- Rising imports were offset by higher exports and inventories

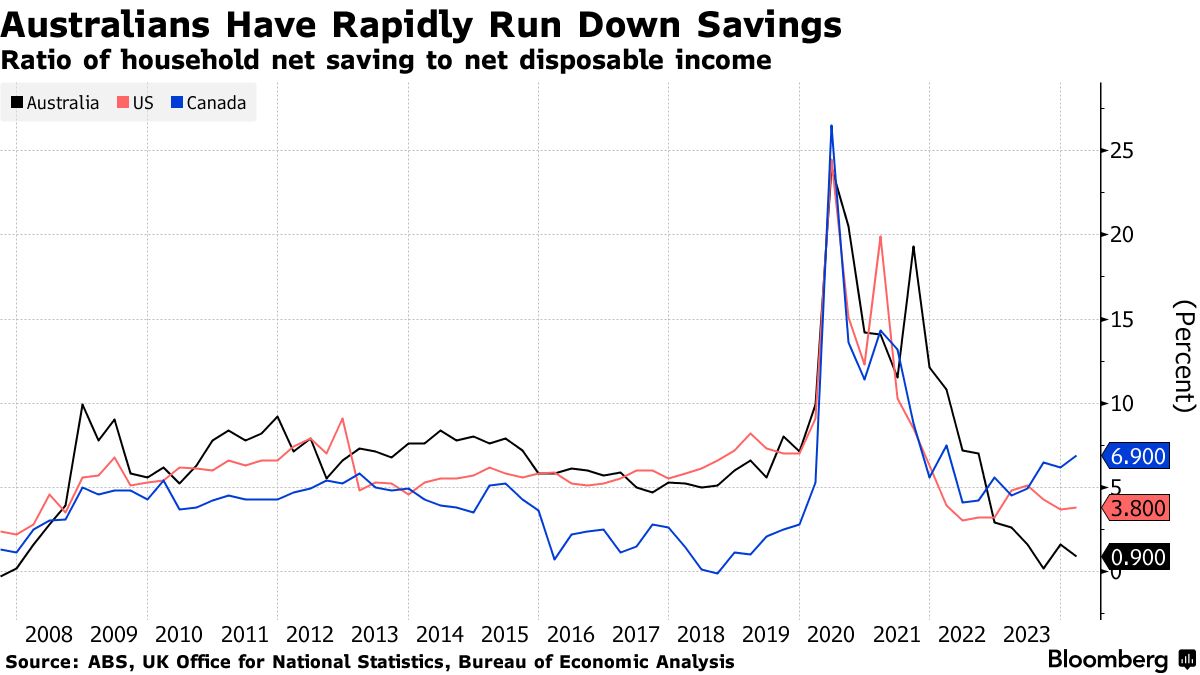

- Household savings slid to 0.9% from downwardly revised 1.6%

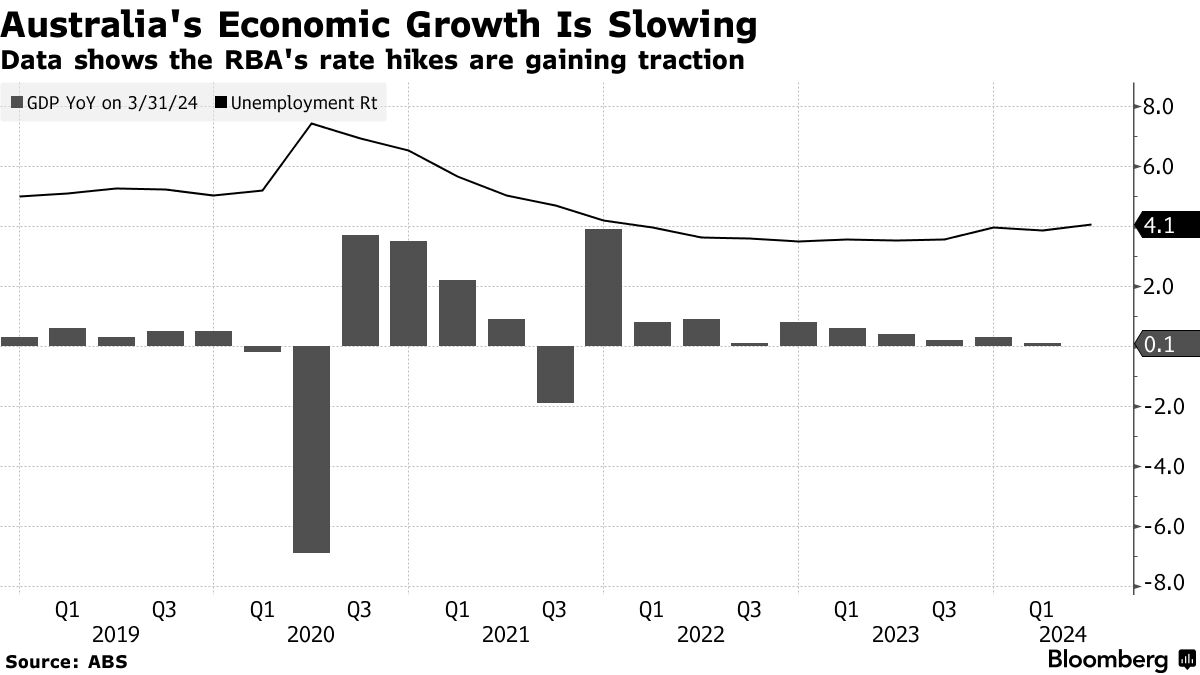

Australia’s economy all-but stalled in the first three months of the year as elevated interest rates and cost of living pressures weighed heavily on households and broader activity.

Gross domestic product rose just 0.1% from an upwardly revised 0.3% in the prior quarter and below economists’ forecast of 0.2%, government data showed Wednesday. From a year earlier, it grew 1.1%, also missing estimates.

The annual result was the weakest, outside the pandemic, since the first quarter of 1992, when Australia was emerging from a recession, and compares with a decade average of 2.4%. The slowdown will likely increase pressure on the Reserve Bank to begin an easing cycle after it held rates unchanged at 4.35% at its past four meetings.

“What is abundantly clear is that individual households, particularly those with a mortgage, are feeling the brunt of higher rates and cost of living pressures,” said Alex Joiner, chief economist at money manager IFM Investors. “Nonetheless, while inflation is uncomfortably high the RBA will judge it necessary to keep economic growth weak.”

Governor Michele Bullock reiterated earlier Wednesday that the central bank remains data-driven and isn’t ruling anything in or out. She predicted GDP would be “low,” adding that household spending in the economy is “very, very weak.” Treasurer Jim Chalmers echoes those sentiments in a later press conference, saying “overall the story of consumption is a story of weakness.”

Financial market reaction was subdued given the anemic growth was broadly in-line with expectations. Traders slightly trimmed bets on a rate cut this year to a 25% chance from a one-in-three probability prior to the release. A cut is not fully priced in until the first half of 2025.

