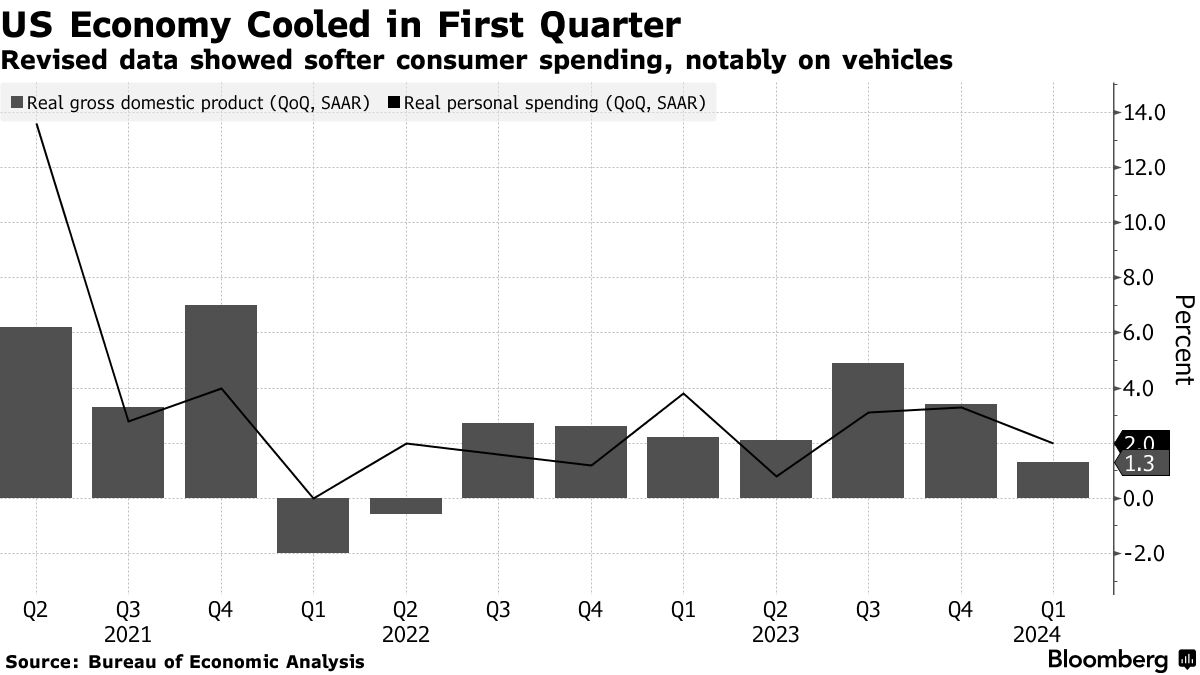

- Economy expanded at 1.3% pace versus initial estimate of 1.6%

- Consumer spending was lower on outlays for goods like autos

The US economy grew at a slower pace in the first quarter than initially reported, primarily reflecting softer consumer spending on goods.

Gross domestic product rose 1.3% annualized in the first three months of the year, below the previous estimate of 1.6%, Bureau of Economic Analysis figures published Thursday showed. The economy’s main growth engine — personal spending — advanced 2.0%, versus the previous estimate of 2.5%.

The numbers underscore a loss of momentum to start 2024 after continual upside surprises in 2023. High interest rates, waning pandemic-era savings and slower income growth are some of the key factors weighing on American households and businesses.

Consumer spending was marked down as outlays for goods — particularly autos — were much softer. Federal government spending slowed, while imports picked up compared to the first estimate. Net exports subtracted from growth for the first time in two years.

The downward revision to consumer spending was partially offset by stronger business and residential investment. A key measure of underlying domestic demand known as final sales to private domestic purchasers rose 2.8%, versus the initially reported 3.1% increase.

Economists have pointed to the strength in this metric as reason to believe that demand is still strong, even if the headline GDP figure looks weak by comparison.

“Monthly data beyond March generally point to a continued, albeit gently cooling, economic expansion. We anticipate continued GDP gains this year and a healthy advance in 2024 overall,” Nationwide Financial Markets Economist Oren Klachkin said in a note.

“Some warning signs regarding the economic outlook are visible beneath the surface, but nothing that makes us pessimistic about the road ahead.”

| Metric | Revision | Initial Estimate |

|---|---|---|

| GDP | +1.3% | +1.6% |

| Consumer spending | +2.0% | +2.5% |

| Nonresidential investment | +3.3% | +2.9% |

| Residential investment | +15.4% | +13.9% |

| Government spending | +1.3% | +1.2% |

Alongside its second estimate of GDP, the BEA also publishes data on gross domestic income, its other main measure of economic activity. GDI rose 1.5% in the first quarter, according to the report. GDP measures spending on goods and services, whereas GDI measures income generated and costs incurred from producing those same goods and services.

The GDI data include figures on corporate profits. In the first quarter, adjusted pre-tax profits fell 0.6%, the first decline in a year. After-tax profits as a share of gross value added for non-financial corporations, a measure of aggregate profit margins, were little changed at 15.2%.

On the inflation front, the Federal Reserve’s preferred metric — the personal consumption expenditures price index — rose at a 3.3% annualized rate in the first quarter, slightly down from the initial projection. Excluding food and energy, the core PCE gauge rose 3.6%, versus 3.7% in the previous estimate.

Growth in disposable personal income was marked up to 1.9% versus 1.1% initially. That may bode well for consumer spending and GDP going forward.

Economists are looking ahead to the release of monthly PCE data for April, due Friday from the BEA, after reports published earlier this month showed a stalling in growth of retail sales and a slower pace of increase in consumer prices to start the second quarter.

Fresh merchandise trade figures for April suggest little room for improvement in the second quarter. Separate data out Thursday showed the gap in goods trade last month widened to the largest since May 2022.

Meantime, initial applications for unemployment benefits were little changed in the latest week at low levels.

Written by: Matthew Boesler — With assistance from Chris Middleton, Daniel Neligh, and Jarrell Dillard @Bloomberg

The post “US GDP Growth Was Slower Last Quarter on Soft Consumer Spending” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.