We dig into the bullish and bearish case for the market as we head into the end of the year. Currently, investors face a conundrum between year-end seasonality and the Fed starting to taper its bond-buying program. Such was evident in a recent email I received from a reader:

“I am holding a lot of cash, and am worried about a deeper correction. While I understand that you recently got more aggressively allocated due to improving short-term technicals, the risk of the Fed beginning to taper their bond-buying seems to be problematic. What do you think I should do?”

It’s a great question, and one that I think represents many of our readers.

One of the biggest challenges investors always face is allocating capital to markets once a correction has occurred. The concern is purely emotional as investors worry the market may continue to decline. While specific reasons suggest a deeper correction is possible, other factors are supporting a more positive outcome.

In the longer term, it is only fundamentals that matter. So what is happening between the economic and earnings data is all you need to know if you are a long-term investor.

Unfortunately, you aren’t.

Despite all of the protestations that you are a long-term investor, most are not. The emotional biases of being either bullish or bearish, primarily driven by the media, keep you from truly focusing on long-term outcomes. Instead, you either worry about the next downturn or are concerned you are missing the rally. Therefore, you wind up making short-term decisions that negate long-term views.

Understanding this is the case, let’s look at the markets from both a bullish and bearish perspective. From there you can decide what to do next.

The Bullish Case

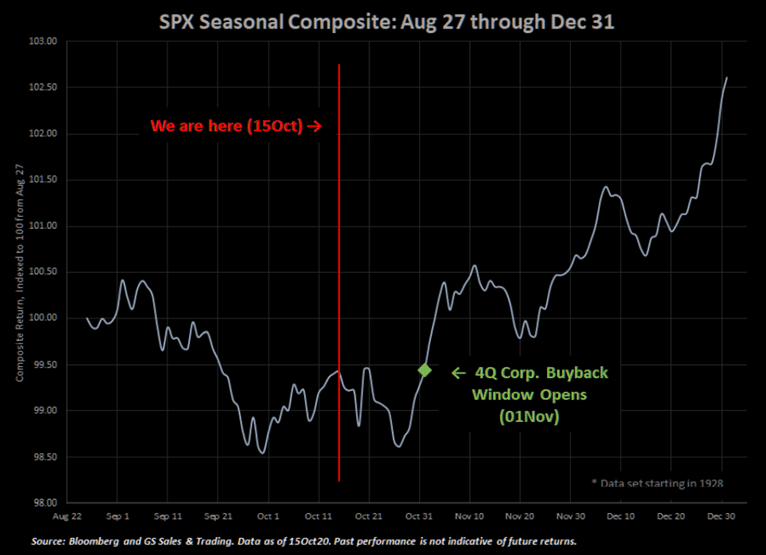

1) Seasonality

With the recent correction in October now behind us, the market is entering into the “seasonally strong” period between November and May. While this period does not always provide positive returns, the statistical tendencies favor increased equity exposure. The chart below from TheMarketEar shows the average return profile from October through the end of the year.

Importantly, notice the corporate stock “buyback” window that opens on November 1st.

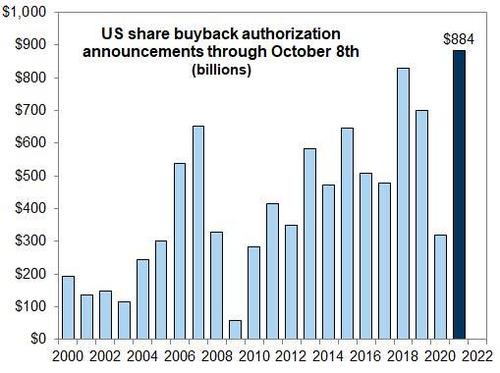

2) Corporate Share Buybacks

A significant source of liquidity over the last several years, and in this year, in particular, has been the record levels of cash utilized by companies to repurchase their shares. Such has provided underlying support to asset prices as corporations provide a consistent bid for stocks.

