of oil fall, as it likely would if the U.S. enters a recession in the near future.”

When Presidential & Decennial Cycle Collide

There have been quite a few articles out lately suggesting that in 2020 the 10-year bull market is set to continue because it is a presidential election year. This sounds great in theory, but Wall Street and the financial media always suggest that next year is going to be another bullish year.

However, there are a lot of things that will need to go “right” next year from:

- Avoidance of a recession

- A rebound in global economic growth

- The consumer will need to expand their current debt-driven consumption

- A marked improvement in both corporate earnings and corporate profitability

- A reduction or removal in current tariffs, and;

- The Fed continues to remain ultra-accommodative to the markets.

These are all certainly possible, but given we are currently into both the longest, and weakest, economic expansion in history, and the longest bull market in history, the risks of something going wrong have certainly risen.

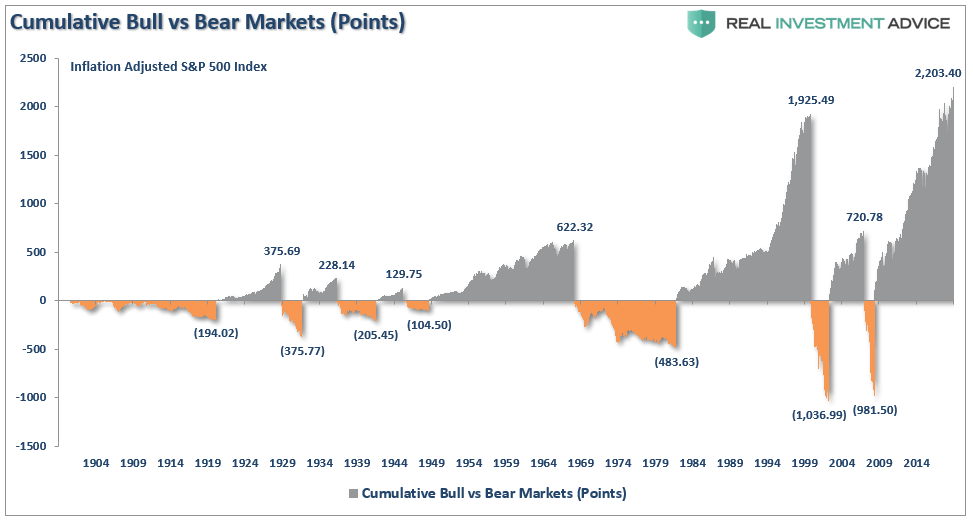

(While most financial media types present bull and bear markets in percentages, which is deceiving because a 100% and a 50% loss are the same thing, it worth noting what happens to investors by viewing cumulative point gains and losses. In every case the majority of the previous point gain is lost.)

However, what about the election coming up in less than a year?

