In this 05-08-21 issue of “Poor Jobs Report Gives Bulls A Reason To Charge.“

- Market Review And Update

- Peak Earnings

- Bonds Aren’t Buying It

- Portfolio Positioning

- #MacroView: No. Bonds Aren’t Overvalued.

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Market Review & Update

Last week, we said:

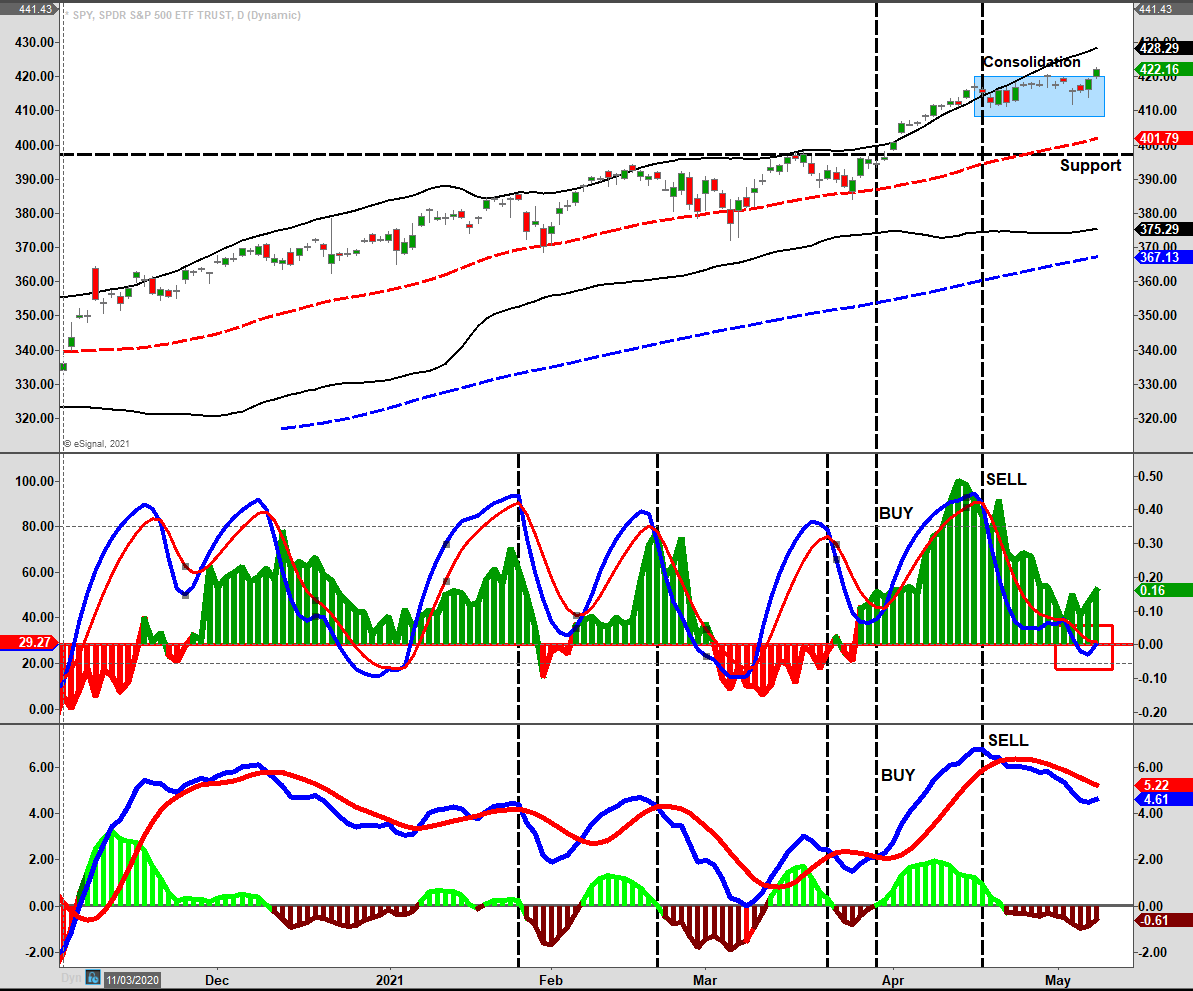

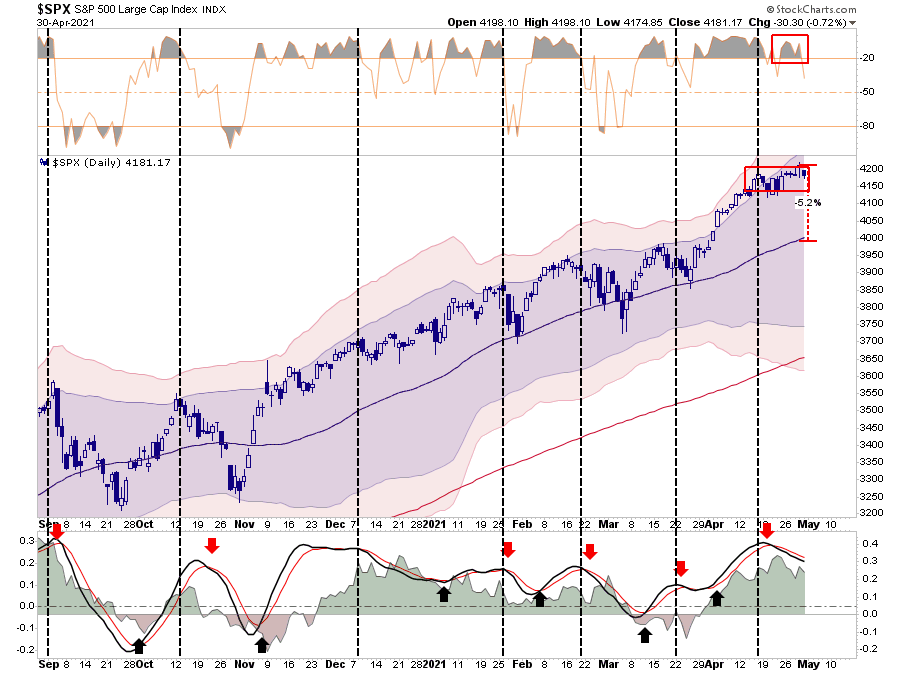

“While the market remains in a very tight range, the ‘money flow’ sell signal (middle panel) is reversing quickly. Importantly, note that the money flows (histogram) are rapidly declining on rallies which is a concern.”

This past week, market action was sloppy as investors are finding fewer reasons to push stocks higher. Friday’s very disappointing jobs report provided some catalyst as the Fed is assured not to reduce monetary support anytime soon. However, despite the push, the overall conviction was lacking.

Notably, the “money flow buy signal” seemed to cross; however, we need some follow-through action on Monday to confirm. As shown, the uptick in money flows did allow us to add some exposure to portfolios in holdings we had taken profits in with the previous “sell” signal.

Again, we do want to see confirmation that the breakout above the consolidation range can hold. The last breakout failed, so, again, we do need “follow-through” to confirm buyers are indeed back. Notably, the MACD “sell signal” in the lower panel remains, which suggests upside likely remains limited at this juncture. If the “buy signals” align, we will have a much higher level of conviction about higher prices.

Overall, the market trend remains bullish, so there is no need to be overly defensive. Just a regular process of tweaking risk and managing exposures is all that portfolios require for now. Such is what we have recommended over the last several weeks, so we are now in a position to take advantage of a short-term bullish move.

For the rest of this week’s message, we will go into deeper detail on the issues I discussed in the latest “3-Minutes” video:

- Peak Earnings,

- Inflation, and Margins, and

- Hedgefund selling.