“In Q4, the GS buyback desk estimates +$230B repurchases, this is broken down by +$70B in October during the blackout window using 10b5-1 plans and +$160B in November and December.” – Zerohedge

“According to GS Research, November is the best month for buyback executions, November plus December is the best two month period of the year for executions. November 1st is the defacto start to the buyback season with 65% of corporations in the open window. That is followed by November 8th where 90% of corporates are in the open window.” – Zerohedge

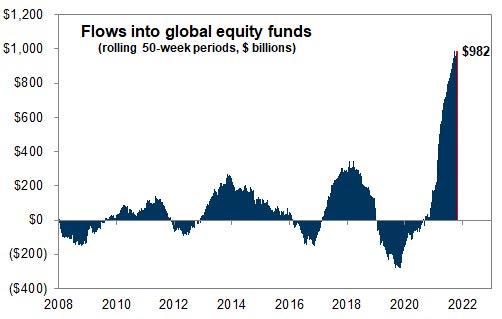

3) Money Flows Remain At Historic Highs

Of course, it is not just corporate share buybacks supporting asset prices currently, but record global inflows of capital at a pace never before seen in history. Now at $982 billion, and counting, the flood of liquidity globally into equities is unprecedented.

“Global equity inflows surpassed $774.5 billion on a year-to date basis. It is the best year on record by a mile. In the 190 trading days ending on October 6th. This will be roughly $1 Trillion worth of inflows for 2021. That is approximately +$4.1 billion worth of [retail] demand every single day of 2021.” – Goldman Sachs

The bulls are carrying solid arguments for being long equities currently. With earnings season underway, sentiment reversed from recent bullish extremes, and an ongoing flood of liquidity, there is an inherent bias to the upside.

However, while the bulls case is strong, the bears have equally valid arguments for remaining cautious.

