Last week, we asked the question: “Is everything ‘priced in?’” On Monday, the market realized no help is coming as the political backdrop worsened markedly.

However, we need to back up a little bit to discuss how we got here. In the middle of August, we wrote “Close But No Cigar,” which addressed the potential of a market correction due to the extreme positioning in markets. To wit:

“With the markets overbought on several measures, there is a downside risk heading into the end of the month. These risks come from several fronts we will discuss momentarily. However, from a technical perspective, the downside risk is about 5.6% to the 50-dma and 9.4% to the 200-dma. (Shown above)

A 5-10% decline in any given year is not outside of the norm. However, since investors have entirely forgotten what a drop feels like, a 5-10% slide will ‘feel’ worse than it is.”

At that time, there seemed to be little to worry about. The Federal Reserve was remaining accommodative to the markets, and expectations of additional monetary support were high. Expectations were high that Congress would pass other fiscal measures to support the recessionary economy soon.

More money meant higher markets, hence the speculative bias.

As I stated then, the market was overbought on multiple measures, which typically coincides with short-term market peaks and corrections. That overbought condition, combined with more extreme speculative positioning by investors, provided the fuel for a correction when it came.

All that was needed as a “catalyst” to trigger the selling.

Remembering 2016

I liked David Rosenberg’s note yesterday on the current correction:

“The stock market has really gone through a change of complexion — to a far greater degree than the last corrective phase in June when valuations, momentum, leverage, and sentiment were less extreme than was the case heading into this current period.”

Last week, we noted a list of concerns relating to the market, which could undoubtedly pressure markets lower. One of those, in particular, was the lack of additional “fiscal stimulus” coming from Congress.

Over the weekend, and summed up in the video below, a collision of events brought concerns to the forefront.

The death of Supreme Court Justice Ruth Ginsberg has sparked a replay of the 2016 passing of Justice Scalia. At that time, President Obama wanted to appoint a replacement for Scalia even as the Presidential election was just a few months away. Congress got into a contested debate over whether a justice should be selected so close to an election. That debate is again on display as President Trump wants to appoint a replacement for Ginsberg as soon as possible. Still, the Democratically controlled Congress is fighting to delay it until after the election.

Politically, this is an incredibly important appointment. Since justices get appointed for life, if President Trump adds another “conservative” justice to the Supreme Court, rulings on more liberal causes could be stymied for a decade or more.

A Collision Of Events

Why is this important to the market? Because Congress is facing three different events that have removed the focus from additional financial support for the economy.

- With the election fast approaching, Congress does not want to pass a fiscal support bill to help the other Presidential candidate. Such is why there are dueling bills between the House and Senate currently.

- September ends the 2020 fiscal year of Congress. Such requires either a “budget,” or another C.R. (Continuing Resolution) to fund the government and avoid another shut-down.

- Lastly, the death of RBG will have the entire Democratic Party, which controls the House, focused on how to stop President Trump from nominating a replacement before the election. All Trump needs is a simple majority in the Senate to confirm a justice that he can likely get.

As I discussed with our RIAPro Subscribers in this morning’s “Sector Trading Review,” the realization of “no more fiscal support” killed the “economic reflation” trade yesterday.

“A common theme through today’s update is the exit of the ‘reflation’ trade. Markets had been hoping for additional ‘fiscal support’ from Congress. However, with the election looming, a need for a budget negotiation to avoid a ‘shutdown,’ and now a battle over replacing a Supreme Court Justice, the odds of a fiscal deal getting done is minuscule.

Looking at XLB, the sell-off yesterday reflected the exit of the reflation trade. You will see the same in Industrials, and Transportation as well which were all down in excess of 3%.”

In short, this all presents a problem which markets discovered Monday morning – “no more monetary support.”

(Click the banner below to get notified of our daily “3-minutes” videos.”

The Fed Is Limited

At the September FOMC meeting, Jerome Powell made a critical statement overlooked by the majority of the mainstream media.

“Federal Reserve Board Chairman Jerome Powell warned Wednesday that a lack of further fiscal support from Congress and President Trump could “scar and damage” a U.S. economy restrained by the coronavirus pandemic.

