In this 09-10-21 issue of “‘Investors Hold Record Allocations Despite Rising Warnings.“

- Market Starts Correction Right On Cue.

- Investors Record Allocations & Rising Warnings

- Beige Book Highlights Fed’s Biggest Problem

- Portfolio Positioning

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Market Starts A Correction Right On Cue

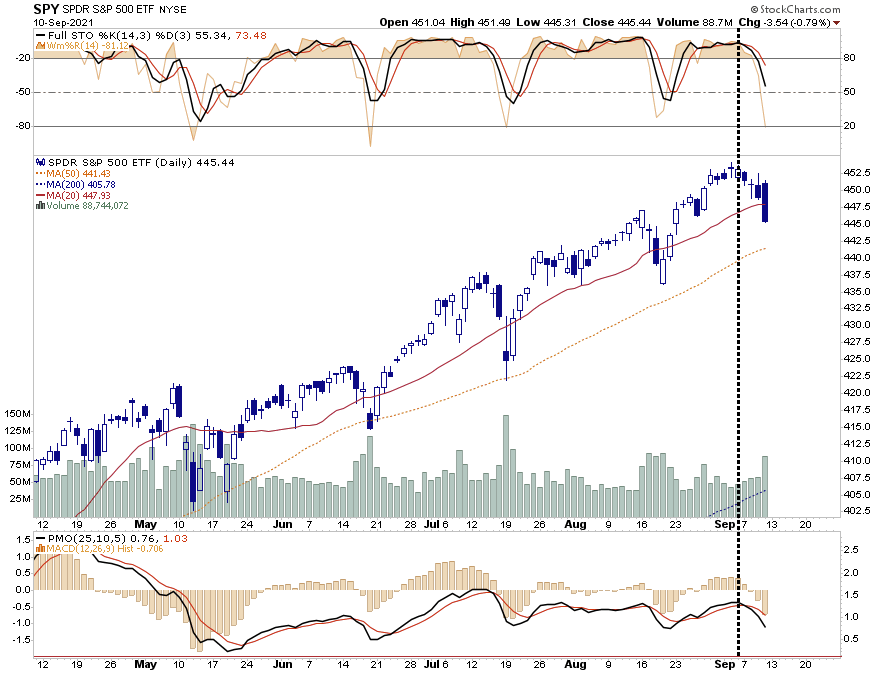

“However, in the meantime, the “stairstep” advance continues with fundamentally weak companies making substantial gains as speculation displaces investment in the market. Thus, while prices remain elevated, money flows weaken, suggesting the next downturn is roughly one to two weeks away. So far, those corrections remain limited to the 50-dma, which is approximately 3% lower than Friday’s close, but a 10% correction to the 200-dma remains a possibility.”

That correction started on Monday with the week ending in 5-straight down days which is the worse slide since February.

However, while that sounds terrible, the total decline for the week was just -1.69%. Yes, that’s it, less than 2%. While CNBC probably ran their “Markets In Turmoil” segment, traders were huddled over candles and incense chanting incantations at the Fed for more accommodation.

With sell signals in place, volume rising, and breadth weak, a retest of the 50-dma early next week will not be a surprise. The question will be whether traders show up again, as they have done every other time over the last 6-months to “buy the dip.”