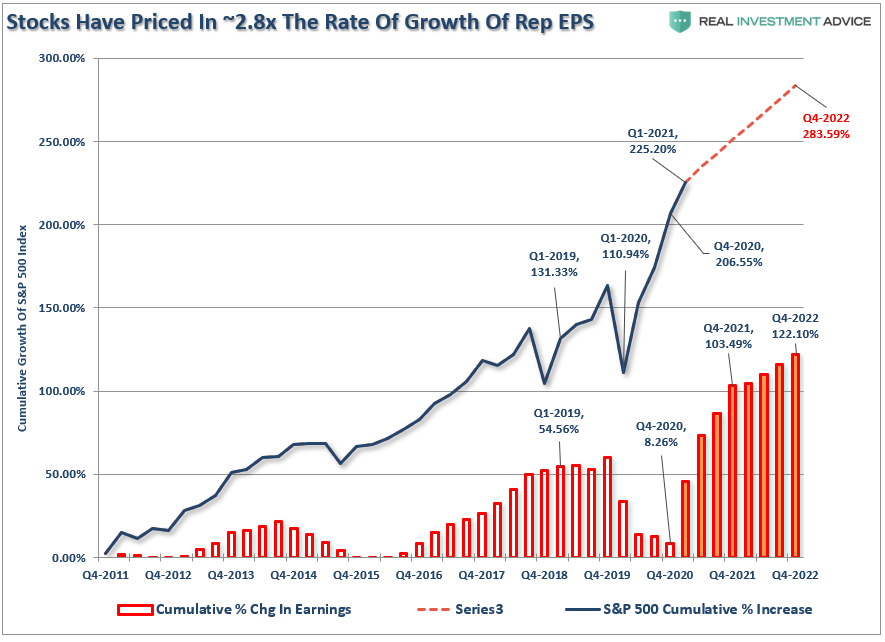

Peak Earnings?

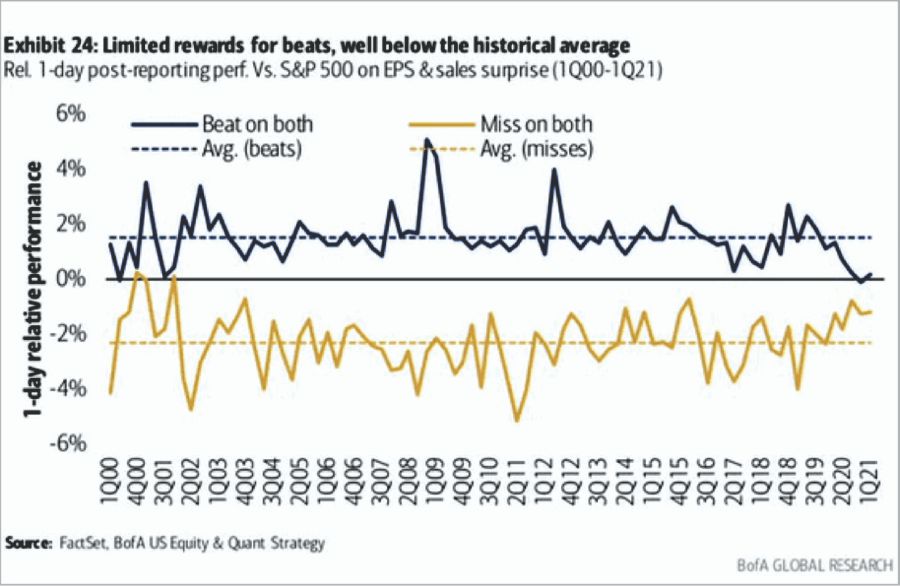

Over the last few weeks, we have seen numerous companies report stellar earnings growth. Yet, the market has failed to reward the good news as stocks get sold off. As the chart below shows, it has not been just a few select isolated cases.

There are a couple of reasons for this.