‘If there’s no follow-up on that, if there isn’t additional support and there isn’t a job for some of those people who are from industries where it’s going to be very hard to find new work. That will start to show up in economic activity. It’ll also show up in things like evictions and foreclosures and things that will scar and damage the economy.’” – The Hill

The Federal Reserve is trying to plug a hole that fiscal policy was widely expected to fill by now. However, the Fed’s ability to expand on current programs is limited to the Treasury Department’s issuance of additional debt. Without another “fiscal relief” bill, there isn’t enough debt issuance to support another round of interventions by the Fed.

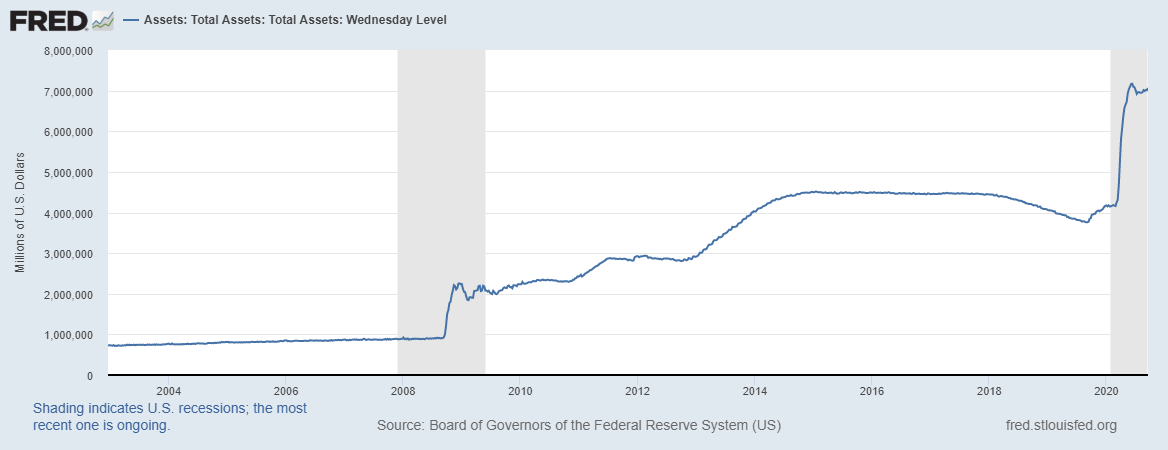

Currently, the Federal Reserve is continuing to run “Quantitative Easing” at $120 billion per month, but much of that is just replacing bills that are maturing. As shown below, the Fed’s balance sheet has been stagnating since June as the uptake from its various programs has waned.

Short-Term Bearishness

The realization the Federal Reserve will likely not get any “fiscal support” from Washington in the short-term is problematic for the markets. Without fiscal support, the Fed is limited in its monetary response. Rates are already at zero, and economic data is beginning to show signs of weakening as the “direct checks” and “expanded U.I. benefits” to households has run out.