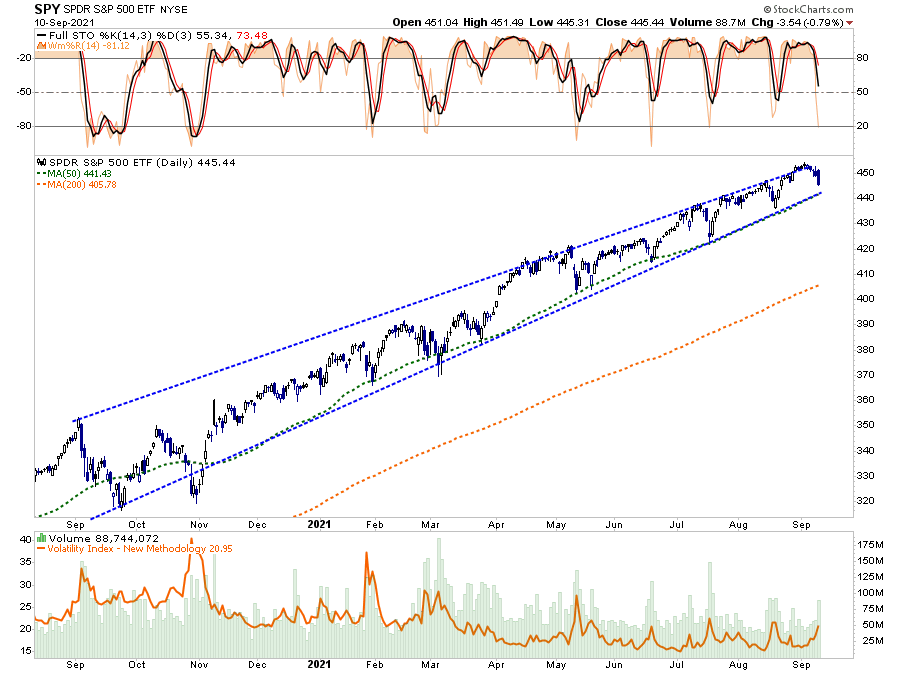

As shown, the market remains well confined to its rising trend with support sitting at the 50-dma. Volatility did pick up late last week as volume spiked suggesting more selling pressure on Monday.

The question is “this time different.” Will the market hold the 50-dma again, or has the risk of a more substantial correction finally caught up with investors.

As noted previously, 5-10% corrections are absolutely normal in any given market year. However, if you didn’t like the 1.69% correction this week, a 10% correction will feel like an all-out “crash.”

Such is why we have repeatedly suggested taking some actions in advance.

Macro Conditions Continue To Deteriorate

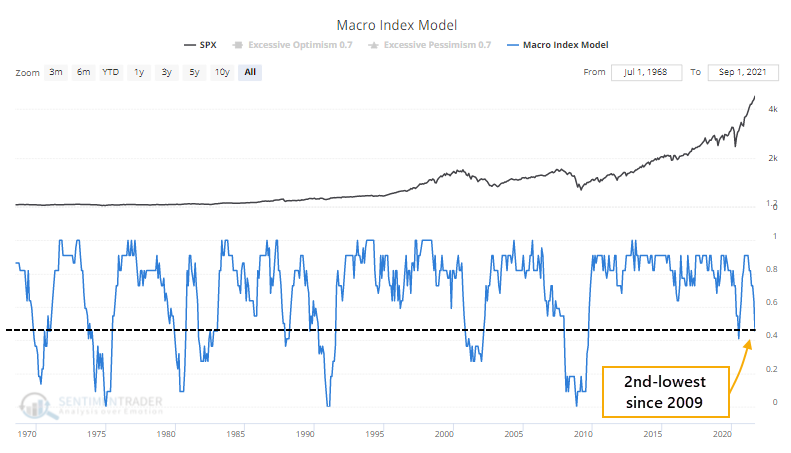

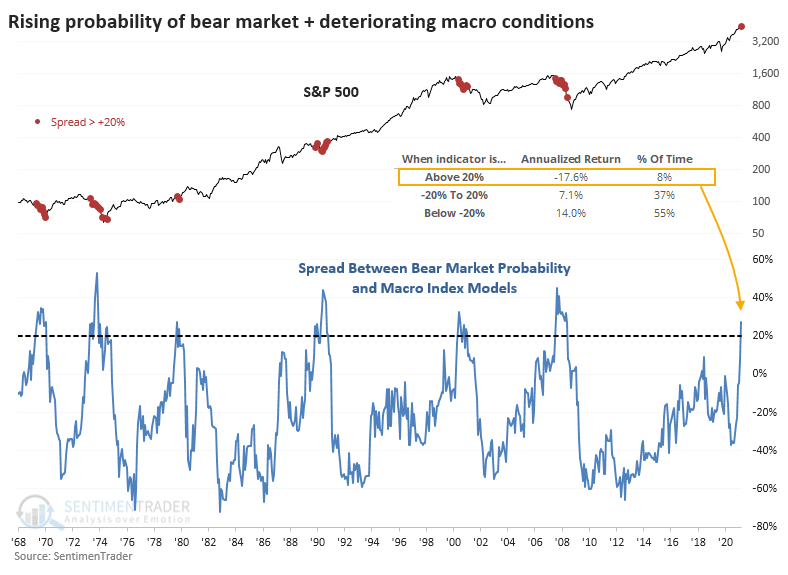

Over the last couple of weeks, I noted the deterioration of underlying market conditions. Weakening breadth, lower participation, and negative divergences all suggest risks of a correction. On Thursday, Sentiment Trader provided some additional commentary supporting our concern.

