In this 07-09-21 issue of “Yields Plunge Dollar Surges The Reflation Trade Unravels.“

- Market Pulls Back As Signals Turn

- Yield Plunge, Dollar Surge

- The Reflation Trade Unravels

- Portfolio Positioning

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Market Stumbles But Rallies Back

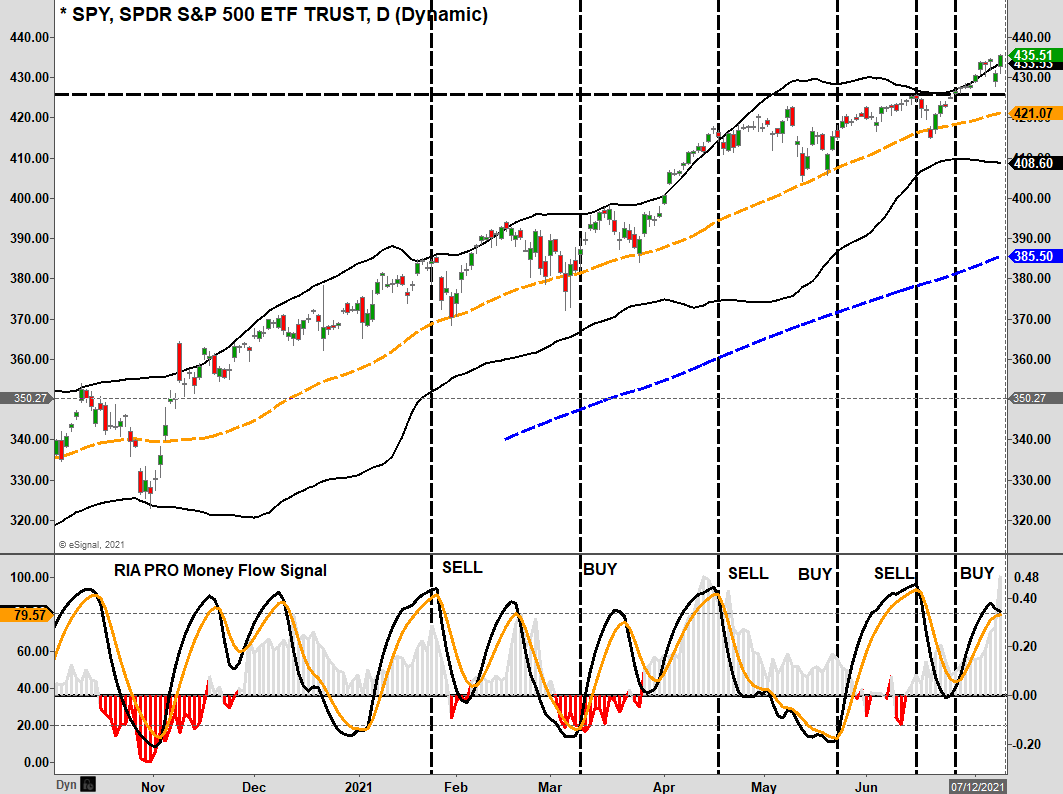

Last week, we discussed the market hit new highs with the index getting back to more extended and overbought conditions. To wit:

“The technical backdrop is not great. With the market back to 2-standard deviations above the 50-dma, conviction weak, and investors extremely bullish, the market remains set up for additional weakness.

However, we are in the first two weeks of July, which tends to be bullishly biased. After increasing our equity exposure previously, we will give the market the benefit of seasonality for now.”

While market volatility did pick up this past week, the index held its breakout support levels and closed at a new high. Such keeps the bullish bias intact. However, as shown, the money flow signals are now back to more elevated levels, which will provide resistance to higher prices short term.

We are still within the seasonally strong period of July, which tends to last through mid-month. However, August and September are typically more challenging for returns. As we stated last week:

“The bulls are indeed in charge of the markets currently, but the clock is ticking.”