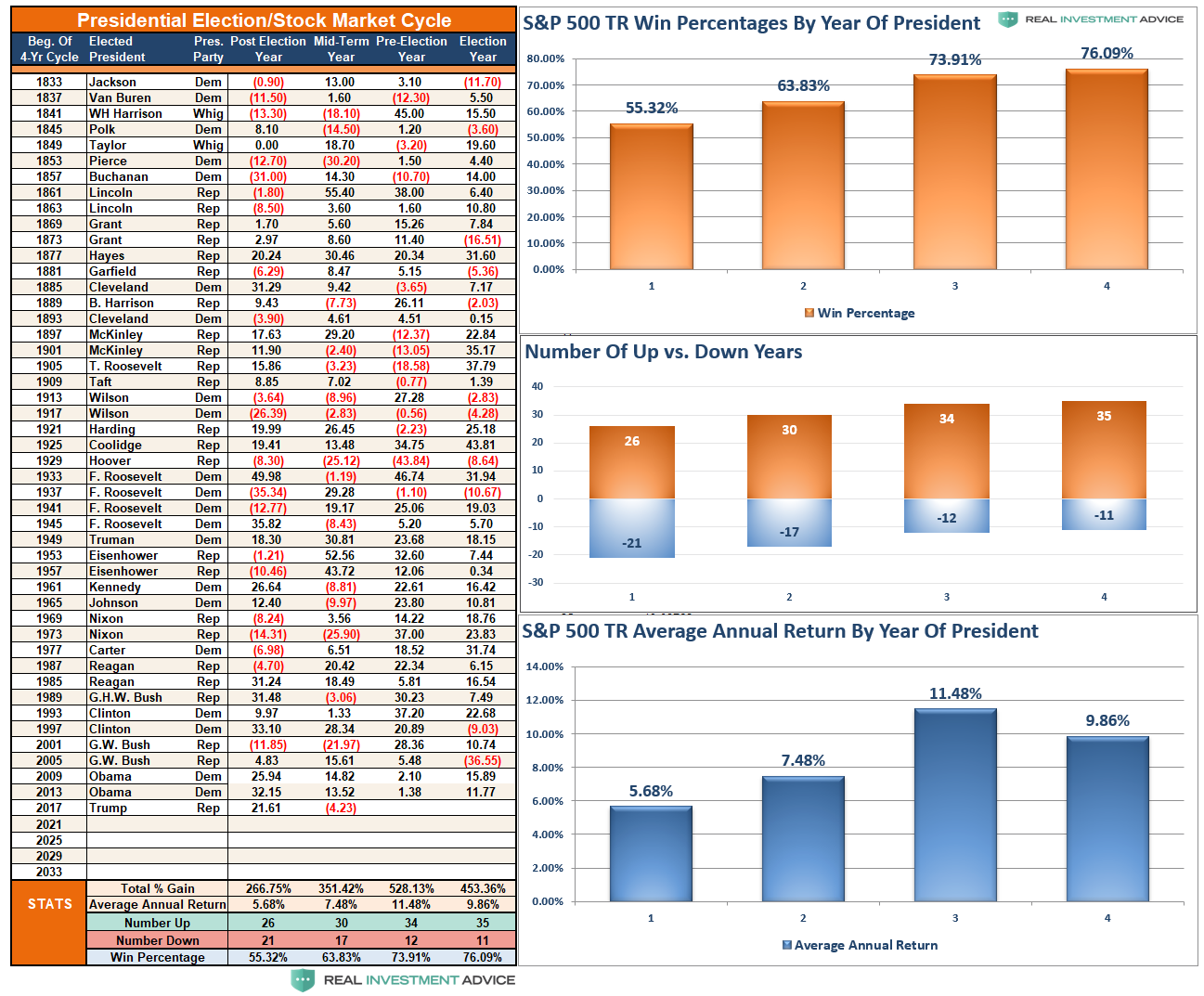

Presidential Cycle

With “hope” running high that things can continue going into 2020, the question becomes whether or not the Presidential election cycle can hold its performance precedent. Since 1871, markets have gained in 35 of those years, with losses in only 11.

Since 1948, there have only been two losses during presidential election years which were 2000 and 2008. In fact, stocks have, on average, put in their second-best performance in the fourth year of a president’s term. (The third year has been best as we are seeing currently.)

With a “win ratio” of 76%, the media has been quick to assume the bull market will continue unabated. However, there is a 24% chance a bear market will occur which is not entirely insignificant. Furthermore, given the duration, magnitude, and valuation issues associated with the market currently, a “Vegas handicapper” might increase those odds just a bit.

One thing to remember about all of this is that while the odds are weighted in favor of a positive 2020 from an election cycle standpoint – there have been NO cycles in history when the majority of the industrialized world was on the brink of a debt crisis all at the same time.

