- Says L’Oreal is fundamentally ‘good company’ but expensive

- Carmignac fund is long Adidas, Prada and short Nike, Burberry

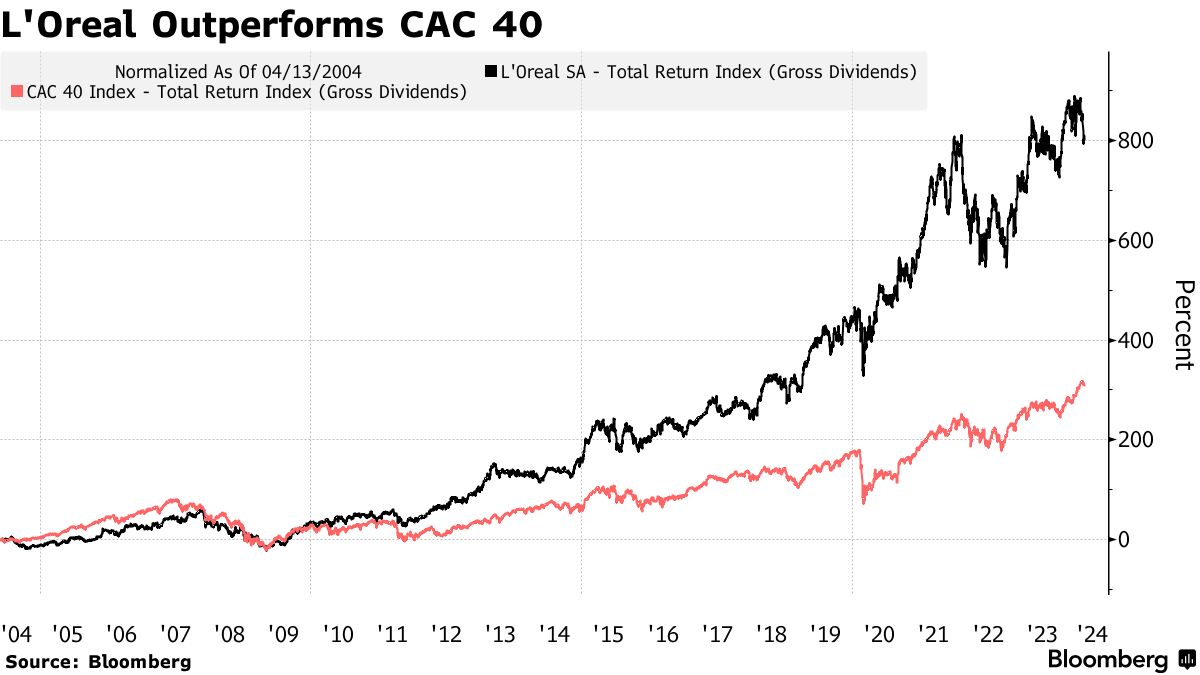

French cosmetic giant L’Oreal has returned close to 12% annually for the past 20 years, but Malte Heininger, manager of Carmignac’s Long-Short European Equities Portfolio, is now betting against it.

Heininger, whose fund is beating 97% of peers year-to-date, said he saw a crack in L’Oreal’s equity story in February when the French cosmetic giant reported fourth-quarter sales that disappointed the market. While the owner of beauty product brands Lancome and Garnier typically beats earnings expectations, the miss reflected a decline in shopping by Chinese travelers.

“Basically, we just think organic growth is decelerating,” Heininger said. “It’s fundamentally a good company but it’s very expensive.”

Short-sellers typically borrow stocks and sell them, hoping to buy them back later at a discount and pocket the difference.

Heininger expects margin pressure and little relief from Chinese and US consumers, saying analysts’ expectations were likely to be cut. The stock trades at 32 times estimated 12-month forward profits and has fallen 7% year-to-date, losing its spot as the second most-valued company in the French blue-chip CAC 40 index to luxury group Hermes.

It has 13 buy ratings, 12 holds and five sells, according to data compiled by Bloomberg. The number of shares out on loan, an indication of the proportion of investors betting against it, is just 0.2% of the free float, according to S&P Global Market Intelligence.

L’Oreal declined to comment.

Arbitrage Opportunity

So far, macro-economic trends don’t look like they will be the driver for equities in 2024, Heininger said, arguing it’s an opportunity to engage in arbitrage between stocks without taking a bet on the market or an industry.

“We long Adidas, we short Nike, we’re long Prada, we’re short Burberry,” Malte explained, adding that he was also selling auto suppliers such as Forvia and Valeo while backing Mercedes Benz.

Taking opposite bets on stocks, sometimes within the same sector, paid off so far for the Carmignac fund, which has about €560 million under management. It beat 79% of its peers over 12 months and 69% over three years.

In tech, the fund is long on SK Hynix, which it thinks will benefit from demand for memory semiconductors due to the boom in artificial intelligence, but is short on Aixtron, AMS Osram and Grifols.

Written by: Julien Ponthus @Bloomberg

The post “A French Fund Manager Beating 97% of Peers Is Shorting L’Oreal” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.