Absolute returns or relative? There is a very important difference. Most investors say they want the latter, in reality, they want the former. The problem is they are unaware of the risk they are accepting.

I have had many discussions with clients, prospects, and listeners about the idea of “absolute returns” in portfolio management versus “relative returns.” The most common response to the discussion generally begins with:

“I understood the part up to where you started speaking.”

Kidding aside, the importance of the concept of absolute returns should not get dismissed. Such is particularly the case since Wall Street has trained most investors to believe that relative performance is all that matters.

- Relative performance is the comparison of the returns of your portfolio to that of some benchmark index.

- Absolute performance is the return of the portfolio itself on a year-over-year basis.

The reason that Wall Street wants you to focus on “relative performance” is they need you to continually “comparison shop.”

Wall Street Wants You To Compare

Comparison is the root cause of more unhappiness in the world than anything else. Perhaps it is inevitable that human beings as social animals have an urge to compare themselves with one another. Maybe it is just because we are all terminally insecure in some cosmic sense.

Let me give you an example. Assume your boss gave you a new Mercedes as a yearly bonus. Obviously, you would be thrilled, until you found out everyone else in the office got two. Now you are upset because on a “relative” basis you got less than everyone else. However, are you really deprived on an absolute basis by getting a Mercedes?

Comparison-created unhappiness and insecurity is pervasive. Social media is full of images of people showing off their lavish lifestyles giving you something to compare to. No wonder social media users are terminally unhappy.

The flaw of human nature is that whatever we have is enough; until we see someone else who has more.

Comparison in financial markets can lead to remarkably bad decisions. Such is investors have trouble being patient and letting whatever process they have work for them.

For example, if you made 12% on your investments, but only needed 6%, you should be pleased. However, when you find out everyone else made 14%, you feel disappointed. But why? Does it really make any difference?

Here is an ugly truth. Comparison-related unhappiness is for Wall Street’s benefit.

The financial services industry is predicated on making people upset so they will move money around in a frenzy. Money in motion creates fees and commissions. The creation of more and more benchmarks, products, and style boxes is nothing more than the creation of more things to COMPARE with. The end result is investors remain in a perpetual state of outrage.

Goal Based Investing

Changing your view from “relative performance” to an “absolute” investment strategy can greatly increase your long-term results. Such is because the behavioral biases get brought under control, leading to fewer emotionally-driven investment decisions.

The first thing we do with every client is to establish their investing goals. More often than not investors have no idea what their money is supposed to be doing for them. For the most part, they think that if they buy stocks, those investments will ultimately go up and make them wealthy. However, without clear goals, investors tend to take on excessive risk as investment decisions get based on emotions rather than a strategy.

The biggest contributor to long-term problems is the comparison of one’s portfolio to an all-equity index. As we discussed previously, there are many differences between an index and your portfolio.

- The index contains no cash.

- Indices have no life expectancy requirements – but you do.

- An Index does not have to compensate for distributions to meet living requirements.

- To match, much less beat, an index, you must take on an equivalent, or more, risk than the index.

- Indexes have no taxes, costs, or other expenses associated with it.

- An index has the ability to substitute at no penalty, you don’t.

Here is the point.

If you want to be happy, the first thing you need to do is eliminate that which is making you unhappy, which is all of the comparisons.

Graphical Representation

Clients who have learned the wisdom of “enough” are content. Their benchmark is not an artificial one, but one based on their own goals and risk tolerance. They are comfortable that their risk is being managed and understand the game plan for getting from Point A (where they are now) to Point B (retirement, or wherever they want to get to in the future). Most importantly, they invest to obtain their goals with as little risk as possible.

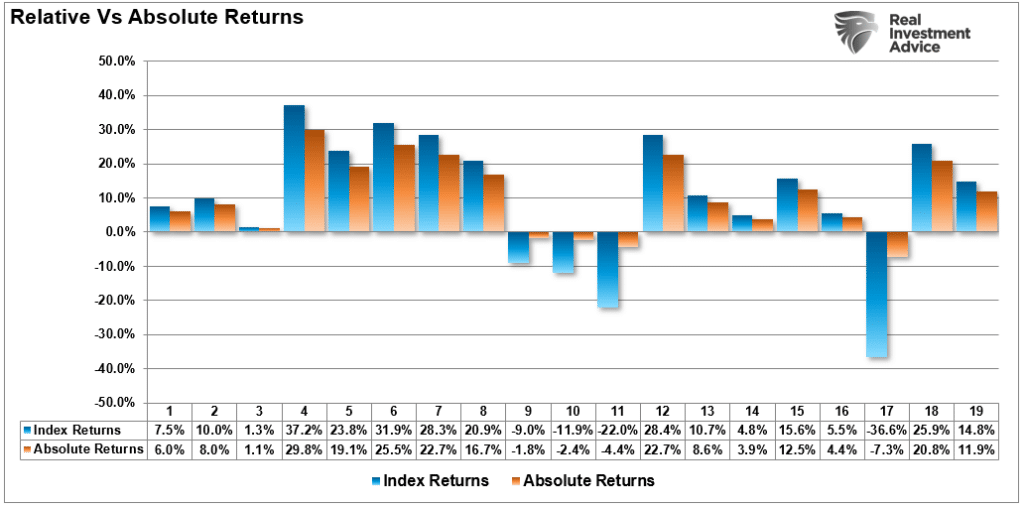

Let’s take a look at an example of what we are talking about. In the chart below we ran a random return model on the S&P 500 for what the next 20 years might look like. As you can see there are quite a few up years and some down years too.