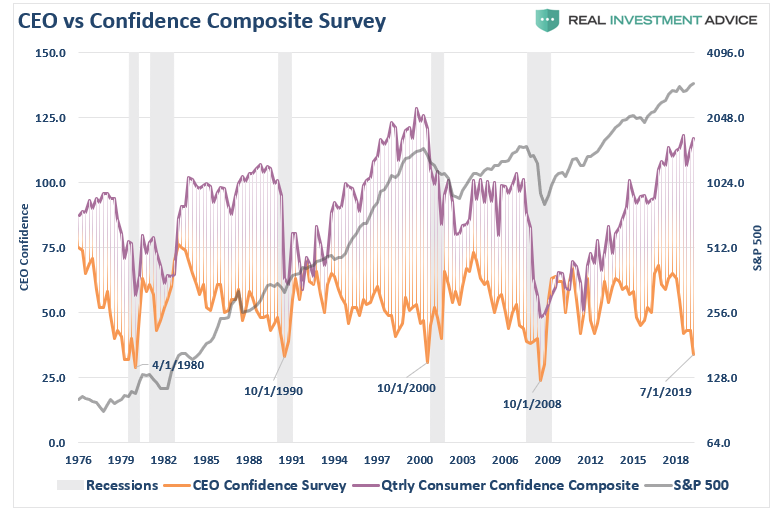

While the election of the next President will impact the market’s view towards policy stability; it is the world stage that will drive investor sentiment over the coming months and years. The biggest of those drivers is employment which has been weakening as of late. Importantly, there is an important correlation between consumer/investor sentiment, CEO confidence, and employment as noted above.

“Take a closer look at the chart above.

Notice that CEO confidence leads consumer confidence by a wide margin. This lures bullish investors, and the media, into believing that CEO’s really don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

‘I’m sorry, we think you are really great, but I have to let you go.’”

“It is hard for consumers to remain ‘confident,’ and continue spending, when they have lost their source of income. This is why consumer confidence doesn’t ‘go gently into night,’ but rather ‘screaming into the abyss.’”

But there is another cycle that we need to consider which is colliding with the Presdential election cycle, and that is the 10-year or decennial cycle.

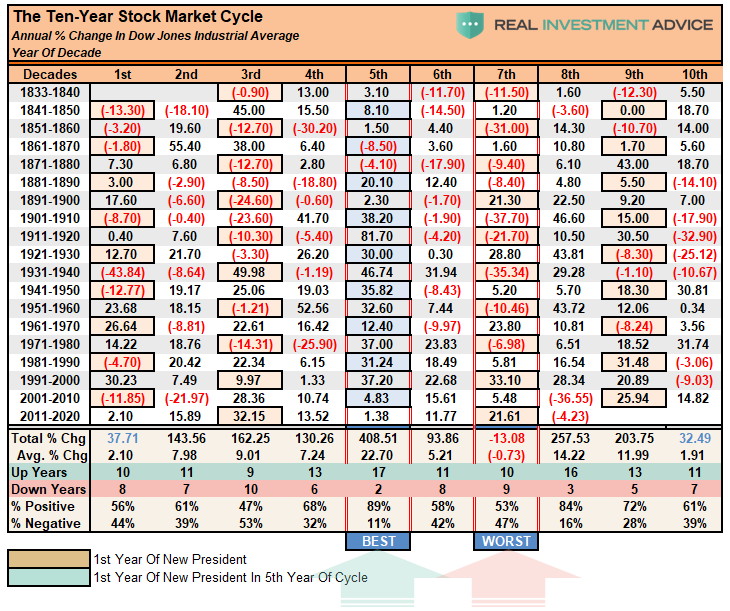

Decennial Cycle

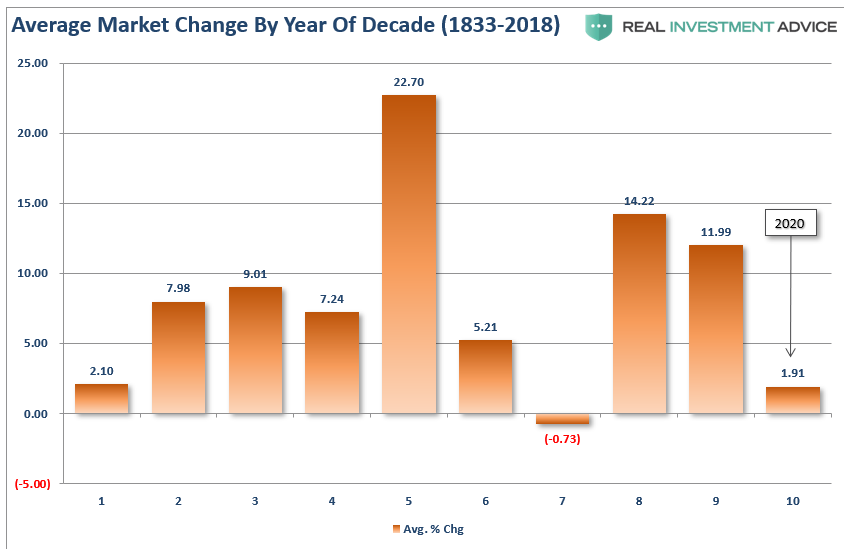

Using the same data set going back to 1833 we find a little different outlook. While the 10th year of the decade (2020) is on average slightly positive, it’s win/loss ratio is only 56%, or not much better than a coin toss.