“To differentiate temporary slowdowns from real problems, we look for significant macro deterioration. The Macro Index Model combines 11-diverse indicators to determine the state of the U.S. economy. Stock market investors should be bullish when the Macro Index is above 0.7 and bearish when below or equal to 0.7.

Once the final reports were in for August, the model plunged below 46%, the 2nd-lowest reading of the past decade.“

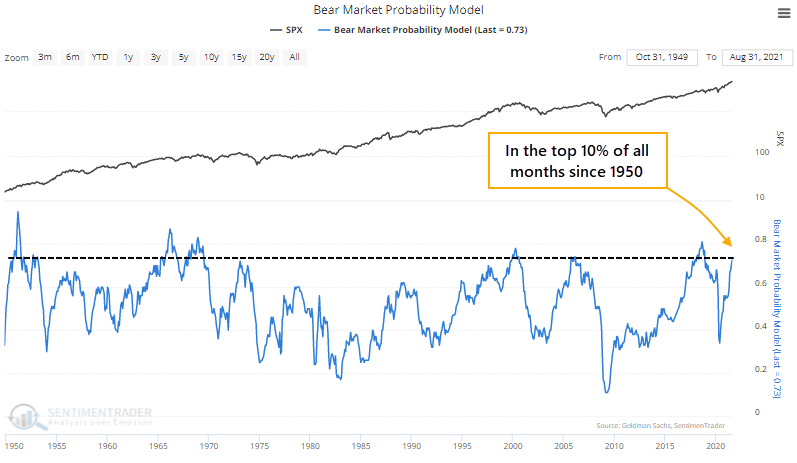

At the same time, Sentiment Trader noted their Bear Market Probability Indicator also jumped. This model has 5-inputs, namely the unemployment rate, ISM Manufacturing index, yield curve, inflation, and valuations.

“The higher the score, the higher the probability of a bear market in the months ahead. Last May, the model was in the bottom 10% of all months since 1950. This month, it jumped into the top 10% of all months.“

So, what does all of this mean? According to Sentiment Trader, the combination of these two measures should not be overlooked. To wit:

“The chart below shows the spread between the Bear Market Probability and Macro Index models. The higher the spread, the higher the probability of a bear market. The chart shows that the S&P 500’s annualized return is a horrid -17.6% when the spread is above 20% like it is now.”

The point here is that while the market remains exceedingly bullish, there are signs of trouble brewing beneath the surface. Such is why we suggested raising cash levels, adding non-correlated assets, and reducing overall risk.

But as Paul Harvey used to say: “There is more to this story.”

