Market Review & Update

We noted last weekthat while the market was short-term overbought, the market could rally further. To wit:

“As we head into the end of the month, a further push to the upside is not out of the question as mutual funds, pensions, and investment firms rebalance portfolios (window dressing) for the end of the quarter. The recent surge in interest rates has decreased the bond side of allocation funds. Also, the decline in the markets since the beginning of the year has fund managers at reduced equity levels, overweight cash, and negatively biased.”

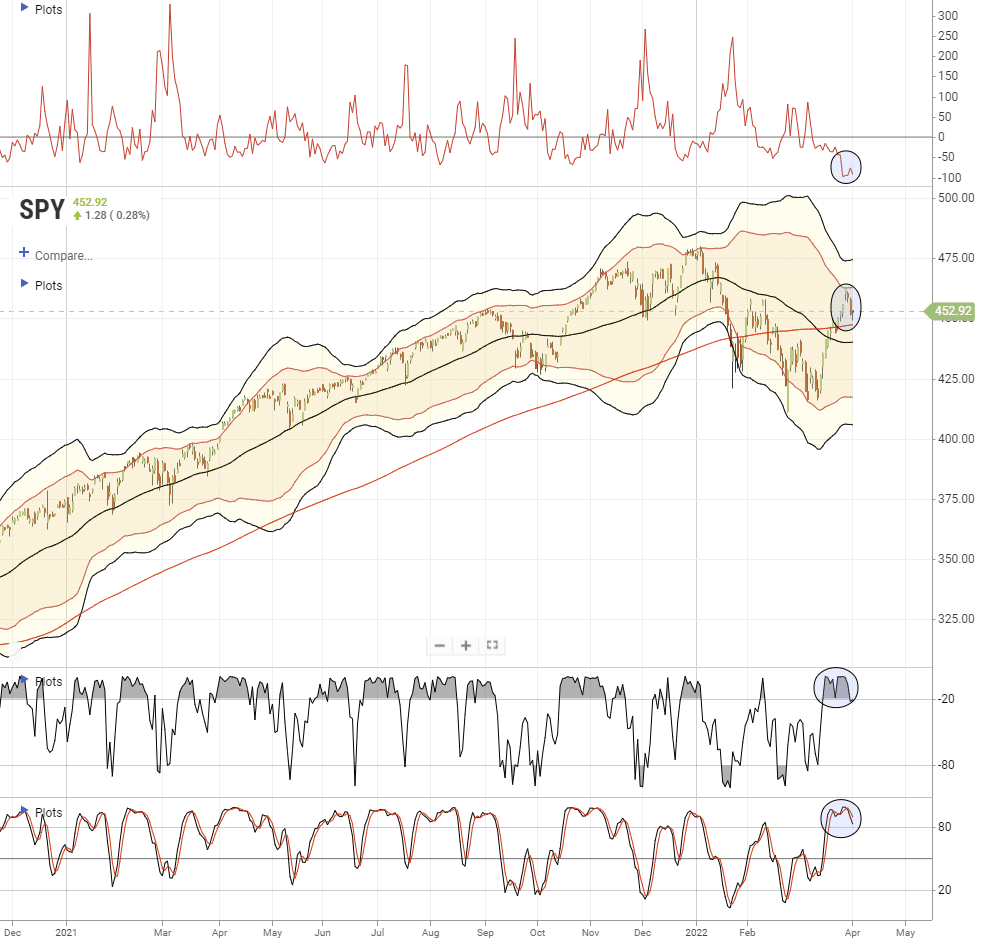

That window dressing rally was quite strong and pushed the market into extreme overbought territory.

Technically, the pullback on Thursday and Friday was healthy as it began to reverse the more extreme overbought conditions. However, there is more work to do before a better entry point is available.

If the market can hold support at the 200-dma, or even the 50-dma just below, then the market could make another rally attempt later this month. If not, then the rally was reflexive, short-covering, and will retest lows.

However, be careful getting too bearish. As we will discuss momentarily, April tends to be a historically strong month of the year. Notably, negative sentiment has improved and other indicators are suggesting a short-term bottom may be in. To wit:

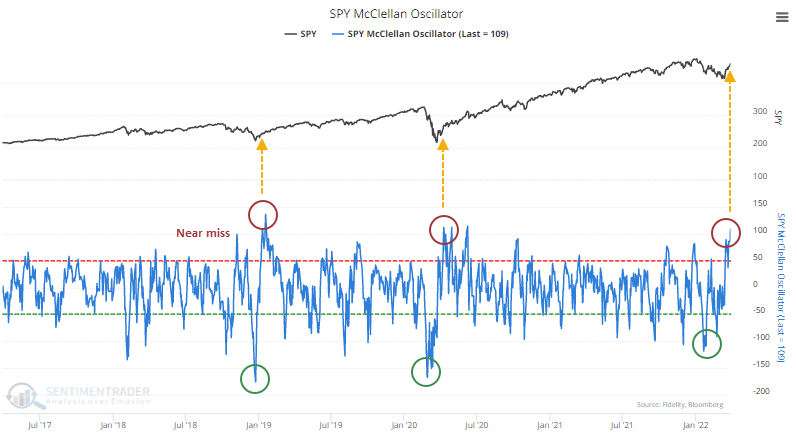

“Over the past few weeks, we’ve looked at various thrusts underlying some of the impressive moves in major indexes. Among them is the momentum underlying the S&P 500, with the McClellan Oscillator for the S&P cycling from below -100 to above +100.