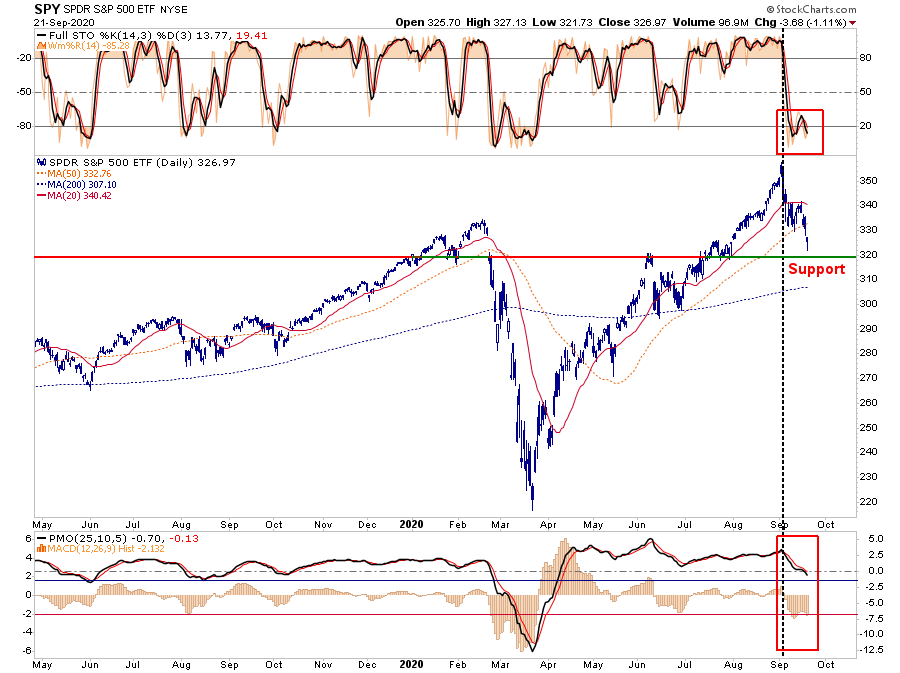

The subsequent selling in the market has led to increased short-term bearishness in the markets. As shown below, markets are very oversold short-term on several measures. Furthermore, the bounce of support yesterday suggests we could see a follow-through rally back to the 50-dma, which will act as crucial overhead resistance short-term.

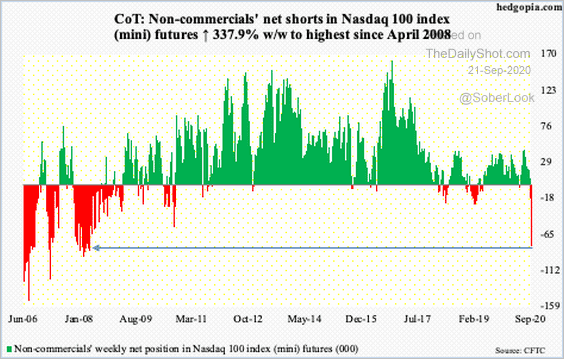

Furthermore, besides being oversold, there is the largest net-short position on the Nasdaq we have seen since 2008.

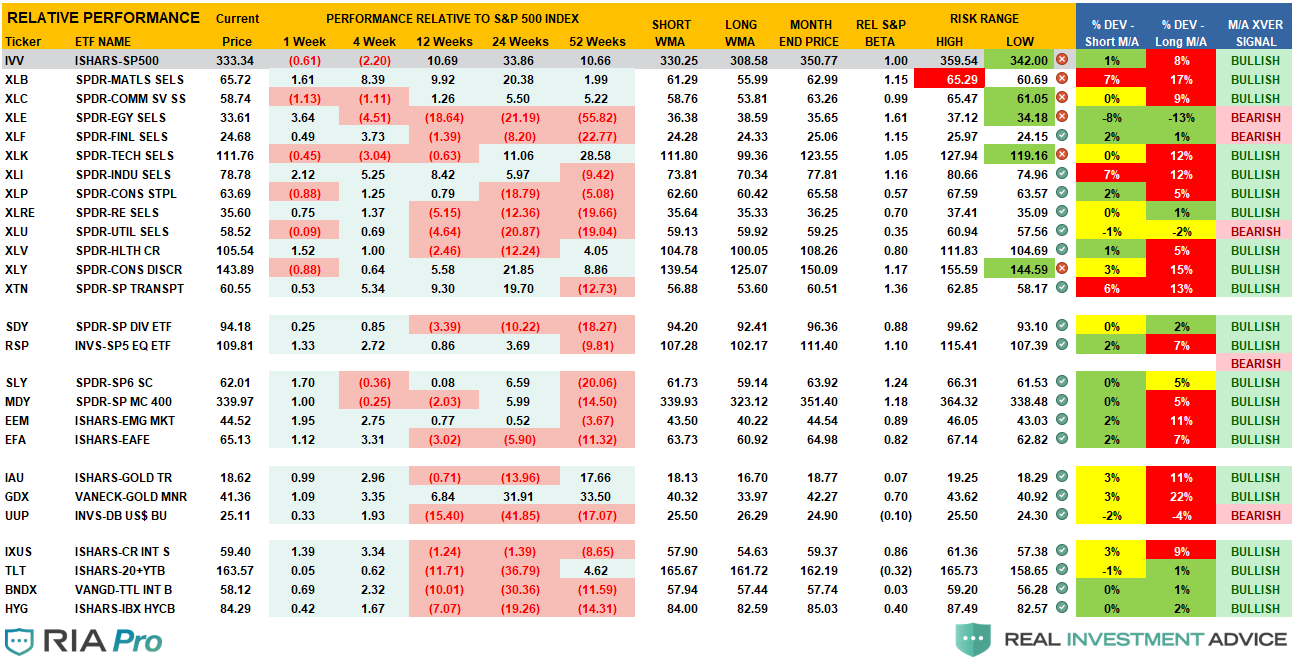

As we showed our RIAPro Subscribers (30-Day Risk-Free Trial), the sharp sell-off in Technology specifically pulled the sector out of its Risk/Reward range.

