- Wall Street prime brokers say clients ramped up short selling

- Bears benefit as the most-shorted stocks led the market rout

As the cross-asset selloff engulfed Wall Street last week, hedge funds ramped up their bets against stocks while one measure of their market positioning plunged the most since the March 2020 crash.

From retail investors to rules-based systematic traders, appetite for equities is subsiding after a 20% rally this year that’s fueled by euphoria over artificial intelligence.

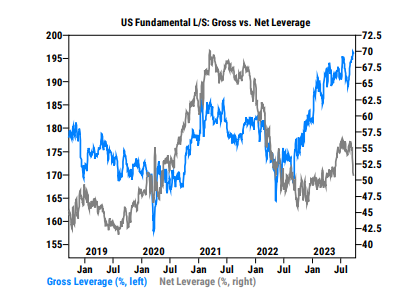

Fast money investors increased their bearish wagers to drive down their net leverage — a gauge of risk appetite that measures long versus short positions — by 4.2 percentage points to 50.1%, according to Goldman Sachs Group Inc.’s prime brokerage. That’s the biggest week-on-week decline in portfolio leverage since the depths of the pandemic bear market.

At the same time, short selling rose at hedge funds tracked by JPMorgan Chase & Co., while Morgan Stanley’s clients cut their net leverage at a pace not seen since last October.

Fueling the latest bout of pessimism is the resolve by the Federal Reserve to keep interest rates higher for longer — creating pressure on already stretched market valuations. At the peak in July, the S&P 500 was traded at 20 times forecast profits, a multiple that’s 27% higher than the two-decade average.

“Client activity has been reflexive, as lower prices have been met with significant de-risking from the trading community and the loss sponsorship from the retail community,” Tony Pasquariello, Goldman’s head of hedge-fund coverage, wrote in a note. “While I’m a believer in the durability of US growth and the exceptionalism of US mega cap tech, from today’s levels it is hard for me to get excited about either the ‘E’ or the ‘PE’ into next year.”

A drop in net leverage means the so-called smart money is taking a less bullish stance on equities. Another measure of hedge fund risk appetite is gross leverage, which adds up both long and short positions. That gauge can go in the opposite direction of the net measure when shorts rise — as is the case now. A short-driven build up in gross leverage means hedge funds are increasingly leaning against the stocks and they’re doing it with high conviction.

Stocks swung between gains and losses on Monday after S&P 500’s worst weekly slide since the banking turmoil in March. Down almost 6% from its 2023 high in late July, the benchmark index now hovers near a three-month low.

To investors who have watched 2023’s equity rally starting to lure the gambling crowd, the return of skepticism is perhaps welcome news if it prevents the market from running too hot. If anything, defensive positioning can set the stage for a bounce, as happened last October. Timing that recovery, however, is not easy.

As a group known for making bold wagers in the market, hedge funds took advantage of the pullback to raise their stakes. Last week, the dollar amount of their net selling reached the highest level since January 2022, Goldman data shows. At Morgan Stanley, clients boosted shorts against expensive technology shares, consumer retail and AI beneficiaries.

A Goldman basket of the most-shorted stocks is down more than 10% this month, handing bears with handsome profits.

“Short additions were concentrated in already shorted sectors,” Morgan Stanley’s team including Christopher Metli wrote in a note. “Positioning was also a clear driver of price action.”

Yet JPMorgan’s analysis shows that the cohort’s overall performance has not held up as it did during the turbulence in August. At this point last month, the group’s monthly return was flat, while the market was in deep in red. Now, they’re down 1.8% in September amid a broad selloff on a similar scale. That’s mostly because their long positions have failed to generate above-market returns, or alpha, according to the team including John Schlegel.

“The risk is that this potentially goes in reverse and puts more pressure on performance, either via longs sold if the market continues to weaken or via shorts covered if the market snaps back quickly,” they wrote. “The best environment (for alpha) is likely one where the market remains range-bound and the macro backdrop appears supportive, but not too hot.”

Written by: Lu Wang and Denitsa Tsekova @Bloomberg.com

The post “Hedge Funds Cut Stock Leverage at Fastest Pace Since 2020 Crash” first appeared on Bloomberg.com

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.