In this 01-21-22 issue of “Retail Investors Panic As Market Plunges.”

- Retail Investors Panic

- The “Value Trade” Isn’t Really A Value

- Portfolio Positioning

- Sector & Market Analysis

Retail Investors Panic As Market Plunges

Last week, we noted:

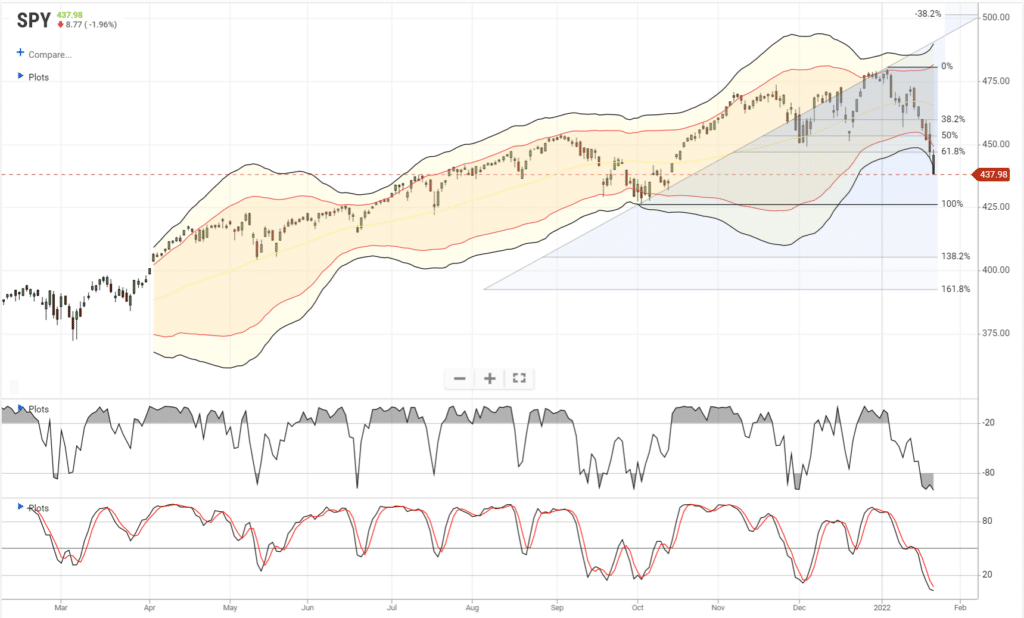

Notably, despite the market’s failure to hold previous gains, it successfully retested and held the lower trend line. However, sell signals remain in place and have not yet reached more oversold levels. The concern remains the Fed’s more aggressive stance to battling the inflation surge, which hit 7% annualized this past month.

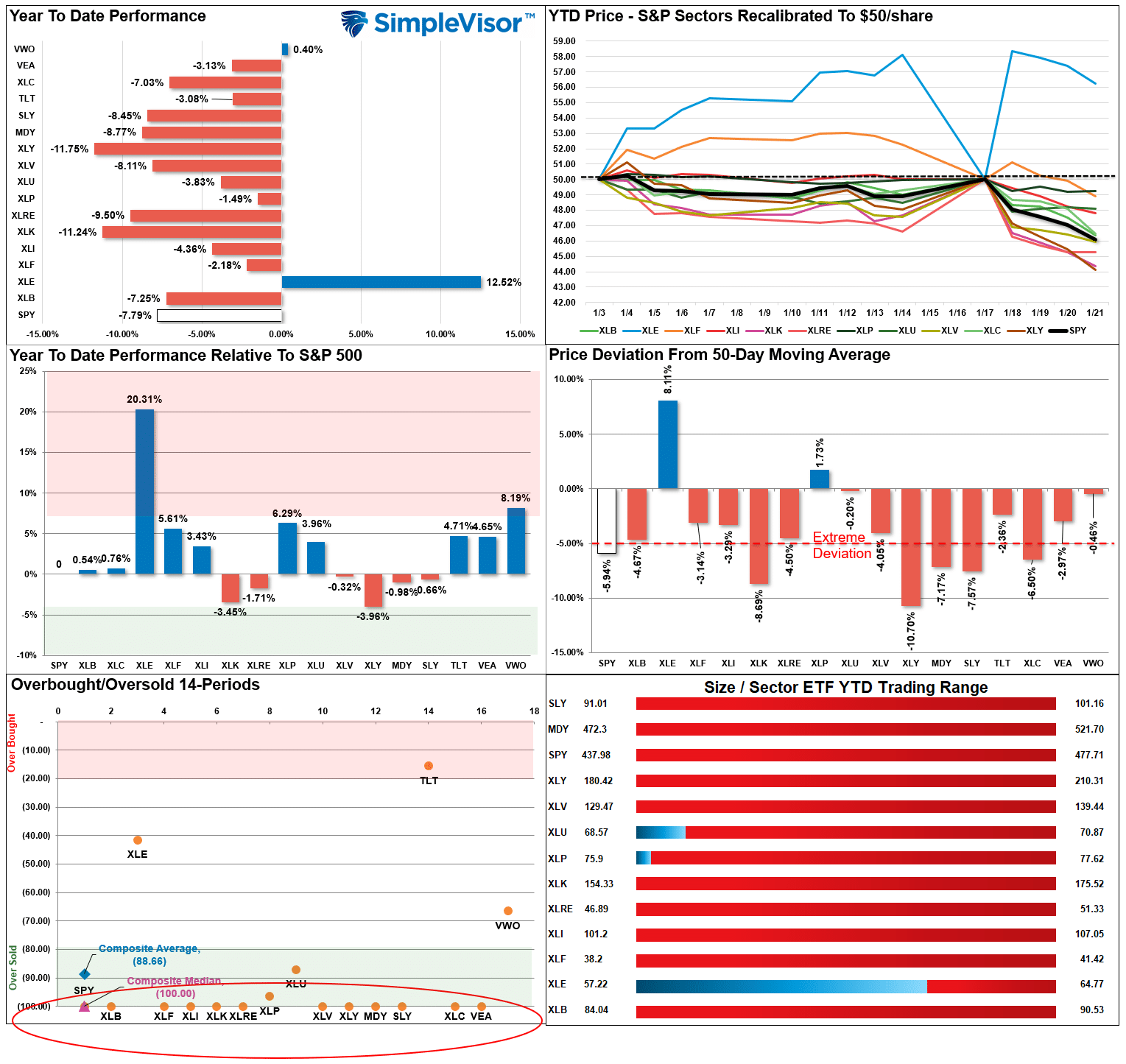

This past week, retail investors began to panic sell as “meme” stocks fell apart. Previous favorites became an anathema from AMC to Gamestop to Pelton and Netflix. The selling pressure took the S&P 500 below its trendline support, deep into oversold territory, and well into 3-standard deviations below the mean.

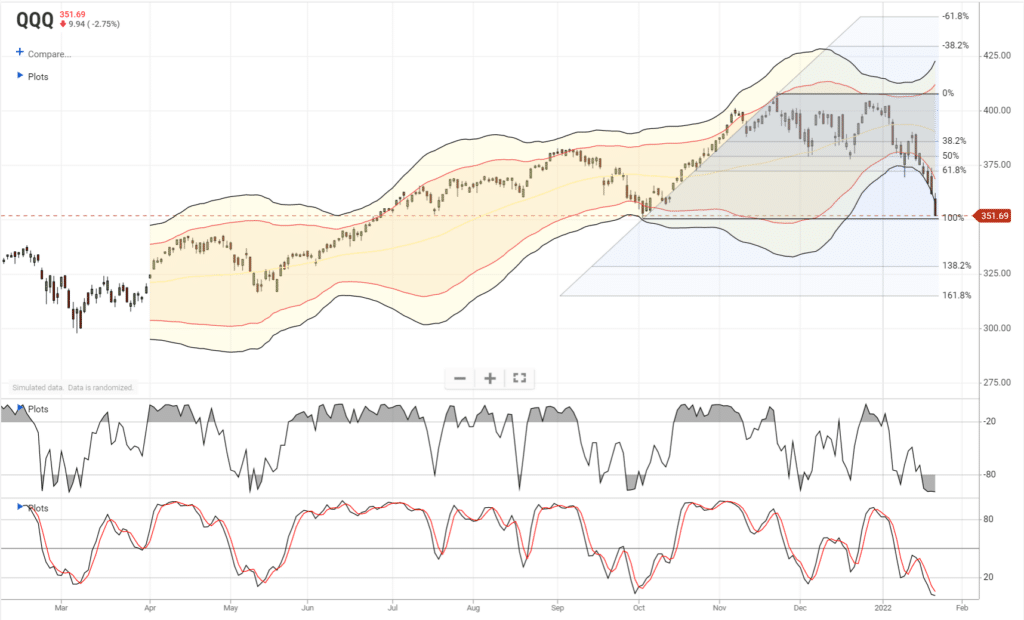

The selling pressure was worse in the Nasdaq taking that index to extreme oversold and 4-standard deviations below its 50-dma. Such is the worst start for the Nasdaq since 2008 and is at support from October lows.