This is only the 3rd time the indicator has made such an extreme round trip over the past 5 years. The other two coincided with significant bottoms.” – Sentiment Trader

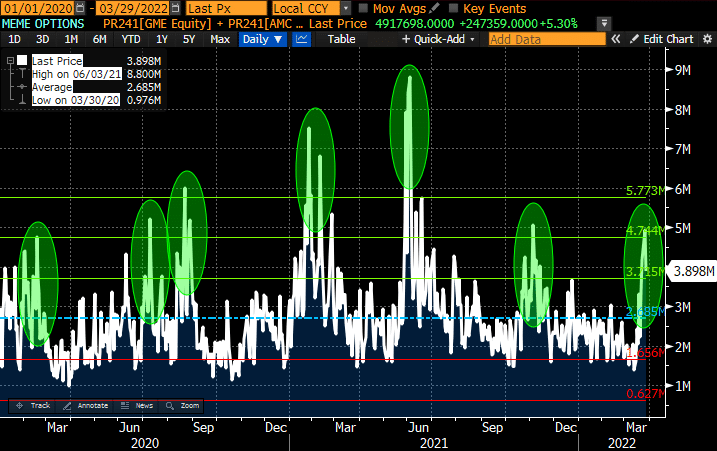

Since the lows from a few weeks ago, the market surged sharply higher. While that surge was impressive, it had “bear squeeze” earmarks,as some of the most shorted names surged higher.

While the rally was significant, with companies like GameStop up more than 100% in two weeks, the underlying market drivers are reversing.

- Interest rates have moved higher in advance of the Federal Reserve.

- The Federal Reserve is hiking rates and appears committed to continuing in upcoming meetings.

- Liquidity, from checks to households, unemployment, and child tax credits, is ended, and savings are declining.

- The economy is slowing.

- Inflation is remaining stubbornly higher, further tightening monetary policy.

- Earnings expectations for the S&P 500 are declining rapidly, and;

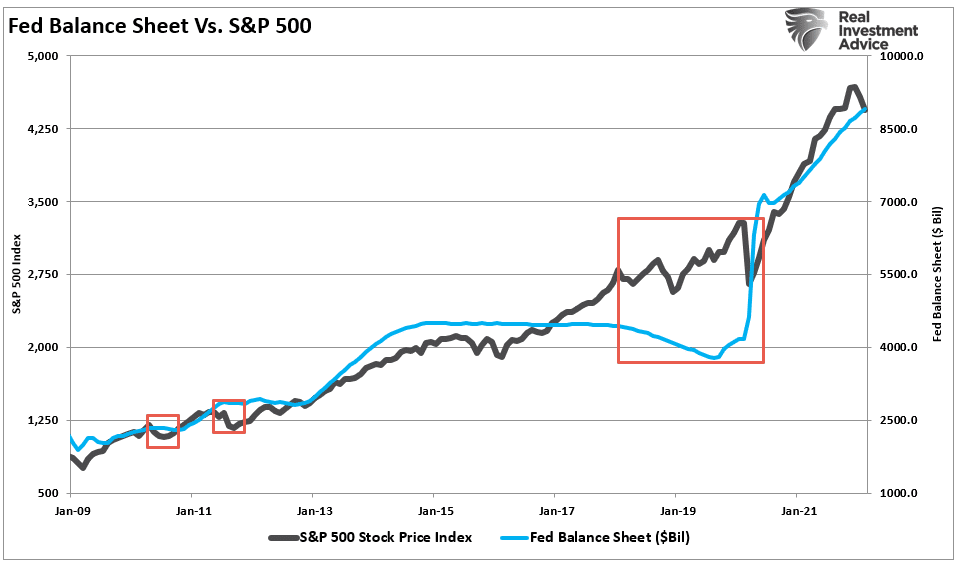

- The Federal Reserve will begin to reverse, or taper, the size of its current balance sheet.

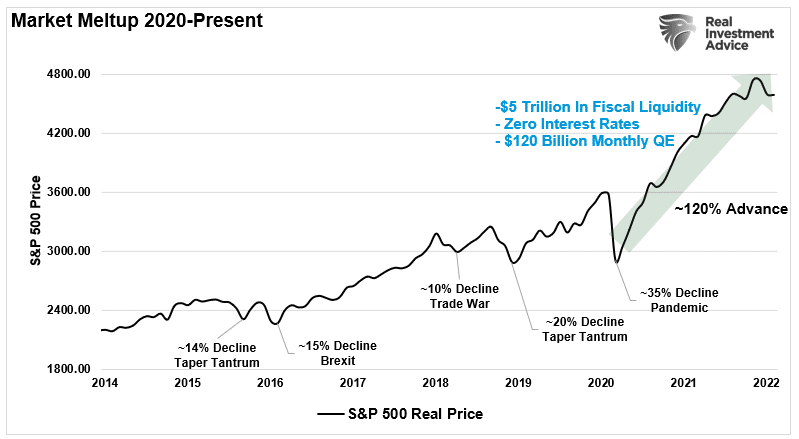

The two most critical points to continuing a bull market are the reversal of liquidity and the Fed’s taper.

We remain concerned about the reversal of liquidity as it was a crucial influence on the outsized market advance in 2020 and 2021. Such was due to the younger investing generation migrating to apps like Robinhood to substitute stock betting for sports.

