Market Review & Update

Between Paypal, Facebook, and Netflix, the volatility swings in the market over the last couple of weeks were nothing short of nauseating.

As we discussed last week:

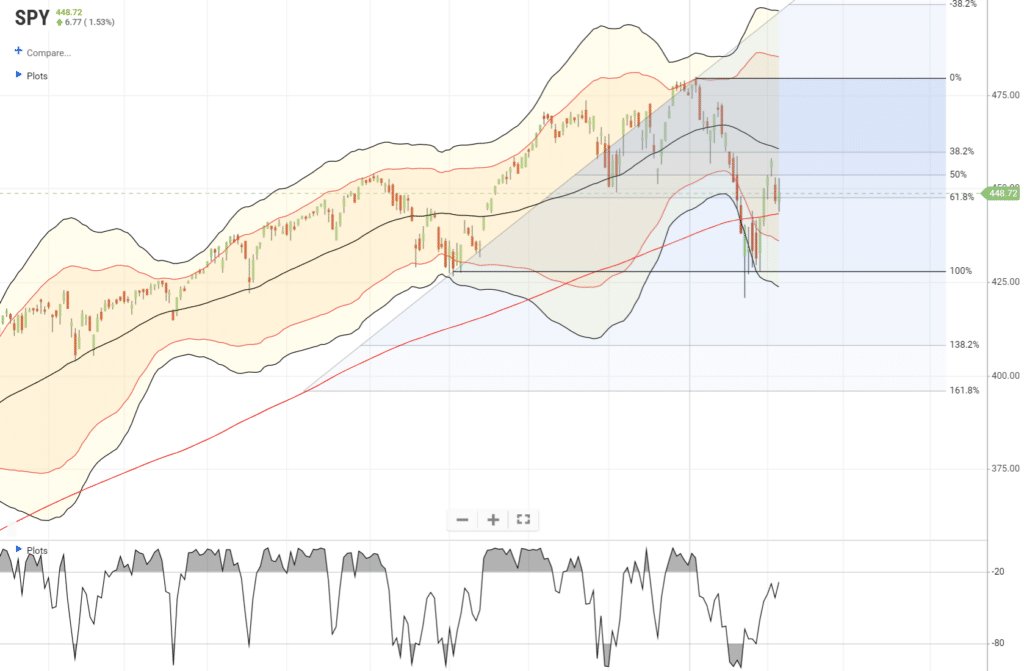

“The markets do look to be stabilizing, as shown below, and are holding the October lows. That 100% Fibonacci retracement, and multiple rally attempts, triggered a short-term buy signal. All of this is short-term bullish.“

However, here was the most crucial commentary.

“This analysis continues to suggest any rally that occurs will likely:

- Fail at a lower high / resistance level; and,

- The subsequent decline will potentially retest or break recent lows.

We base that assumption on things remaining “status quo” with the Fed’s current stance on tightening monetary policy. However, if the Fed softens its stance or reverses course entirely, this analysis will change.

With the market rally, the previously oversold indicators are reversing, and buy signals are heading higher. We are now in “no man’s land.” In other words, with earnings season still in play, we could see the markets push higher. We could also see a retest of recent lows. The problem with making any “major allocation” call is dangerous of being on the wrong side of the trade.

We are worried enough about the current weakness in the market that we continued to reduce equity exposure this week and added to our short S&P 500 index hedge. If the market continues to push higher, we will continue that process for now. Until, and unless, the Fed reverses its stance on monetary tightening.

The risk does remain to the downside, as we will discuss momentarily, but timing is always the challenge.

Is The Bull Market Over?

There is much debate in the financial media questioning the 12-year old bull market? Is this just a correction in an ongoing bull trend? Or, is this the beginning of a “real” bear market?

Unfortunately, we won’t know the answer until after the fact. However, we can take note of the current market environment and make some reasonable assumptions about the risk we are taking in portfolios.

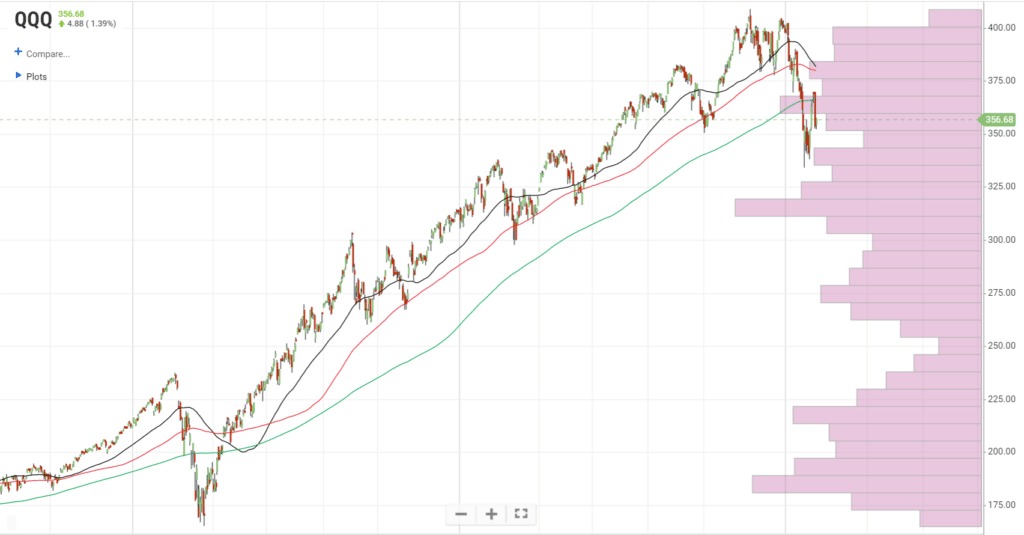

Let’s look at the Nasdaq Index (QQQ), for example. For the first time since March 2020, the index is trading below the 50, 100, and 200-day moving averages. With those previous support levels broken, there could be a “trend change” at work in the markets.

The “price trend” is what denotes a “bull” or “bear” market. Since March 2020, the markets traded primarily above their moving averages, suggesting a bull market was intact. However, with markets now trading below those averages, the market’s tone is changing.

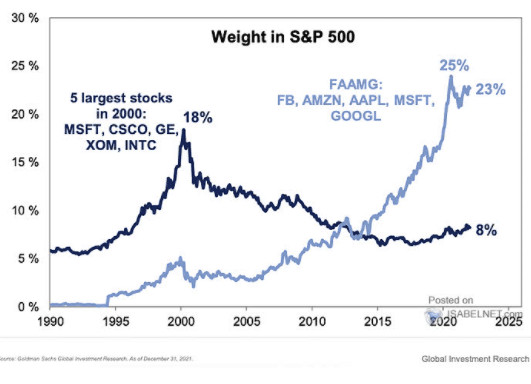

I am focusing on the Nasdaq, given the extreme weighting of just a handful of companies in the index. The recent cracking of Facebook and Netflix following earnings reports is just a taste of what happens if the support of those “Generals” gets lost.