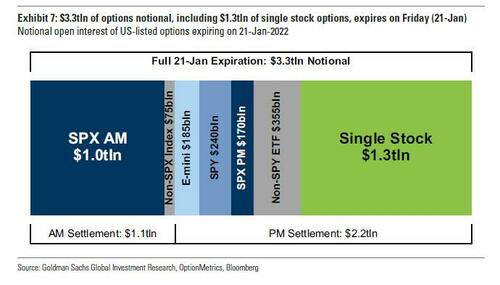

Friday was problematic for stocks due to the $3.3 Trillion simultaneous expiration of index and stock options.

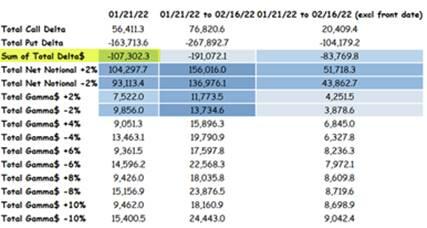

The “good news,” if you want to call it that, and as noted by Zerohedge, is there is now a good bit of “combustible fuel” to create a counter-trend rally heading into the Fed meeting next week.

“The extreme negative / short Delta” across all option expiries is at risk of becoming a combustible fuel for a mechanical squeeze if spot rallies. There is over -$107B of front-week Delta alone.“

All this means is that investors are now all on “one side of the boat,” which is a prime setup for a counter-trend bounce.

However, it is likely a bounce you will want to use to “derisk” your portfolio.

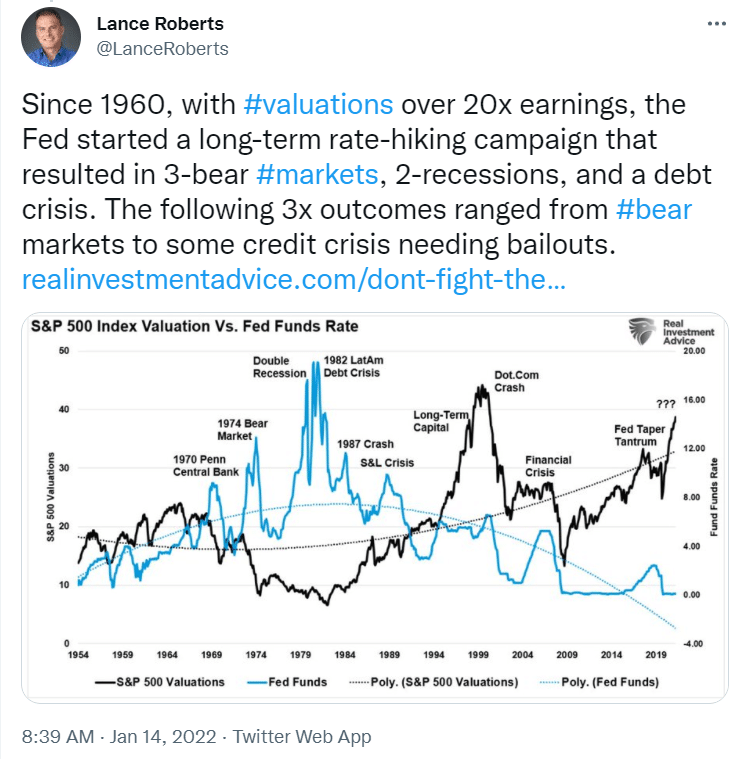

The Big Risk Next Week

Next week is the January meeting of the FOMC. The results of that meeting will set the market’s tone for the next few months. With the markets already in correction mode, the big question is whether or not the Fed will press ahead with monetary tightening.

On Friday, I took a poll asking whether the Fed will forge ahead with tighter policy (hawkish) or try and soften its stance to maintain financial stability (doveish).

As discussed previously, the Fed’s most considerable risk remains the “stability” of the financial markets. While the Fed is concerned about “inflation” and its impact on the economy, financial instability is a greater risk. Just as in 2008, a cratering financial market undermines economic growth and exacerbates the risk of a financial crisis from a highly leveraged economy.

We suspect the Fed will ultimately opt for financial stability. However, the Fed has a long history of making the wrong choice first before coming to the rescue.

The Big Crash

The crucial point is that we have “no idea” what the Fed will do. What we do know, as stated, is the Fed usually makes a mistake. Such was the crux of comments by Jeremy Grantham:

“All 2-sigma equity bubbles in developed countries have broken back to trend. But before they did, a handful went on to become superbubbles of 3-sigma or greater: in the U.S. in 1929 and 2000 and in Japan in 1989. There were also superbubbles in housing in the U.S. in 2006 and Japan in 1989. All five of these superbubbles corrected all the way back to trend with much greater and longer pain than average.

Today in the U.S. we are in the fourth superbubble of the last hundred years.”

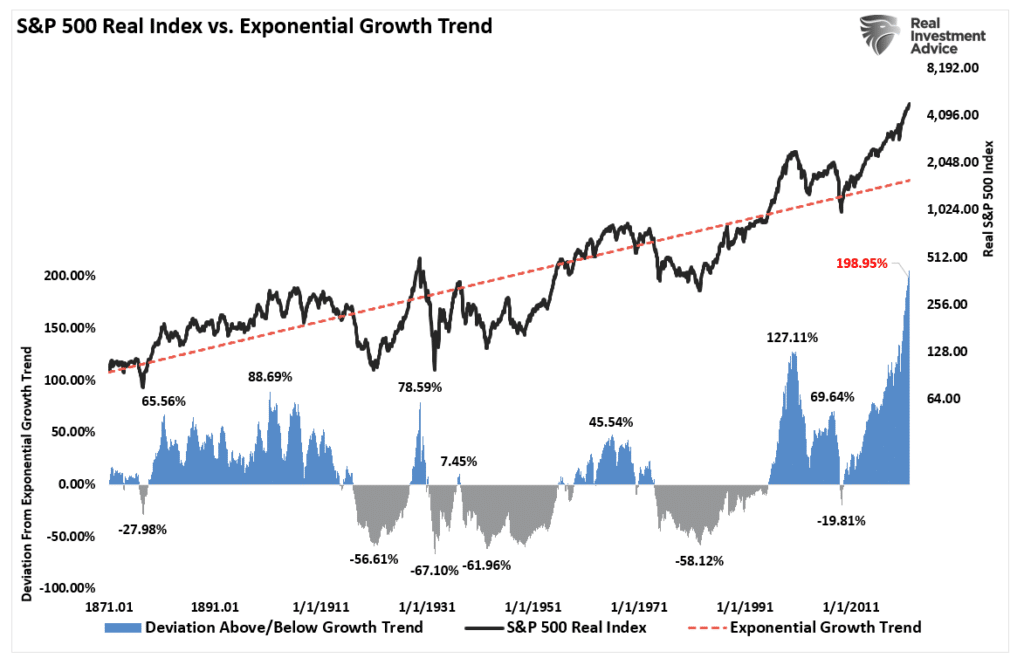

The bubble is easy to spot in the chart below of deviations of the market from its long-term exponential growth trend.

