- Higher-for-longer rate settings reshape market outlook

- Guggenheim favors corporate bonds, Standard likes German bunds

Major advanced economy central banks are likely to take back less than half of the interest-rate hikes they rammed through over the past two years — an outlook reshaped significantly by US outperformance.

After the Federal Reserve, European Central Bank and Bank of England jacked up their benchmarks by a collective 1,475 basis points, only 575 basis points of reductions are in store by the end of 2025, according to new Bloomberg Economics estimates.

The latest outlook, coming after a series of disappointingly high inflation readings in the US along with better-than-anticipated economic activity, is revamping the investment landscape. It offers more time to lock in today’s relatively high yields, plus opportunities for relative-value bets as some central banks ease before others.

The Bloomberg Economics macro-yield model back in November suggested 10-year Treasuries would end this year at 4.1%. As of Thursday, it’s pointing to 4.4% — which would mark a modest drop from 4.65% now. To Ana Galvao, the Bloomberg economist who built the model, “downside surprises from the inflation releases at the end of 2023, followed by the upside surprises from February” did most to reshape the outlook.

Longer Miles

Monetary policy pivots are always hard to time, but the havoc the pandemic caused and the unprecedented, massive dose of fiscal stimulus since spring 2020 has made things all the harder, said Anne Walsh, chief investment officer at Guggenheim Partners Investment Management.

“All the historical mile markers that had been in existence in the past — for example, from the time the Fed starts hiking it’s usually 18 to 24 months to when the recession starts — have been extended,” she said.

Fed Chair Jerome Powell and his colleagues’ mission to get inflation back to 2% has been complicated by fiscal deficits that continue to come in historically large, according to Walsh at Guggenheim, which manages over $300 billion in assets. She pointed out the anomaly of big deficits at a time of sub-4% unemployment rates.

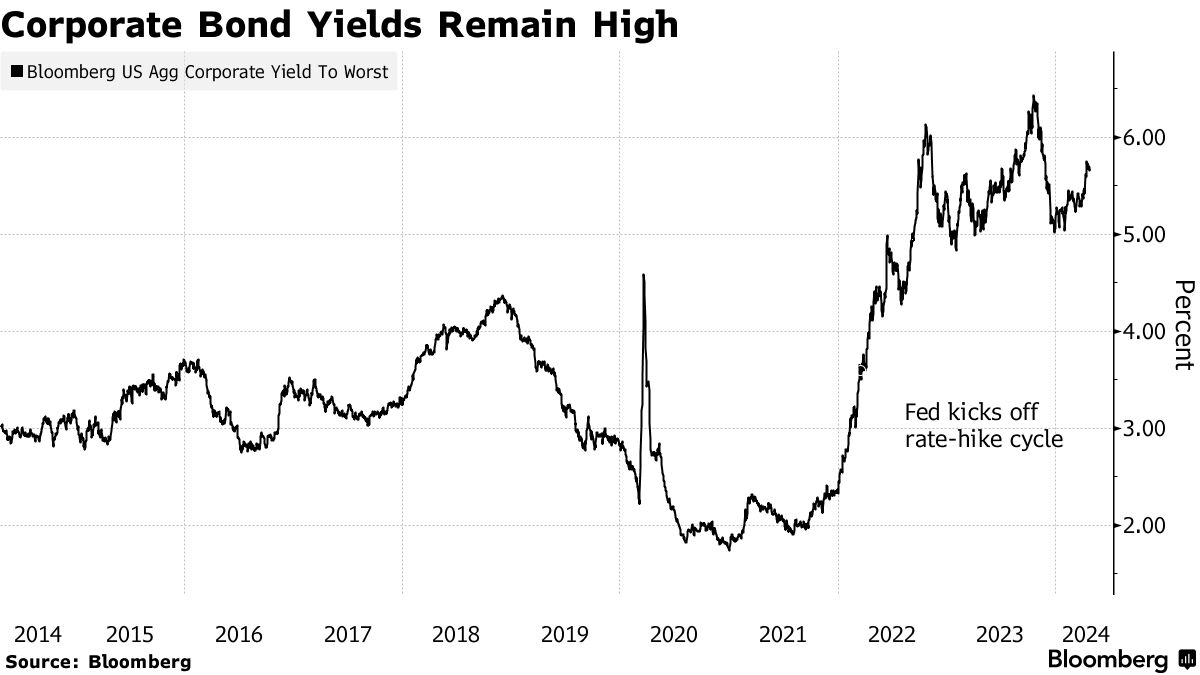

Walsh said she’s very positive on investment-grade bonds, seeing underlying credit fundamentals as good and yields at about 5.5% to 6.5% as attractive. The Bloomberg US Aggregate index yielded 5.75% as of Thursday.

Derivatives trading also shows a reshaped outlook. Only one Fed quarter point rate cut is fully priced in for this year, compared with at least five as recently as early February. Some options offer traders protection against another hike.

