Avoiding a climate catastrophe is often portrayed as a question of political will. Yet the push to reduce carbon emissions is also a daunting technical and societal challenge. Retooling power and transportation systems to run on renewable energy will require far more copper than the companies that produce it are currently committed to deliver.

The question is whether a traditionally cautious mining industry — grappling with increasingly rigorous regulations — will embrace the scale of investment needed to rewire the world. In an indication of how difficult it is to develop new copper projects, BHP Group Ltd. has proposed a $39 billion takeover of Anglo American Plc, part of a larger trend of mergers and acquisitions as metal producers look to buy rather than build production growth. Failure by the industry to deliver sufficient copper supplies could throw the transition to cleaner power sources off course.

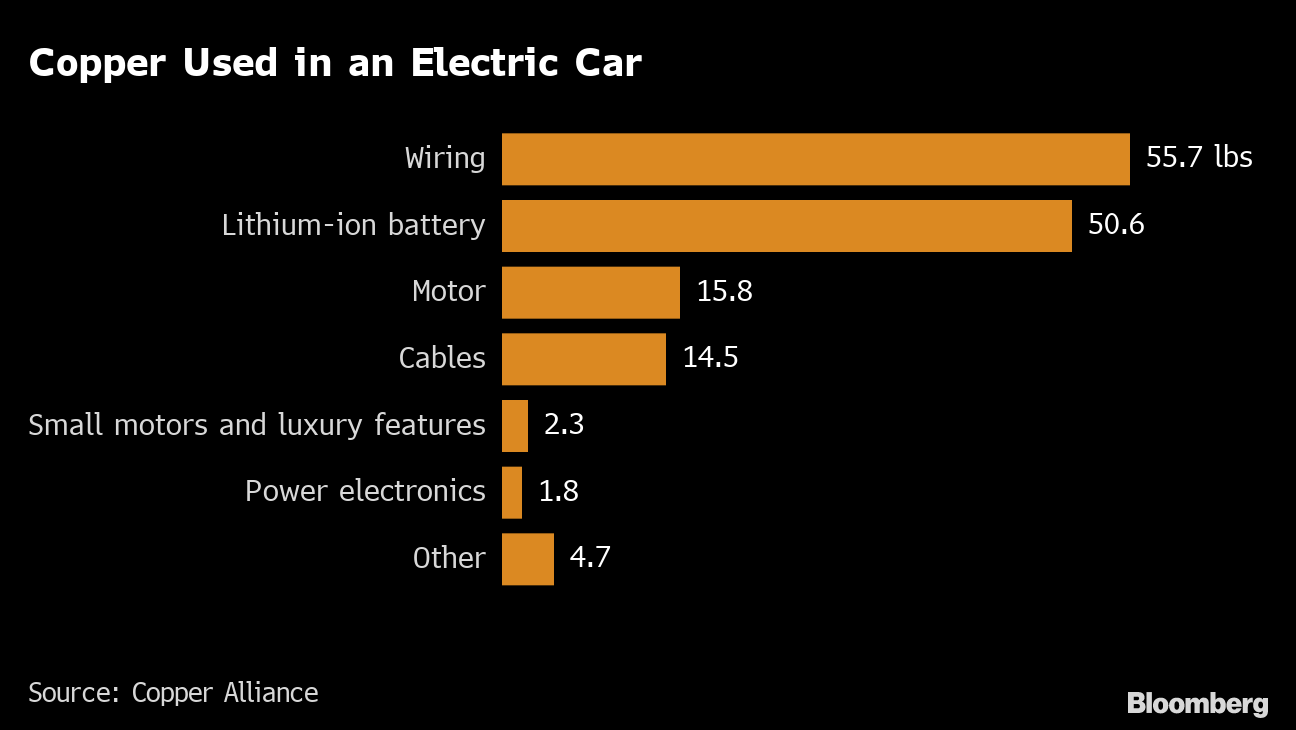

Copper’s role in the energy transition

Copper is the most conductive metal after silver. While it’s expensive, using cheaper alternatives like aluminum means compromising on efficiency. You can find copper in products as varied as toasters, air conditioners and microchips. There are about 65 pounds (29 kilograms) of it in the average car and more than 400 pounds in the typical home. Millions of feet of copper wiring are needed to build the more complex grids that can handle electricity produced by decentralized renewable sources and balance out their intermittent supplies. Solar and wind farms, often spread out over large areas, require more copper per unit of power produced than do centralized coal- and gas-fired power stations. Electric vehicles use more than twice as much copper as gasoline-powered cars do, according to the Copper Alliance.

