- Investors bet on more aggressive easing as economy stalls

- Some economists say cash rate must fall below neutral level

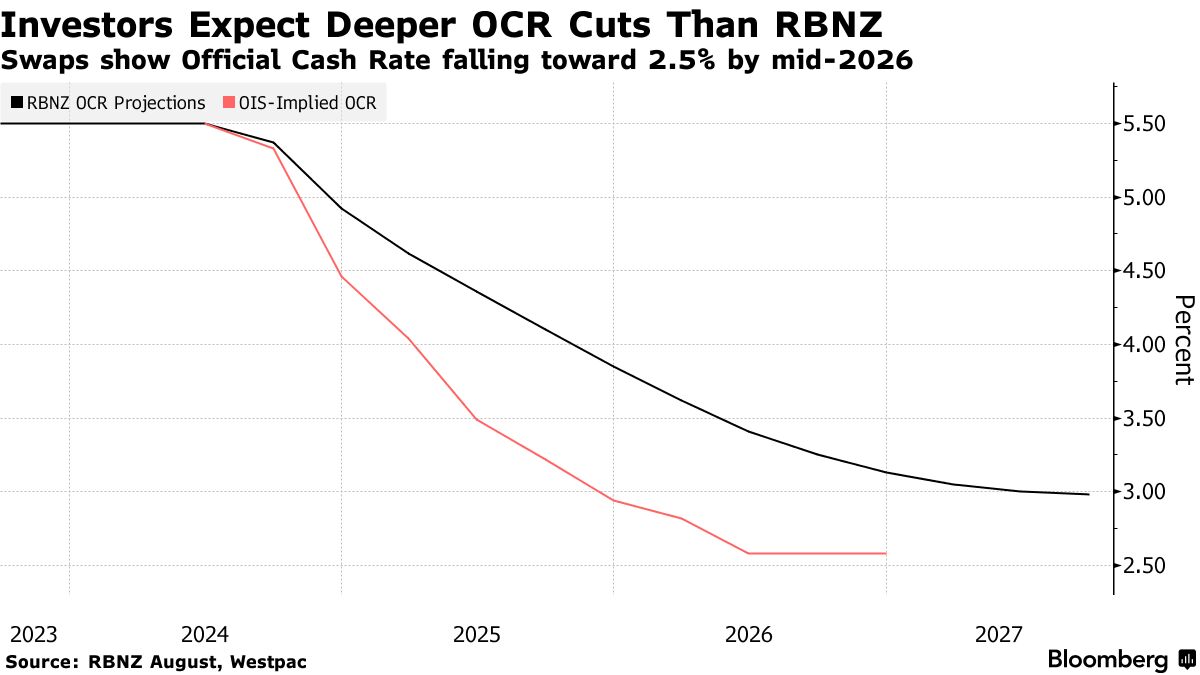

New Zealand’s central bank will cut interest rates further and faster than it says it will as the economy contracts and inflation slows, according to investors and some economists.

The Reserve Bank, which embarked on an easing cycle last month, will take its Official Cash Rate to 2.5% by mid-2026 from 5.25% today, market pricing shows, a view shared by economists at Capital Economics and Kiwibank. That’s despite the RBNZ projecting the OCR will trough at 3% from around the end of 2026.

“If we look back at the start of previous easing cycles, the Bank has always underestimated how aggressively it would end up cutting rates,” said Abhijit Surya, Australia and New Zealand economist at Capital Economics in Singapore. “We think this time won’t be any different.”

The central bank has already made an abrupt change to its policy stance, cutting rates by a quarter percentage point Aug. 14 after threatening to raise them just three months earlier. Markets are betting it will be forced to reverse course more aggressively as a prolonged period of elevated borrowing costs chokes demand.

Gross domestic product data next week are expected to show the economy shrank in the second quarter, putting it on the verge of its third recession since late 2022.

Tax Cuts

To be sure, government tax cuts that took effect on July 31 may support domestic spending and a recovery in the key tourism industry could also boost economic growth.

Of the nation’s four largest banks, only economists at Bank of New Zealand forecast the OCR will fall below 3%. At the other extreme, Westpac expects the benchmark to bottom out at 3.75%.

Still, inflation has slowed more than expected, to 3.3% at the end of June, and the RBNZ now projects it will return to its 1-3% target band this quarter. Indeed, selected components of the Consumer Price Index published today suggest annual inflation slowed sharply in August.

Unemployment is rising as the manufacturing and service industries contract and households rein in spending.

“If the RBNZ wants to remove the restrictiveness of interest rates, they need to go back to a neutral setting,” said Jarrod Kerr, chief economist at Kiwibank in Auckland. “That Goldilocks rate is estimated by the RBNZ to be around 2.75%, a long way from 5.25%. And we think they’ll need to go a little below, to 2.5%, to get things moving.”

While Kerr expects the cuts to be delivered in 12 consecutive quarter-point increments, Surya predicts a more rapid easing, with the inclusion of three half-point reductions taking the OCR to a low of 2.25% by the end of next year.

What Bloomberg Economics Says…

“The RBNZ took what it called ‘a gradual first step’ to lower rates last month. Weakness in payroll data suggests it had better move a lot faster than it forecasts to reorient policy toward supporting growth — or risk a deeper downturn and sharper lift in unemployment than it wants”

— James McIntyre, economist

To read the full note, click here

Financial markets see a further 75 basis points of cuts over the final two rate decisions of this year, suggesting one of them will be a 50-point reduction. The RBNZ’s remaining 2024 decisions are on Oct. 9 and Nov. 27.

Written by: Matthew Brockett @Bloomberg

The post “RBNZ Seen Cutting Rates Further, Faster Than It Currently Forecasts” first appeared on Bloomberg

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.