However, it wasn’t too long before the 2008 “Financial Crisis” brought the “Minsky Moment” thesis to the forefront. What was revealed, of course, was the dangers of profligacy which resulted in the triggering of a wave of margin calls, a massive selloff in assets to cover debts, and higher default rates.

So, what exactly is a “Minskey Moment?”

Economist Hyman Minsky argued that the economic cycle is driven more by surges in the banking system, and in the supply of credit than by the relationship which is traditionally thought more important, between companies and workers in the labor market.

In other words, during periods of bullish speculation, if they last long enough, the excesses generated by reckless, speculative, activity will eventually lead to a crisis. Of course, the longer the speculation occurs, the more severe the crisis will be.

Hyman Minsky argued there is an inherent instability in financial markets. He postulated that an abnormally long bullish economic growth cycle would spur an asymmetric rise in market speculation which would eventually result in market instability and collapse. A “Minsky Moment” crisis follows a prolonged period of bullish speculation which is also associated with high amounts of debt taken on by both retail and institutional investors.

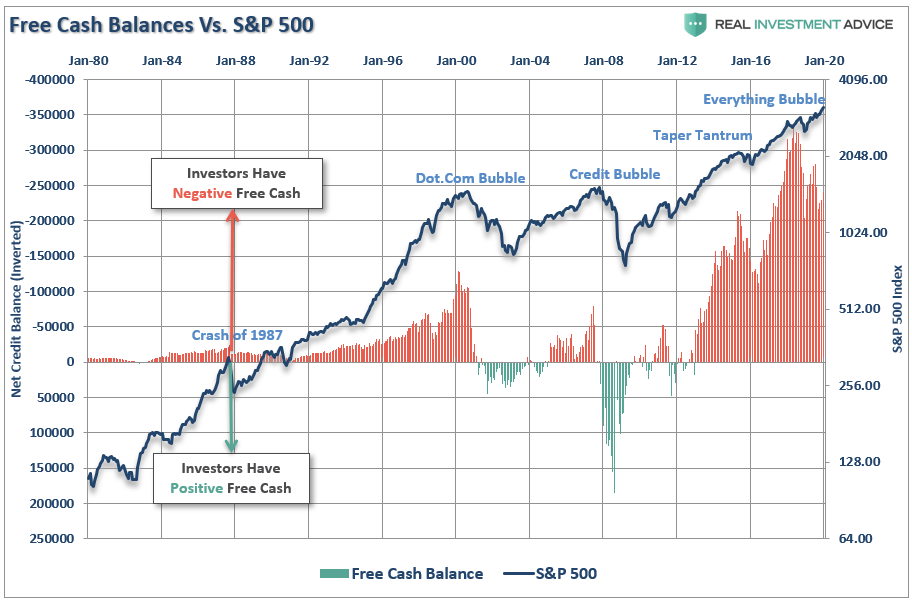

One way to look at “leverage,” as it relates to the financial markets, is through “margin debt,” and in particular, the level of “free cash” investors have to deploy. In periods of “high speculation,” investors are likely to be levered (borrow money) to invest, which leaves them with “negative” cash balances.

While margin balances did decline in 2018, as the markets fell due to the Federal Reserve hiking rates and reducing their balance sheet, it is notable that current levels of “leverage” are still excessively higher than they were either in 1999, or 2007.