As Grantham correctly notes, investors don’t want to admit that a correction of magnitude is possible. However, the possibility of a 40-50% contraction to revert the massive extension from the long-term growth trend is highly probable. All that is needed is the right catalyst, which so far has yet to appear.

The problem is that crashes start slowly and then all at once. Only in hindsight does the catalyst become obvious.

Therefore, we continue to suggest using any rally heading into the Fed meeting to reduce risk exposure. If the Fed turns dovish and the bull market continues, it’s easy to add exposure. If they don’t, lower levels of risk will shield you from a further decline.

Risk management isn’t about being right. It’s about protecting capital when you’re wrong.

Retail Investors Pile Into Value

Since early December, we have discussed the “value trade” would likely make a resurgence in 2022. That trade came in strong during January. Energy surged sharply on the back of higher oil prices, and retail investors poured into ETFs.

“Retail investors have been plowing a great deal of money into the markets in recent days. But remarkably, in addition to the broad index ETFs, they’ve been buying value sector ETFs (according to JP Morgan Research). So this rotation is not limited to institutions.” – The Daily Shot

Professionals also have plowed into those areas as well.

There are two things to note about the “value” trade.

- It tends to be a “late cycle” trade, followed by economic weakness (2012), market corrections (2018), and outright bear markets (2008),

- By the time “retail investors” pile into the trade, it is generally too late.

However, the most crucial factor is the companies retail investors are piling into are not really “value.”

Value Isn’t Really A Value

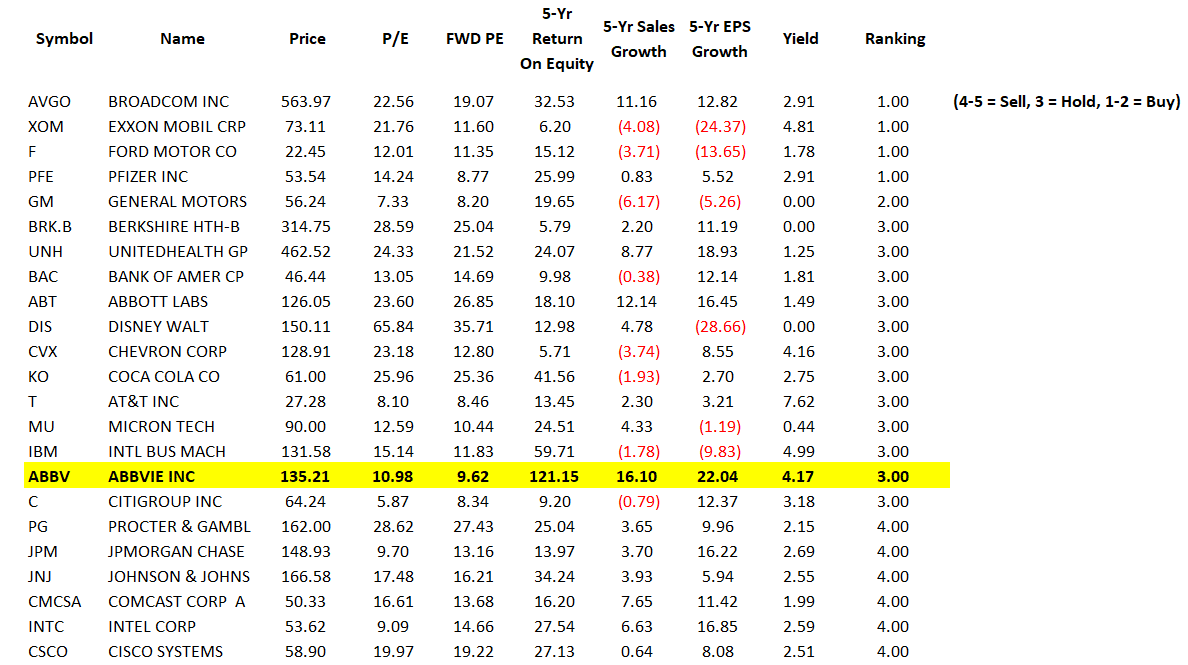

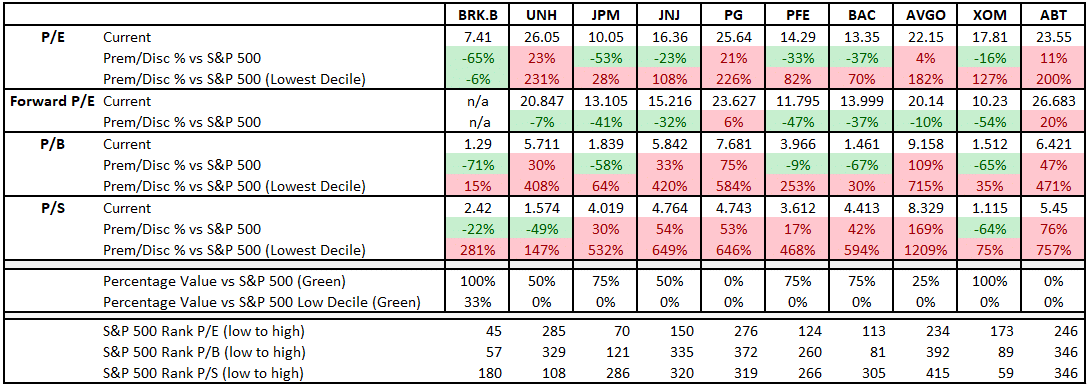

However, the value trade isn’t really what it seems. For most investors, the idea of value investing is the purchase of “fundamentally undervalued” companies. Unfortunately, such isn’t the case as investors buy ETFs of stocks only traditionally “classified” as value. As shown in the table below, which is a compilation of the top-10 holdings of the 3-largest value ETFs, only one company truly qualifies as a fundamentally cheap stock.

Another view of the same comes from Michael Lebowitz on the top-10 holdings of the Vanguard Admiral Fund.

While companies like AT&T are indeed “cheap” on a P/E basis, return on equity (ROE), sales, and EPS growth, are all very low. Conversely, the more familiar names in the “value” sector like Proctor & Gamble, Berkshire Hathaway, Coca-Cola, and Disney, while great companies are wildly overvalued. As a result, Abbvie stands out as an apparent “value” leader in the group.

The issue is that the “value” trade is getting driven by a flood of money by retail investors into passive ETFs. As we explained previously, when money pours into ETFs, the underlying companies get bought, increasing share prices. Therefore, given the overlap of the most significant holdings of value-based ETFs, the overvaluation of many of the companies is not surprising.

The problem, of course, is that while ETF “buying” pushes these stocks higher, the “selling” of ETFs will drive them lower. If the Fed is on the verge of a policy mistake, the eventual market correction will drive “value” stocks lower as the ETFs are dumped indiscriminately by panicking investors.

Energy Is Overdone

Such is also the case for energy stocks, which also fall into the “value” category.