Secondly, there is a direct correlation between the reversal of the Fed’s balance sheet and market corrections.

Currently, the market dynamics as we advance are less than bullish. We suspect the current rally remains an opportunity to rebalance portfolio risk and manage exposures. Historically, when “bear squeezes” are over, the sellers reemerge and drive prices lower again.

That’s what we saw at the end of the week, and why we remain cautiously biased.

Caution Remains

While the short-term technical underpinnings have improved as window dressing ensued, I remain cautious currently for several reasons:

- The market is GROSSLY overbought in the short-term and must either consolidate at current levels or correct to lower levels to resolve it.

- Negative trends are still in place, which suggests the current rally, while significant, remains within the context of a reflexive rally.

- Volume is declining on the rally, suggesting a lack of conviction.

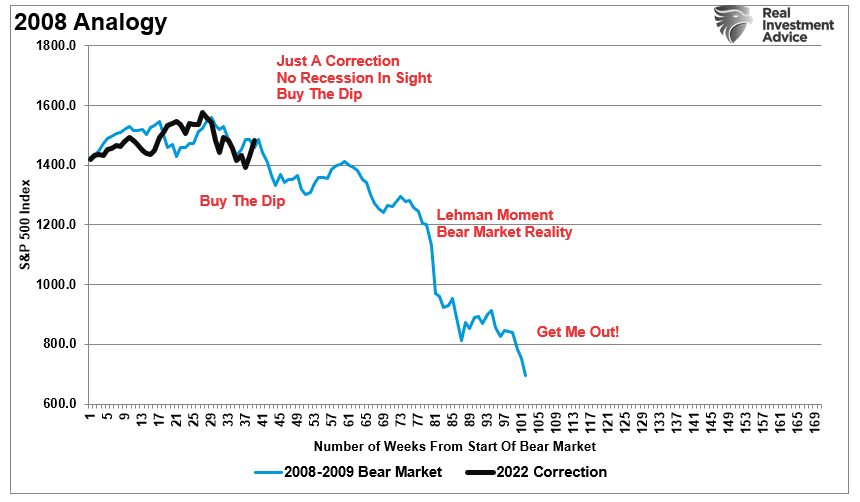

- The current rally looks similar to the rally in 2008, except the fundamentals are substantially weaker. (i.e., valuations.)

NOTE: We are not saying the market is about to go into a protracted bear market. However, the recent 10%ish rally in the market is similar to what we saw during the 2008 market.

Notably, in early March, we discussed that after two-negative months of returns and the worst start to a year since the “Financial Crisis,” it would not be a surprise to see a positive return. As noted in “The Revenant:”

“There is a high probability of an outsized reflexive rally over the next two months due to several factors. While we expect a significant rally from current levels, likely following the Fed’s meeting next week, such should get used to reduce risk and rebalance exposures accordingly.

- Extreme negative sentiment

- Bearish portfolio positioning

- Higher levels of cash holdings by fund managers

- Dumb money is bearish

- Put/Call ratios are offside

- The number of stocks trading at 52-week lows.

While the reflexive rally was likely, whether or not it turned into a sustainable “bull market” trend depends on whether recessionary factors persist.

With the yield curve rapidly inverting, the risk of a recession is certainly more elevated than it was a month ago.

Can April Continue The Run?

Could April continue the bullish run?

With quarterly “window dressing” now behind us, all eyes will focus on the vital short-term drivers of markets.

- Fed policy commentary before the May FOMC meeting.

- The start of the Q1-2020 earnings season will show slower earnings growth

- Inflation impact on economic data.

- Corporate share buybacks will remain a key driver of stock buying.

- Economic data will likely start to show signs of weakness.

