- Company projects 1% to 2% revenue growth, down from 8% to 11%

- Dating firm ties lower outlook to ‘reset’ of growth strategy

Bumble Inc.’s shares took a record plunge on Thursday after the dating company slashed its annual revenue outlook, signaling that an overhaul of the brand’s flagship app has failed to reignite growth.

The Austin, Texas-based company said late Wednesday that 2024 revenue will gain by 1% to 2% from a year earlier. It had previously forecast growth of as much as 11%, and Wall Street was expecting 8.4%, based on estimates compiled by Bloomberg. Second-quarter results also largely missed forecasts.

Bumble, which went public in 2021, had already seen its shares plummet to a record low earlier this year after issuing a weak sales outlook and cutting around a third of its workforce. The company’s struggles to expand its user base reflects the broader challenges plaguing the US online dating industry, which has yet to recover from a post-pandemic reckoning.

The shares fell as much as 39% after trading opened in New York on Thursday, its biggest intraday decline on record. Bumble’s earnings also weighed on the shares of rival Match Group Inc., which saw a 2.8% decline in Thursday trading.

Bumble’s executives tied the dramatically lower outlook to a “reset” of the company’s overall strategy, which they unexpectedly laid out during a call with analysts on Wednesday. The platform, which has traditionally marketed itself as the best experience for women, will invest more in “the right balance and mix” of customers and more compelling dating experiences, they said.

Bumble’s subscription tiers will change to reward “positive peer behaviors,” and near-term, money-making efforts such as the expansion of its Premium+ offering will slow. “While the actions we are taking are difficult in the near term,” Chief Financial Officer Anuradha B. Subramanian said in the call, “we are in a healthy position financially as we execute.”

Bumble has also been raising the minimum requirements for new user profiles and photos, a move that it expects to lead to a more “authentic” experience over time. The company said it will invest in several new features, including new interest filters, a better matching algorithm and an AI-assisted photo picker. The firm also vowed to bolster efforts to crack down on bad actors on the platform.

The lower outlook has investors “concerned that the company is unclear around what its growth story will be from here,” said Jamie Lumley, an analyst with the research firm Third Bridge. The company needs “a clearer longer-term strategy” to retain talent, he added.

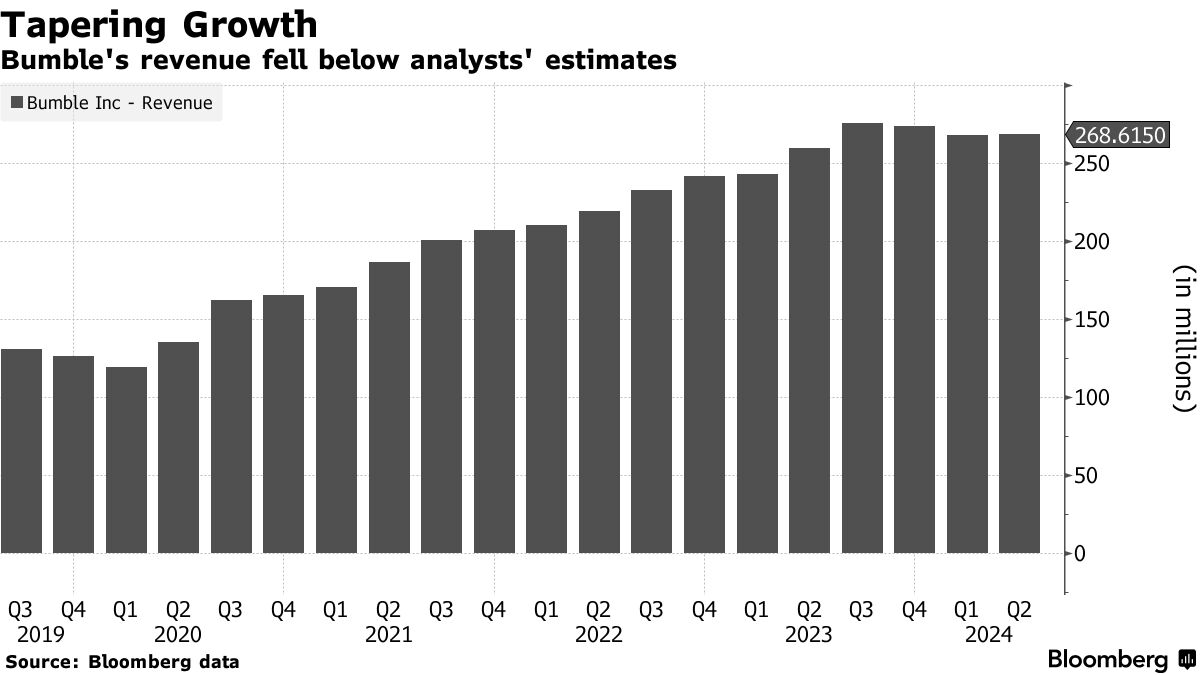

Bumble’s third-quarter forecast and second-quarter broadly missed the mark. Bumble expects sales for the current period of $269 million to $275 million, below the $296.1 million that analysts projected. Adjusted earnings before interest, taxes, depreciation and amortization will be between $77 million and $80 million, the company said. Wall Street was hoping for $91.5 million.

Revenue for the period ended June 30 increased 3.4% to $268.6 million, missing the average analyst estimate of $273.2 million. The number of users paying for Bumble — an important metric for investors — rose 14.7% to 2.8 million, in line with Wall Street estimates.

In contrast, Match, which owns Bumble’s biggest rival Tinder, jumped the most in nearly two years last week after the company delivered better-than-expected quarterly results.

Bumble has been in the throes of an internal leadership transition since founder Whitney Wolfe Herd announced in November that she would step down as Chief Executive Officer. Bumble has since named four new C-suite executives, who have been charged with overhauling the company’s mobile app to make it more appealing to younger users.

The redesign of the app has seemingly not been enough to court younger users or overcome macroeconomic conditions, said Chandler Willison, a research analyst with data analytics firm M Science.

“I believe Bumble in some ways is seeing the slowing growth that we’ve observed for Tinder as these businesses scale and face increasingly difficult year-ago comparisons, potentially facing some degree of saturation,” he added.

Increasing the number of paying users has been key to Bumble’s growth strategy, but progress has slowed since late 2021. The app’s higher-price Premium+ subscription tier launched in December but did not bring the “incremental uplift” the company had expected, executives said in February.

Written by: Evan Gorelick — With assistance from Natalie Lung @Bloomberg

The post “Bumble Shares Take Record Plunge on Slashed Annual Outlook” first appeared on Bloomberg