-

Man GLG’s Cole says markets are pricing in ‘almost no landing’

-

S&P 500 below 3,000 would reflect cyclical risks, he says

US stocks need to drop by more than a quarter from current levels to adequately reflect the looming slowdown in economic growth and company earnings, according to Man GLG.

Markets are pricing in a “spectacularly dovish, glass-half-full view of the world,” Edward Cole, managing director and co-portfolio manager for equity solutions at Man GLG, said in an interview in London. “The way equity assets are priced implies a scenario of immaculate disinflation without any landing at all.” Man GLG is one of the investment divisions of Man Group Plc.

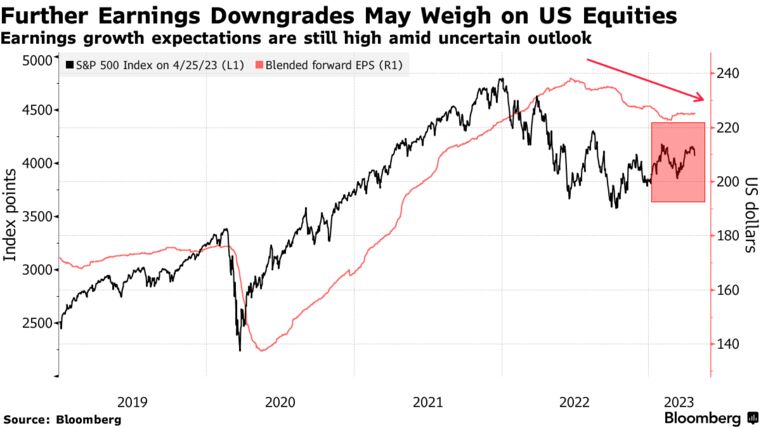

The S&P 500 index should be trading at or below 3,000 points in order to reflect cyclical risks, with slowing macro momentum expected to feed through into earnings over the coming months, he said. The US benchmark closed Tuesday at 4,072, while analysts see companies in the index earning an aggregate $218 a share this year.

“My expectations for a proper hard landing is for S&P 500 earnings per share to be below $200,” Cole said.

The S&P 500 is up 6.1% this year, with optimists expecting the US to weather a recession, and buoyed by a better-than-expected first-quarter earnings so far. The gauge remains in the green despite turmoil in the banking sector, sparked by the collapse of Silicon Valley Bank — a risk that strategists didn’t see coming.

“The balance of probabilities is against a soft landing but we are priced for almost no landing,” Cole said. Markets are pinning too much hope on a Chinese economic rebound and the possibility of US interest rate cuts, he said.

He’s not the only pessimist around, with Morgan Stanley’s Michael Wilson saying this week that a rally for US stocks in the run-up to the earnings season has added to the bearish outlook. A Bloomberg News analysis of US recessions since 1929, meanwhile, suggests it’s a question of when, not if, the stock market takes a tumble.

Cole oversees research for various equity portfolios at Man GLG and doesn’t run specific funds, according to the firm. The euro-denominated Man GLG European Equity Alternative fund, which focuses on companies that are listed in Europe or get a substantial portion of their revenues in the region, has lost 0.6% this year through Monday, according to the firm’s website, after losing 2.5% in 2022. The company declined to comment on performance.

While the fund isn’t managed with reference to a benchmark, the Stoxx Europe 600 Index has returned 11% this year including dividends, having shed 9.9% in 2022.

Data due this week on US first-quarter gross domestic product will give more clues into how the economy is holding up after a year of elevated inflation and energy prices. The data is expected to show consumer spending got off to a solid start for the year. It’ll also likely confirm that inflation remains too high, potentially pointing to higher-for-longer rates.

“The shoe that’s probably left to drop this year is how and when deceleration of macroeconomic momentum in developed markets translates into an earnings slowdown,” Cole said.

Written by: Sujata Rao-Coverley and Ksenia Galouchko @Bloomberg.com

The post “Fund Manager Man GLG Says Stocks Need to Fall 26% to Reflect Looming Economic Slowdown” first appeared on Bloomberg.com

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.