Furthermore, while presidential election years have a near 10% average annual return profile, the 10th-year of the decennial cycle is markedly weaker at just 1.91% on average.

The best year of the decade is the 5th which has been positive 79% of the time with an average return of 22%. The worst year is the 7th with only a 53% win rate but a negative average annual return. As noted, 2020 comes in as the second place for the worst of the annual returns.

With a win/loss record of 11-7 an investor betting heavily on a positive outcome for 2020 may be left short changed given the current political, economic, fundamental, and financial environment.

I have also overlaid the 1st-year of the new presidential cycle with the “orange boxes” above. You will notice that again, return parameters and win/loss percentages are low. This should suggest some caution for investors over the next 24-months given the length of the current bull market advance.

A Lot Of If’s

All of this analysis is fine but whether the market is positive or negative in 2020 comes down to a laundry list of assumptions:

- If we can avoid a recession in the U.S.

- If we can avoid a recession in Europe.

- If corporate earnings can strengthen.

- If the consumer can remain strong.

- Etc.

Those are some pretty broad “if’s” and given the weakness is imports, which suggests a weakening domestic consumer, and struggling manufacturing, the risk of something going wrong is elevated.

As far as corporate earnings go – they peaked this year as the tax cut stimulus ran its course, and forward expectations are being sharply ratcheted lower. As we discussed on Tuesday:

“Since April, forward expectations have fallen by more than $11/share as economic realities continue to impale overly optimistic projections.”

This earnings boom cycle was skewed heavily by accounting rule changes, loan loss provisioning, tax breaks, massive layoffs, extreme cost cutting, suppression of wages and benefits, longer work hours, and massive share buybacks along with extraordinary government stimulus.

But when it comes to actual reported “profits,” which is what companies actually earned, reported, and paid taxes on, it is a vastly different story.

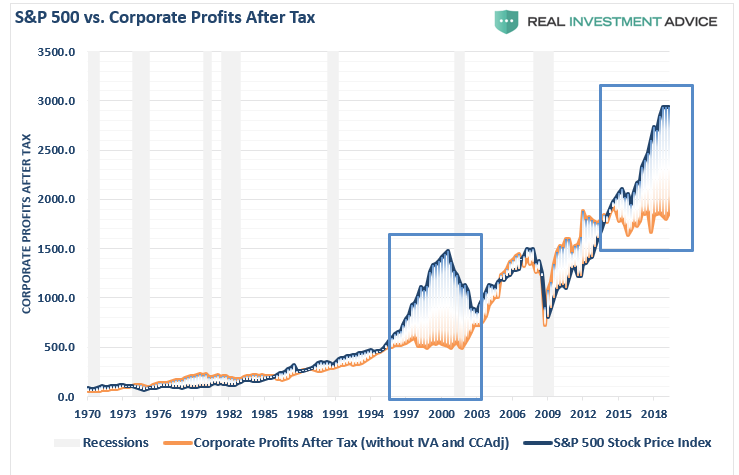

“Many are dismissing currently high valuations under the guise of ‘low interest rates,’ however, the one thing you should not dismiss, and cannot make an excuse for, is the massive deviation between the market and corporate profits after tax. The only other time in history the difference was this great was in 1999.”