The Bearish Case

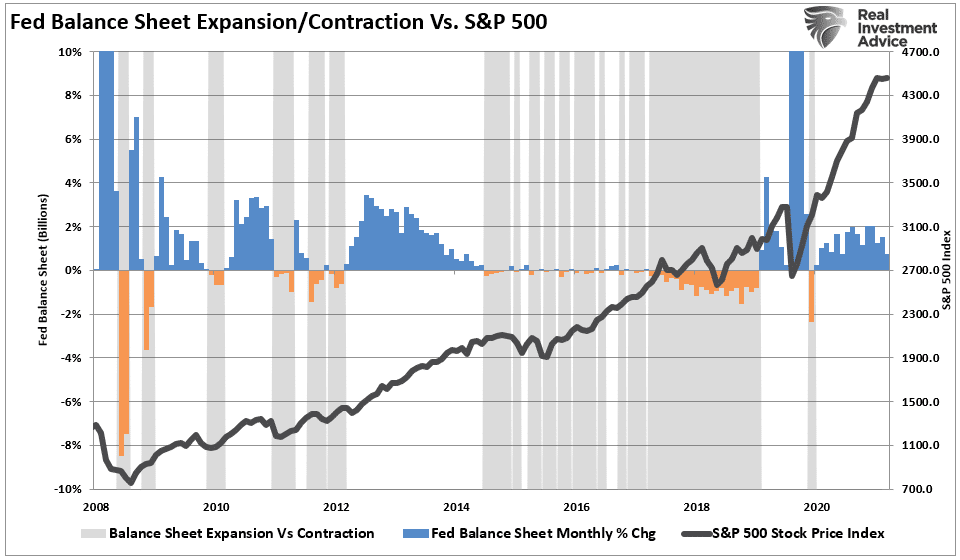

1) The Fed Is Set To Taper

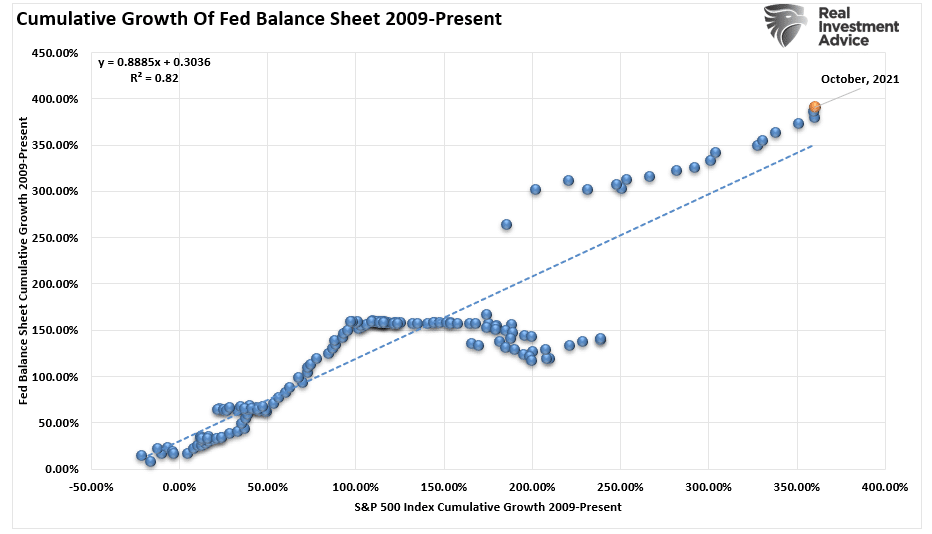

The most obvious concern for the “bears” is the Fed reducing their bond-buying activity starting in November. While many argue that “QE” has no impact on financial markets, as shown below, the “psychological” link between the Fed and the financial markets is apparent. Such is known as the “Fed put.”

The chart below shows the correlation between the monthly change in the S&P 500 Index and the Fed’s balance sheet. At 82%, there is a sufficient correlation to suggest a direct link between the markets and monetary policy.

With such a high correlation, it is not surprising that periods of a contraction in liquidity corresponds with increased market volatility and corrections in the markets. Thus, the grey shaded bars highlight the periods where the Fed’s balance sheet contracted in size.

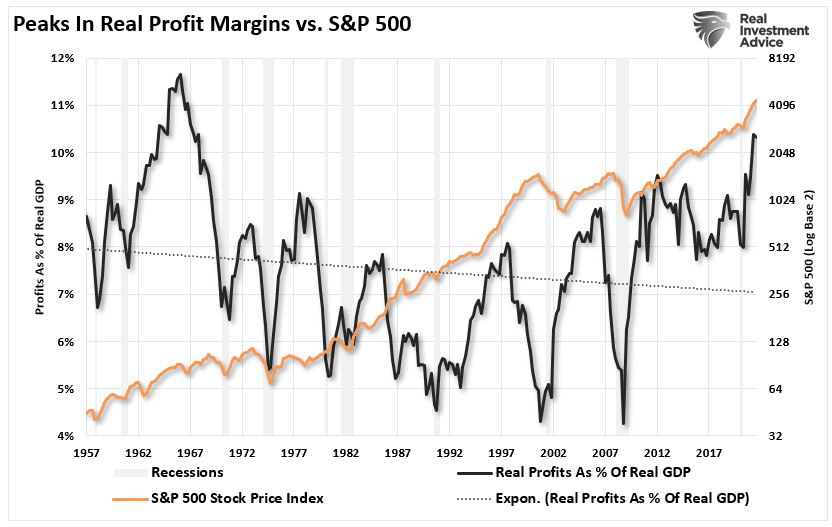

2) Profit Margins

Another concern is the surging level of inflation in the economy currently. Between supply line disruptions, inflationary pressures, and rising wages, corporations will face margin compression. Thus, the considerable risk to the bullish argument is that earnings fail to support currently high valuations.

Peaks in real (inflation-adjusted) profit margins correspond with peaks in financial markets. However, with profit margins currently elevated due to the $5 trillion in “pandemic relief” in 2020, the current contraction in fiscal policy supports combined with higher inflation could well deteriorate profits into next year.