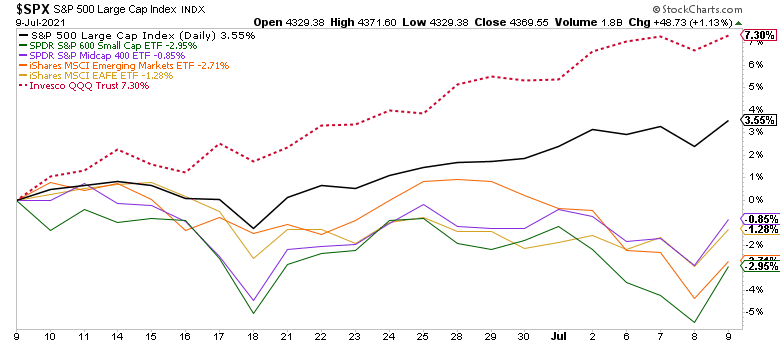

The market is also weak from a breadth perspective. While large-cap stocks have done better as of late, the rest of the markets have not. I discuss this in more detail in Friday’s video.

The critical point, as noted in the video, is there has been a definite rotation out of the “reflation trade” (small, mid, emerging, and international markets) into the large-cap names (primarily technology), which is the “deflation trade.”

As we will discuss, the reflation trade ran well ahead of reality. Over the next couple of months, the test will be to see if earnings can support the surge in prices and valuations.

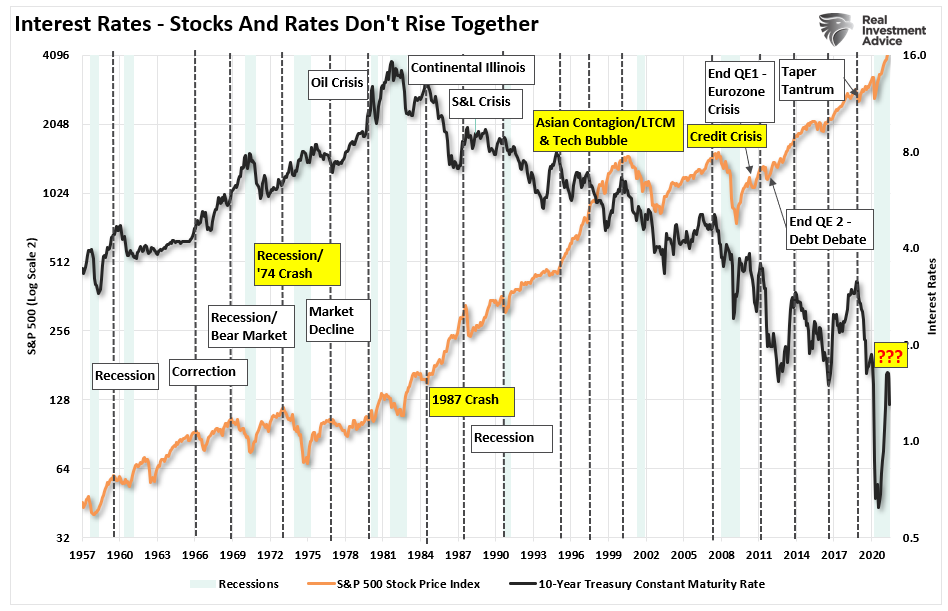

Yields Overbought

We will discuss the “yield warning” momentarily. However, in the short term, yields have gotten very overbought. We suspect we could see a retracement in yields short-term, but such will likely be an opportunity to increase bond exposure in portfolios as we head further into the year.

As shown, previous overbought conditions (indicators get inverted concerning yields) lead to retracements to resistance. Currently, a retracement to 1.5% would be likely. Ultimately, a break below 1.25% will suggest much lower yields are coming.

From a positioning standpoint, we increased our bond duration several weeks ago. However, while we want to increase our exposure eventually, we need to wait for the short-term overbought condition to reverse.

Longer-term, as we will discuss next, we believe yields are potentially headed lower as economic growth and inflationary pressures wane.

Yield Plunge, Dollar Surge

In our #MacroView this week, we discuss the warning sign that yields are sending in more detail. However, importantly, the plunge in yields is suggestive that something in the market is becoming strained. As discussed in that article, when interest rise, and peak, such has corresponded with more negative market outcomes.