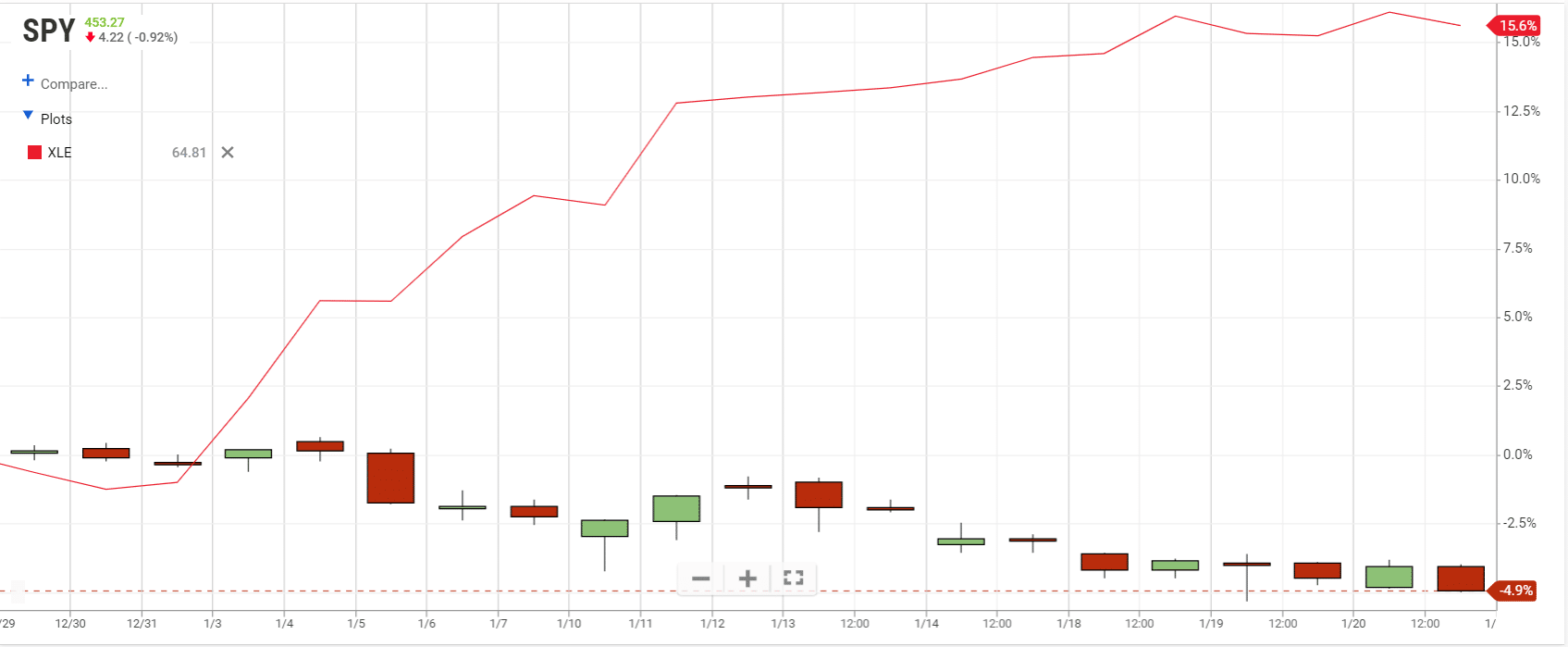

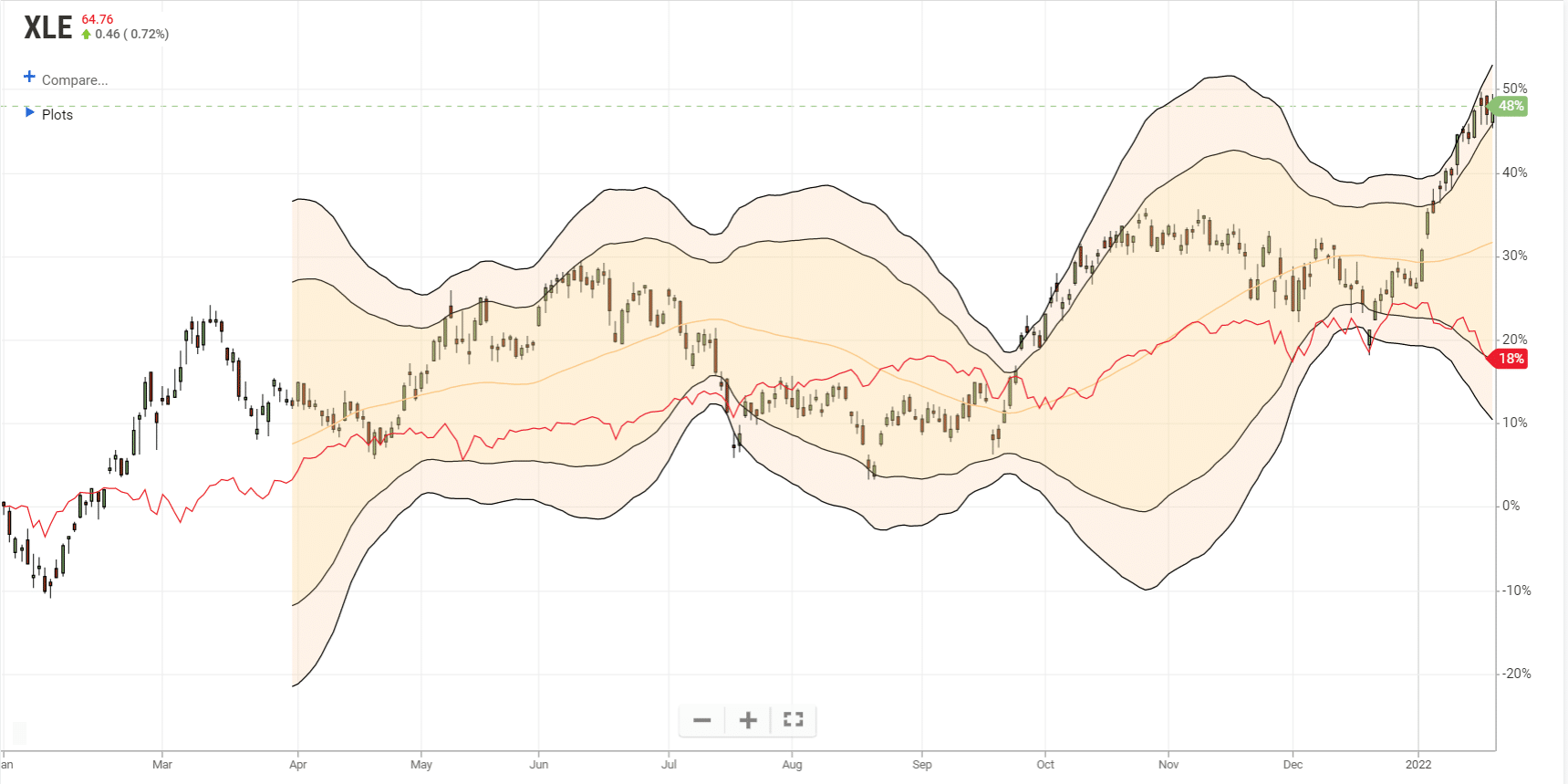

As noted above, energy stocks, which fall into the “value” category, have surged over the last month. Energy stocks are up 15% during that period, while the S&P 500 index is down nearly 5%. That is quite a performance gap.

However, that outperformance should also serve as a warning sign for investors. Over the past year, when energy stocks reached more extreme deviations from their 50-dma, it consistently reversed to the mean. Given the magnitude of the current deviation from the mean, a correction in energy would not be a surprise.