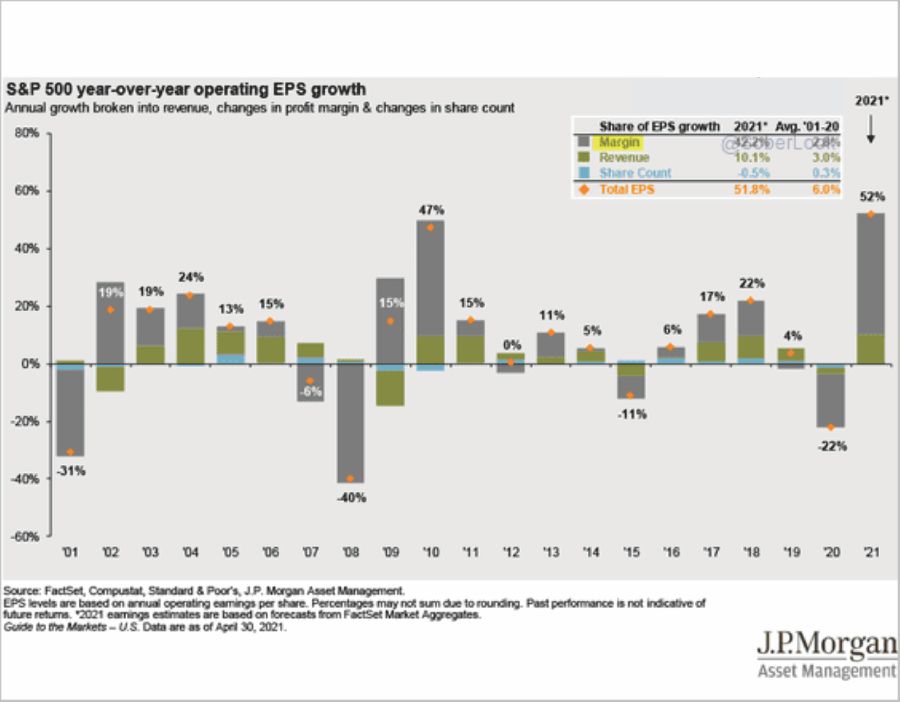

The first is that earnings guidance has not been “exuberant.” Many companies are starting to express concerns over inflationary costs (including labor) and weaker future demand as stimulus fades. The problem with earnings in the near term is that most earnings improvement has come from expanding net margins.

That massive boost to net margins came from the economic shutdown. With reduced workforces, a shift to lower-cost “work-from-home,” and increases in productivity through technology, the surge in margins is not surprising. However, as the economy “reopens,” that tailwind to earnings will fade quickly. The rise of inflationary inputs, increased employment, and potentially higher taxes will shrink net margins dramatically in the quarters to come.

Such also suggests that analyst’s extremely optimistic earnings revisions will likely need to shift down as well. If the market is indeed sniffing out an “earnings peak” short term, it could be increasingly difficult to justify currently high asset prices and valuations.

Here is the problem for investors currently. Given analysts’ assumptions are always high, and markets are trading at more extreme valuations, such leaves little room for disappointment. As shown, using analyst’s price target assumptions of 4700 for 2020 and current earnings expectations, the S&P is trading 2.6x earnings growth.

In other words, is the recovery all priced in? The bond market thinks so.

Bonds Aren’t Buying It.