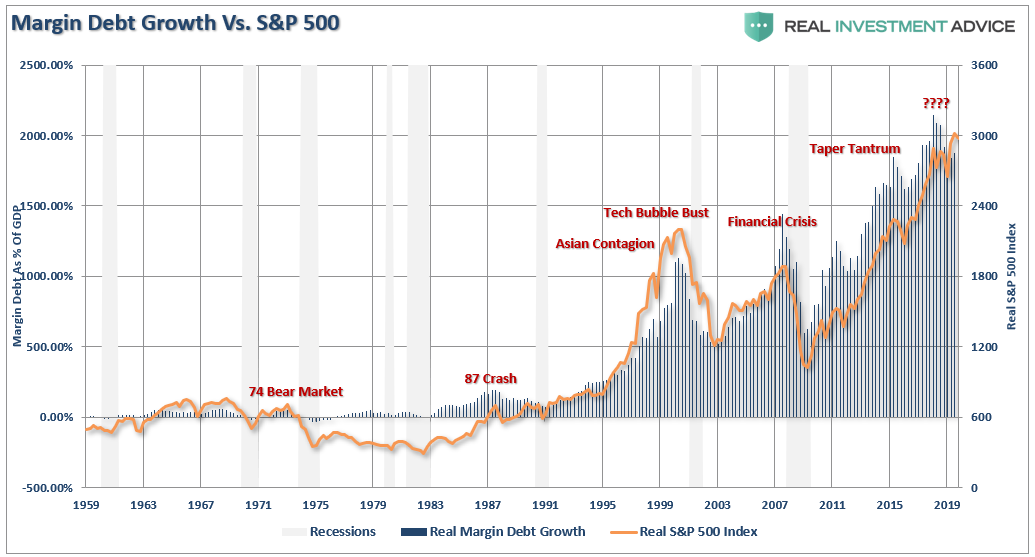

This is also seen by looking at the S&P 500 versus the growth rate of margin debt.

The mainstream analysis dismisses margin debt under the assumption that it is the reflection of “bullish attitudes” in the market. Leverage fuels the market rise. In the early stages of an advance, this is correct. However, in the later stages of an advance, when bullish optimism and speculative behaviors are at the peaks, leverage has a “dark side” to it. As I discussed previously:

“At some point, a reversion process will take hold. It is when investor ‘psychology‘ collides with ‘leverage and the problems associated with market liquidity. It will be the equivalent of striking a match, lighting a stick of dynamite, and throwing it into a tanker full of gasoline.”

That moment is the “Minsky Moment.”

As noted, these reversion of “bullish excess” are not a new thing. In the book, “The Cost of Capitalism,” Robert Barbera’s discussed previous periods in history:

The last five major global cyclical events were the early 1990s recession — largely occasioned by the U.S. Savings & Loan crisis, the collapse of Japan Inc. after the stock market crash of 1990, the Asian crisis of the mid-1990s, the fabulous technology boom/bust cycle at the turn of the millennium and the unprecedented rise and then collapse for U.S. residential real estate in 2007-2008.

All five episodes delivered recessions, either global or regional. In no case was there as significant prior acceleration of wages and general prices. In each case, an investment boom and an associated asset market ran to improbably heights and then collapsed. From 1945 to 1985 there was no recession caused by the instability of investment prompted by financial speculation — and since 1985 there has been no recession that has not been caused by these factors.

Read that last sentence again.

Interestingly, it was post-1970 the Federal Reserve became active in trying to control interest rates and inflation through monetary policy.

As noted in “The Fed & The Stability Instability Paradox:”

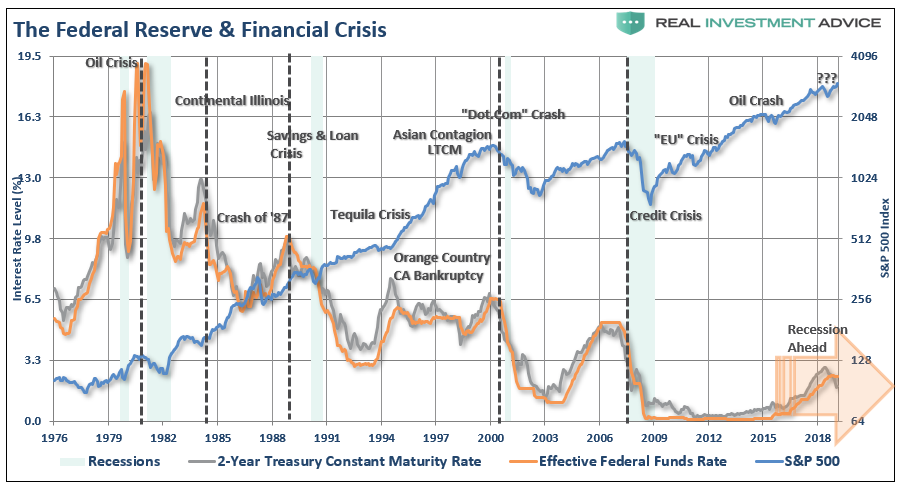

“In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became ‘active,’ monetarily policy-wise, in the late 70’s. As shown in the chart below, when the Fed has lifted the short-term lending rates to a level higher than the 2-year rate, bad ‘stuff’ has historically followed.”