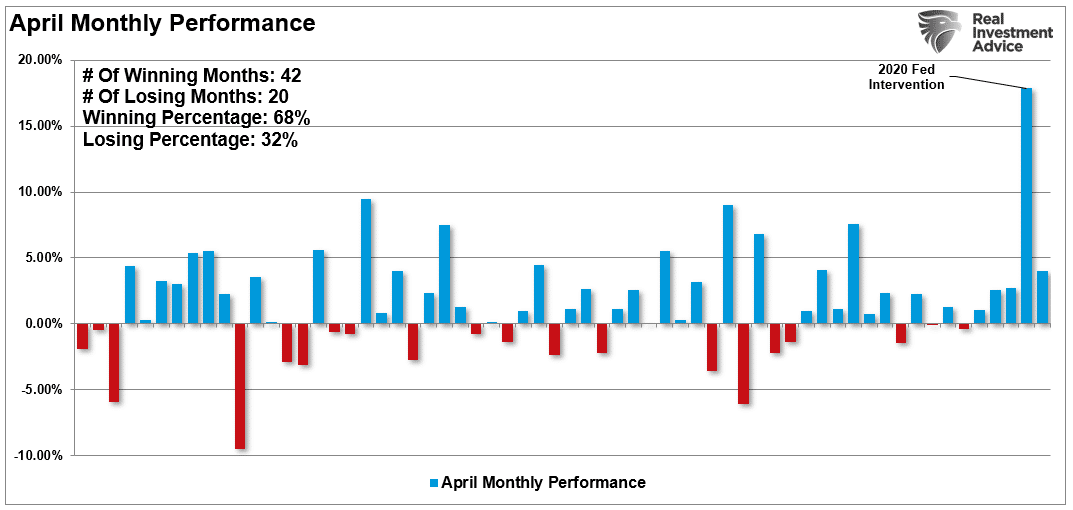

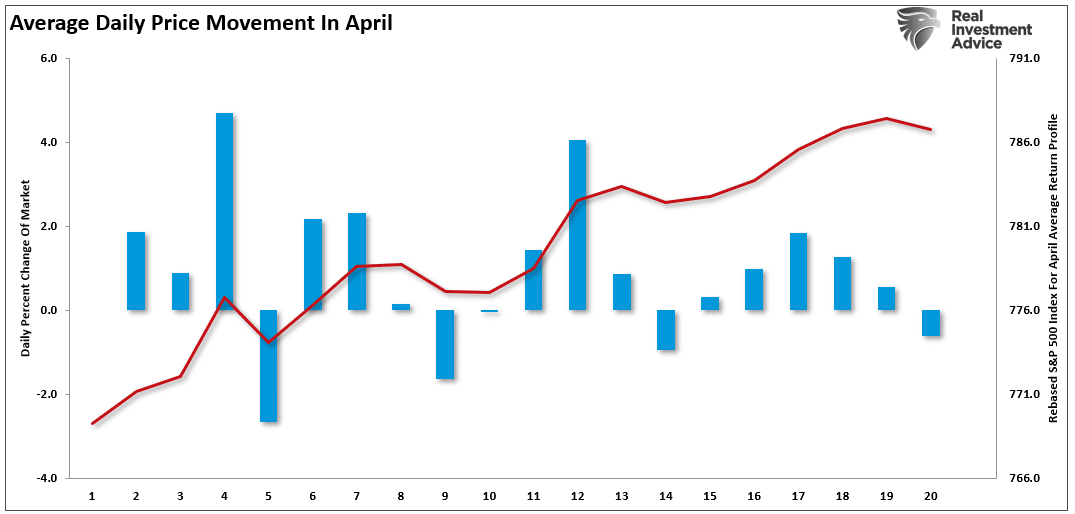

Notably, the historical tendencies are bullish for April.

Furthermore, April gains tend to come at the beginning and middle of the month following tax filing deadlines.

Going back to 1957, it should not be a foregone conclusion that April will end in positive territory. While the statistical odds currently favor such a scenario, it does not mean it will be the case.

Any good news on the Russia/Ukraine front, weaker commodity prices, or a pivot by the Fed to a more “dovish” stance could encourage the bulls short-term. However, the risk of a further market correction is undoubtedly present.

- Inflation was surging before the rise in oil prices.

- Now those higher prices are impacting consumption.

- Liquidity support is reversing.

- The massive infusions of fiscal liquidity in 2020 and 2021 are gone.

- The Fed’s QE program is over, and they are now hiking rates.

- The Fed will start reducing its balance sheet in May.

However, monetary policy is already much tighter due to the inflationary build. When the Fed hikes rates, it will likely slow the economy much faster than most expect.

While there are bullish arguments to support higher prices, the current risks seem more elevated than witnessed previously.

Again, some caution seems logical.

Portfolio Update

Yes, there are undoubtedly many reasons for investors to be cautious currently. However, there is a possibility that the bulls could regain control of the market and drive asset prices higher. Such would continue the bull rally that started in 2009.

It is always important to never discount the unexpected turn of events that can undermine a strategy. While we continue to err on the side of caution momentarily, it does not mean we will remain wed to that view.

With quarter-end window dressing now behind us, as noted at SimpleVisor.com, we took advantage of the rally to trim back the equity exposure that we increased a couple of weeks ago. The outsized market gain pushed our short-term indicators into more extreme overbought conditions. We are ending the quarter with a higher-than-normal level of cash which will hedge portfolios against potential risk in April.

For the same reasons we are raising and holding higher levels of cash, we are adding exposure to our longer duration bond holdings. Unlike stocks, bonds are very oversold after a substantial increase in rates. Bonds will also hedge our portfolios against a decline in April should one occur.

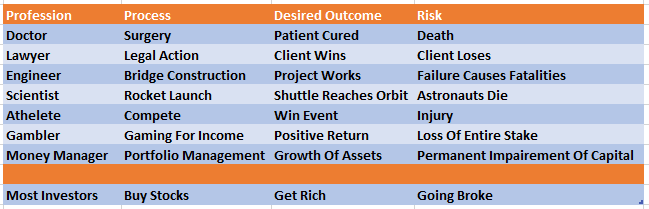

What If You’re Wrong?

As discussed this week, and is worth repeating, is that in every professional field, there is “risk.”

Those who fail to focus on and recognize the inherent risk, more commonly known as “being reckless,” tend not to be around very long in any given profession. What always separates the “winners” from “losers” are those that can avoid catastrophic damage over time.

The control of “risk” is also the essence of portfolio management.

Understanding risk is essential for investors as it is a function of “loss.” The more risk taken within a portfolio, the greater the destruction of capital will be when reversions occur.

Making absolute predictions, bullish or bearish, is not only useless but inherently dangerous concerning portfolio management. All we can do is make educated “guesses” about potential outcomes based on history, statistics, trends, etc.

So, what if I’m wrong?

What if the market continues to rise and all the above risks fade away?

We invest our stored cash back into the equity markets.

It’s not complicated.

It’s just a process.

