- Vol-control funds and CTAs sharply cut stock exposure

- High volatility may cause more selling from systematic players

Systematic funds have offloaded more than $130 billion of global stock bets in recent weeks. Now these rules-based players threaten to take their selling to a whole new level as volatility spikes.

Strategies including risk parity, vol-targeting and trend following will dispose $70 billion to $80 billion of shares Monday, with at least $90 billion more to unwind over the next four sessions, according to estimates from Morgan Stanley’s trading team.

The warning comes on the heels of volatility-controlled or “managed risk” products offloading $103 billion worth of US shares since the middle of July and fast-money quants selling $33 billion of global equities over the past three weeks, according to a separate analysis by Nomura Securities International.

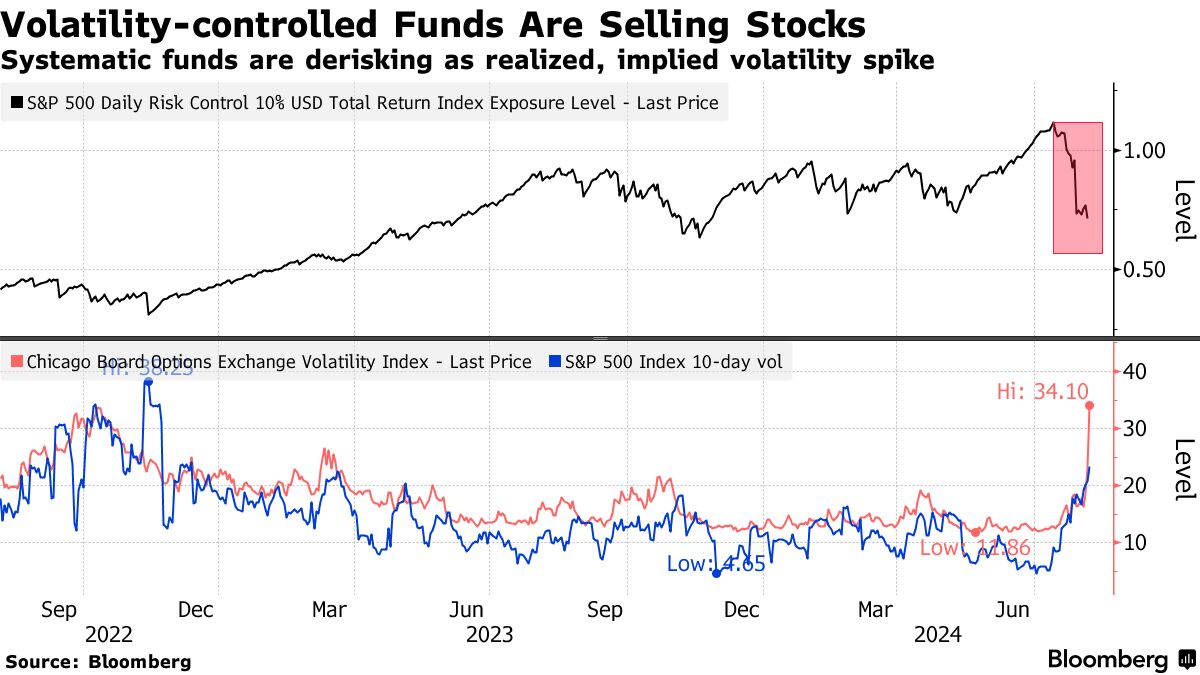

The surge in selling comes amid a jump in the VIX — also known as Wall Street’s “fear gauge” — which briefly spiked to the highest since 2020 Monday. Market watchers are already warning of a so-called volatility loop in which systematic funds are forced to further shed stocks at a frenetic pace, putting more pressure on global shares in the days and weeks ahead.

“While the VIX move may indicate vol markets are reaching max pain, the expected continuation of equity supply from systematic macro strategies is a reason to think that this selloff may have legs,” Morgan Stanley’s Amanda Goldsmith and Christopher Metli wrote in a note to client’s before the market open.

Typically driven by volatility signals, rather than fundamentals forces, these rules-based players are acutely sensitive to changes in price swings — and tend to lever up during periods of market calm while curbing their leverage when turbulence abruptly breaks out.