The Fed Is Doing It Again

As noted above, “Minsky Moment” crises occur because investors, engaging in excessively aggressive speculation, take on additional credit risk during prosperous times, or bull markets. The longer a bull market lasts, the more investors borrow to try and capitalize on market moves.

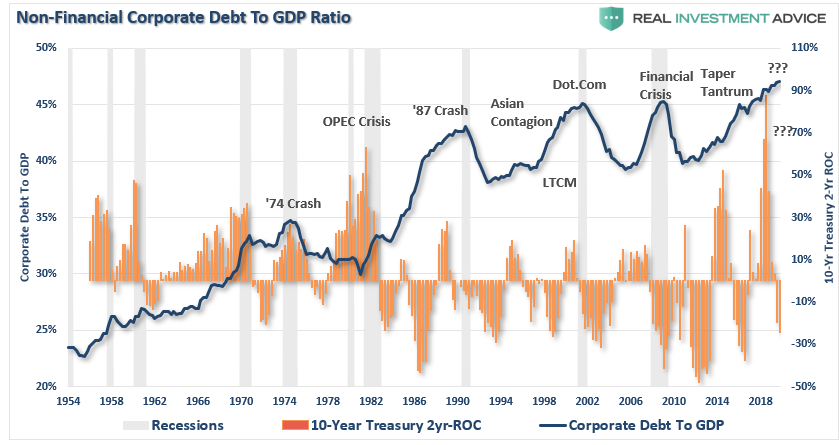

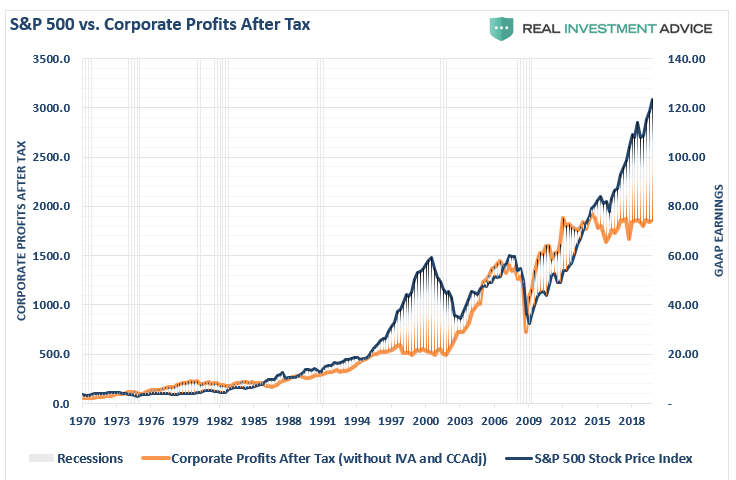

However, it hasn’t just been investors tapping into debt to capitalize on the bull market advance, but corporations have gorged on debt for unproductive spending, dividend issuance, and share buybacks. As I noted in last week’s MacroView:

“Since the economy is driven by consumption, and theoretically, companies should be taking on debt for productive purposes to meet rising demand, analyzing corporate debt relative to underlying economic growth gives us a view on leverage levels.”

“The problem with debt, of course, is it is leverage that has to be serviced by underlying cash flows of the business. While asset prices have surged to historic highs, corporate profits for the entirety of U.S. business have remained flat since 2014. Such doesn’t suggest the addition of leverage is being done to ‘grow’ profits, but rather to ‘sustain’ them.”