As Nobel laureate Dr. Paul Samuelson once quipped:

“Well, when events change, I change my mind. What do you do?”

If this is a quarter-end window dressing “bear squeeze,” we will know soon enough.

See you next week.

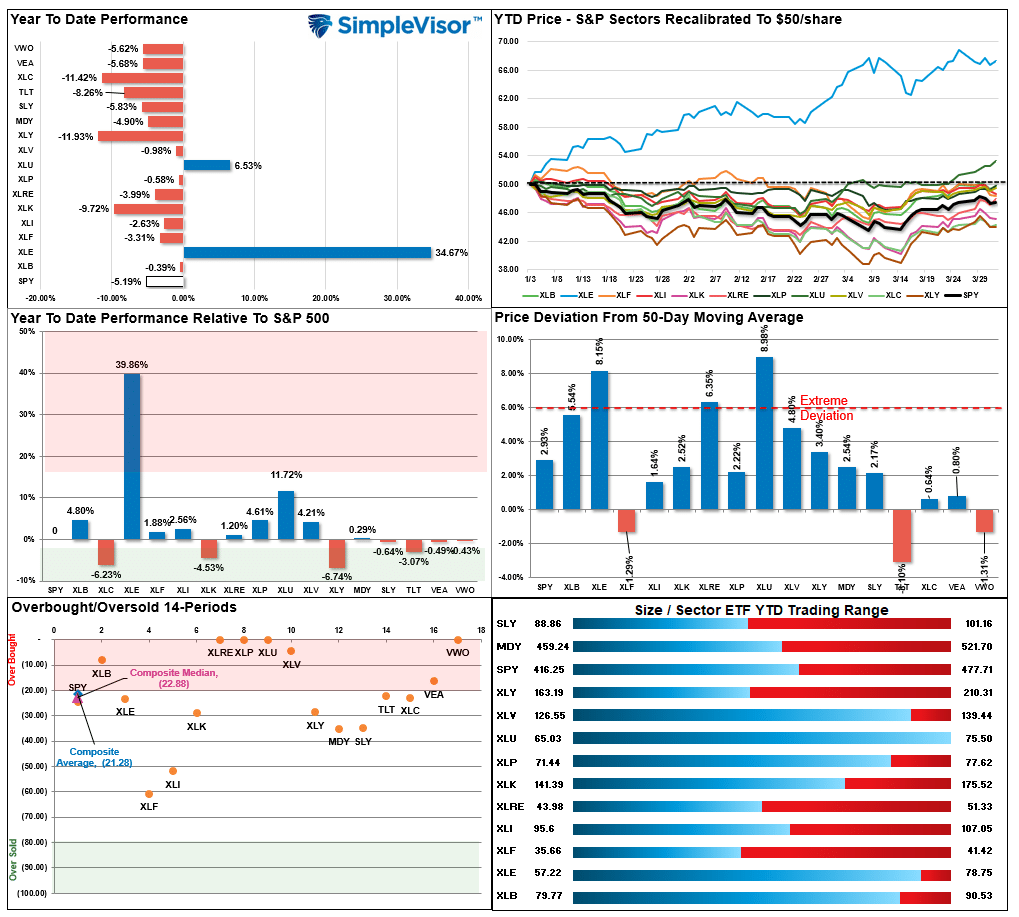

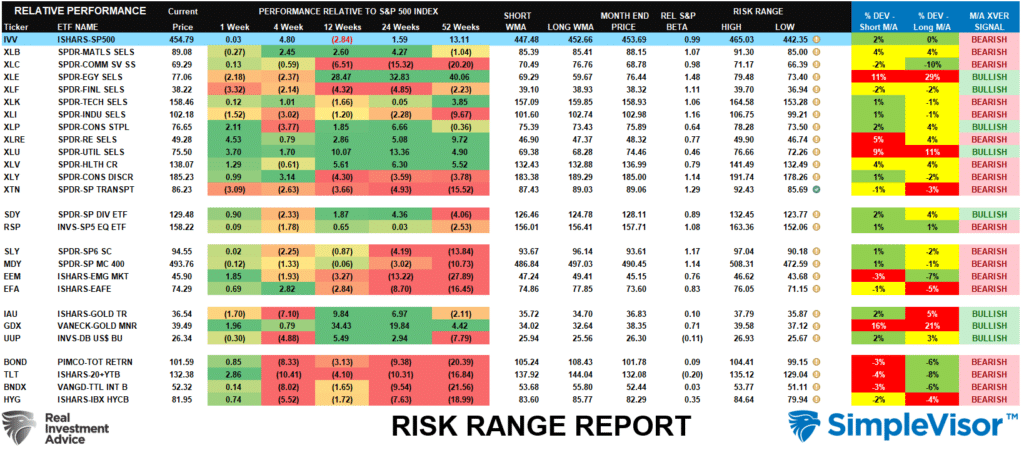

Market & Sector Analysis

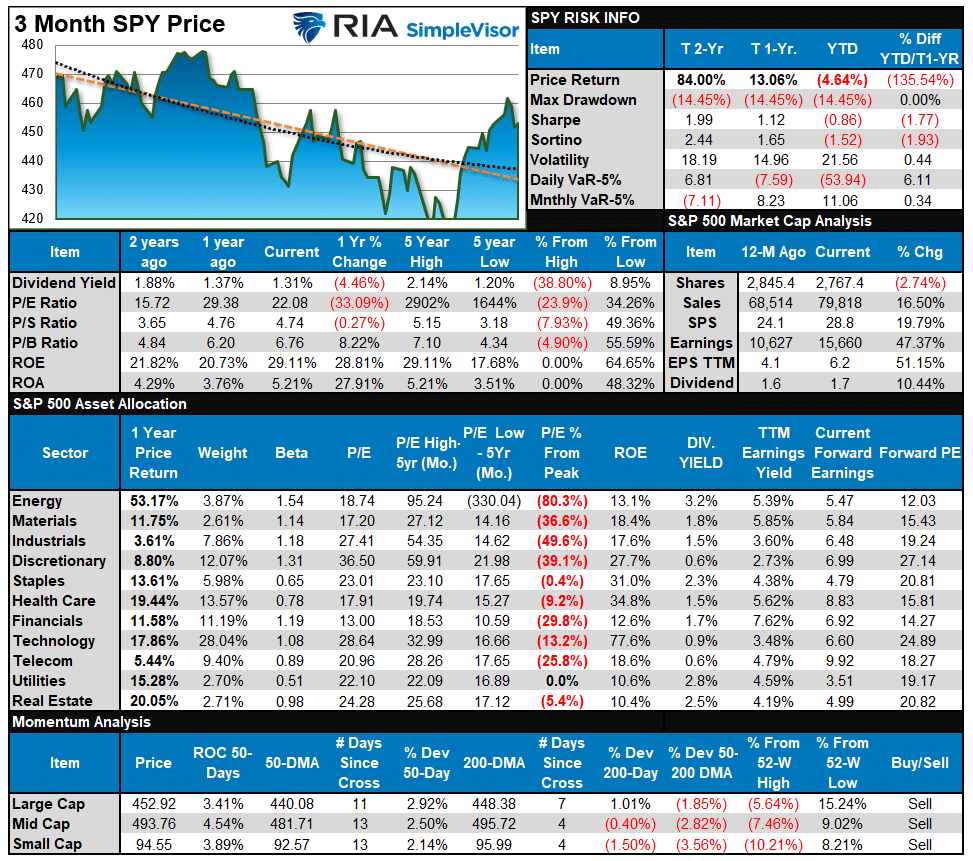