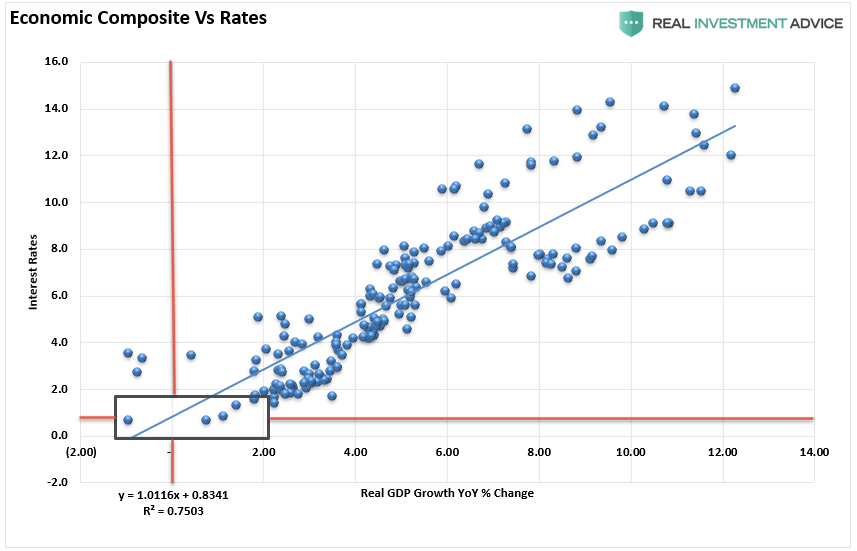

Over the last couple of weeks, we have discussed the correlation between rates and economic growth. To wit:

“As shown, the correlation between rates and the economic composite suggests that current expectations of sustained economic expansion and rising inflation are overly optimistic. At current rates, economic growth will likely very quickly return to sub-2% growth by 2022.”

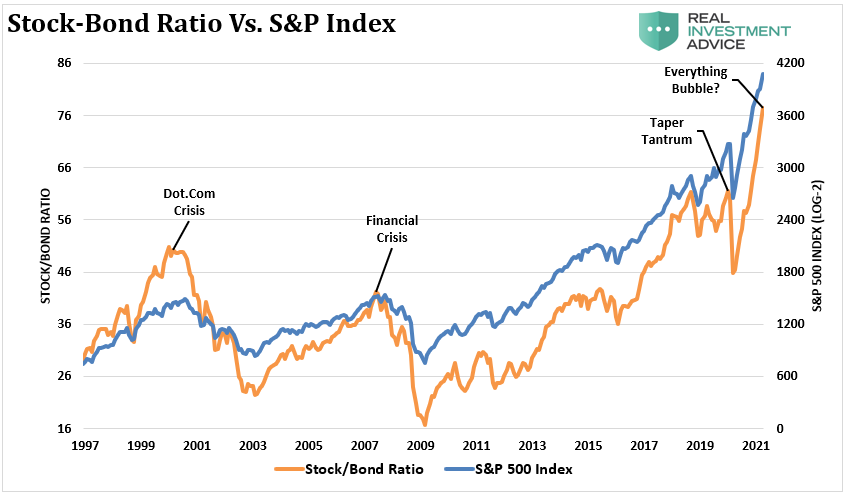

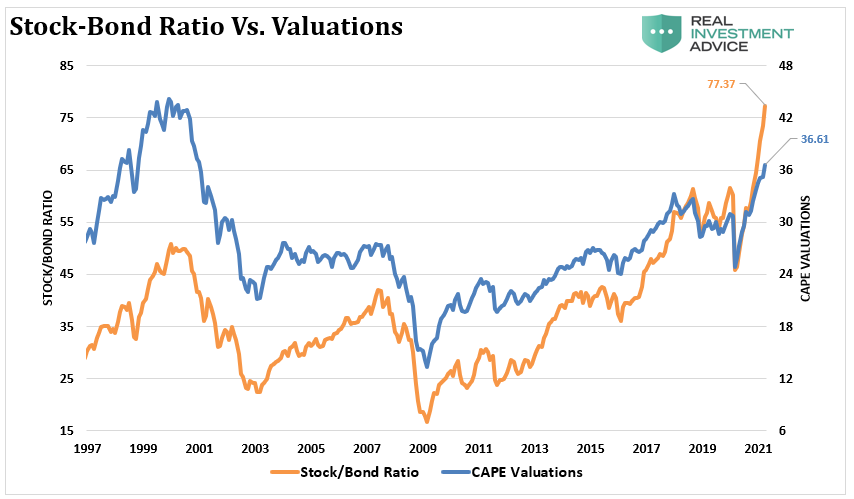

Not surprisingly, given the substantial rise in asset prices, the ratio of stocks to bonds (S&P Index / Bond Total Return) surged to a record high. It is worth noting that previous stock/bond ratio peaks have coincided with corrections and bear markets.