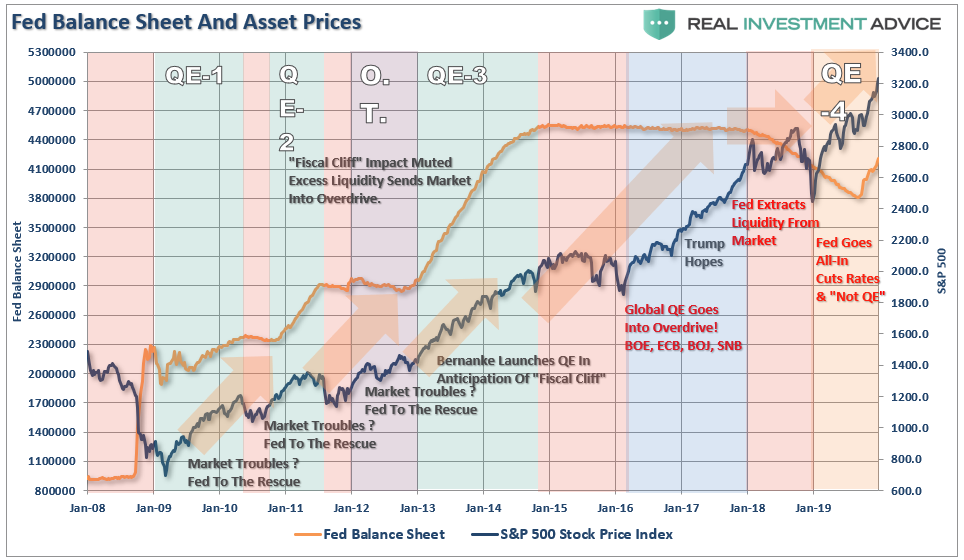

Over the last decade, the Federal Reserve’s ongoing liquidity interventions, zero interest-rates, and maintaining extremely “accommodative” policies, has led to substantial increases in speculative investment. Such was driven by the belief that if “something breaks,” the Fed will be there to fix to it.

Currently, despite a decade long economic expansion, record stock market prices, and record low unemployment, the Fed continues to support financial speculation through ongoing interventions.

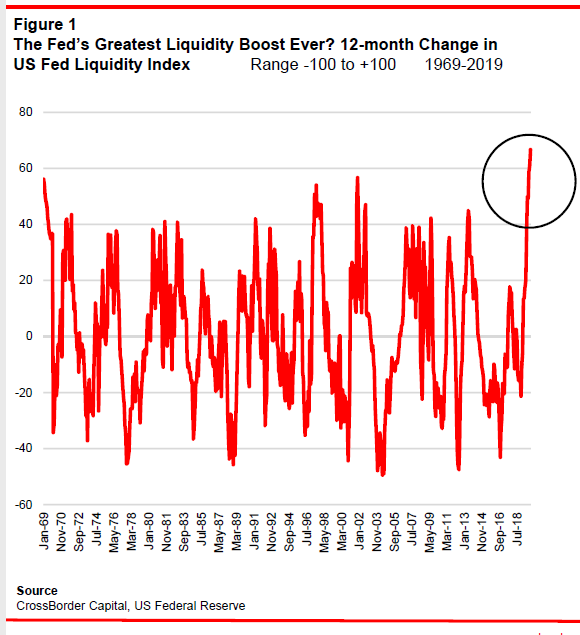

John Authers recently penned an excellent piece on this issue for Bloomberg:

“Why does liquidity look quite so bullish? As ever, we can thank central banks and particularly the Federal Reserve. Twelve months ago, the U.S. central bank intended to restrict liquidity steadily by shrinking the assets on its balance sheet on “auto-pilot.” That changed, though. It reversed course and then cut rates three times. And most importantly, it started to build its balance sheet again in an attempt to shore up the repo market — which banks use to access short-term finance — when it suddenly froze up in September. In terms of the increase in U.S. liquidity over 12 months, by CrossBorder’s measures, this was the biggest liquidity boost ever:”

While John believes we are early in the global liquidity cycle, I personally am not so sure given the magnitude of the increase Central Bank balance sheets over the last decade.