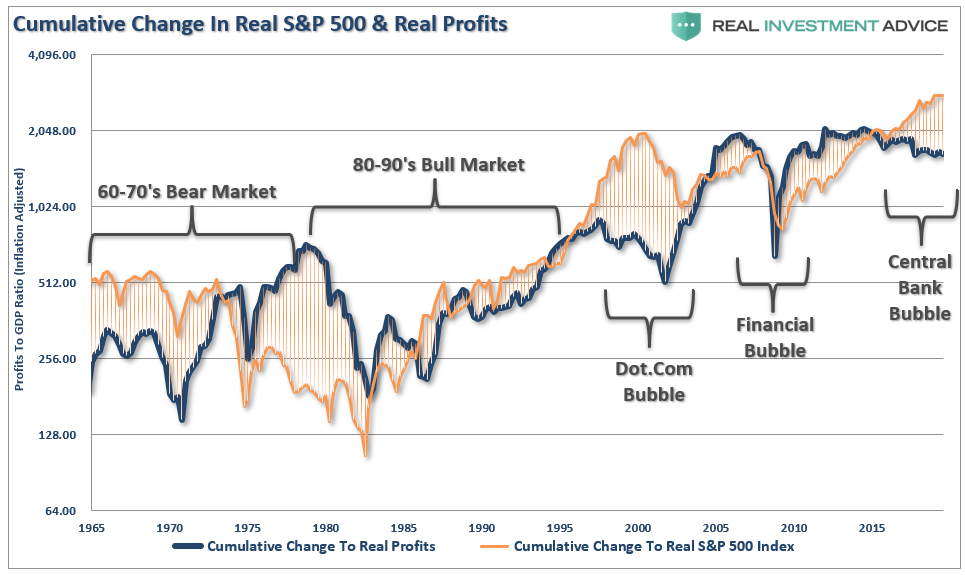

The chart below shows the real, inflation-adjusted, profits after-tax versus the cumulative change to the S&P 500. Here is the important point – when markets grow faster than profitability, which it can do for a while; eventually a reversion occurs. This is simply the case that all excesses must eventually be cleared before the next growth cycle can occur. Currently, we are once again trading a fairly substantial premium to corporate profit growth.

So, if, somehow, maybe, possibly, all these things can be sustained we should be just fine.

The problem is, however, all of the pillars that supported the earnings boom are now going away beginning next year, each of them to some degree, which throws into question the sustainability going into 2020-2021.

While doing statistical analysis on the Presidential and Decennial cycles certainly make for interesting articles, it is crucially important to remember what drives the financial markets the short-term which is psychology and sentiment.

In the next 12-18 months, there will be more than enough event risks to skew the potential outcomes of the markets. This doesn’t mean that you should go and hide all in cash or gold. It does suggest you need to actively pay attention to your money.

This idea plays into our allocation theme of higher quality income, hedged investments and precious metals as an alternative to direct market risk. With expectations of lower economic growth in the coming quarters, reduced earnings, and pressure on the consumer, the markets are likely to remain highly volatile with little overall progress.

While we are in the midst of prognostications, it has also been predicted the world will end in 2020, so anything other than that will be a “win.”

If you need help or have questions, we are always glad to help. Just email me.

See you next week.

“NEW” – Financial Planning Corner

by Danny Ratliff, CFP®, ChFC®

10-Don’t Miss Year-End Financial Planning Tips

Let’s give thanks that Thanksgiving week and the numerous “big” shopping days have officially come to a close. Christmas is fast approaching and now would be an easy time to push these year-end tips to 2020. Don’t. Spend 15 minutes and make sure you’re doing all you can to take advantage of 2019 and setting yourself up for a successful 2020.

- Evaluate this year’s financial plan progress: If you created a plan for 2019 how are you doing? What have you accomplished for the year and what do you still have time to complete? Many people just look at the investment returns and while that’s important don’t forget to look at your behaviors. How much have you spent and saved?

- Take another look at your 401(k): Does your employer match your 401(k) contributions? Now would be a good time to make sure you aren’t leaving any money on the table in the form of matching contributions. For 2019 you can contribute up to 19,000 to your 401(k) and an additional catch up of 6,000 if you turned 50 this year. Once the calendar turns to 2020 you won’t be able to go back and make up those missed contributions.

- Have access to a Health Savings Account (HSA,) max it out: HSA accounts are like the fountain of youth for the financial planning world. They’re almost too good to be true. This is the only account in the world that will give you a triple tax benefit. Money goes in tax free, grows tax free and if used for medical expenses comes out tax free. Think your medical expenses in retirement won’t be that bad? Thank again, Fidelity just did a study that shows the average 65-year-old couple will spend $280,000 in medical expenses. In 2019 individuals can contribute $3,500 and a family can contribute $7,000. Here’s the kicker, if you really want to maximize these plans you need to try to pay for current medical expenses out of pocket and let these funds grow.

