In October, the markets were down 10% from the July high, bond yields were touching 5%, and talk of a coming recession was rampant. What happened?

Interestingly, a Wall Street axiom says, “Sell the last Fed rate hike.” The reason is that when the Fed starts cutting rates, it is due to the onset of a recession, a bear market, or a financial event. At that point, as shown below, the markets are repricing for lower expectations of earnings growth rates and profitability.

As Michael Lebowitz noted previously in “Federal Reserve Pivots Are Not Bullish:”

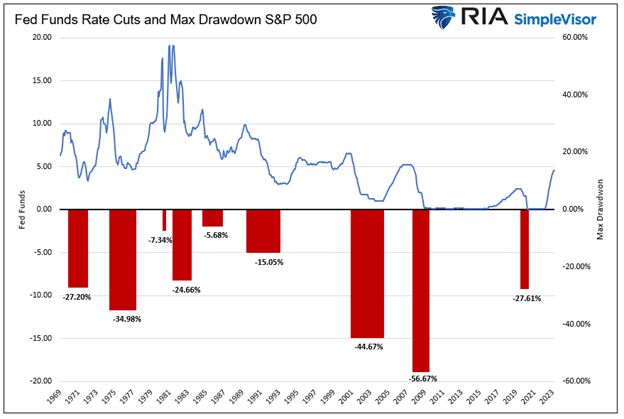

“Since 1970, there have been nine instances in which the Fed significantly cut the Fed Funds rate. The average maximum drawdown from the start of each rate reduction period to the market trough was 27.25%.

The three most recent episodes saw larger-than-average drawdowns. Of the six other experiences, only one, 1974-1977, saw a drawdown worse than the average.”

Given that historical perspective, it certainly seems apparent that investors should NOT be anticipating a Fed rate-cutting cycle. Such should, in theory, coincide with the Fed working to counter a deflationary economic cycle or financial event.

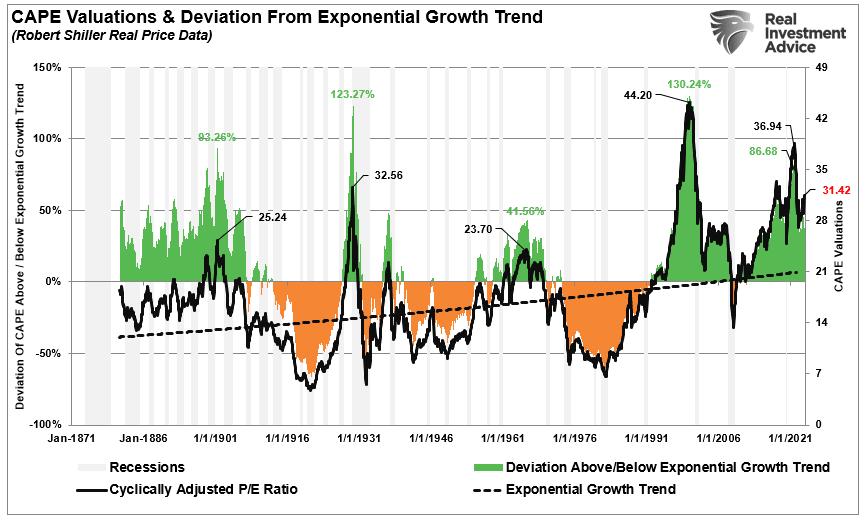

Yet, since the beginning of November, the markets have risen sharply in anticipation of the Fed cutting rates as soon as the first quarter of 2024. More interestingly, the worse the economic data is, the more bullish investors have become looking for that policy reversal. Of course, in reality, weaker economic growth and lower inflation, which would coincide with a rate-cutting cycle, do not support currently optimistic earnings estimates or valuations that remain well deviated above long-term trends.