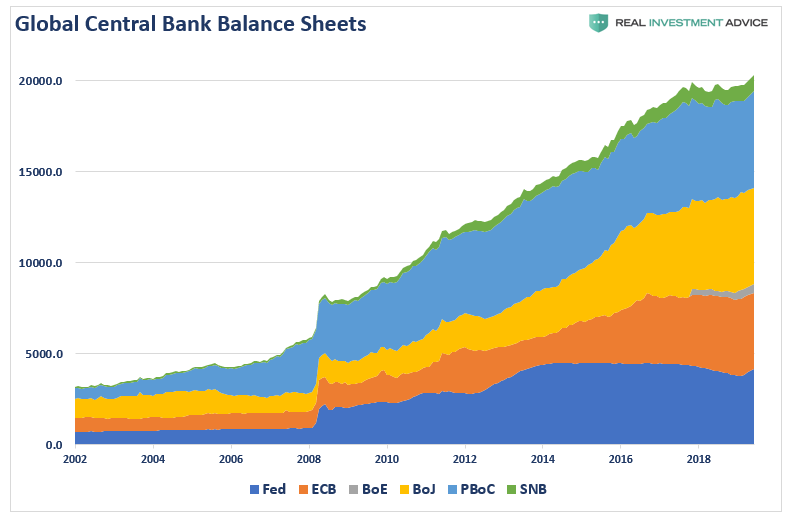

Currently, global Central Bank balance sheets have grown from roughly $5 Trillion in 2007, to $21 Trillion currently. In other words, Central Bank balance sheets are equivalent to the size of the entire U.S. economy.

In 2007, the global stock market capitalization was $65 Trillion. In 2019, the global stock market capitalization hit $85 Trillion, which was an increase of $20 Trillion, or roughly equivalent to the expansion of the Central Bank balance sheets.

In the U.S., there has been a clear correlation between the Fed’s balance sheet expansions, and speculative risk-taking in the financial markets.

Is Another Minsky Moment Looming?

The International Monetary Fund (IMF) has been issuing global warnings of high debt levels and slowing global economic growth, which has the potential to result in Minsky Moment crises around the globe.

While this has not come to fruition yet, the warning signs are there. Globally, there is roughly $15 Trillion in negative-yielding debt with asset prices fundamentally detached for corporate profitability, and excessive valuations on multiple levels.

As Desmond Lachman wrote:

“How else can one explain that the risky U.S. leveraged loan market has increased to more than $1.3 trillion and that the size of today’s global leveraged loan market is some two and a half times the size of the U.S. subprime market in 2008? Or how else can one explain that in 2017 Argentina was able to place a 100-year bond? Or that European high yield borrowers can place their debt at negative interest rates? Or that as dysfunctional and heavily indebted government as that of Italy can borrow at a lower interest rate than that of the United States? Or that the government of Greece can borrow at negative interest rates?

These are all clear indications that speculative excess is present in the markets currently.

However, there is one other prime ingredient needed to complete the environment for a “Minsky Moment” to occur. That ingredient is complacency.

Yet despite the clearest signs that global credit has been grossly misallocated and that global credit risk has been seriously mispriced, both markets and policymakers seem to be remarkably sanguine. It would seem that the furthest thing from their minds is that once again we could experience a Minsky moment involving a violent repricing of risky assets that could cause real strains in the financial markets.”

Desmond is correct. Currently, despite record asset prices, leverage, debt, combined with slowing economic growth, the level of complacency is extraordinarily high. Given that no one currently believes another “credit-related crisis” can occur is what is needed to allow one to happen.

Professor Minsky taught that markets have short memories, and that they repeatedly delude themselves into believing that this time will be different. Sadly, judging by today’s market exuberance in the face of mounting economic and political risks, once again, Minsky is likely to be proved correct.

At this point in the cycle, the next “Minsky Moment” is inevitable.

All that is missing is the catalyst to start the ball rolling.

An unexpected recession would more than likely due to trick.

The BullsNBears.com website was founded by market crash expert Michael Markowski to specialize at publishing articles by him and by other authors who have been screened. The articles pertain to market crashes, market bottoms and recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.