S&P 500 Tear Sheet

Relative Performance Analysis

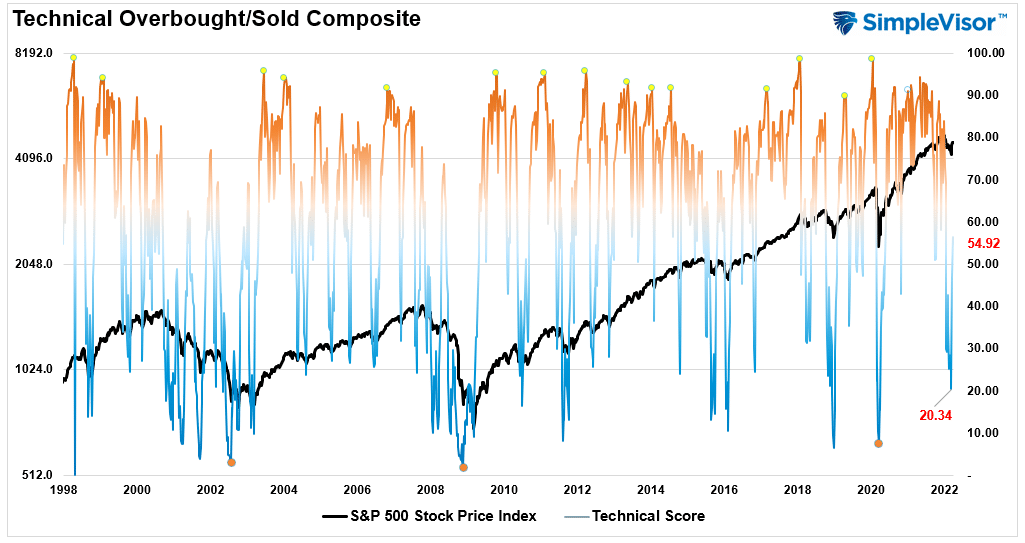

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 54.92 out of a possible 100.

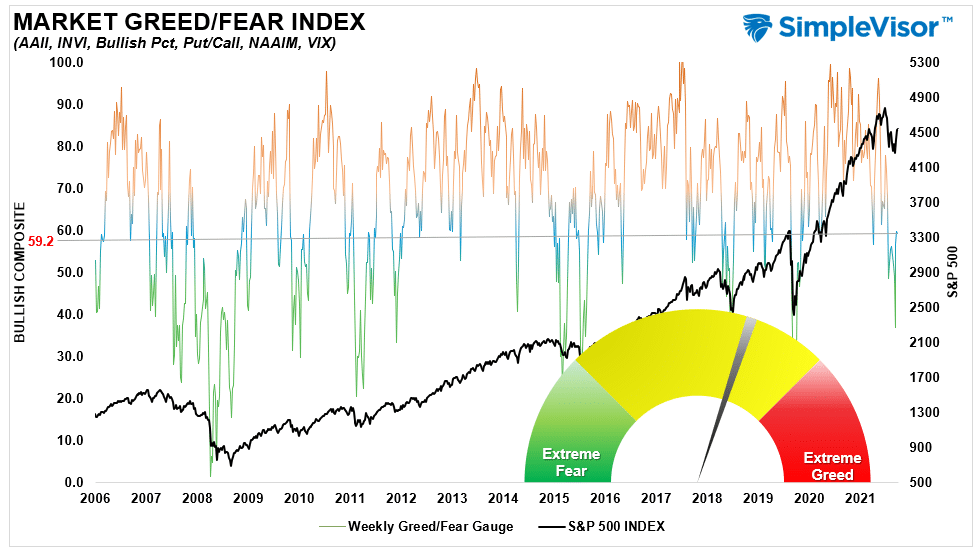

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 59.2 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is under the Dashboard/Sentiment tab at SimpleVisor.