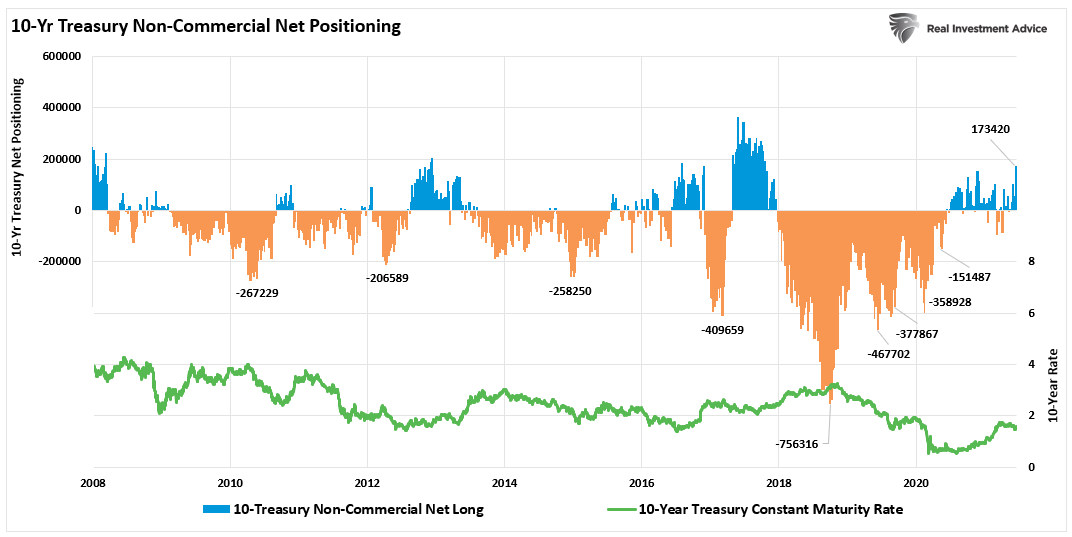

Is the current rise in rates signifying the next market downturn? Historically, sharp spikes in rates have done so by slowing economic growth more than expected. However, as we noted previously in our Commitment Of Traders report:

“The number of contracts net-long the 10-year Treasury already suggests the recent uptick in rates, while barely noticeable, maybe near its peak.”

Some of the pressure in bonds has come from the market bracing itself for some large auctions of new bonds next week. A lot of the action on Friday was the shift in focus to next week’s auctions. On Monday, there will be $38 billion in 10-year notes and $24 billion in 30-year bonds on Tuesday.

However, as noted by Zerohedge on Friday:

“But those who are betting on a continued rise in yields may get disappointed for one key technical reason. As Morgan Stanley’s derivatives strategist Chris Metli notes, CTAs – those mindless trend-followers who just ride on momentum waves until they crash, are still short bonds and at current yields have to buy $95bn notional of TY-equivalent duration over the next week.

As Morgan Stanley notes such ‘could continue the bond rally and put pressure on stocks as equity investors fear the bond market knows something they don’t about future growth prospects.’”

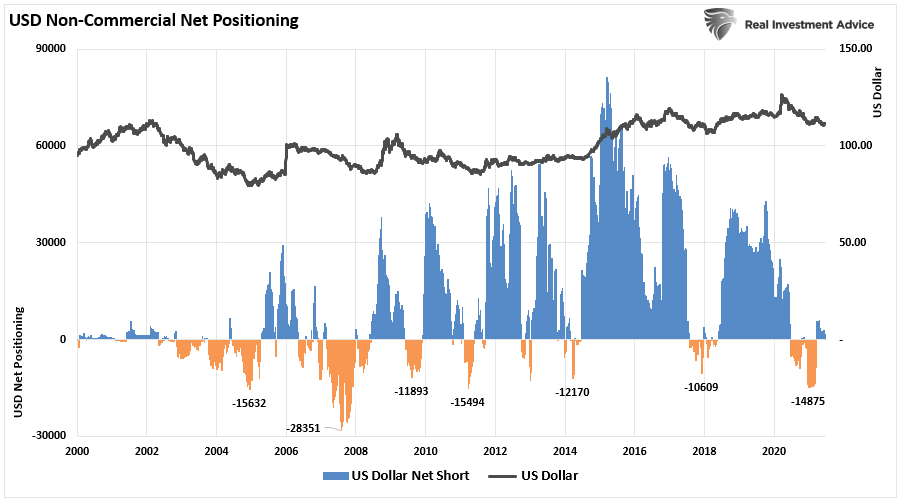

The dollar is also confirming the same.