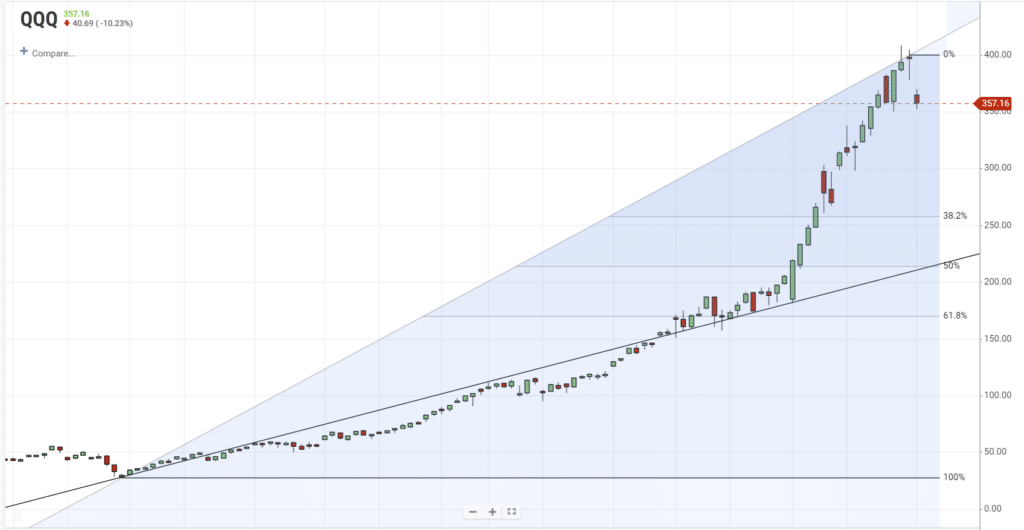

If the “growth” period of the market is over, then the Nasdaq has a substantial way to fall to complete a 50% correction from the 2009 lows. However, that correction would only return the Nasdaq to its previous bullish trend line. A 61.8% retracement would make it a “bear market” by breaking the bullish trend.

Such goes to show you just how exacerbated markets have become due to a decade of monetary interventions.

Could such a correction happen? Absolutely.

Will it happen? Who knows.

However, the Fed has a long history of breaking “bull markets.”

One And Done? Is The Fed Trapped At Zero?

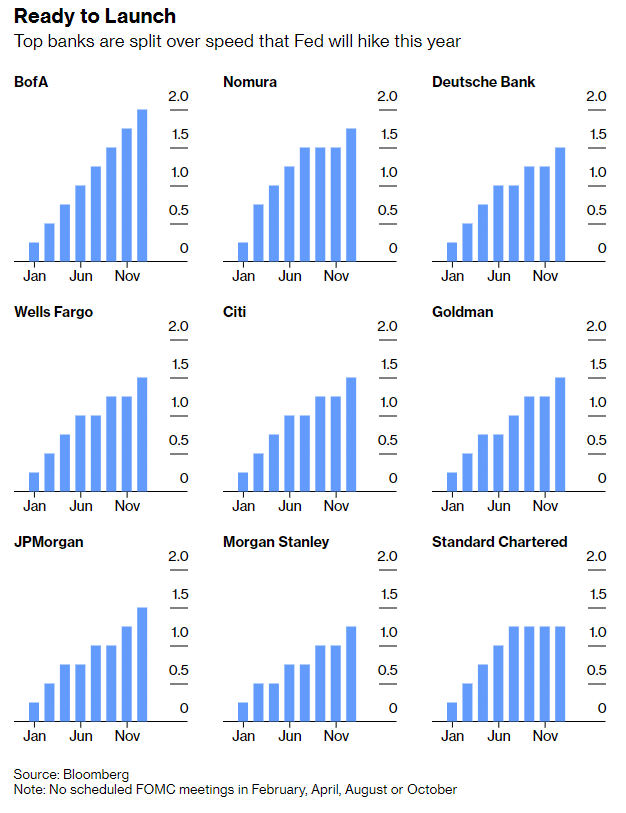

Bloomberg penned an interesting article this past week.

“Wall Street’s biggest banks are at odds over how fast and far the Federal Reserve will raise interest rates after Chair Jerome Powell signaled it could be more aggressive than previously anticipated in tackling the strongest inflation in four decades.

With Powell declining to give specific guidance on what the Fed may do beyond indicating it will hike rates in March, economists and investors are making different judgments about the future. Such could risk a rough ride ahead for markets.”

The chart below presents the various projections by those surveyed.

BofA is the most aggressive suggesting the Fed will hike rates by 200bps (2%) by the end of the year. The majority of the banks targeted a 150bps increase to 1.5%, with two banks coming in at 125bps (1.25%).

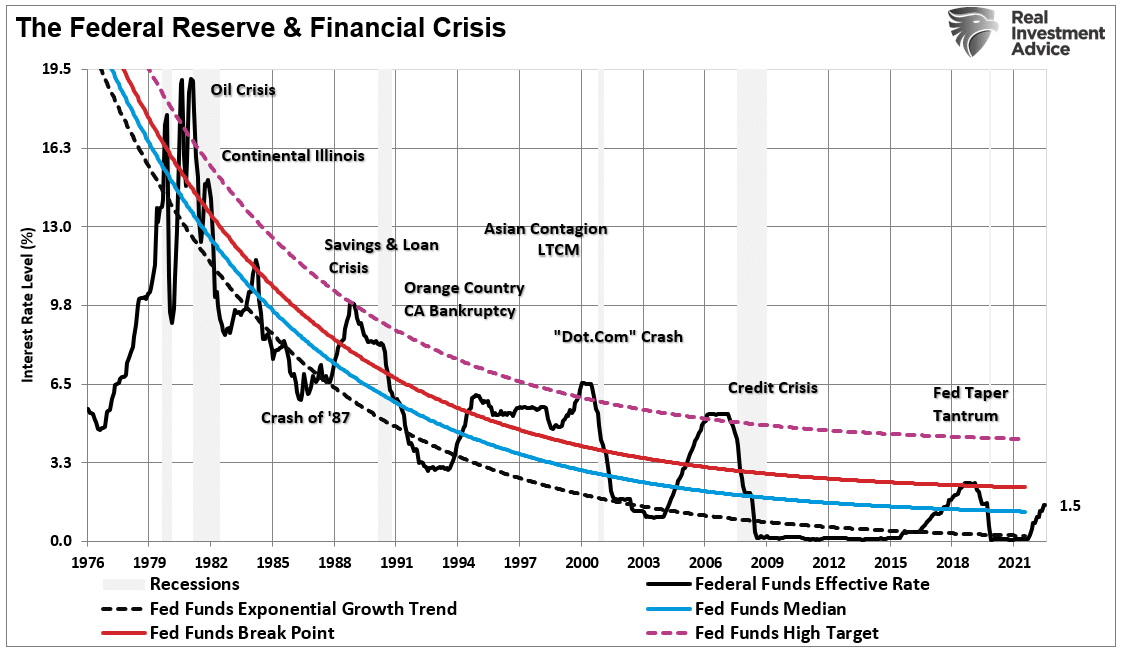

Given the majority are estimating an increase of 1.5% in the overnight lending rate, where does that put the Fed rate to previous rate hikes? Using the Fed Funds rate chart fromthis past week’s newsletter,an increase of 1.5% would be higher than the long-term growth trend median.

While the Fed funds rate has historically gone above the median, an increase of 1.25% would approach the highs of 2018 where previous trouble asserted itself.

However, as I will discuss, there is more than a sufficient case brewing that the Fed may not be able to hike much at all. In other words, the Fed could be “one and done.”