Such short-term bearishness provides a good backdrop for a short-term rally over the next few days. Be careful you don’t “panic sell” the market; use counter-trend bounces to reduce risk logically.

There Is Downside Risk

As noted previously:

“The reason we suggest selling any rally is because, until the pattern changes, the market exhibiting all traits of a “topping process.”

- Weak participation

- Failure at long-term resistance

- Extreme bullish speculation

- Negative divergences in relative strength

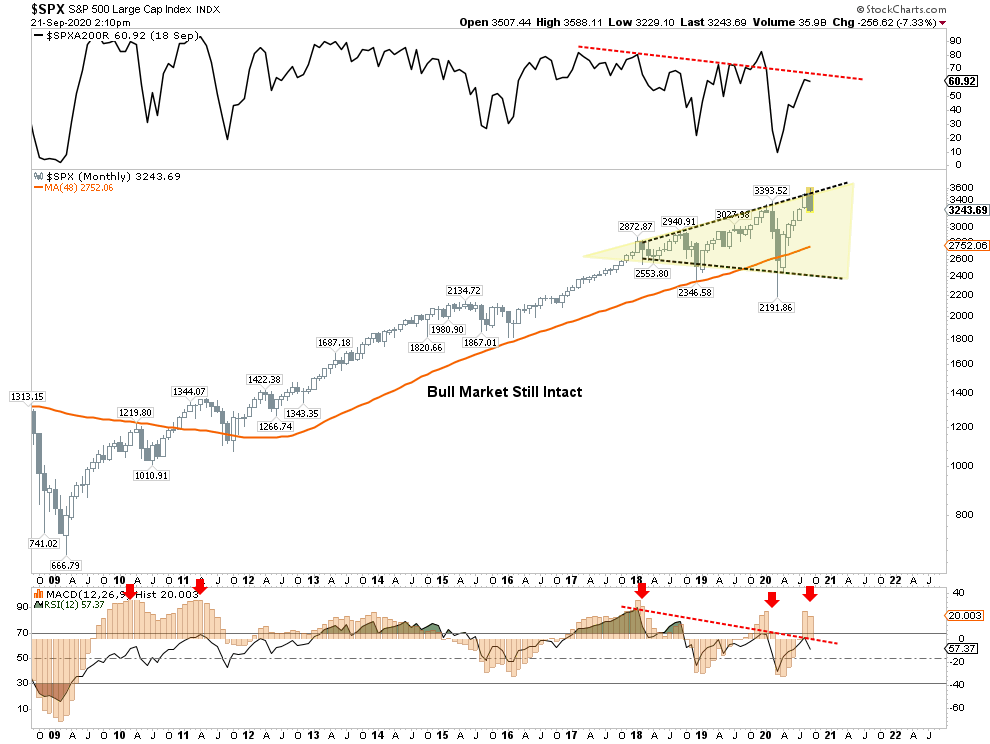

We can show this in a long-term monthly chart.”

Since 2009, whenever the monthly MACD “buy signal” was this elevated, it typically correlated to a short- to intermediate-term market peak.