- Use the balance of your Flexible Spending Account (FSA): If you have an FSA, now is the time to spend that unspent balance. Some plans will allow you to carry over a small amount of the funds to next year, but many won’t. So, use it or lose it.

- Review your Insurance Coverage: If you have life, health, disability, homeowners or long- term care insurance make some time to review your policies. Has anything changed with your policies, have premiums gone up? In regard to your life insurance have you had any life events that would warrant a change in your coverage?

- Review or Create Estate Planning Documents: If you and I have had a face to face meeting this is something I’ve probably asked you. This is so important, but often overlooked or pushed to the back burner. Stop denying the inevitable, you’re going to die, make sure your loved ones are taken care of the way you wish.

- Review Expenses: Many people have no idea how much they spend each month or where they are spending their money. This goes back to #1 evaluating your progress in your plan.

- Have a Conversation with your Tax Advisor: Between now and Christmas is a great time to have a chat with your tax advisor to ensure you aren’t leaving any deductions on the table before we get into 2020 and it’s to late. Everyone likes to reduce their tax bill.

- Roth Conversions: While you’re talking with your CPA and Advisor find out if you have any room for a Roth conversion. We talk about these often and run many analyses, they’re not for everyone, but these can be a great tool to give you more flexibility in retirement.

- Sell Losers to offset Gains: Tax loss harvesting is an easy way to lower your taxes on a year to year basis. Do you have any gains for the year and hold positions with losses? Realize your losses to offset those gains. The losses will offset your gains dollar for dollar. You can also use an additional $3,000 to offset other income and if you have more than $3,000 in excess losses you can carry that over indefinitely until those losses are exhausted.

Achieving your financial goals is a never-ending process and staying on top of financial planning is imperative to your success. December is an ideal time to assess your current situation and ensure you’re taking advantage of all you can for 2019.

Need a financial partner to help keep you on track or looking for ways to fine tune your financial plan? Contact us to see how we can help create a financial plan that uses realistic data that will provide your family peace of mind and security.

Don’t hesitate to send me an email if you have any questions or if you, or someone you know, needs help. We encourage your feedback and look forward to hearing from you.

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now!