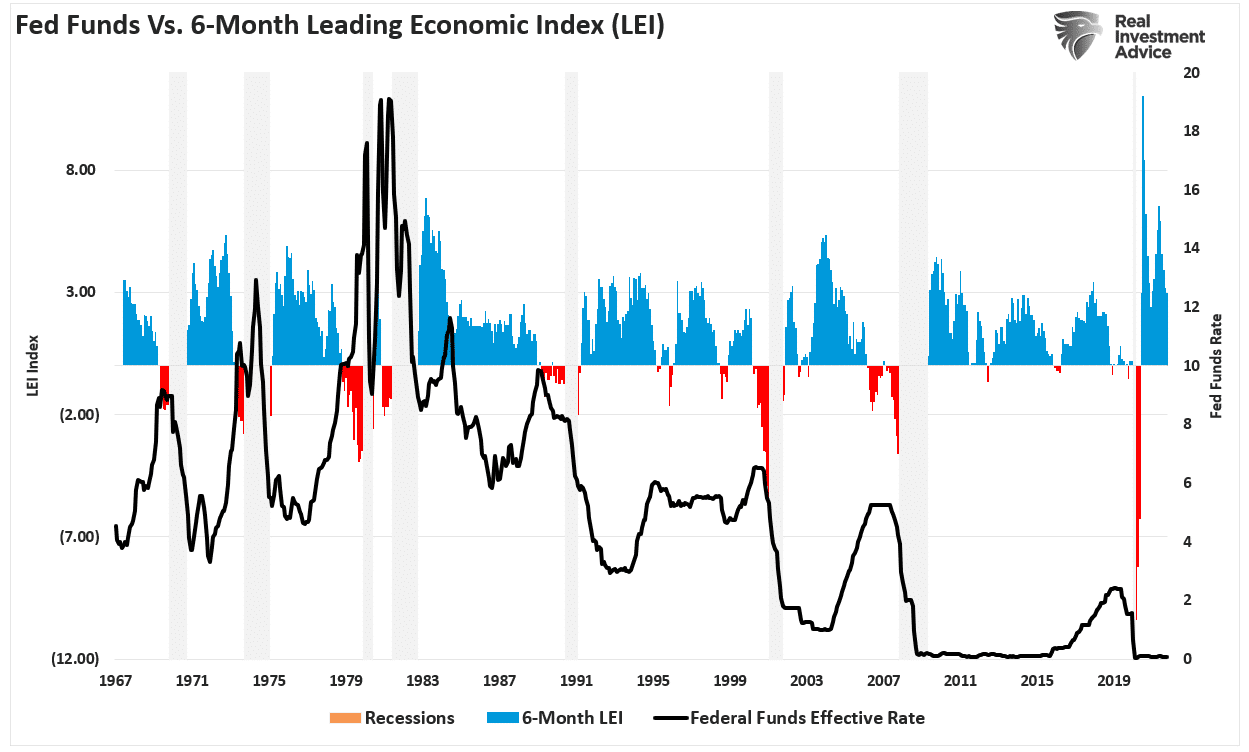

The Fed Is Too Late

As shown below, our composite economic indicator (which comprises more than 100 different data points) suggests a peak in economic growth currently. The correlation with the 6-month average of the Leading Economic Index confirms the same.

As shown, both leading indicators are turning lower, suggesting a peak in economic activity. If we overlay the Fed Funds rate with the 6-month Leading Economic Index (LEI), we see that the economy slows every time the Fed starts a rate hiking campaign. Notably, the peak of each rate hike cycle was lower than the last.

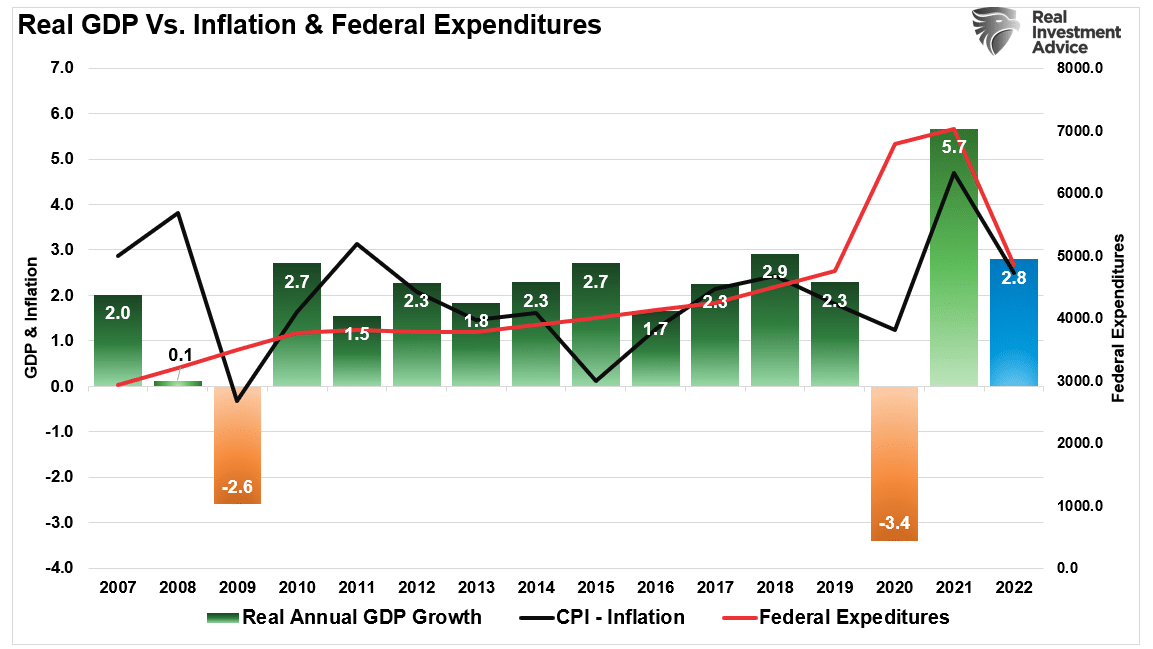

Furthermore,as we noted yesterday, the contraction of liquidity, as shown by Federal expenditures, suggests the economy, and subsequently, inflation will reverse in 2022.

The Fed’s Precarious Position

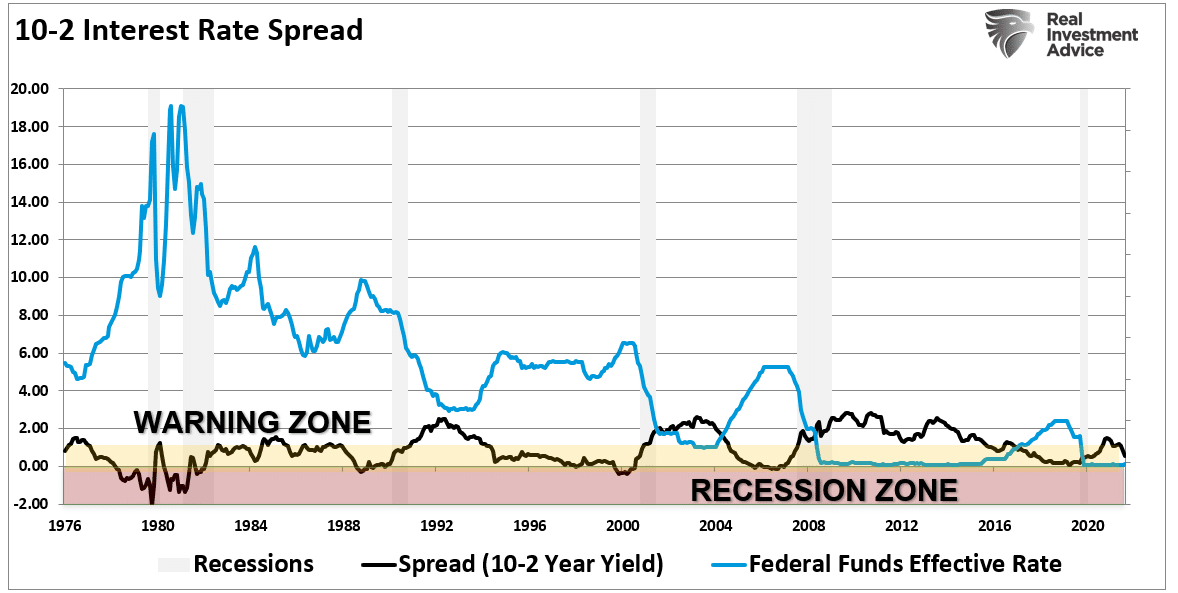

Such puts the Fed in a precarious position of tightening monetary policy at precisely the wrong time. The yield curve is already screaming the Fed is hiking rates too late.

