- Oil falls from three-week high; iron tumbles on China worries

- US markets closed; S&P 500 and Nasdaq 100 futures gain 0.3%

Stocks and US equity futures were steady in muted trading as investors awaited fresh catalysts after a week that saw the S&P 500 breach new records and European equities falling just short of that mark.

S&P 500 futures edged 0.2% higher and Nasdaq 100 contracts rose 0.3%, with US cash markets shut for the President’s Day holiday. Earnings from bellwether Nvidia Corp. Wednesday could provide new impetus for equities as investors try to gauge the strength of the global economy.

The Stoxx Europe 600 was little changed following the previous week’s 1.4% surge that took the gauge to within four points of its January 2021 high. Basic resources stocks led declines after iron ore tumbled, while the technology sector also underperformed. Defensive sectors, including telecoms and health care, posted gains.

Among individual movers in Europe, AstraZeneca PLc climbed more than 3% after trial data showed its Tagrisso drug slowed disease progression in lung cancer patients. German arms manufacturer Rheinmetall AG advanced as much as 4% after announcing it will open a new plant in Ukraine. Banco Santander SA rose after kicking off a share buyback.

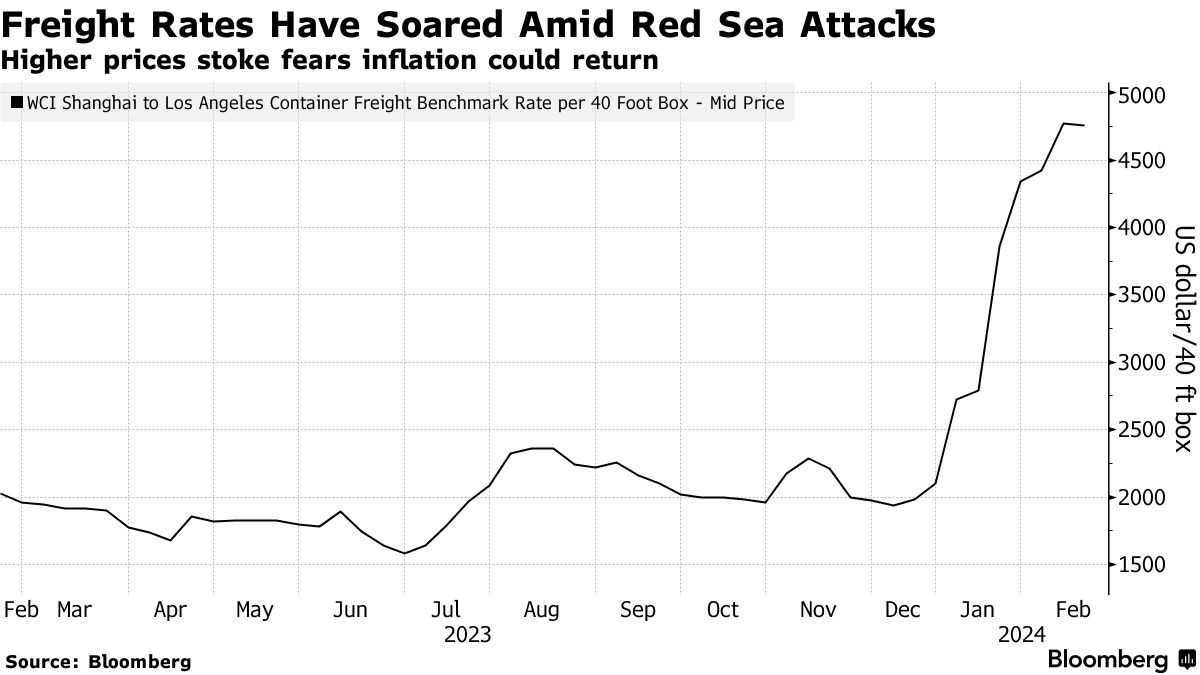

US and global stocks are yet to respond to the selloff in Treasuries this month, after a string of better-than-expected economic data and hawkish comments by policy makers drove traders to roll back aggressive bets on rate cuts. Investors also have to contend with mixed earnings, while the Middle East conflict and Red Sea shipping chaos pose major risks to the outlook for profits.

“Our base case remains that equities will end the year higher than current levels, but we do not expect it to be a straight path,” said Mohit Kumar, the chief economist for Europe at Jefferies International Ltd. “We are looking for a bit of a pull-back in the near term, which would provide better levels to reset long positions.”