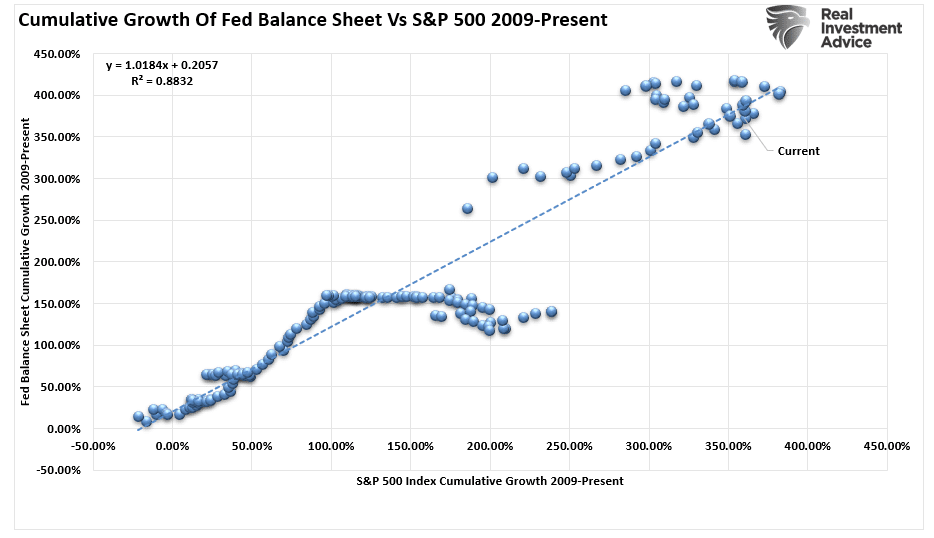

Of course, that deviation of valuations has been the direct result of more than $43 Trillion in monetary interventions since 2008, which has trained investors to ignore the fundamental factors.

Has Pavlov’s Experiment Trained Investors

Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g., food) is paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when the neutral stimulus was introduced, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

In 2010, then Fed Chairman Ben Bernanke introduced the “neutral stimulus” to the financial markets by adding a “third mandate” to the Fed’s responsibilities – the creation of the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

– Ben Bernanke, Washington Post Op-Ed, November, 2010.

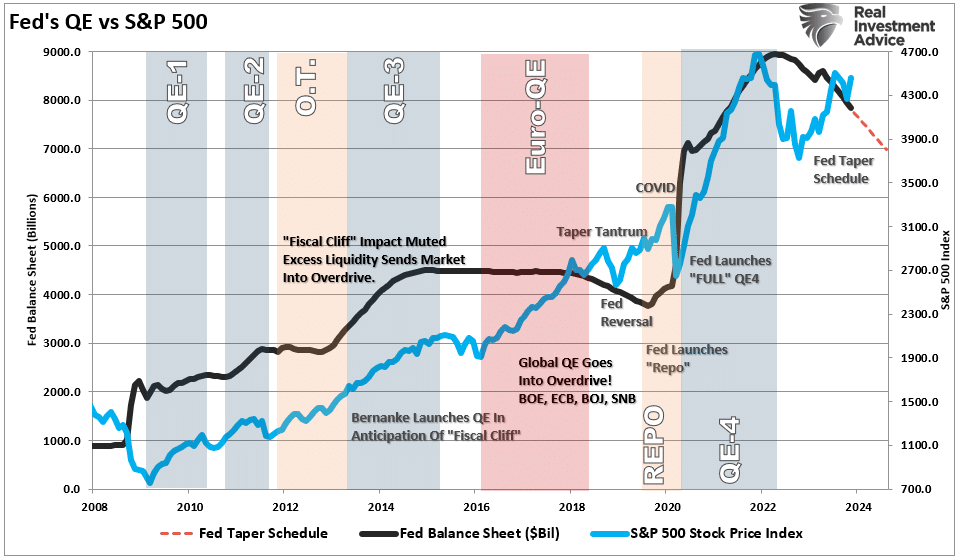

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must be followed by the “potent stimulus” for the “pairing” to be completed. For investors, as each round of “Quantitative Easing” was introduced, the “neutral stimulus,” the stock market rose, the “potent stimulus.”

While there has been previous debate on the impact of the Fed’s balance sheet changes on the markets, there is a very high correlation between the two, suggesting it is more than just a coincidence.