Such leaves only TWO possible options, both of them are not good.

- Leave rates at zero to support the stock market, but economic inequality widens further.

- Hike rates and the risks an economic decoupling that leads to a deleveraging process.

The second problem is the most significant. Given the Fed stayed at zero for far too long, the ability to significantly lift rates before triggering a recession has likely passed. Therefore, the Fed may be “one and done” effectively negating the most effective tool for cushioning a recession.

As noted above, by chasing inflation (reactive versus proactive), the Fed has a long history of creating bad outcomes for the market and the economy.

This time will likely be no different.

The Fed’s Trapped At Zero

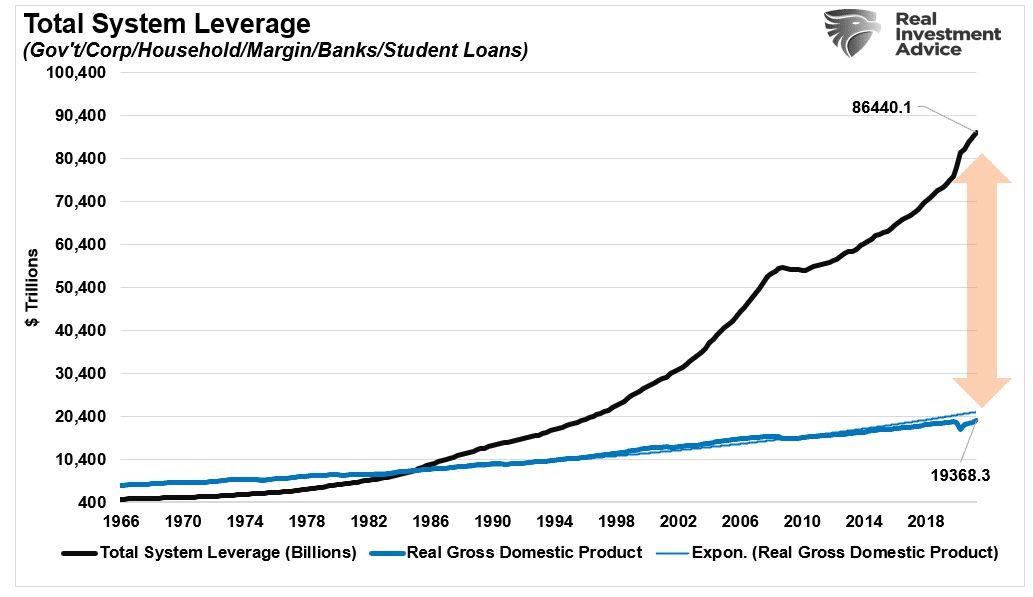

Furthermore, the debt problem remains the most significant risk. Such is because it takes an enormous amount of leverage to support increasingly feeble economic growth rates. Such means that “low borrowing” costs are essential to maintain consumption.

While the Fed uses monetary policy as a blunt instrument, they face several challenges that erode policy effectiveness.

- An aging demographic, which continues to strain the financial system

- Increasing levels of indebtedness, and

- Unproductive fiscal policy

Notably, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. As a result, the rise and fall of stock prices have little to do with the average American’s participation in the domestic economy.

Interest rates are an entirely different matter.

Since the turn of the century, monetary and fiscal policy has remained “bottled up” in the top 20% of the economy.

However, for the bottom 80% who drive the majority of economic growth, interest rates affect “payments.” When rates increase, there is an almost immediate negative impact on consumption, housing, and investment which comprises the bulk of economic growth.

Given the latest economic data points, the decline of the yield curve, and record leverage at all levels, we suspect the Fed has very little wiggle room.

Don’t be surprised if the Fed is “one and done” in March.

If you don’t believe me, maybe you will listen to the Mises Institute:

“The Fed is trapped in its own web. It does not have much room to raise rates without major complications in the financial market and in the economy. Even if it finally delivers on tapering and starts raising rates, it won’t get any further than it did back in the last rate hike (2015–18) and balance sheet shrinking (2017–19) cycles.”

Portfolio Update

Last week, we discussed comments from my colleague Doug Kass on the difficulty of “buying when there is blood in the streets.”

“Most importantly, the upside reward versus downside risk has improved and there is a growing list of attractive stocks.” – Doug Kass

The expected bounce continued with “growth stocks,” leading the charge higher this week. The outperformance came from recent earnings reports from Apple, Microsoft, and Google. However, while earnings supported investor buying, much of the rally was short-covering from extremely oversold levels.

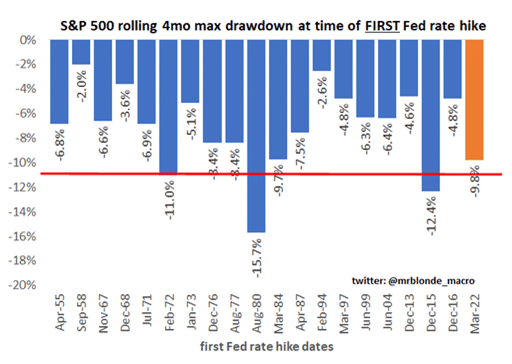

The recent 10% drawdown is in line with other periods preceding an initial rate hike.

However, it remains too early to say with certainty the recent lows were “the bottom.” We suspect that such is not the case, and a retest is likely at some point. History, as noted, also suggests that rate hike cycles are not particularly kind to bull markets.

We are currently maintaining a more cautionary stance in our portfolios. However, this week we did get more defensive by reducing our equity exposure and increasing our short-S&P 500 hedge position.

Investors remain convinced the Fed will always bail the market out. However, it could be from much lower levels than we saw in January, even if the Fed is “one and done.”

Former Dallas Fed President Richard Fisher provides some insight.

“The market has been wearing beer goggles for the longest possible time. They just assume the Fed’s going to bail them out. I think the strike price on the Fed put has moved significantly. And unless we have a dramatic turn in the markets that indicates it can infect the real economy, I don’t believe they will be weak in following through on what they pronounced.”

In other words, don’t depend on the Fed.

Manage your portfolio risks instead.