Given we already know high valuations equate to low long-term returns, the outlook for returns gets confirmed by the extreme stock/bond ratio,

Importantly, as discussed here, indicators like stock/bond ratios, valuations, and fundamentals all suggest low returns over the longer term. However, in the short-term, the next few weeks or months, there is very little correlation.

It will be the Federal Reserve that controls the near term.

The Fed May Not Like What It Gets

Over the last couple of weeks, both Fed members and Treasury Secretary Janet Yellen floated “trial balloons” that it may be time for the Fed to start lifting rates. The latest comments came from Dallas Fed President Robert Kaplan when he noted the Fed is likely to achieve its “substantial progress” metric as the economy recovered faster than expected.

As I discussed last week:

“The Fed is again suppressing rates but should be using the massive liquidity injections and economic recovery for hiking rates and taper bond purchases to prepare for the next downturn.”

Over the next couple of months, there will be an evident surge in inflation, which the Fed wanted. However, that surge in inflation may come in a lot “hotter” than they anticipated. If that occurs, bond yields will jump higher, effectively “tightening” monetary policy very quickly.

“The Fed has been very articulate in the message they are sending, and as I mentioned the last time, they are placating the equity market. But at the same time, daring the bond market to push rates higher. If the Fed gets its wish of higher inflation, it will push long-term rates significantly higher from here, and there is no way for the equity market to combat that.

The problem is that the market already is trading at its most overvalued levels vs. the 10-year since the mid-2000s when all of this low rate policy began.The higher stocks and yields move, the more overvalued the equity market grows, and the more dangerous it becomes.” – Mott Capital Management

Maybe More Than Just Talk

While the Fed continues to push the narrative, they “aren’t even thinking about thinking about tapering,” the recent “trial balloons” from both the Fed and Treasury may suggest differently. More importantly, as Mott concludes:

“While it sounds all fine and great for the equity market now, it won’t be if rates get just a little bit higher. Powell clearly made the correct call at the March meeting, buying himself another six weeks, but with a slew of economic data coming in the next few days that will show a lot of inflation, he may find the next six weeks harder to endure.”

While the “bullish mantra” has continued to be, correctly, keep buying dips as long as the “Fed Goes BRRRRR,” there is a rising possibility the “printing presses” may need to be turned off. The Fed faces the problem and understands that if inflation runs hot, interest rates will rise. When that happens, it isn’t just the equity market that comes under pressure. Every market built on debt from houses to automobiles, credit markets, mortgage markets, and consumer credit is at risk.

Of course, the biggest issue of all is when the reversal in equities occurs. That reversal will ignite the leverage that now extends into levered ETF’s, cryptocurrencies, options, and a myriad of other speculative investments.

In other words, the Fed got trapped between continuing to suppress interest rates or deflating the most significant asset bubble in financial history. While the hope is that the Fed can do it in a controlled manner (a soft landing), the Fed’s past attempts have been less than successful.

Portfolio Update

As we noted last week,

“Another reason we don’t expect a lot of upside to markets because the recent “consolidation” failed to work off any of the overbought conditions. Notably, the market remains more than 5% above its 50-dma, which is historically extreme. Such gets corrected, usually through a price decline or a consolidation.”