Rate differentials between major central banks are also on the move. On Feb. 1, markets implied that the Fed and ECB would end the year with rates at 3.97% and 2.52% respectively. As of Friday, markets saw about 4.96% and 3.20%.

Money markets in Europe show greater confidence in easing this year, with about 69 basis points for the European Central Bank and 43 basis points for the Bank of England as of Friday.

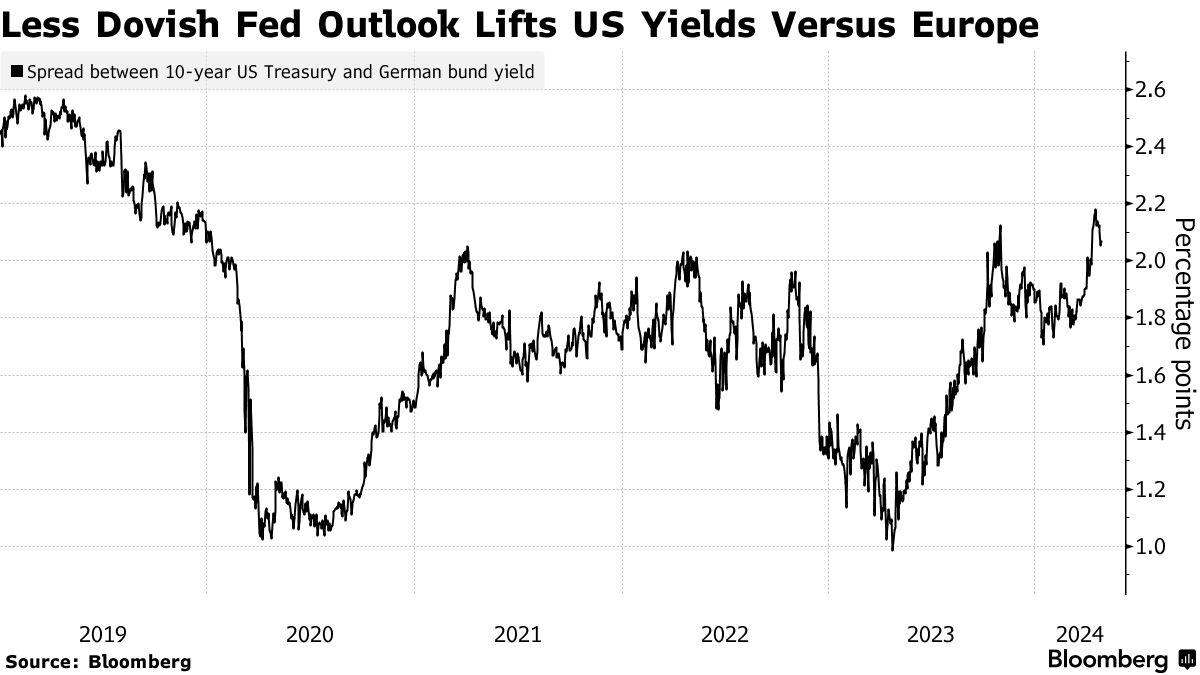

“There’s less downside risk in US rates than we see in Europe,” said Steven Barrow, the London-based head of G-10 strategy at Standard Bank. He’s telling clients to favor German bunds over US Treasuries.

Continued economic resilience — the International Monetary Fund now sees an acceleration in advanced economies this year rather than a slowdown — should allow the main central banks to keep shrinking balance sheets that had ballooned during the Covid crisis.

The Fed, ECB, BOE and Bank of Japan collectively expanded their balance sheets by a combined $9 trillion in 2020 and 2021. By the end of next year, Bloomberg Economics now sees the group as on course to conduct a cumulative amount of some $3 trillion worth of quantitative tightening over 2024 and 2025. That’s even after the Fed suggested it favors slowing the pace of QT by roughly half, starting soon.

That means private-sector investors will need to step up to absorb the supply of government debt. Higher-for-longer yields may make that an easier proposition.

For Anwiti Bahuguna, chief investment officer of global asset allocation at Northern Trust Asset Management, it’s an environment where it’s worth moving out on the credit spectrum.

Northern Trust, which oversees about $1.2 trillion, expects a maximum of two cuts from the Fed in the second half of this year, and is leaning hard into US high yield debt — anticipating the Fed will succeed in bringing down inflation without imploding the economy. Yields on the Bloomberg high-yield corporate index are above 8.2%.

“We are very neutral across every asset class except high yield,” Bahuguna said in an interview in New York. “High yield should do well as there is a high coupon buffer and growth is slowing but still strong — so default risk is low.”

Written by: Liz Capo McCormick, Enda Curran, and Scott Johnson — With assistance from Tom Orlik, Eliza Winger, Zoe Schneeweiss, and James Hirai @Bloomberg

The post “Central Banks Will Probably Cut Only Half as Much as They Hiked” first appeared on Bloomberg