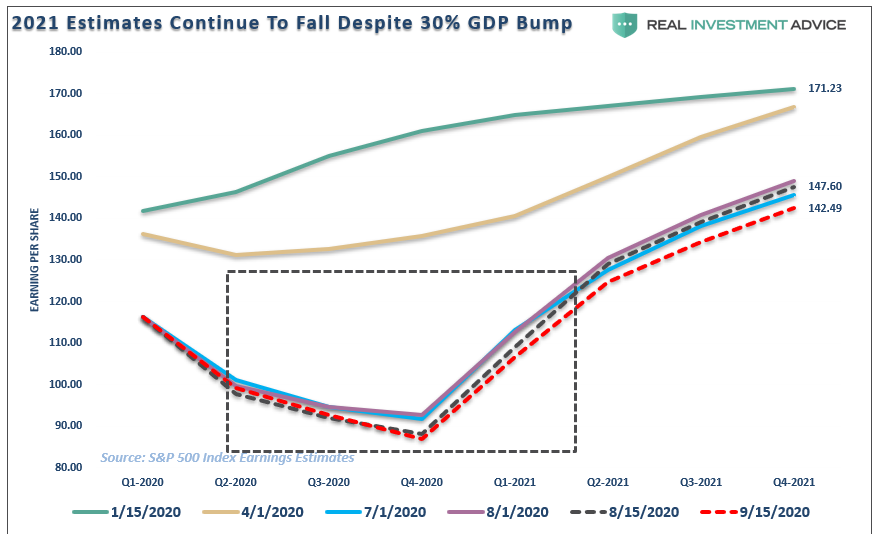

Such also correlates with weaker economic data showing up. Weaker economic data translates into reduced earnings outlooks for companies. During the last 30-days, 2021 estimates for the S&P 500 have declined by an additional $5/share. Furthermore, those estimates are down nearly $30 from the original forecast in January 2020. Yet, markets remain only slightly off all-time highs.

Still A Sellable Rally

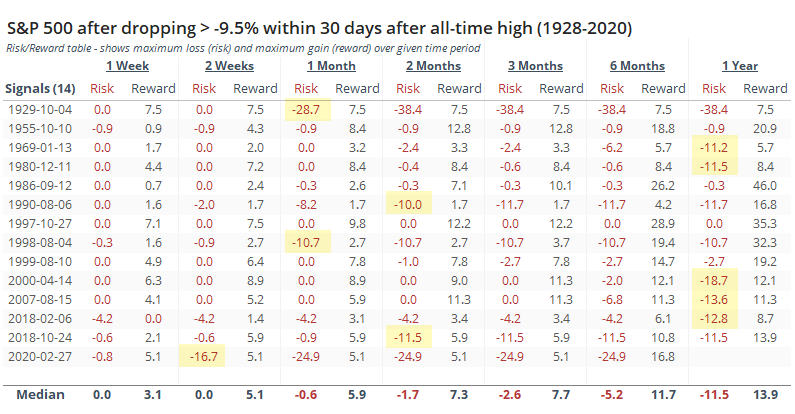

As noted in this past weekend’s missive, we still expect a “reflexive rally” given the short-term oversold condition of the market. However, we still expect there could be further downside risk over the intermediate-term.

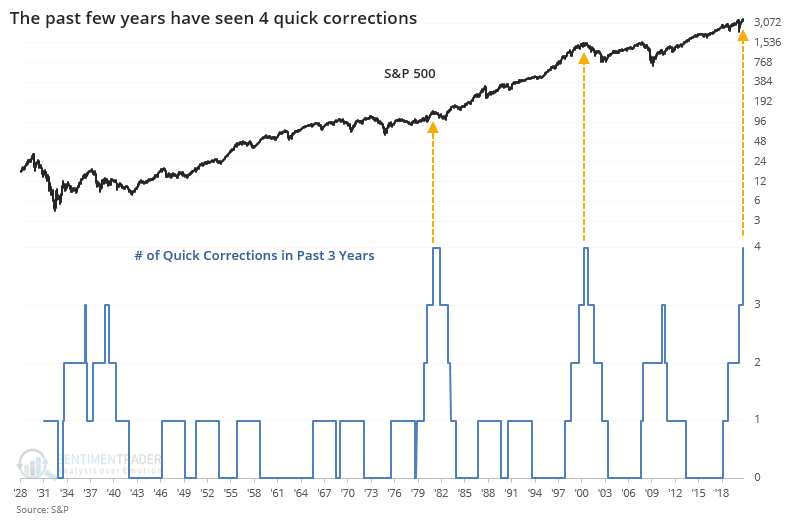

The current correction is the 4th of 10% or more over the last 3-years. Do not dismiss this lightly as Sentiment Trader noted on Monday:

We have discussed previously, the pickup in volatility over the last couple of years is more akin to a broader “topping” process for the markets. Outcomes from such have not been outstanding.

However, given the more bearish tone to the market, and the extreme net short position on the Nasdaq, it won’t take much to elicit a “short-covering” rally. Some “encouraging” words from the White House promising fiscal support, or a Fed speaker suggesting monetary action, would do the trick.

While either would give the markets a short-term lift, we suggest using rallies to reduce risk, for now.

We suspect that given the rather numerous headwinds currently facing the markets, from the Fed to the election, a failure at lower highs would not be surprising.

The post Technically Speaking: Market Realized No Help Is Coming appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.