- Narrative around economic growth has changed since 2015

- Reluctance to use big stimulus makes lifting confidence hard

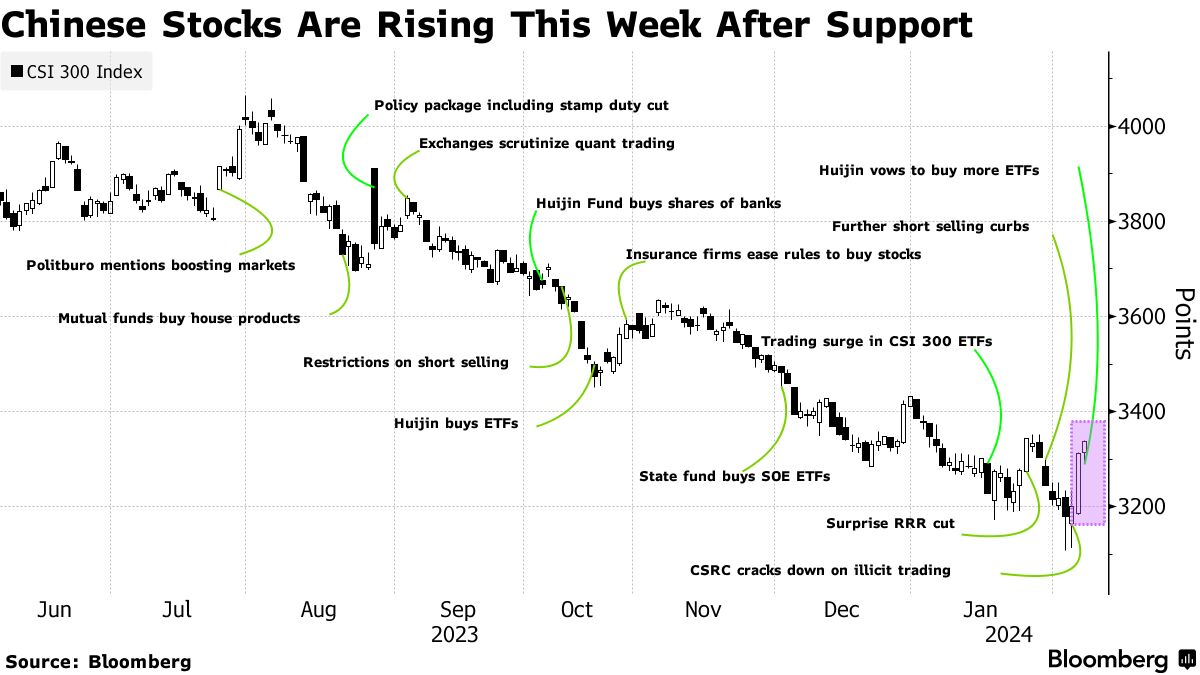

China’s efforts to arrest a $7 trillion stock market rout are evoking memories from 2015, when Beijing took drastic steps to stem a crash. This time, investors say, the problems are much more entrenched.

Authorities have snapped into crisis mode to support China’s tumbling markets, taking aim at short-sellers and freeing up cash for banks, while state funds are boosting purchases. Signaling the growing alarm, China abruptly ousted its market chief Yi Huiman on Wednesday, rolling out another hallmark of the near decade-old blueprint to boost stocks.

“The shuffle demonstrates that the political impulse remains to tighten administrative controls rather than address fundamental problems facing the economy,” Eurasia Group analysts wrote in a note after the surprise shake-up. Rather than helping, they wrote, “it entrenches the sense of malaise and weighs on confidence.”

The move came as President Xi Jinping was set to be briefed by regulators on financial markets, prompting a knee-jerk rally on bets of more forceful moves to halt a rout that earlier this week had outstripped a $6.8 trillion selloff that began in mid-2015.

Back then, Xi personally ordered an unprecedented campaign to protect the interests of small and mid-level investors. While some of the measures taken this year mirror those from the previous rout, authorities in Beijing haven’t yet responded with the same overall force. The central bank has held off making major liquidity pledges, and Xi’s economic team hasn’t pulled the trigger on a proposed 2 trillion yuan ($278 billion) rescue package.