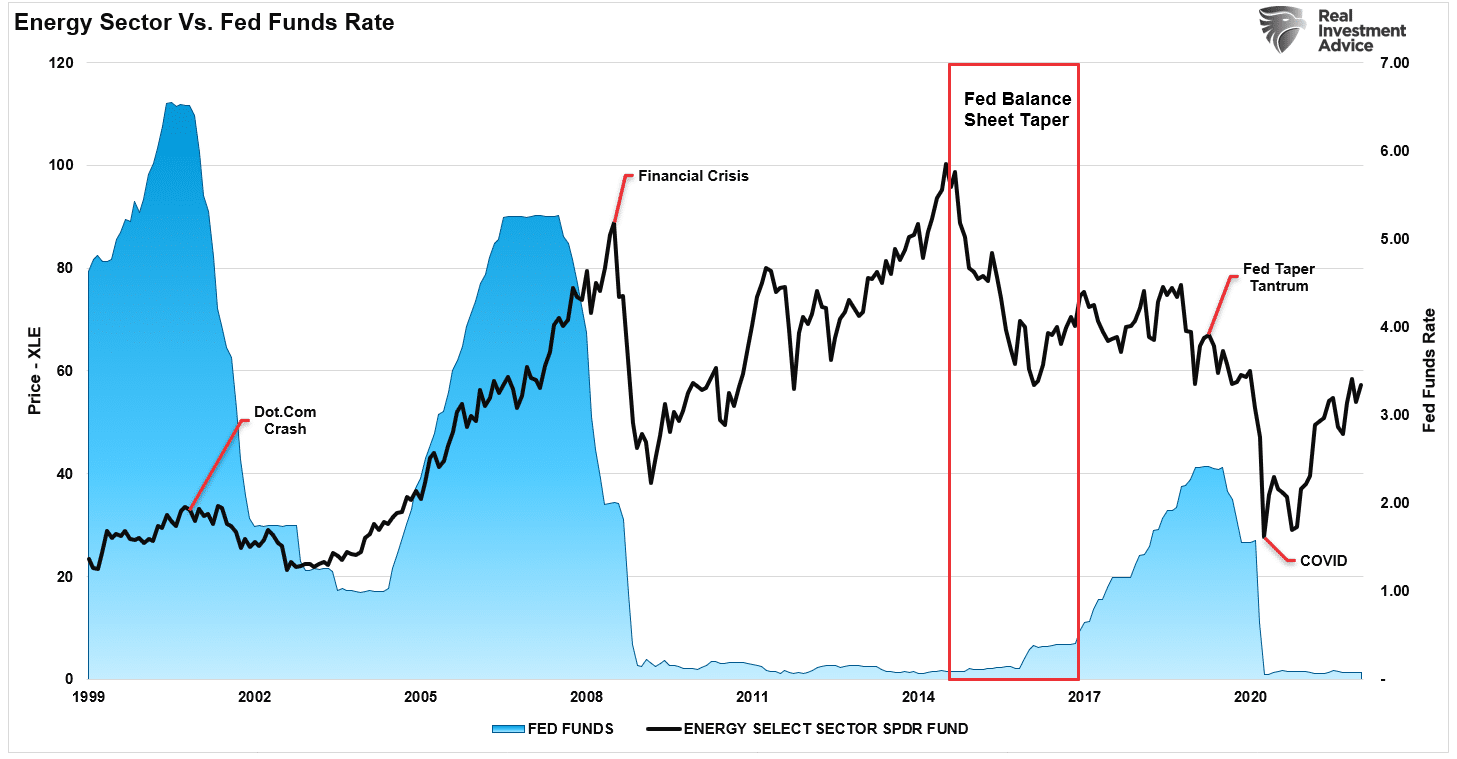

Of course, slowing economic growth and deflationary pressures will bring about a correction in oil prices. One of the things that could generate that environment, sooner than later, is the Federal Reserve tightening its monetary policy. Such was a point I discussed this week in a3-Minutes On Marketsvideo.

Notably, here is the primary chart I discussed. Historically, when the Fed has hiked rates or tapered its balance sheet, oil prices have come under pressure due to slower economic growth and deflationary pressures.

While the recent rally in energy stocks has been quite strong, the Fed is about to aggressively tighten monetary policy with the sole goal of combating inflation. In other words, to bring down inflation, they will slow economic growth, which reduces demand for commodity-based products.

Unfortunately, I suspect it won’t be just oil prices and energy stocks that get brought down in the process.

Such is why we continue to reduce our exposure to equities.

Portfolio Update

As noted last week, we previously sold our S&P index trading position and increased bond holdings to lengthen the duration. This week we continued reducing equity exposure by trimming technology and energy holdings. As a result, our current allocation to risk continues to decline. However, we are looking for a short-term rally to reduce risk further.

The market is starting to show valid concerns of rate hikes and monetary tightening into an already weakening economic environment. The extreme overbought, overvalued condition provides the fuel for a more significant selloff.

As we laid out just recently, many of the headwinds that supported the ramp in speculative behaviors have, and are, reversing. To wit:

- Tighter monetary policy, and high valuations.

- Less liquidity globally as Central Banks slow accommodation.

- Less liquidity in the economy the previous monetary injections fade.

- Higher inflation reduces consumption

- Weaker economic growth

- Weak consumer confidence due to inflation

- Flattening yield curve

- Weaker earnings growth

- Profit margin compression

- Weaker year-over-year comparisons of most economic data.

As noted above, the event that changes the “bullish psychology” is always unknown. However, the eventual market reversion is almost always a function of changes in liquidity and a contraction in earnings. Such was a point I made recently on Twitter:

When the “bull is running,” we believe we are more intelligent than we are. As a result, we take on substantially more risk than we realize as we continue to chase market returns allowing “greed” to displace logic. Like gambling, success breeds overconfidence as the rising tide disguises our investment mistakes.

Unfortunately, our errors always return to haunt us. Always too painfully and tragically as the loss of capital exceeds our capability to “hold on for the long-term.”

We will likely relearn many lessons this year.

Market & Sector Analysis

S&P 500 Tear Sheet

Relative Performance Analysis

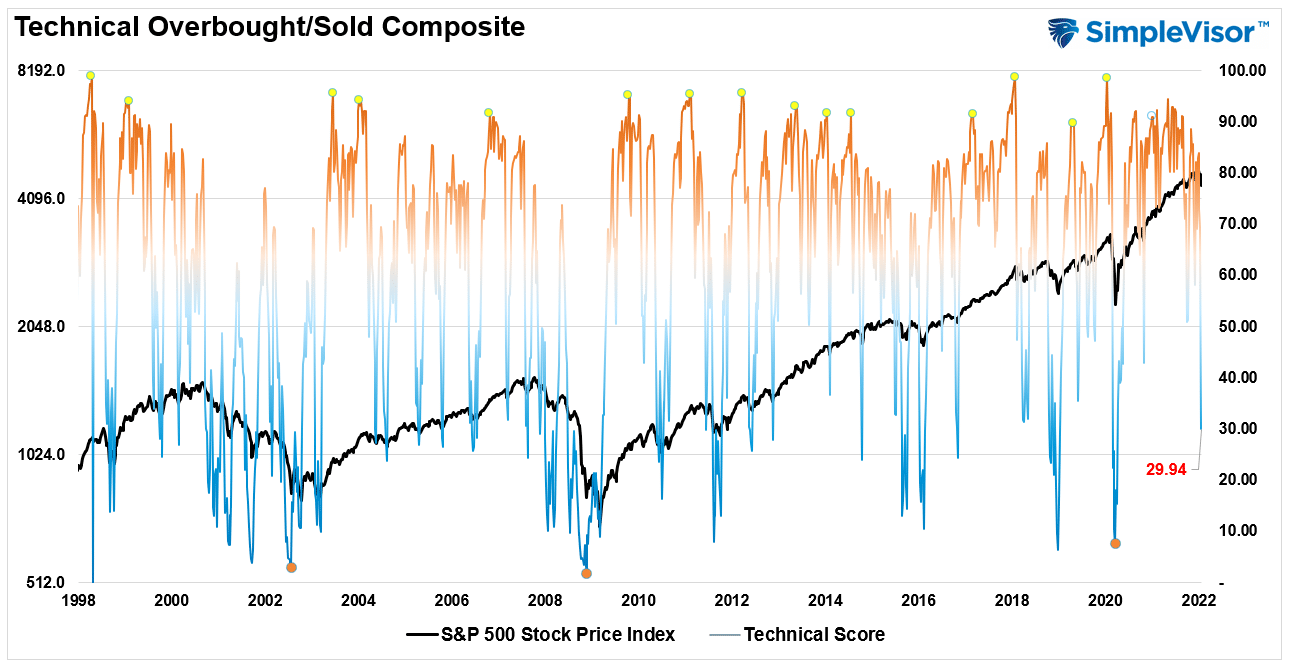

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 29.94 out of a possible 100.