Swaps are now pricing about 90 basis points of Federal Reserve rate cuts in 2024 — from more than 150 basis points at the start of February. In Europe, wagers have been whittled down to about 100 basis points, from 150.

For JPMorgan Asset Management, US stocks are priced for perfection amid “healthier” market momentum since the beginning of the year.

“Markets have adjusted to the idea that rate cuts would come later and probably be less important than what was originally priced,” Vincent Juvyns, global market strategist, said on Bloomberg Television. The move upward are also “really driven by decent earnings growth that we have seen during the fourth quarter,” he added.

This week, traders will be keeping an eye on European inflation data as well as earnings from Nvidia and mining giants BHP Group Ltd and Rio Tinto Plc. Meantime, conflict in the Middle East is set to drag on as negotiations aimed at securing an Israel-Hamas cease-fire and the release of hostages haven’t progressed as hoped, Qatar’s foreign minister said.

Bond markets were muted, with no cash trading of Treasuries due to the US holiday. They fell on Friday, with two-year yields up seven basis points to 4.65% after the producer price index rose on a sizable jump in costs of services. The greenback weakened against most of its Group-of-10 peers.

China Reopens

Elsewhere, a gauge of Asia-Pacific shares ticked upwards and was set to climb for a third session. China mainland benchmark CSI 300 Index rebounded from earlier losses in the first day of trading after the Lunar New Year break. The stocks had struggled in the early hours despite buoyant travel and tourism data that suggested consumption revved up even as the broader economy struggles with deflation and a property crisis.

Traders are now looking for further policy support across China’s monetary and fiscal space, in addition to a cut in the reserve requirement ratio already undertaken. Chinese Premier Li Qiang on Sunday called for “pragmatic and forceful” action to boost the nation’s confidence in the economy.

In commodities, oil slid from the highest level in three weeks as lingering concerns over the demand outlook offset ongoing Middle East tensions. Gold held a two-day gain. Concerns over China’s economy also led iron ore to slump after five days of gains.

Some of the key events this week:

- Reserve Bank of Australia Feb. meeting minutes, Tuesday

- China loan prime rates, Tuesday

- BHP Group Ltd earnings, Tuesday

- European Central Bank publishes euro-area indicator of negotiated wage rates, Tuesday

- Rio Tinto Plc earnings, Wednesday

- Eurozone consumer confidence, Wednesday

- Nvidia Corp earnings, Wednesday

- Federal Reserve Jan. meeting minutes, Wednesday

- Atlanta Fed President Raphael Bostic speaks, Wednesday

- Eurozone CPI, PMI, Thursday

- European Central Bank issues account of Jan. 25 meeting, Thursday

- Fed Governor Lisa Cook, Minneapolis Fed President Neel Kashkar speak, Thursday

- China property prices, Friday

- European Central Bank executive board member Isabel Schnabel speaks, Friday

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 3:49 p.m. New York time

- Nasdaq 100 futures rose 0.3%

- The MSCI Asia Pacific Index rose 0.1% to the highest in about 22 months

- The MSCI Emerging Markets Index was little changed

- S&P/TSX Composite Index rose 0.2% to the highest in about 22 months

- Ibovespa Brasil Sao Paulo Stock Exchange Index rose 0.2%, climbing for the third straight day, the longest winning streak since Dec. 27

- S&P/BMV IPC rose 0.6%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at $1.0778

- The British pound was little changed at $1.2597

- The Japanese yen was little changed at 150.15 per dollar

- The offshore yuan was little changed at 7.2124 per dollar

- The Canadian dollar was little changed at 1.3491 per dollar

- The Mexican peso rose 0.1% to 17.0362 per dollar

Cryptocurrencies

- Bitcoin was little changed at $51,894.65

- Ether rose 3.2% to the highest in more than 21 months

Bonds

- The yield on 10-year Treasuries was little changed at 4.28%

- Germany’s 10-year yield was little changed at 2.41%

- Britain’s 10-year yield was little changed at 4.11%

Commodities

- West Texas Intermediate crude rose 0.1% to the highest since Nov. 6

- Spot gold rose 0.2% to $2,017.21 an ounce

Written by: Robert Brand — With assistance from Charlotte Yang and Tassia Sipahutar

The post “Stocks Pause Near Record as Traders Await Catalyst: Markets Wrap” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.