Market & Sector Analysis

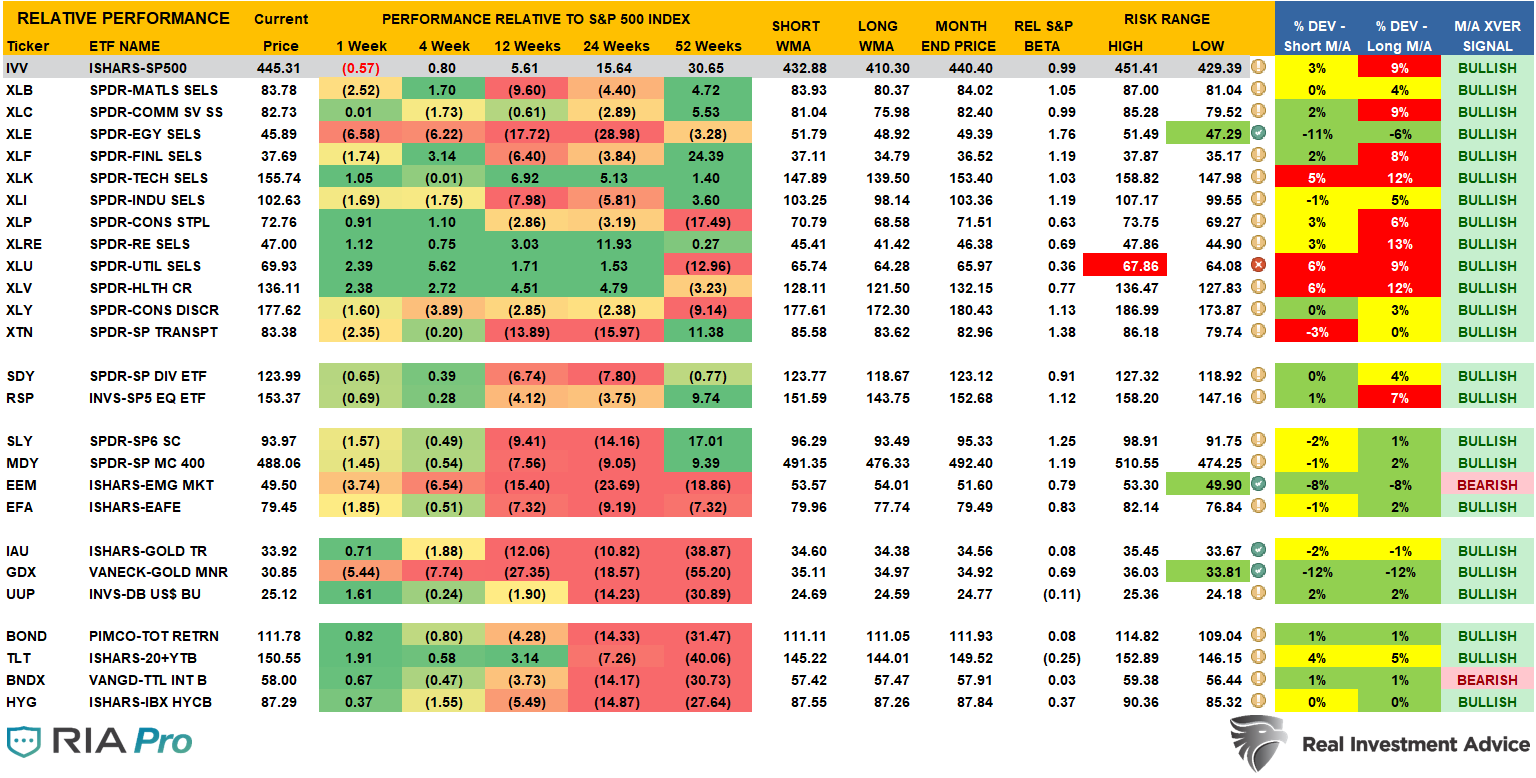

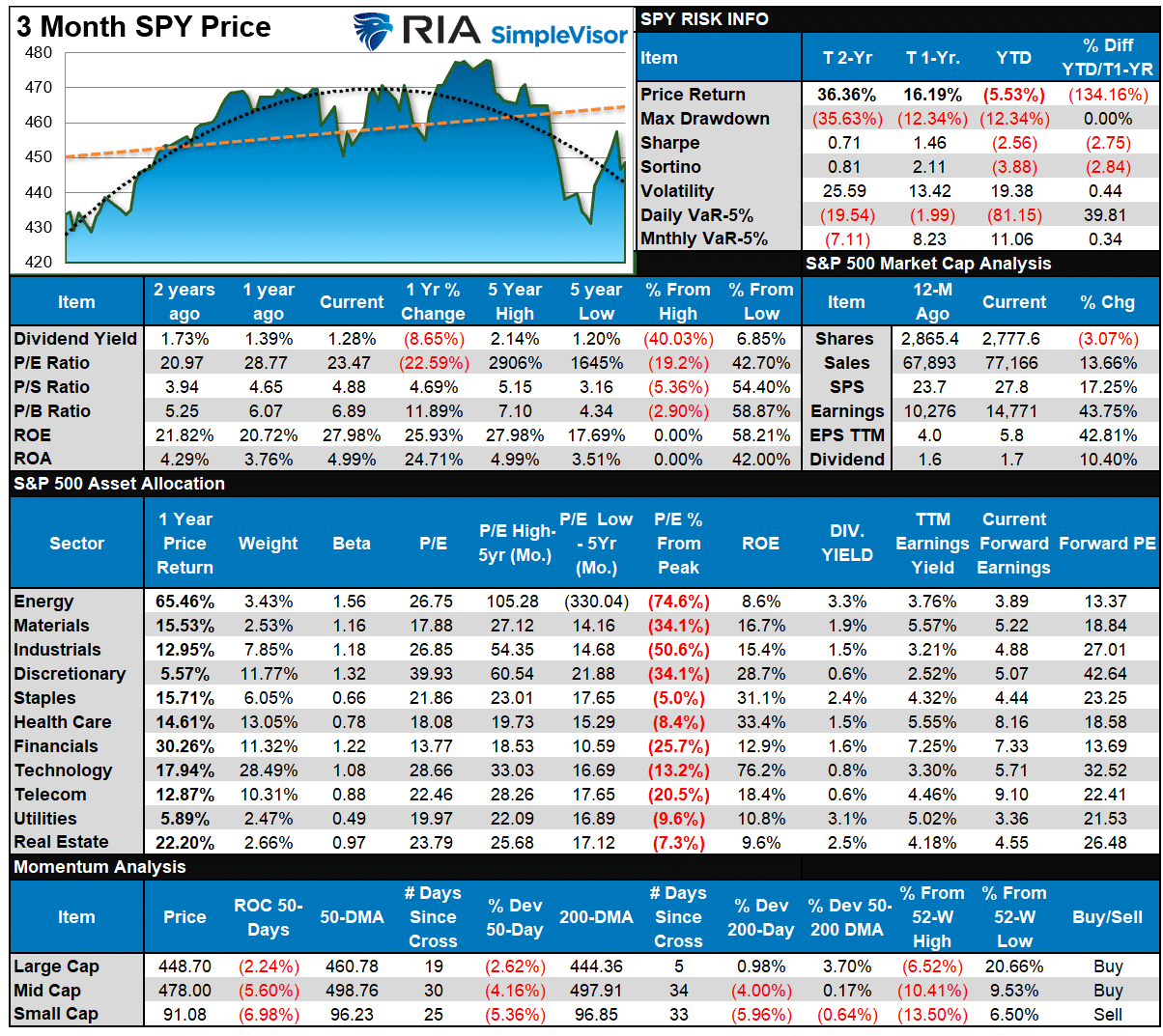

S&P 500 Tear Sheet

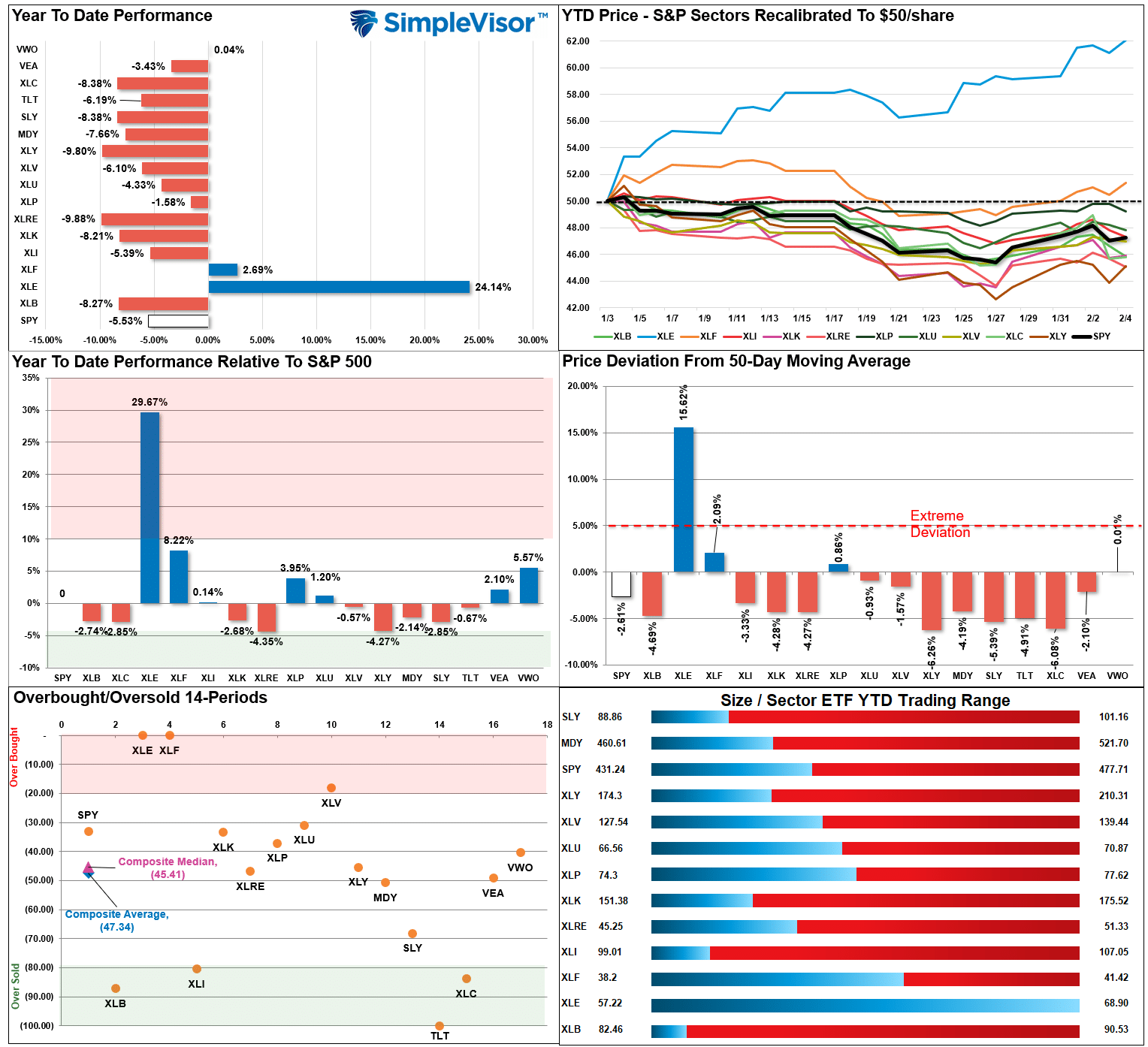

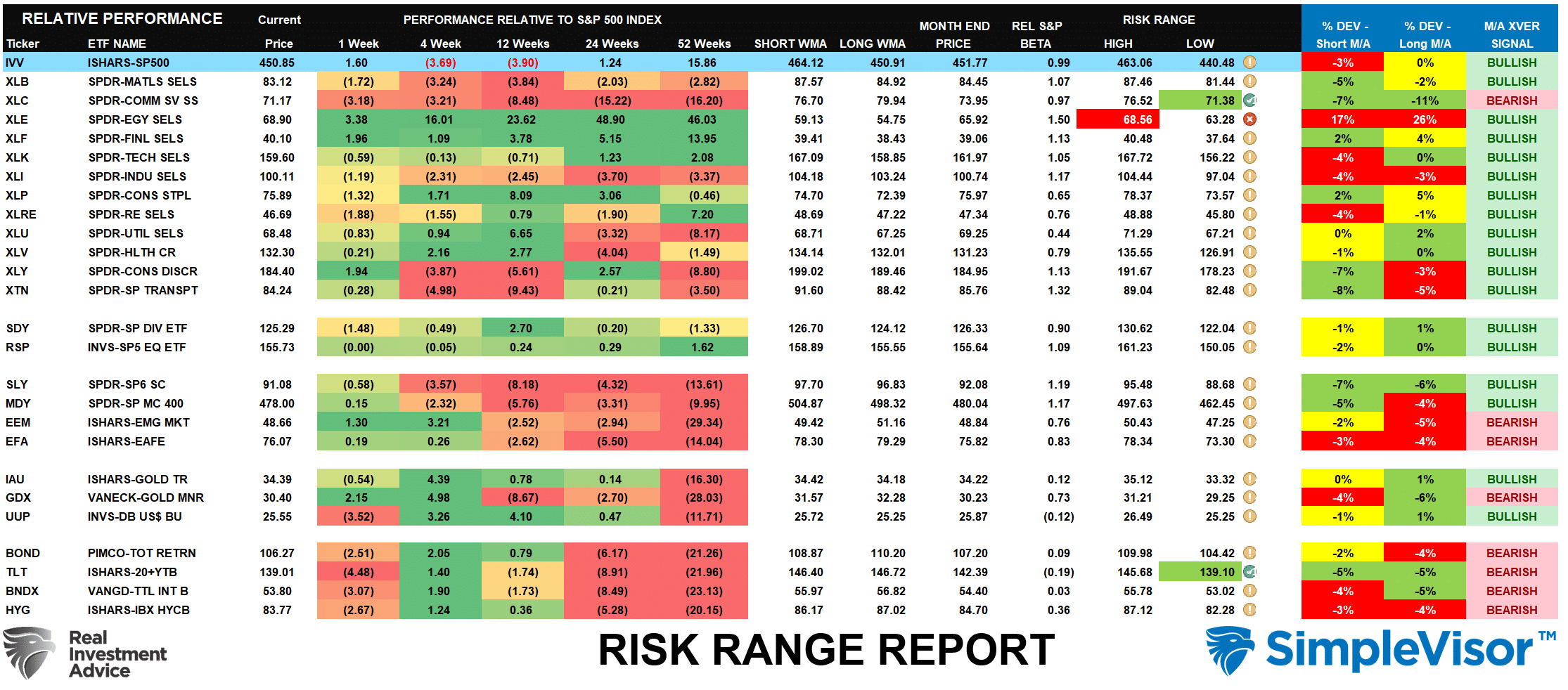