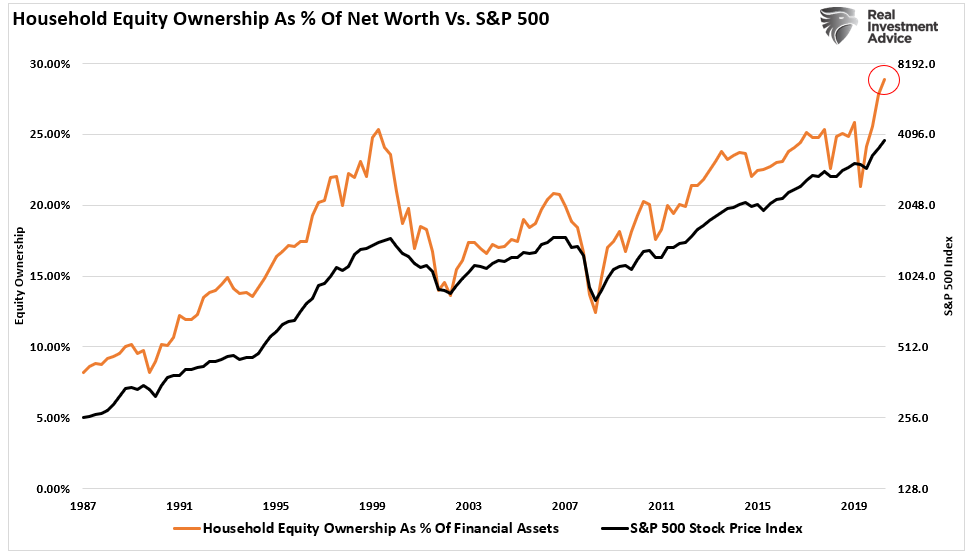

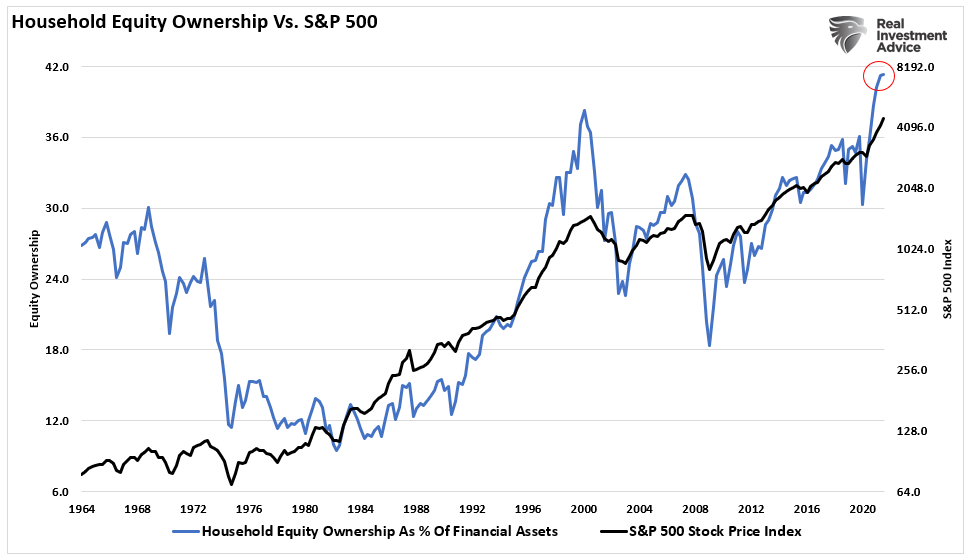

As noted, there is certainly cause for concern. However, investors aren’t.

Such should be of no surprise after an extended bull market advance with very low volatility. Without any concern for corrections, individuals have increased equity risk levels relative to their overall net worth.

Or, we see the same when we analyze their equity allocations as a percentage of their overall financial assets.

Regardless of the calculations, the message is the same. As we noted in Thursday’s Daily Market Commentary:

“Bob Farrell’s rule #5 states: “The public buys the most at the top and least at the bottom.”

The two charts above speak volumes as to the wisdom of Bob Farrell’s rules. Previous peaks in equity ownership have corresponded with peaks in financial markets.

As the old Wall Street axiom states: “If everyone has already bought, who is left to buy?”

At the moment, however, investors are incredibly confident that markets can only go higher as long as the “Fed” remains accommodative. While there is undoubtedly a substantial argument as to the ability of the Fed to keep markets inflated, there are other “risks” present that could lead to a short-term correction.

While investors are carrying record allocations, some of the largest Wall Street banks are worrying. A recent article on Zero Hedge compiled their outlooks. To wit:

“Andrew Sheets warns that equity market internals has continued to follow a “midcycle transition.” That process usually ends with quality stocks, like the FAAMGs, getting hit and poses an outsized risk to the S&P 500 through October.” – Morgan Stanley