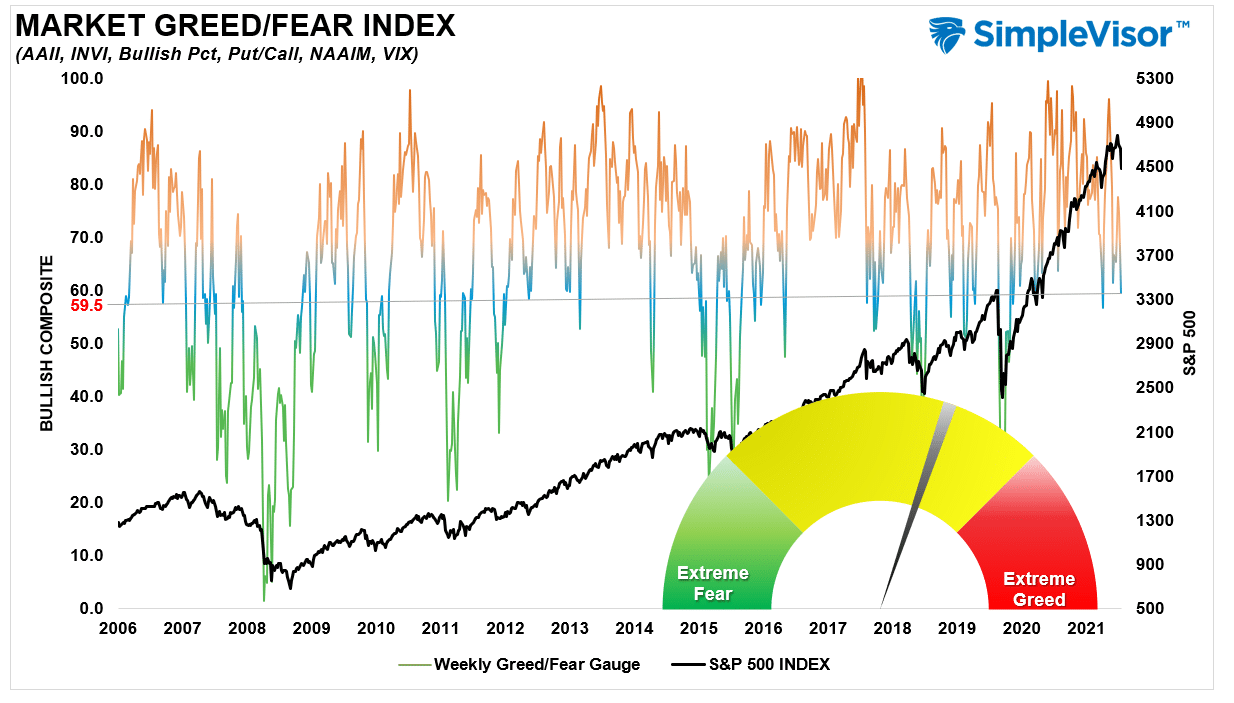

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 59.45 out of a possible 100.