Relative Performance Analysis

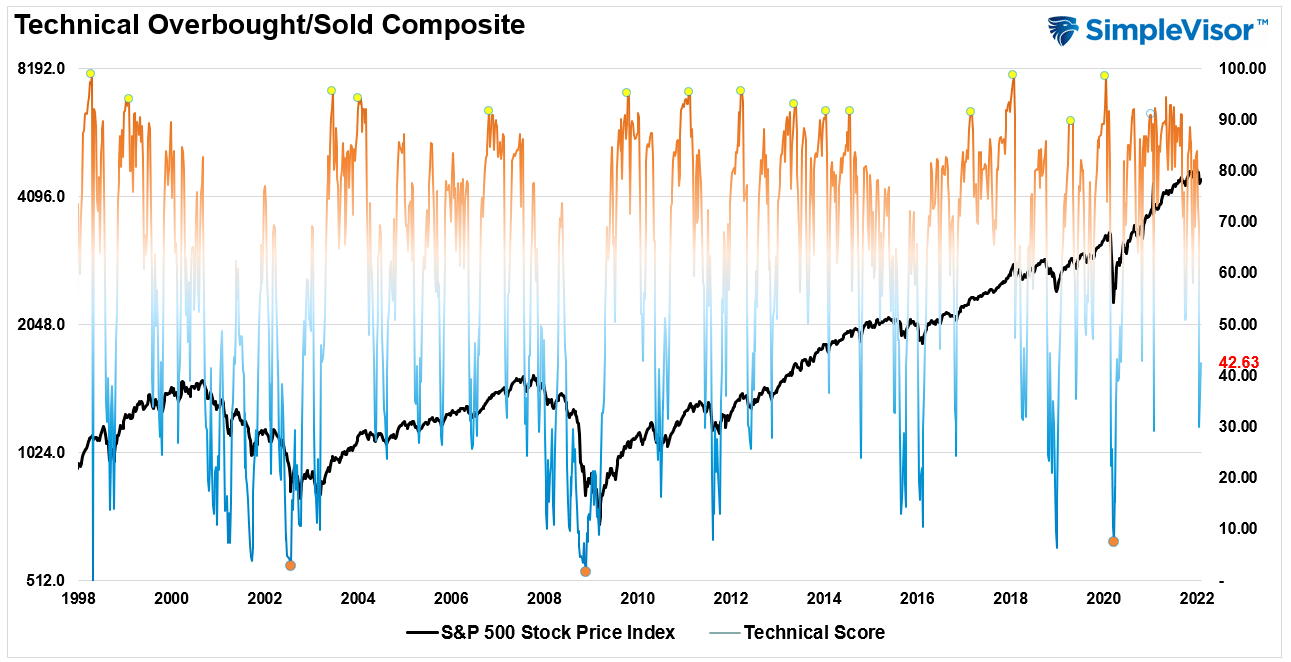

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 42.63 out of a possible 100.