The decline in realized volatility for the S&P 500 before the pullback saw one class of volatility-control funds increase their allocations in equities to 110%, according to a model. That’s now tumbled to 70%.

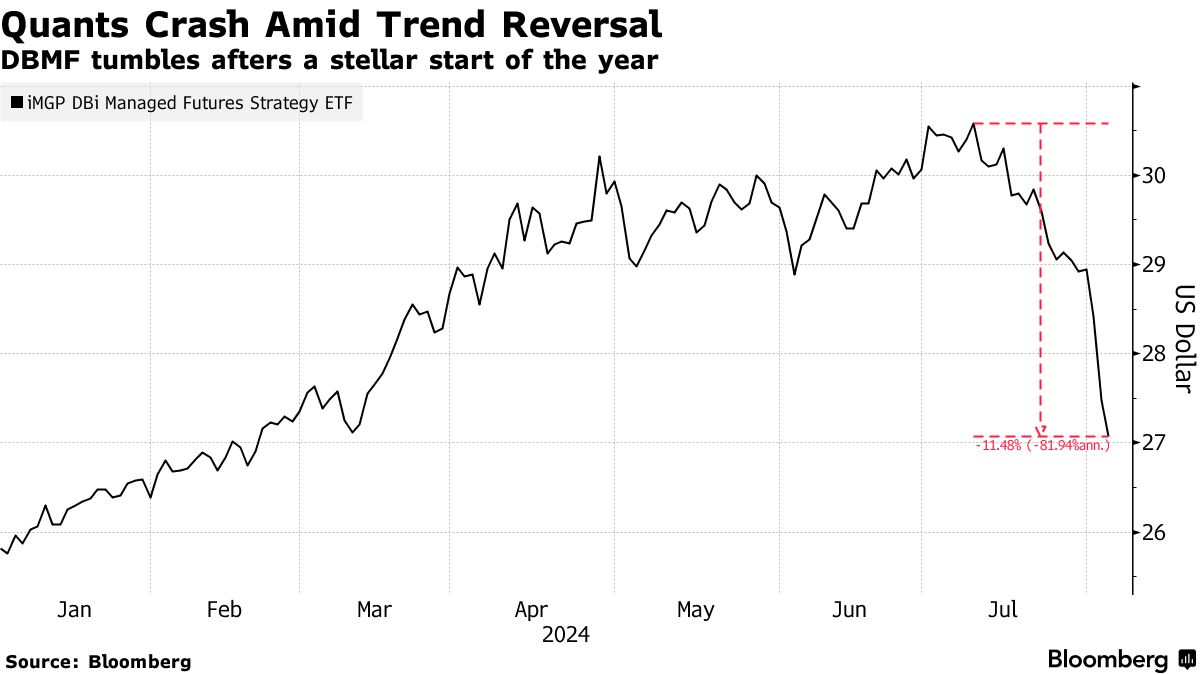

The iMGP DBi Managed Futures Strategy ETF (ticker DBMF), which touts an easy-access version of a CTA strategy and is a proxy of the industry’s exposure, has tumbled about 12% since July 10.

“Low volatility allows for accumulation of exposure,” said Charlie McElligott, a cross-asset strategist at Nomura. “This extremely long accumulation built upon the edifice of ‘low vol’ then takes only a modest vol move higher to elicit extremely large notional selling.”

The persistent buildup in equity holdings by systematic funds since October, when optimism over economic growth and artificial intelligence propelled stocks to record highs, saw the VIX remain below the widely watched level of 20 for the longest stretch since early 2018.

With the VIX spiking to nearly 66 Monday amid concerns over the Federal Reserve’s ability to avoid a recession, the fast money is rushing for the exit.

“When volatility spikes, the vol-control funds will need to sell. This selling into poor liquidity will likely lead to more volatility. This is just one of the many factors out there right now, but it is clearly having an impact,” said Chris Murphy, co-head of derivatives strategy at Susquehanna International Group.

Written by: Denitsa Tsekova and Lu Wang @Bloomberg

The post “Volatility-Rocked Quants Threaten New $170 Billion Selling Spree” first appeared on Bloomberg