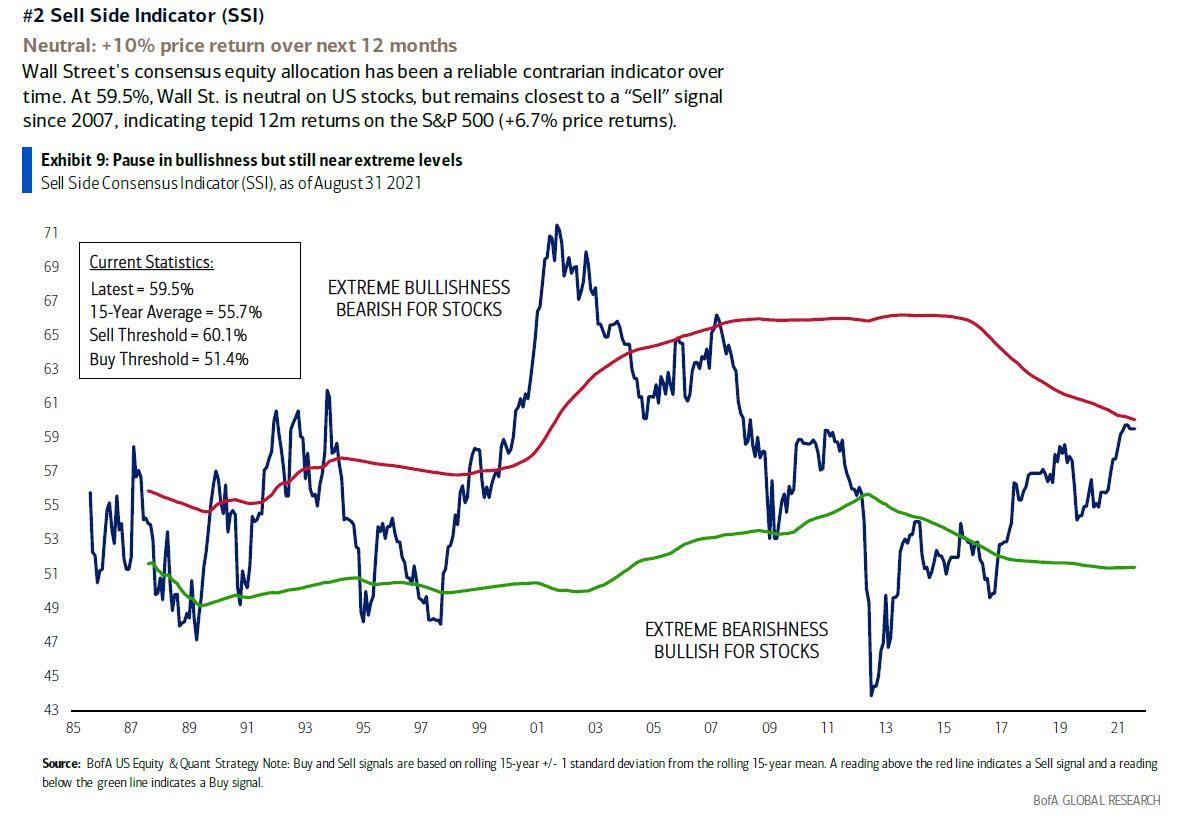

“Suvita Subramanian, warned that ‘downside risks remain’ and asking ‘what good news is left?’ Sentiment is all but euphoric with our Sell Side Indicator (see SSI) closer to a sell signal than at any point since 2007.” – Bank of America

Deutsche Bank’s strategists ‘expect an imminent correction‘ even though they see the S&P 500 rising back around current levels by year-end. Some more details on the coming pullback in markets which DB believes will see the S&P drop 6%-10%:

Christian Mueller-Glissmann stated that high valuations have increased market fragility. If there is a new negative development, it could generate growth shocks that lead to rapid de-risking. As such, there is very little buffer left if you get large negative surprises.” – Goldman Sachs

You get the idea. Between the leverage in the market, economic growth slowing, and rising inflationary pressures, numerous issues could disrupt the high levels of market complacency.

The bullish argument is that such a correction will force the Fed’s hand. As Zerohedge aptly concluded:

“Even the smallest market hiccup will prompt a furious response at the Marriner Eccles building, because we are now well beyond the point of no return and Jerome Powell and company simply can not afford even the smallest drop in stocks without risking a full-blown market meltdown, much to the chagrin of the banks above who are predicting just that.”

In Case You Missed It

Beige Book Reveals The Fed’s Biggest Problem

The most significant risk for the market is a change in investor psychology. As long as nothing disrupts that bullish bias, investors will continue to aggressively “buy dips.” However, that psychology is directly linked to the Fed’s ongoing balance sheet expansion. Thus, the potential problem for investors is inflation.

The Fed’s Beige Book is a summary of economic conditions in the 12 Federal Reserve Districts.

- Boston: “Inability to get supplies and to hire workers.”

- New York: “Businesses reporting widespread labor shortages.”

- Philadelphia: “Labor shortages and supply chain disruptions continued apace.”

- Cleveland: “Staff levels increased modestly amid intense labor shortages.”

- Richmond: “Many firms faced shortages and higher costs for labor and non-labor inputs.”

- Atlanta: “Wage pressures more widespread.”

- Chicago: “Wages and prices increased strongly”

- St. Louis: “Contacts continued to report labor and material shortages.”

- Minneapolis: “Hiring demand outstriped labor response by a wide margin.”

- Kansas City: “Wages grew at a robust pace.”

- Dallas: “Wage and price growth remained elevated amid widespread labor and supply chain shortages.”

- San Francisco: “Hiring activity intensified further, as did upward pressures on wages and inflation.”