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

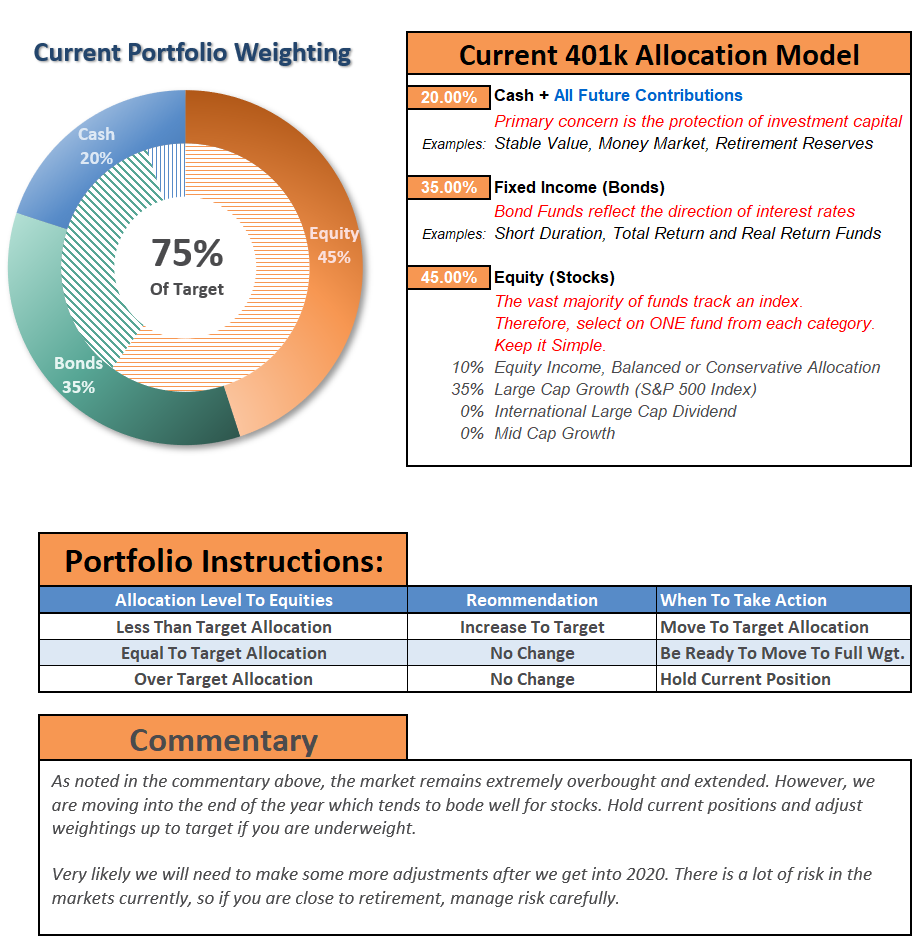

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

If you need help after reading the alert; do not hesitate to contact me.

Click Here For The “LIVE” Version Of The 401k Plan Manager

See below for an example of a comparative model.

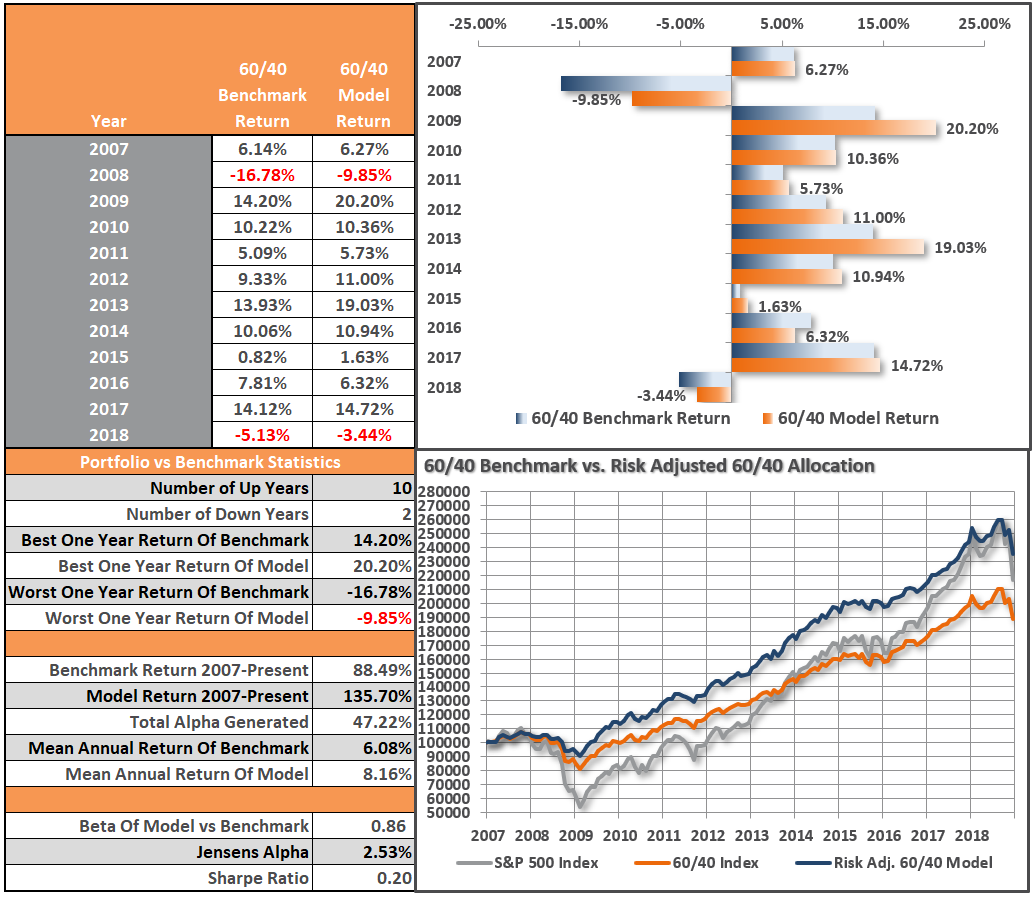

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.