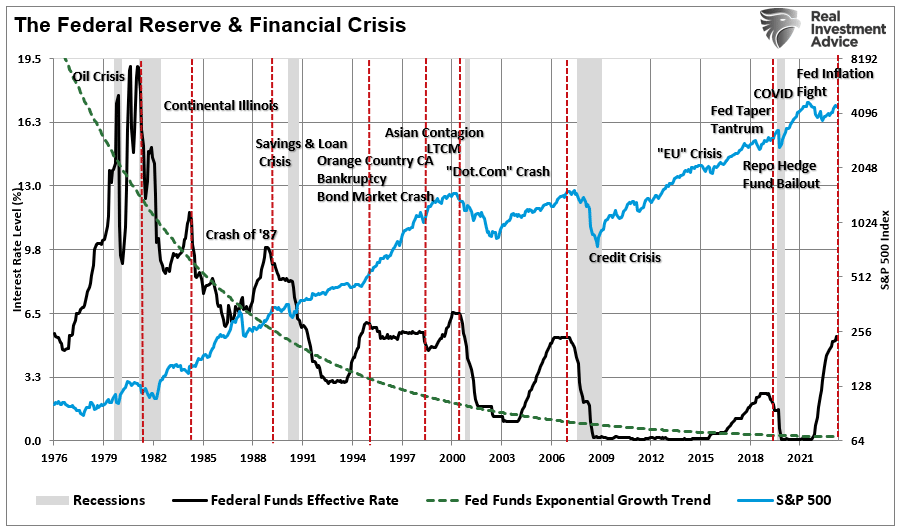

Notably, before 2008, there was clear evidence that markets repriced lower when the Fed began a rate-cutting cycle. Such was because the realization of a financial event created selling pressure in the market. Stocks historically fell until that rate-cutting cycle was over and the catalyzing event was resolved.

However, since 2008, the Fed has trained investors. Any financial or recessionary event jeopardizing the markets would be met with rate cuts and accommodative policy. That training was completed with the Fed’s response to the “pandemic-era shutdown” that led to massive monetary and fiscal interventions.

There is currently a large contingent of investors who have never seen an actual “bear market.” For many investors in the markets today, their entire investing experience consists of continual interventions by the Federal Reserve. Therefore, it is unsurprising investors are fully trained to “fear of missing out” on the next round of Fed support.

Are Investors Front-Running The Fed?

We have previously discussed the many economic indicators suggesting a recession is possible. However, one has yet to manifest itself, and economic growth has continued to defy tight monetary policy. Subsequently, investors have now concluded that a recession will be avoided, the Fed will cut rates, and stocks will rise.

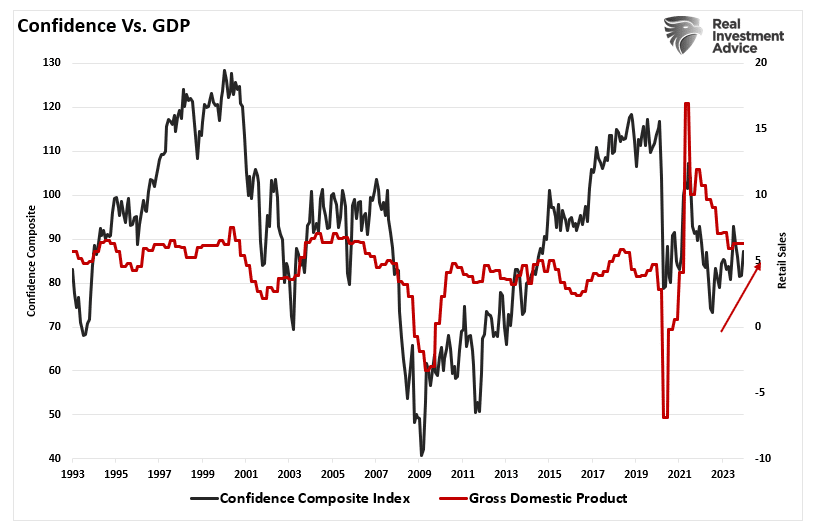

The market’s increase since November has the knock-off effect of boosting consumer confidence. As noted in Ben Bernanke’s quote, the result should be increased economic activity to keep the economy out of recession. The chart below is the consumer confidence composite index as compared to GDP.