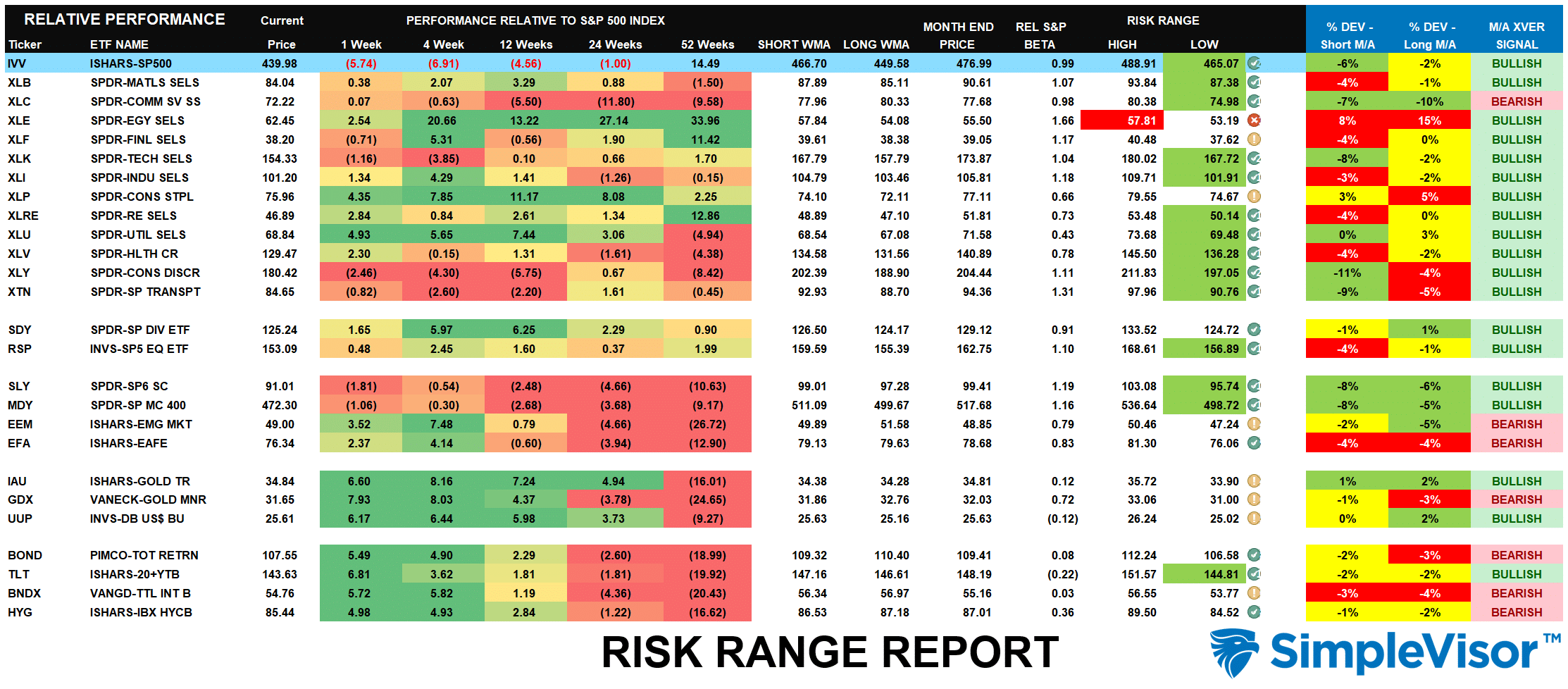

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

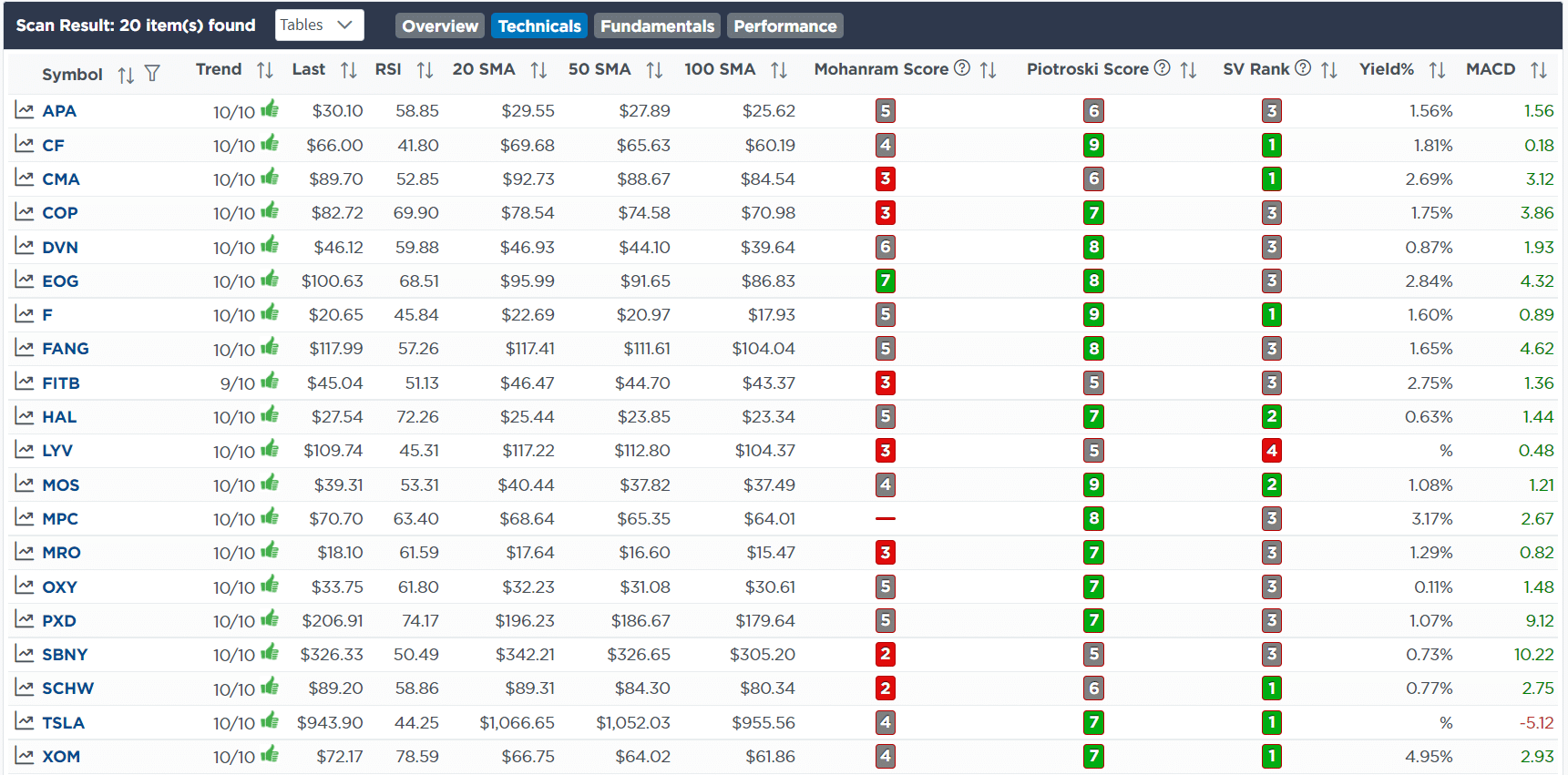

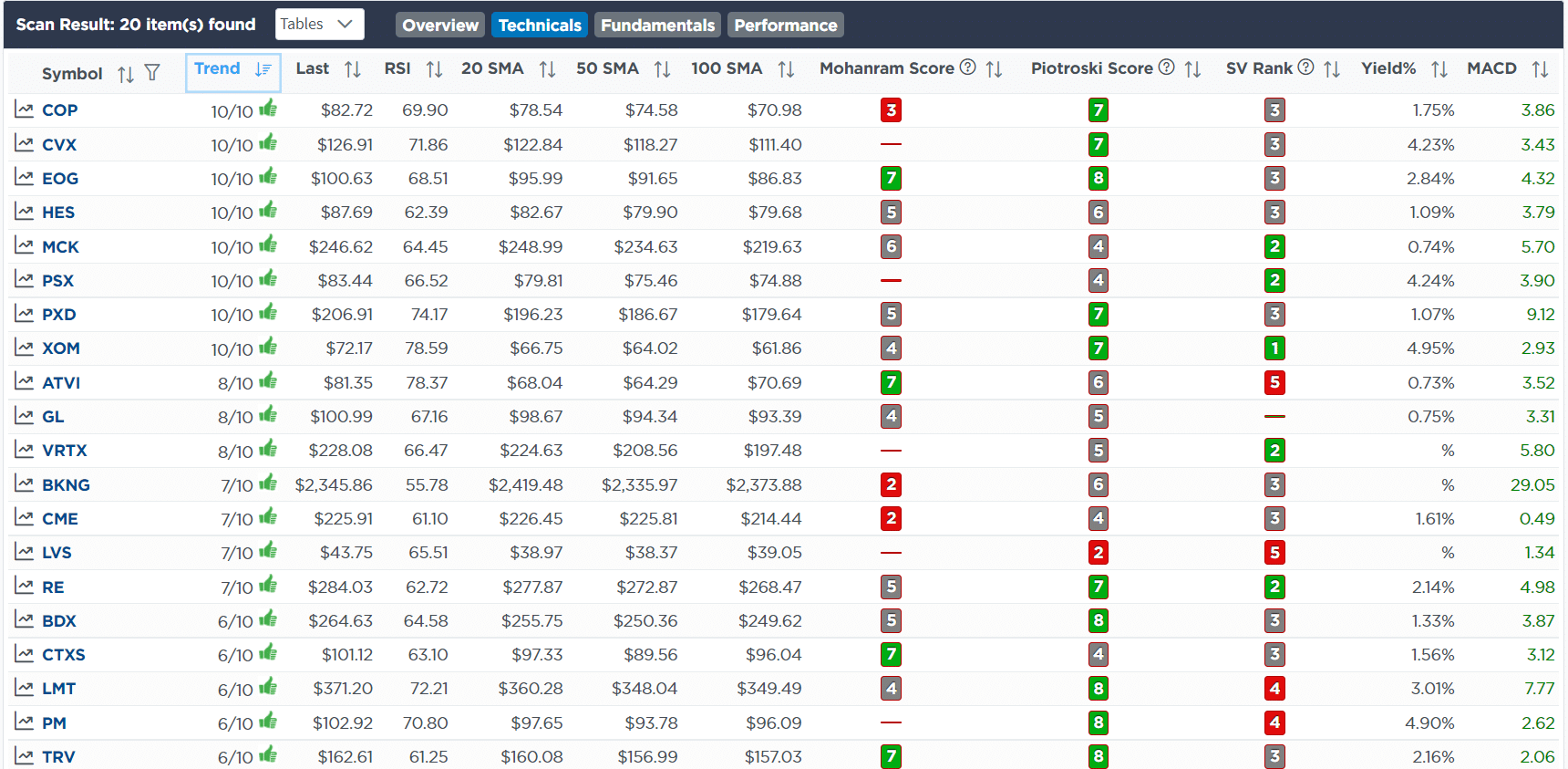

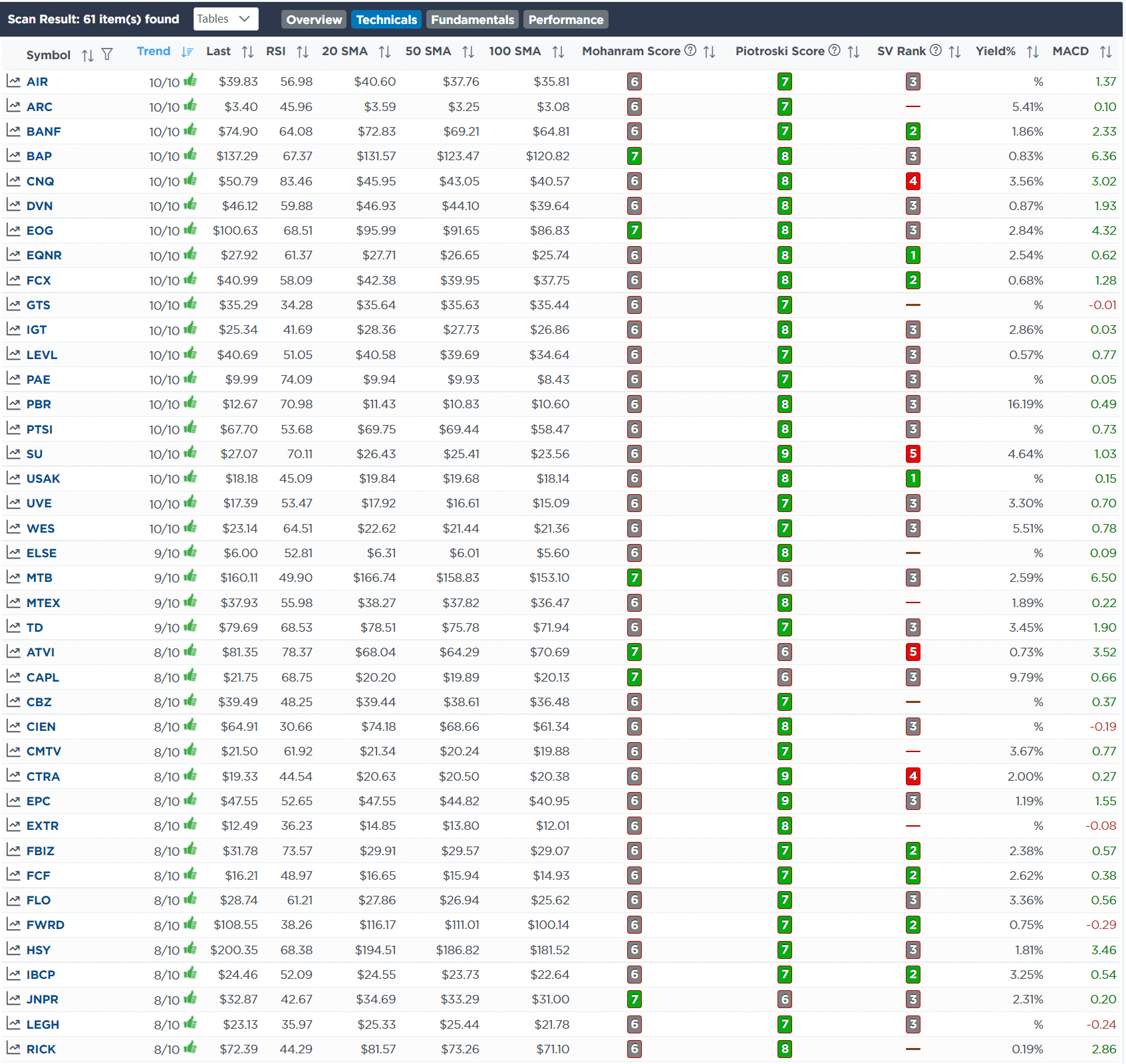

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

This week, there was a lot of action, so I have broken it down by date for easier reading.

Tuesday, 18th

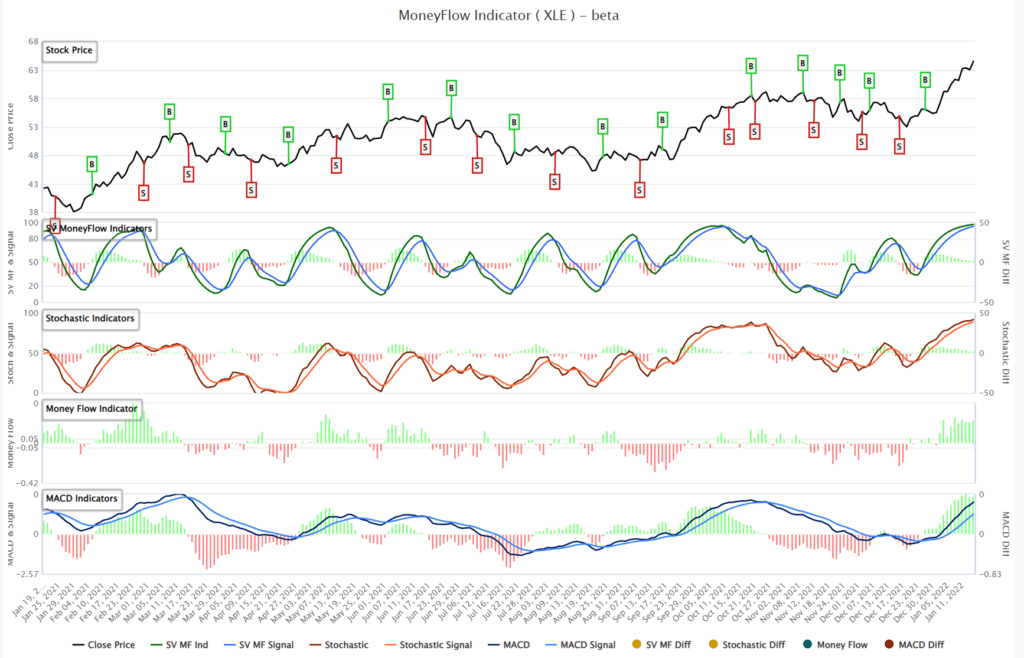

“This morning we trimmed exposure in energy and Ford (F) due to their more extreme overbought conditions. As shown in our MoneyFlow indicator (Under the Research tab) XLE is extremely stretched and will likely turn lower in the next few days. At the same time many of the technology names are in the exact opposite position, so be careful making wholesale portfolio changes.” – 1-18-22

Equity Model

- Reduce XOM and MRO back to model weights of 2% of the portfolio each

- Reduce F back to 3.5% of the portfolio.

ETF Model

- Reduce XLE back to model weight of 3.5% of the portfolio.

Thursday, 20th

We have been waiting for a rally in the market to reduce equity exposure a bit further. Today’s rally was expected but remains very weak and may not stick. However, if we get some follow-through tomorrow and next week heading into the Fed meeting we will likely reduce equity exposure further.” – 1-20-22