Even if policymakers do ramp up the rescue mission, investors say the old playbook won’t be enough to satisfy questions over the long-term health of China’s slowing economy, which is being dogged by a property crisis, deflation and a shrinking population.

“The real reason why this time is different is the narrative for economic growth has changed,” said Fang Rui, fund manager at Shanghai WuSheng Investment Management Partnership. “We are now at an inflection point unseen in the past decades.”

The market turmoil is also generating veiled criticism of Xi’s government among the public and investors, after years of policy crackdowns and inflexible Covid curbs tanked business sentiment. The imminent Lunar New Year break is adding pressure to stop the rout, as the nation’s 200 million mom-and-pop investors prepare to huddle with family, potentially spreading the gloom.

While the 2015 crash also coincided with an economic slowdown and a housing market slump, China today is facing a changed policy landscape. As Xi tries to reorient the economy toward high-quality growth and away from the debt-fueled property market, top leaders have signaled they won’t lean on big stimulus.

Last time, then-Premier Li Keqiang was the most visible figure taking charge of the response. Following his return from a European trip in July that year, the government unleashed a stabilization fund, the People’s Bank of China pledged to provide ample funding to state-backed investors, and different arms of the financial universe were mobilized to support markets. Xi’s public comments didn’t come until September, months into the rout.

This time around supportive statements from Premier Li Qiang, Vice Premier He Lifeng and central bank governor Pan Gongsheng have failed to have a lasting impact. In a quarterly monetary policy implementation report released on Thursday, the People’s Bank of China said it expected consumer prices to rebound moderately as demand recovers, adding that it would step up monitoring of banking system liquidity and financial market changes.

Now some investors are waiting on word from Xi, who has consolidated power in recent years and diminished the sway of China’s No. 2 official by increasing his own influence over economic policy.

“The fact a special meeting may have been called could indicate things have gotten so bad work needs to be reported to the top,” said Xu Dawei, fund manager at Jintong Private Fund Management in Beijing. If a briefing with regulators is confirmed, he added, “I’d say with confidence this is the pivot point.”

The situation requires Xi to call for fiscal reform, according to Alicia Garcia Herrero, chief Asia-Pacific economist at Natixis SA, who noted the central bank isn’t taking the same leading role it did in 2015. Xi has weakened the PBOC in recent years, handing some of its powers to a revamped financial regulator.

If the central bank does enact looser monetary policy, it’ll also need to increase step up capital controls, she said. “If not, every single yuan they put in circulation will leave. So I’m expecting very, very strict capital controls in China, and this is very bad news for investors because they are locked in.”

Problems nearly a decade ago were also heavily driven by shadow-financed margin trading. That resulted in a quick, violent tumble as leveraged investors were forced to sell. This slump has spanned three years, as a disappointing post-pandemic reopening keeps up losses sparked by Covid disruptions.

“Market interventions cannot work over time unless underlying drivers are addressed,” said Brock Silvers, managing director at private equity firm Kaiyuan Capital. “Recent policies all seem to be treating the symptoms rather than the illness.”

While overall Chinese stocks ended the week with strong gains, some analysts still want more forceful policy to secure the turnaround.

Xin-Yao Ng, an investment director for Asian equities at abrdn, said he was skeptical of a sustainable sentiment bump without a big stimulus, citing a “perception gap” in how top leaders and market participants view China’s economy.

“Investors think the economy is really weak and don’t even believe the GDP figures,” he said. “Mr. Xi and his cabinet might still be relatively comfortable about the pace of economic growth.”

Written by: Bloomberg News — With assistance from John Liu, Yujing Liu, Colum Murphy, Rebecca Choong Wilkins, John Cheng, April Ma, Ishika Mookerjee, and Charlotte Yang @Bloomberg

The post “Xi Can’t Use 2015 Playbook to Calm China Markets, Investors Say” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.