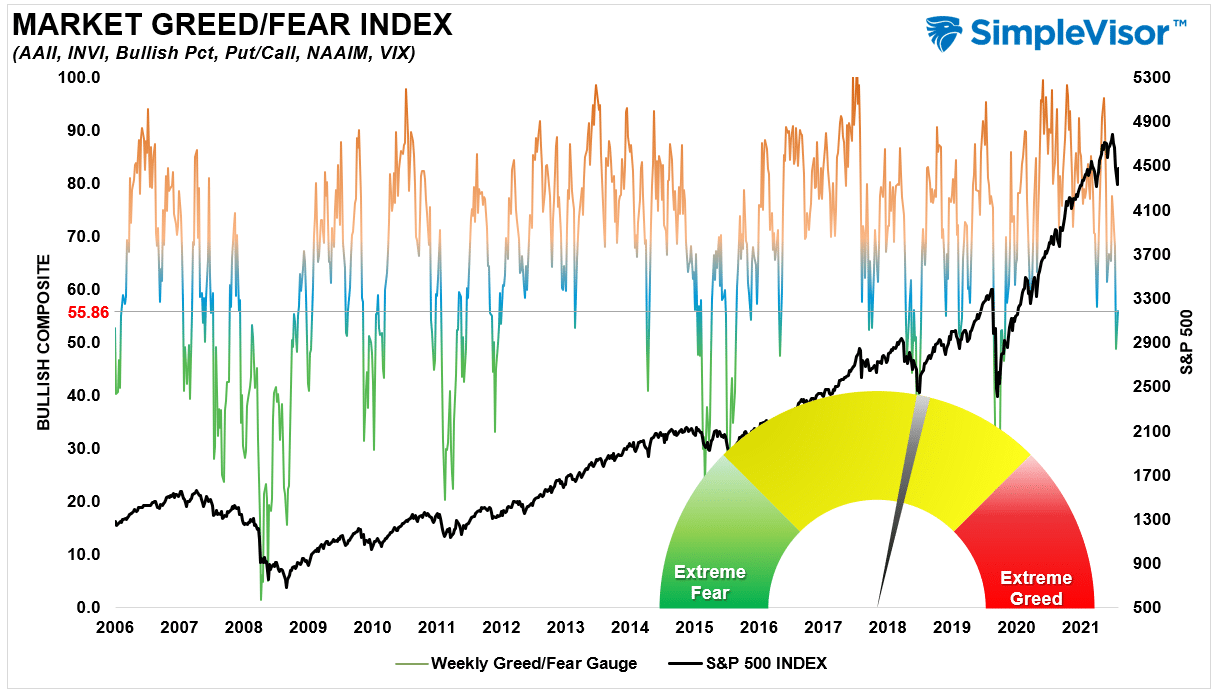

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 55.86 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is on under the Dashboard/Sentiment tab at SimpleVisor