What is important for you to look at here is what the “Absolute Return” matrix looks like. We purposely made sure that in every up year the absolute return matrix underperformed the index, but in down years the absolute return model outperformed by not losing as much as the index. Were there down years in an absolute return portfolio – you bet!

Slightly Better Than Average – Wins

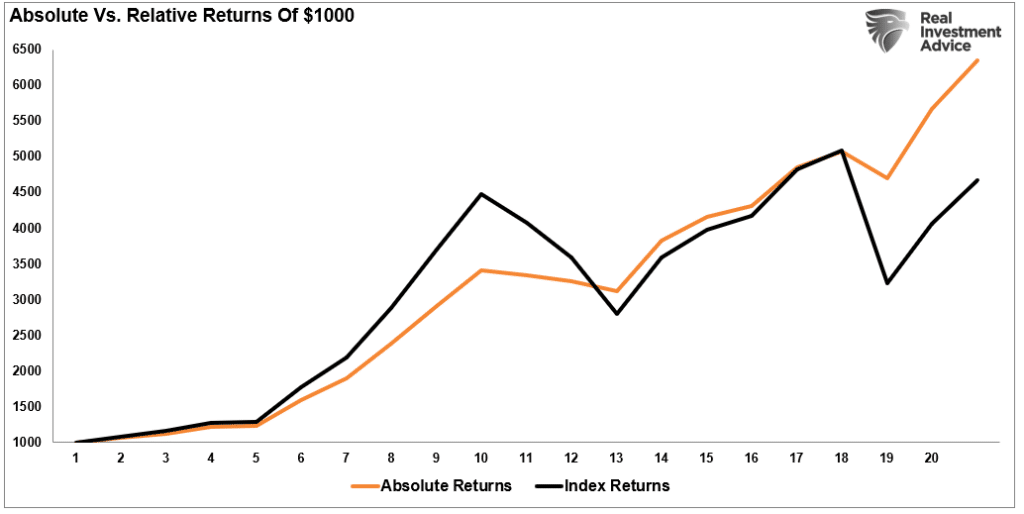

Let’s look at the return matrix chart above and assume that we invested $1000 into the Random Index Return Matrix and $1000 into the Absolute Return Matrix.

Most of you would be told after the first year that you need to move your money to another manager because he underperformed the index. (We see this annually from commentary on manager performance) Same in year two. However, in year three you are feeling pretty good but in every up year you lag – so you chase another fund that beat the pants of the index that year.

The problem with Relative performance is that while you are happy in up years because you are beating some index, however, when that index went down 20%, and you were down 19%, WallStreet says you should be happy because you still beat the index. I haven’t personally met anyone who was happy with that, were you?

The 7th Deadly Sin

The lesson we want to drive home here is the danger of following Wall Street’s advice of beating some arbitrary index from one year to the next. What most investors are taught to do is to measure portfolio performance over a twelve-month period. However, that is absolutely the worst thing you can do. It is the same as being on a diet and weighing yourself every day.

If you could look see the whole future laid out in front of you, as in the chart above, it is very easy to make an investment decision knowing your eventual outcome. However, we don’t have that luxury. Instead, Wall Street suggests that if your fund manager lags in one year, then you should move your money somewhere else. This forces you to chase performance and creates fees and commissions for Wall Street.

We chase performance because we all suffer from the 7th deadly sin – Greed.

Most of us want all of the rewards without regard for the consequences. However, instead, we should learn to “love what is enough.”

Absolute return investing can beat average market returns with less risk and volatility over time. Why? By not losing your principal investment in down years it is possible to actually utilize the power of compounding returns. The problem with market benchmarking, and what financial advisors won’t tell you, is that when there are back-to-back losing years, you compound losses.

Conclusion

If you want to win at the long term investing game Financial Resource Corporation sums it up best;

“For those who are not satisfied with simply beating the average over any given period, consider this: if an investor can consistently achieve slightly better than average returns each year over a 10-15 year period, then cumulatively over the full period they are likely to do better than roughly 80% or more of their peers. They may never have discovered a fund that ranked #1 over a subsequent one or three-year period. That ‘failure,’ however, is more than offset by their having avoided options that dramatically underperformed. Avoiding short-term under-performance is the key to long-term out-performance.

For those that are looking to find a new method of discerning the top ten funds for 2002, this study will prove frustrating. There are no magic short-cut solutions, and we urge our readers to abandon the illusive and ultimately counterproductive search for them. For those who are willing to restrain their short-term passions, embrace the virtue of being only slightly better than average, and wait for the benefits of this approach to compound into something much better…”

If you want to be a better investor do what most investors don’t:

- Look for stable returns – not the highest returns

- Invest for a reasonable annual return that will help you reach your investment goal.

- Don’t compare yourself to some anomalous index.

- Save, Save, Save!

- Manage your money – after all – it is your money.

It’s not as hard as you think.

The post Absolute Returns Or Relative – There Is A Difference appeared first on RIA.

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.