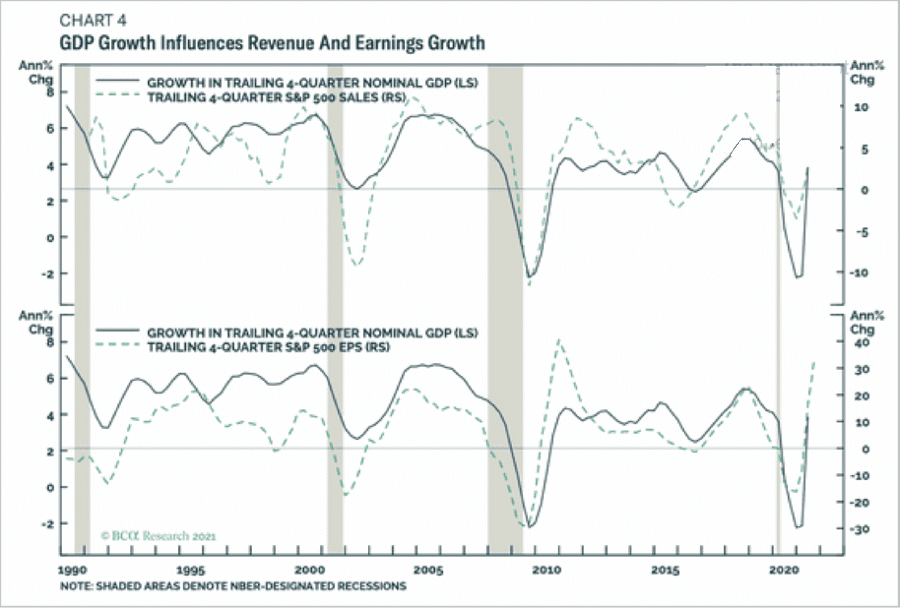

3) Economic Growth Continues To Weaken

While over the short-term markets can certainly rally on hope and optimism, there is a high correlation between economic growth, revenue, and stock market returns in the longer term.

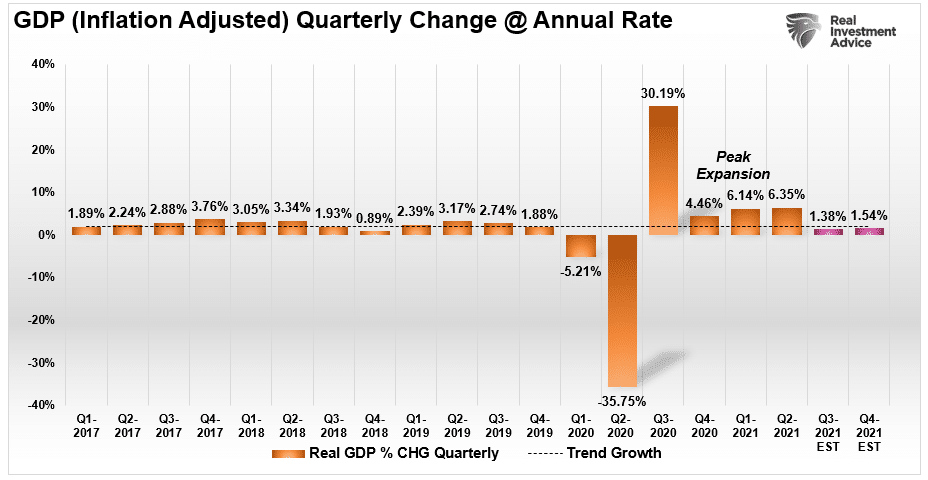

Early this year, estimates were for extraordinary rates of economic growth in 2021. However, as the months progressed and fiscal liquidity ran dry, economic growth rates are quickly reverting to the long-term means.

At the begging of Q2, the Atlanta Fed pegged economic growth at 13.5%. By the time GDP got reported by the Bureau of Economic Analysis, it was just 6.5%. The Atlanta Fed has ratcheted down Q3, which will get reported later this month, to just 1.2%. So far, while hopes are for more robust economic growth in Q4, there is a high probability of disappointment.

For the bearish view, the implications of substantially weak economic growth are broad. Consumer sentiment will continue to remain weak, and increased inflationary pressures will further undermine consumption. The impact on earnings will leave the bulls disappointed.

You Don’t Have To Pick A Side

So what do you do?

As we discussed previously, we believe there is enough to the bullish case to warrant additional equity exposure in portfolios. However, the longer-term dynamics are bearish.

But here is the crucial point – you don’t have to “choose.”

While many think you have to be either “bullish” or “bearish,” the reality is you don’t. In the short term, we can be “bullish” with our equity positioning. However, we can also be “bearish” in our longer-term views.

Regardless of whether you are bullish or bearish, we noted guidelines to increase your odds of success this past weekend.

- Move slowly. There is no rush in making dramatic changes.

- If you are under or over-weight equities, DO NOT try and fully adjust your portfolio allocation in one move.

- Begin by selling laggards and losers.

- Add to sectors, or positions, that are performing with, or outperforming the broader market.

- Move “stop-loss” levels up to recent lows for each position. Managing a portfolio without “stop-loss” levels is foolish.

- Be prepared to sell into the rally and reduce overall portfolio risk. Not every trade will always be a winner. Get rid of losing positions as redeploy capital as needed.

- If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

For now, we remain optimistic about the markets due to liquidity, seasonality, and a reversal in bullish sentiment. However, we remain concerned about the broader macro risks, which keep us cautionary.

There is little value in trying to predict market outcomes. The best we can do is recognize the market environment for what it is, understand the associated risks, and navigate accordingly to achieve the desired outcome.

The post Technically Speaking: The Bullish & Bearish Market Case appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.