Equity Model

ETF Model

- Sell 2% of SPDR Technology ETF (XLK)

Friday, 21st

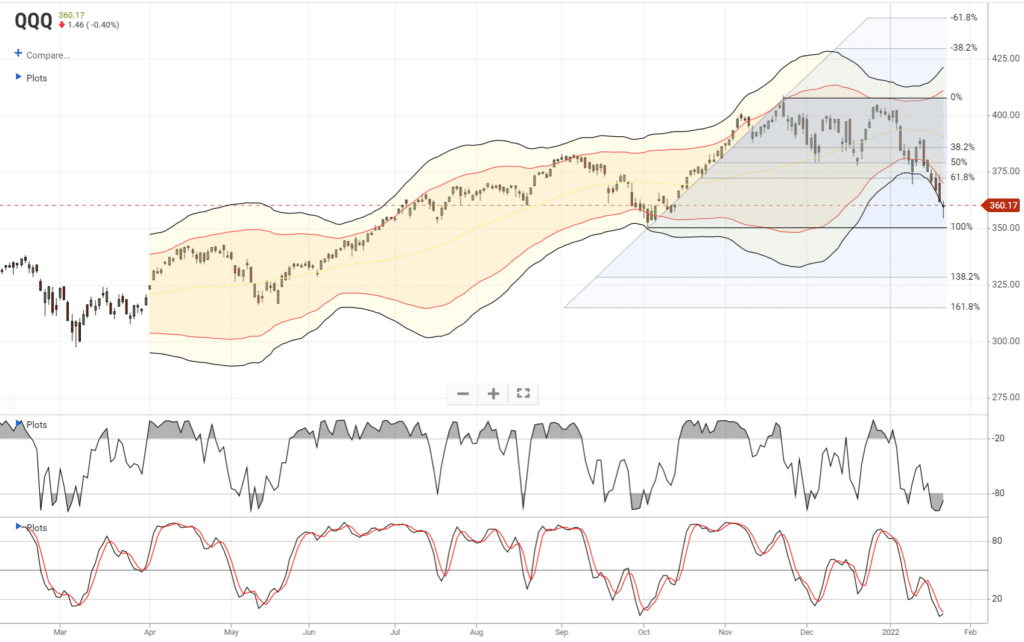

“After a rash of selling over the last two weeks, the Nasdaq is extremely oversold and 3-standard deviations below its 50-dma. Such extreme oversold conditions can’t, and don’t, last for long. With AAII sentiment now extremely bearish, investor positioning negative, and technicals stretched, we think there is a decent setup for a tradeable bounce into next week.“

This morning we are adding a 5% position in QQQ for a bounce to the previous trend line. We are carrying a 2% loss as our stop level.

Also, we have been stopped out of three other positions in our portfolio: ASAN, NFLX, and ADBE. However, given the extreme oversold condition on those positions we are looking for a rally to sell those positions into. Also, on that rally, we will reduce GOOG and AMZN as well.

Overall we are looking to reduce portfolio exposure to 50% of the portfolio during the next rally.” – 01-21-22

- Buy 5% of the Portfolio in QQQ

Lance Roberts, CIO

Have a great week!

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.