Wednesday’s report showed household spending rose 0.4%, contributing just 0.2 percentage point to economic activity. Private business investment fell by 0.8%, driven by both mining and non-mining related spending, said Katherine Keenan, head of national accounts at the Australian Bureau of Statistics.

One area of resilience was government expenditure which added 0.2 percentage point to GDP. Economists expect the outlook for public demand to remain firm, with extra spending earmarked in the budget expected to flow over coming financial years. There also remains a large pipeline of public infrastructure projects underway.

Chalmers said the data “are another reminder of the pressures people are under,” highlighting that essential spending outpaced discretionary consumption. The household savings ratio also declined to 0.9% in the quarter from a downwardly revised 1.6%.

The slowdown comes as inflationary pressures remained stubbornly high with first-quarter figures coming in hotter than expected while price gains quickened in April.

“This isn’t an ideal situation for the RBA,” said Robert Carnell, regional head of research for Asia-Pacific at ING Groep N.V. “If growth is weakening, but inflation is beginning to rise again, it will be hard for the RBA to turn a blind eye to it and leave rates where they are.”

The RBA’s most-recent forecasts had annual economic growth troughing at 1.2% in the middle of this year, before regaining momentum. Most economists expect the RBA will begin its easing cycle later this year.

Today’s GDP data also showed:

- Strong population growth saw GDP per capita fall 0.4%, extending recent declines

- Inventories climbed as imports of consumption goods like food, clothing, electrical items and cars increased

- Services imports rose 0.7%, driven by transport services, while outbound tourism saw a second quarterly fall

Written by: Swati Pandey — With assistance from Tomoko Sato and Matthew Burgess @Bloomberg

The post “Australia Economy Almost Stalls as High Rates Hit Households” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.