In Case You Missed It

The Dollar Is Confirming The Same

We specifically noted that the dollar was about to rise sharply. To wit:

“The one thing that always trips the market is what no one is paying attention to. For me, that risk lies with the US Dollar. As noted previously, everyone expects the dollar to continue to decline, and the falling dollar has been the tailwind for the emerging market, commodity, and equity risk-on trade. So, whatever causes the dollar to reverse will likely bring the equity market down with it.”

While the dollar rally is still young, there was a successful test of the “double bottom” with higher lows. The break above the 50- and 200-dma also suggests the rally is just getting started. A further rally in the dollar will get fueled by additional short-covering.

There is a significant difference between a “recovery” and an “expansion.” One is durable and sustainable; the other is not.

Dollar & Rates Are Warning Signs

Those expecting a significant surge in inflation will likely be disappointed for the one reason which seems to get mostly overlooked.

“If the economy were growing organically, which would create stronger rates of wage growth and inflation, then there would be no need for zero interest rates, continued monetary interventions by the Federal Reserve, or deficit spending from the Government.”

The obvious problem is that not all “spending” is equal. Pulling forward consumption through stimulus is indeed short-term inflationary but long-term deflationary. Moreover, since 1980, there has been a shift in the economy’s fiscal makeup from productive to non-productive investment.

As we have pointed out previously, you can not overstate the impact of psychology on an economy’s shift to “deflation.” When the prevailing economic mood in a nation changes from optimism to pessimism, participants change. Creditors, debtors, investors, producers, and consumers change their primary orientation from expansion to conservation.

- Creditors become more conservative and slow their lending.

- Potential debtors become more conservative and borrow less or not at all.

- Investors get increasingly conservative, and they commit less money to debt investments.

- Producers become more conservative and reduce expansion plans.

- Consumers become more conservative, and save more, and spend less.

As we have been witnessing since the turn of the century, these behaviors reduce the velocity of money. Consequently, the decline in velocity puts downward pressure on prices. Moreover, given the massive increases in debt and deficits, the deflationary drag increases as the stimulus fades from the system.

Likely, the dollar and rates already figured this out.

The Reflation Trade Unravels

The importance of this analysis relates to a potential change in investor positioning in the market. To wit:

“The unraveling of the inflation/reflation trade has accelerated over the past week. US 10y bond yields continue to decline and have now broken a crucial technical level. Such could see the rally accelerate sharply, and with it, the continued unraveling of both cyclicals and commodities.” – Albert Edwards

Albert’s comment aligns with our views previously that such would likely be the case.

I believe that the pandemic recession allowed policymakers to cross the Rubicon of fiscal rectitude. They have reached a new land where existing monetary profligacy can now get coupled with fiscal debauchery.

In that respect, I am very much in the inflation/reflation camp. But I think it is a secular theme that will play out later in this cycle. The problem is the markets have been too early in betting on the reflation trade and have gotten set up for a huge disappointment.”

We have previously discussed the change in the deflationary credit impulse. But, importantly, the bond and dollar markets are now reflecting that deflation.

Does such mean the markets will crash tomorrow? No.

What is critical to recognize is that the market is well ahead of what reality will turn out to be. As such, when overly exuberant earnings and economic growth expectations fade, the justification supporting overpaying for assets will run into trouble.

Portfolio Update

There is something “not quite right” with the market currently. As discussed previously, the problem with technical indicators is that they do not distinguish between a consolidation, a correction, or more. Therefore, we have to pay attention to warnings, much the same as driving a car.

A yield sign is a warning. We have a choice to blow through yields signs and may get away with it 100 times. However, the 101st time leads to a devastating crash. In the markets, the warning signs suggest reducing our “speed” in the portfolio slightly, watching for risk, and then returning to speed once the danger has passed.

After increasing our bond duration in portfolios to hedge risk, we removed our index trading positions this past week and lowered our equity exposure to hedge risk further. (We slowed down.)

With our money flow “sell signals” approaching high levels, taking some action could be beneficial.

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

Minor adjustments can make significant differences to outcomes when you can avoid “the wreck.”

By Lance Roberts, CIO

The post Yields Plunge. Dollar Surges. The Reflation Trade Unravels. 07-09-21 appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.