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

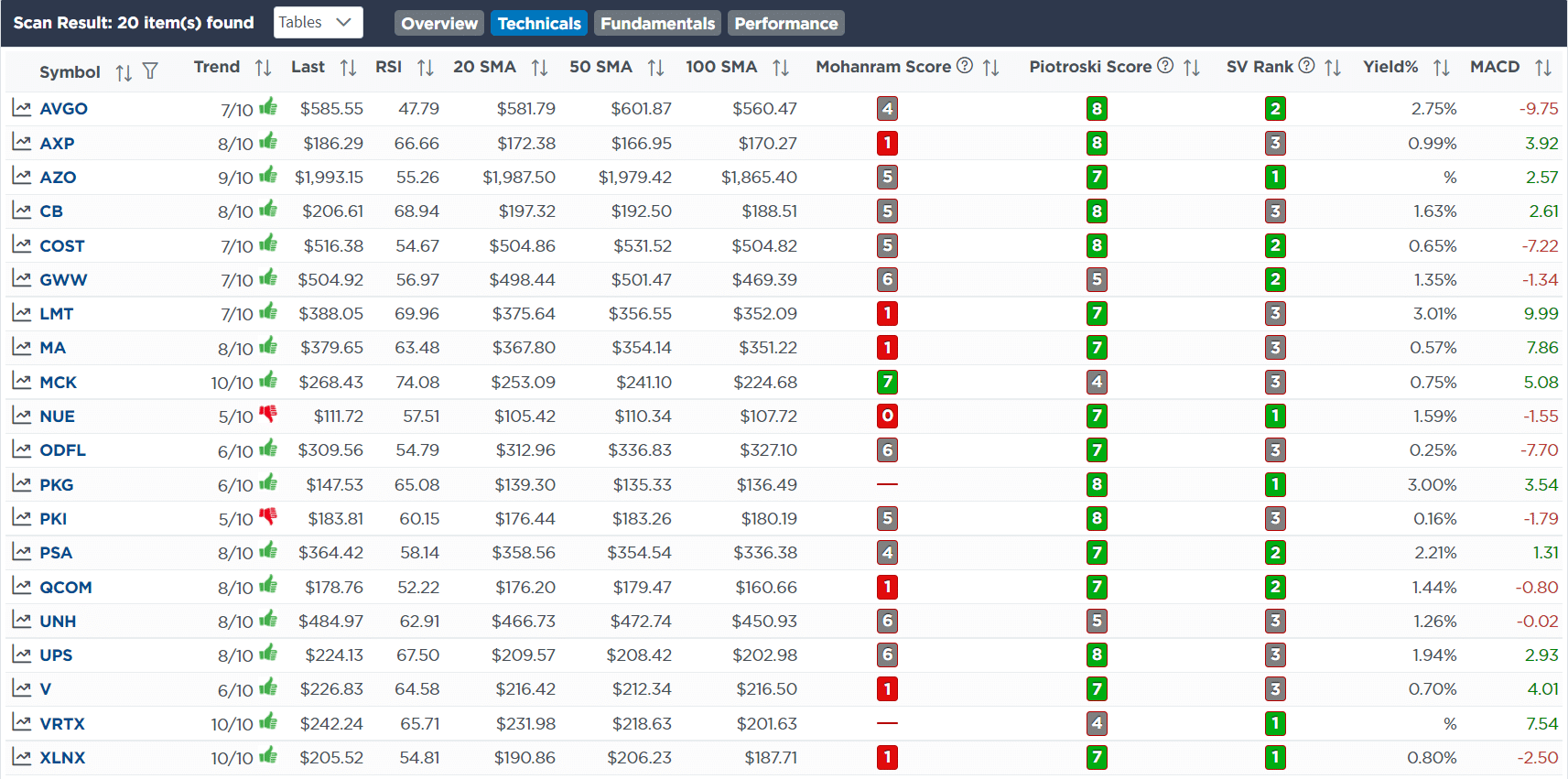

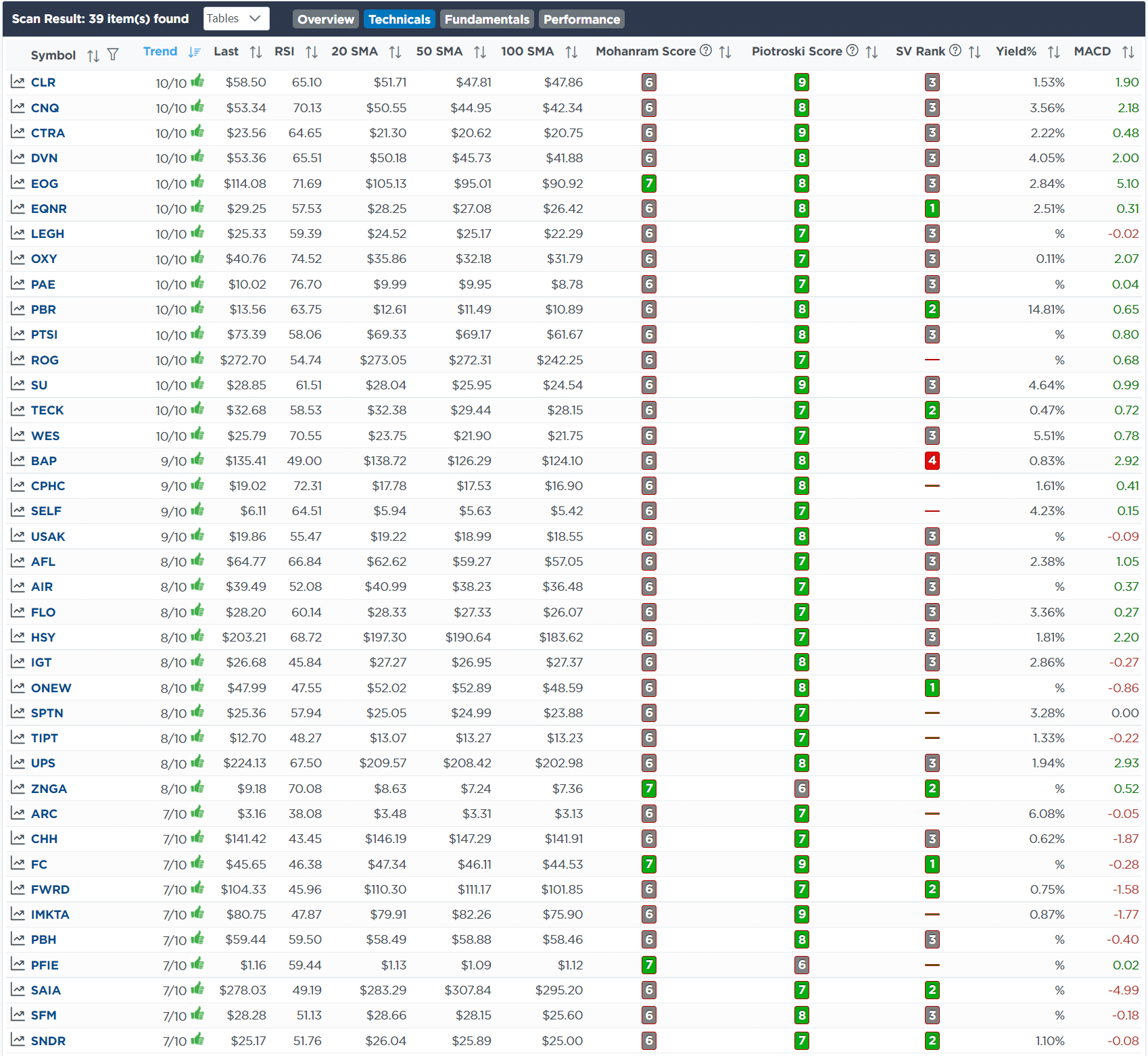

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

There were two sets of trades this week.

February 3rd

We previously noted that we expected an oversold reflex rally in the market and that we would use that rally to add to our short S&P 500 index position and reduce our holdings of PFF.

That bounce came earlier this week with a 61.2% Fibonacci retracement. With the poor earnings announcement from Facebook/Meta (FB), we added to our short position and reduced PFF some more.

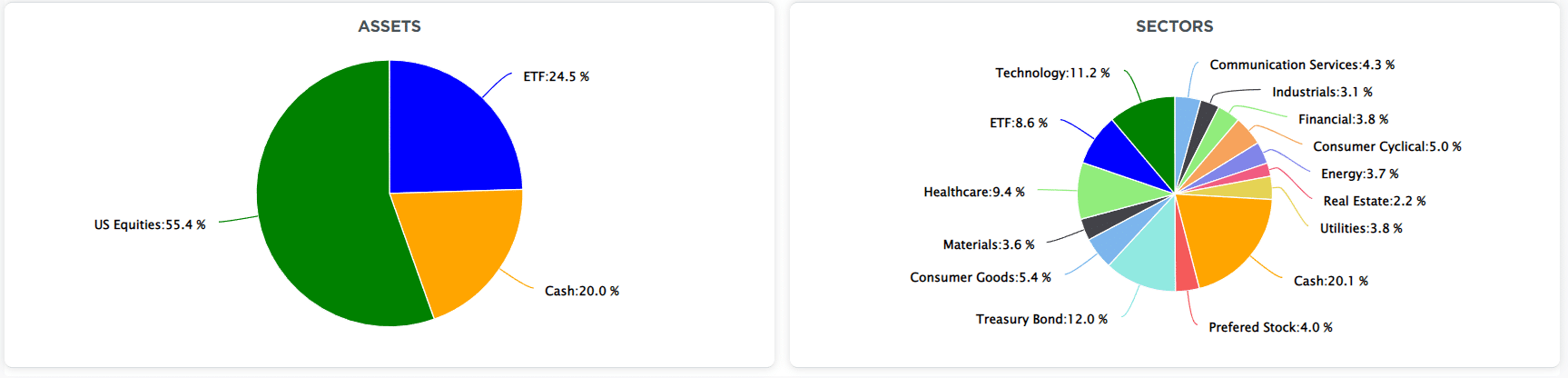

Equity & ETF Models

- Sell 4% of the portfolio position in PFF

- Buy 2% of SPDR S&P 500 5hort (SH)

February 4th

This morning we sold 1/2 of our Amazon stake and reduced the SPDR Discretionary ETF (XLY) by 1% of the portfolio (Amazon is the biggest component.) While we like Amazon longer-term for many reasons, the earnings report yesterday, which caused a spike in the stock this morning, shows weakening across many metrics of sales and revenue growth. As such we are reducing the position and will wait for a future opportunity to add back to it.

Equity Model

- Sell 50% of Amazon (AMZN)

ETF Model

- Reduce XLY by 1% of the portfolio

Lance Roberts, CIO

Have a great week!

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.