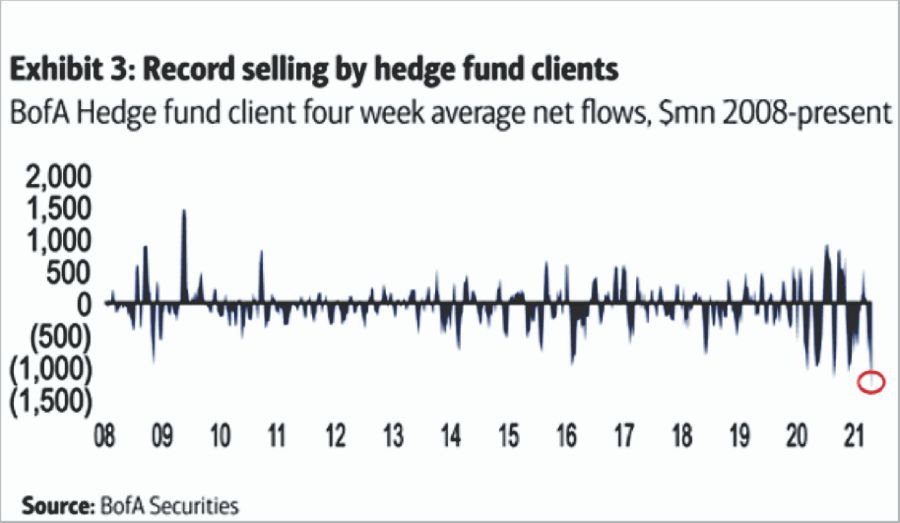

Our “sell signals” have kept us somewhat underexposed to equities and slightly overweight cash. However, the deterioration of “money flows” concerns us and aligns with hedgefund liquidations over the last several weeks.

Given the more extreme selling pressure and the current short-term oversold condition of the market, we have begun nibbling at exposures that we like. There is also a reasonable expectation we will start to see the major tech companies pick up a bid as managers look for positions with lots of liquidity as we head into the weaker summer months.

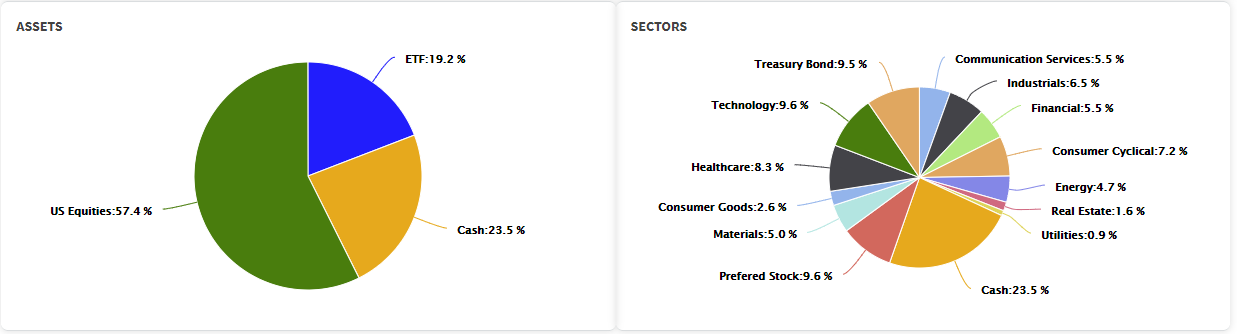

As shown, we are continuing to run a “barbell” approach to portfolios by overweighting our inflation sectors and underweighting our deflation sectors relative to the benchmark. (60/40 index) We have a very short-duration bond portfolio, which is why our “cash” is overweight. (Primarily 1-3 year duration holdings)

Once we get the next “buy” signal, we will adjust our weightings accordingly, but for now, we remain comfortable with our exposures. We continue to “tweak” the allocation as needed to adjust for risk as our intermediate-term concerns remain.

As David Rosenberg recently noted:

“The worst thing anyone can do is to extrapolate to the future. As Bob Farrell once said: ‘When all the experts and forecasts agree, something else is going to happen.’ The consensus has never been more lopsided, and that is reflected in asset allocations that heavily weight stocks relative to bonds.”

We agree.

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

The post Poor Jobs Report Gives Bulls A Reason To Charge 05-08-21 appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.