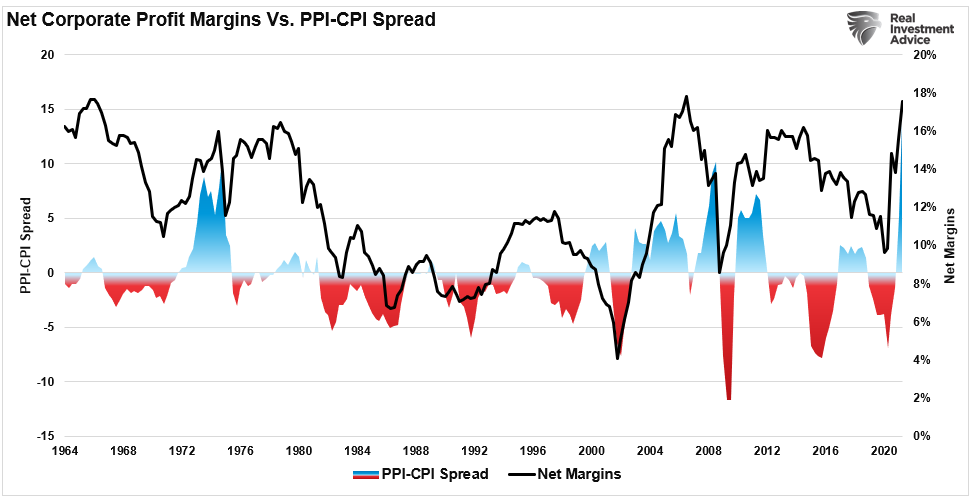

Inflation is becoming problematic for the Fed mainly if these pressures are not as “transient” as hoped. Higher wages are corrosive to both earnings and margins. As shown below, strongly rising producer prices are initially good for profit margins until inflation can not get passed along to consumers. Such is the case currently, with the most significant historical spread between PPI and CPI.

With supply chain disruptions looking to last longer than expected, the Fed is trapped between supporting a slowing economy and fighting inflation.

It’s a battle they are likely going to lose, no matter what they choose.

As noted above, market action became sloppier this week.

Over the last few weeks, we discussed that stock selection was essential to portfolio performance as breadth continues to narrow in the market. This past week was not much different. The question is now whether the previous leaders will become laggards? Such could suggest more trouble overall for markets.

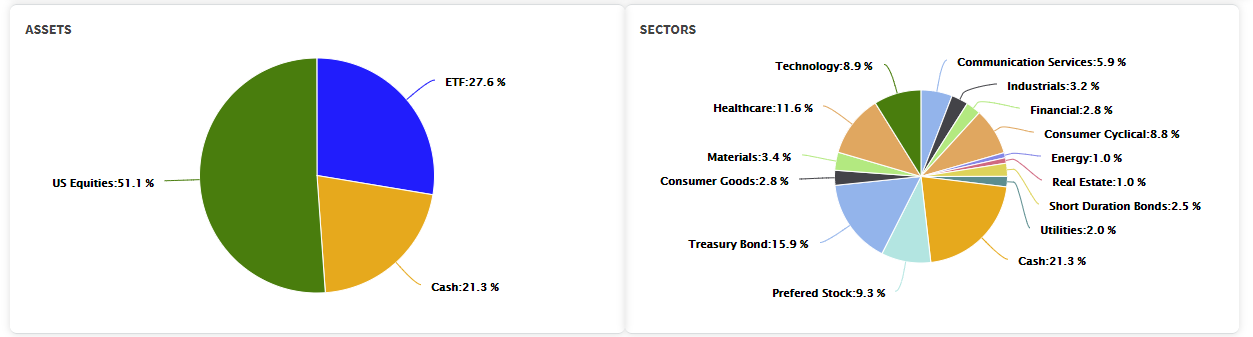

In the meantime, equity allocations remain underweight. We have increased the bond portfolio duration closer in alignment with our benchmark as we continue to look for lower rates as economic growth slows. Cash remains roughly 10% of our equity allocations as a risk hedge for now.

As noted above, there is a reasonable possibility the market stalls at current levels and works off some of the overbought conditions. There is also a more than a possible risk of a correction between 5% and 10%.

However, I don’t know which it will be until we start seeing definite signs of the market breaking down. At that point, it will be too late to make adjustments. Such is why, as we have stated previously, this is an opportune time to get in front of risk by taking some simplistic actions.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines. (Cash, Non-correlated Assets, Direct Hedges)

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

These actions will not protect you from a decline. They will, however, lessen the blow and allow you to rebalance risk accordingly where they become present.

Or, you can do nothing and hope for the best.

It’s your choice.

Have a great weekend.

By Lance Roberts, CIO

The post Investors Hold Record Allocations Despite Rising Warnings 09-10-21 appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.