Note the increase in consumer confidence since the lows of October 2022. The question becomes, has the expected market decline from a Fed rate hiking cycle already completed? In the linked article above, Michael Lebowitz tackled that question. He used a Wicksellian model to estimate the expected percentage drawdown during a Fed rate hiking cycle. To wit:

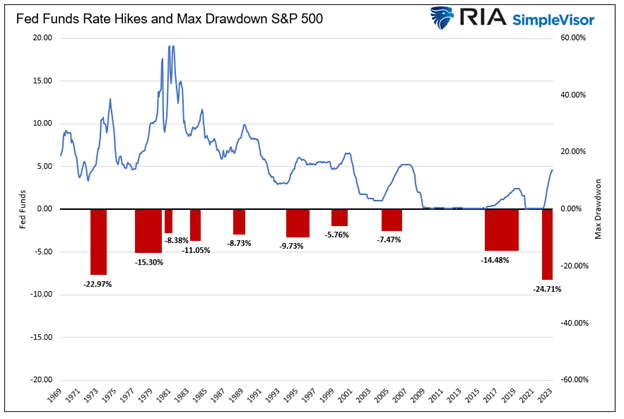

“The graph below shows the maximum drawdown from the beginning of rate hiking cycles. The average drawdown during rate hiking cycles is 11.50%. The S&P 500 experienced a nearly 25% drawdown during the current cycle.”

That estimate of a 24% drawdown was not far off the market’s 20% nominal drawdown in 2022. This poses an interesting question to investors who are currently expecting a further drawdown in 2024.

“Since the market experienced a decent drawdown during the rate hike cycle starting in March 2022, might a good chunk of the rate drawdown associated with a rate cut have already occurred?“

A Range Of Possibilities

Let me clearly state that I do NOT have a crystal ball for 2024. Even my “Crazy Eight Ball” replied with “outlook uncertain.”

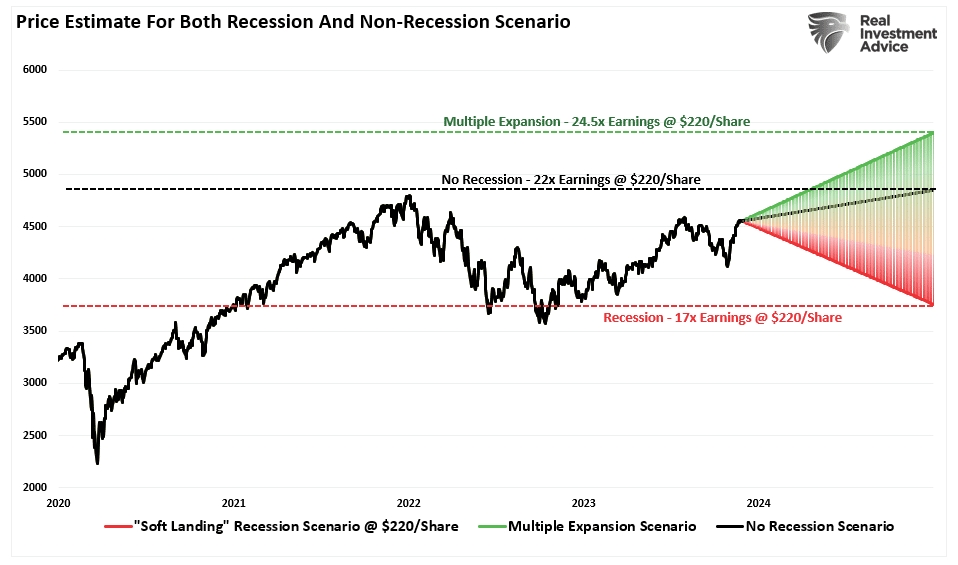

However, there are three primary possibilities for the markets we must consider.

- The Fed cuts rates and navigates a soft landing, stabilizing earnings growth, and the markets price higher on easier monetary policy and reversing “Quantitative Tightening” or “QT.”

- Due to increased asset prices and consumer confidence, economic activity picks up, and the Fed remains on hold over concerns about a resurgence of inflationary pressures. The markets reprice modestly to accommodate for a drag on economic growth, but recession fears are dismissed.

- A financial event and a recession occur due to the current restrictive level of monetary policy, and even though the Fed drastically cuts rates and reverses QT, stocks reprice lower due to a drop in earnings growth.

These possibilities are the drivers behind the range of potential outcomes discussed last week.

Using history as a guide, the many voices suggesting more bearish outcomes for 2024 seem logical. However, we must consider the impact of the Fed’s decade-long training of investors to “buy monetary policy changes.”

It may not make logical or fundamental sense. However, we must remain open to the possibility that markets are front-running the eventual Fed’s “ringing of the bell.”

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.