Achieving net-zero carbon emission targets would likely entail a doubling of annual copper demand by 2035 to 50 million metric tons, according to an industry-funded study by S&P Global. Even the more conservative forecasters see demand growing by a third over the next decade, as governments and businesses step up investments in decarbonization. It’s far from certain that this much of the red metal will become available.

Why supplies could fall short

Although more copper is being recycled, it won’t be enough to cover demand, so the only alternative is to dig more out of the ground. There’s plenty down there, and the industry has responded to demand surges in the past. But there are also numerous obstacles to meaningfully boosting output.

Copper is a classic bellwether of the global economy – rising and falling in tandem with industrial production – and miners are cautious about ramping up capacity for fear of getting caught out by a drop in demand. Added to this is a deeper, more structural problem: New deposits are getting harder, and costlier, to extract as ore grades fall, meaning more rock needs to be mined to secure the same amount of metal. Growing scrutiny of the environmental costs of copper mining is also discouraging more investment.

A recent rally in prices has traders and executives wondering if copper is starting to react to a looming supply squeeze. Goldman Sachs Group Inc. estimates that the industry needs to spend $150 billion over the next decade to address a projected annual supply shortfall of 8 million tons. To trigger that kind of outlay, mining companies would need prices to rise to record levels, according to Trafigura Group and BlackRock Inc.

How countries are jostling to secure supplies

Much as oil dictated the geopolitics of the last century, access to copper is becoming an economic imperative in this one, with governments jostling to secure those limited future supplies. Most copper ore is mined in Latin America and Africa and processed locally to create a more concentrated product, which is then exported to other nations where it’s smelted to create pure copper.

China has compensated for its poor domestic reserves by snapping up mines overseas and building out massive smelting capacity domestically. Though excess capacity in China has helped reduce smelting fees to unprecedented levels, the US and its allies are uneasy with Beijing’s sway over such a strategic industry and are looking to source and refine more of the metals needed for the energy transition at home or in friendly nations.

With so many eager buyers, major producers such as Chile, Peru and the Democratic Republic of Congo have more opportunity to dictate the terms of trade. Communities in mining regions are pushing for more social benefits from mine projects and calling on miners to do more to mitigate the environmental damage.

Copper is extracted from ore using chemicals that can enter groundwater, contaminate farmland, kill wildlife and pollute drinking water. The amount of waste rock that’s left over after copper ore is processed is set to grow from an annual rate of 4.3 billion ton in 2020 to 16 billion ton in 2050, according to researchers at the University of Queensland in Australia. Safely storing this byproduct, which needs to be managed carefully to avoid slumps and landslides, could cost the industry an additional $1.6 trillion, the researchers estimated.

What if copper falls short

Severe copper shortages would cause a surge in prices that risks damaging the economics of EVs, smart grids and renewables and slowing their adoption. Manufacturers of clean-energy technologies could help themselves by finding ways to use less copper in their products. And higher prices would give miners more incentive to ramp up production. But it takes several years to develop a new mine, so even if a burst of new demand gave miners the confidence to embark on massive new investments, it would take about a decade to move the needle on output projections.

The Reference Shelf

- BHP’s proposed acquisition of Anglo American explained.

- Chile’s Chuquicamata offers a cautionary tale for an industry beset by rising costs and heightened scrutiny.

- An unprecedented squeeze in the market for copper ore fires up the bulls.

- Moves by Glencore, Trafigura show the unintended consequences of sanctions.

- A $10 Billion copper mine is now sitting idle in the jungle.

Written by: James Attwood @Bloomberg

The post “Why the World Needs More Copper — a Lot More Copper” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.