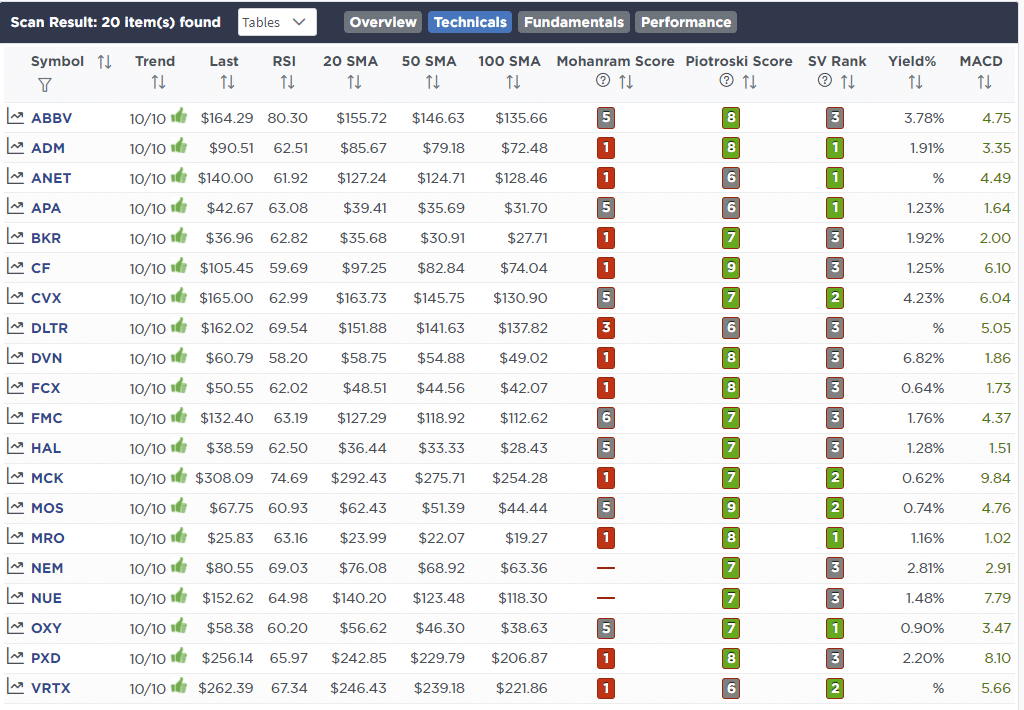

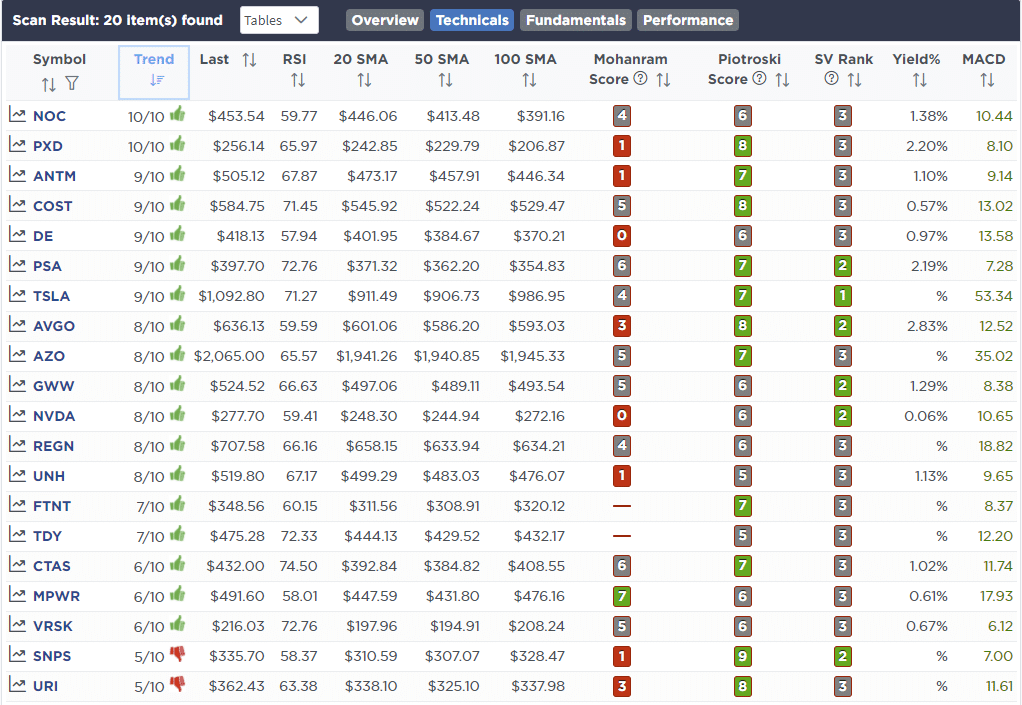

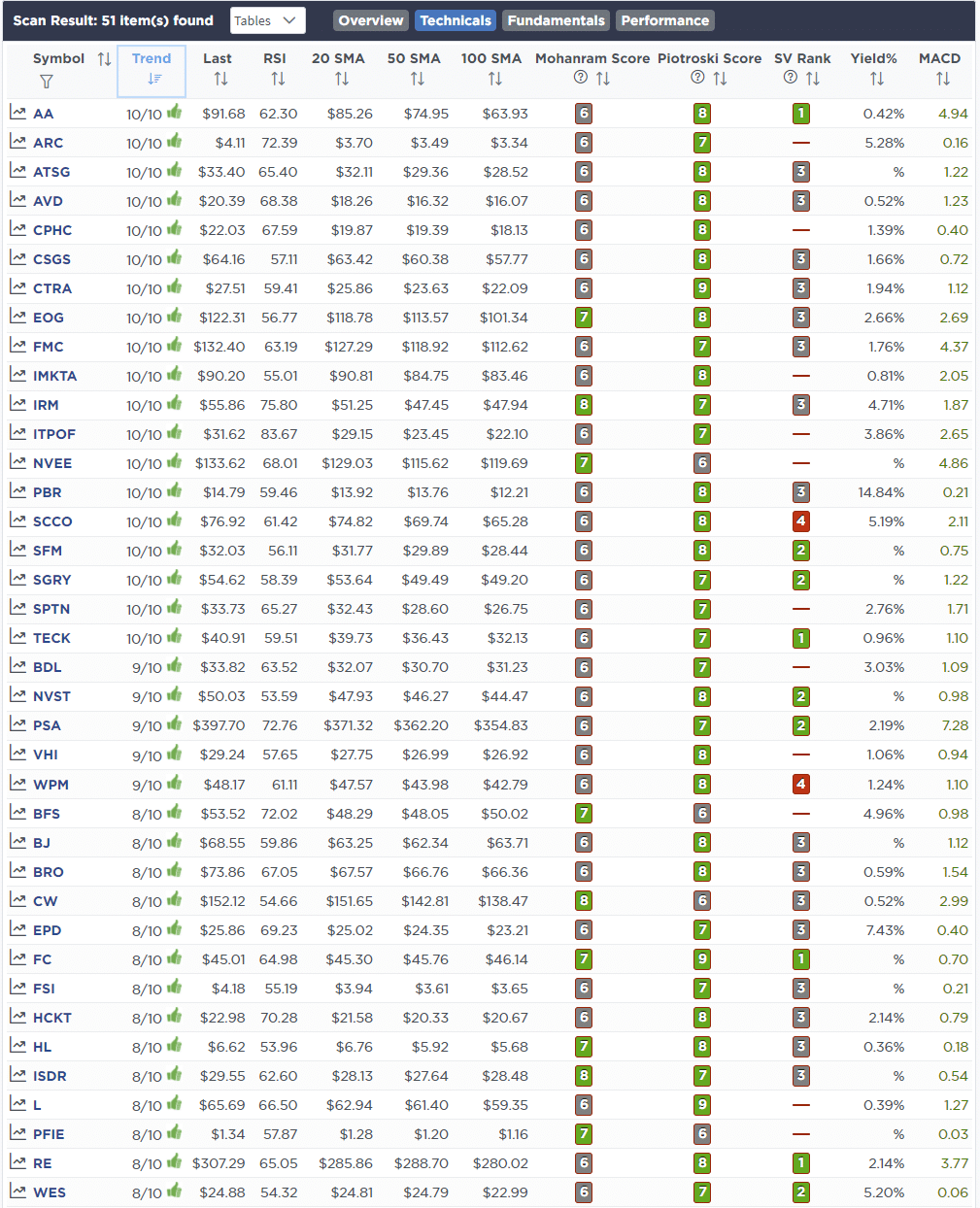

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

March 28th

We are taking profits in our recent growth stocks that we increased exposure to a couple of weeks ago. We had previously expected a reflexive rally, however, that rally was much stronger, and faster, than we expected. With equity markets now back to very overbought we are taking profits. However, with the bond market extremely oversold we also added to our bond exposure last week.

Equity Model

We are reducing the following positions

- Apple (AAPL) from 3% to 2.5% of portfolio.

- AMD (AMD) from 2.75% to 2% of the portfolio.

- Nvidia (NVDA) from 2.5% to 2% of the portfolio.

- Microsoft (MSFT) from 3% to 2.5% of the portfolio.

- Albemarle (ALB) from 4% to 3.5% of the portfolio.

ETF Model

- Reduce SPDR Technology ETF (XLK) by 2% of the portfolio.

April 1st

“This morning we are selling 100% of JP Morgan (JPM) as higher rates, Fed tightening, and weaker consumption data suggest major retail banks may have some challenges ahead. We are holding on to Goldman Sachs for now and monitoring that position carefully. We are looking to add financial exposure in a non-bank area opportunistically. Also, we are underweight equities, and with the market overbought short-term, we will wait for a pullback to increase exposures.”

Equity Model

- Sell 100% of JP Morgan Chase (JPM)

ETF Model

- Reduce XLF by 1% of the portfolio

Lance Roberts, CIO

Have a great week!

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.