Another nail has been pounded in the coffin of the 2009 Bull Market. May the Bull rest in peace (RIP).

Yesterday new Federal Reserve Chairman Jerome Powell gave testimony to the US Senate’s banking committee. Based on his testimony the probability has increased that the US Federal Reserve will increase its discount rate four times during 2018. Analysts and economists had been forecasting that there would only be three rate hikes this year. The Fed’s becoming more aggressive than anticipated is bad news for stocks since they have historically declined when interest rates go up.

Up until the entire first quarter of 2018, the S&P 500 had experienced five accumulation or consolidation (sideways pattern) periods ranging from 14 to 25 days. This happening indicated a very healthy Bull market. However, that all changed. During the first quarter of 2018, the S&P 500 will not experience even one period of accumulation or consolidation.

Unless the markets can enter into a period of sustained accumulation or consolidation many of the long-term investors who were the drivers of the 2009 Bull will exit the market. The extended pattern of volatility is the seventh nail in the 2009 Bull’s coffin.

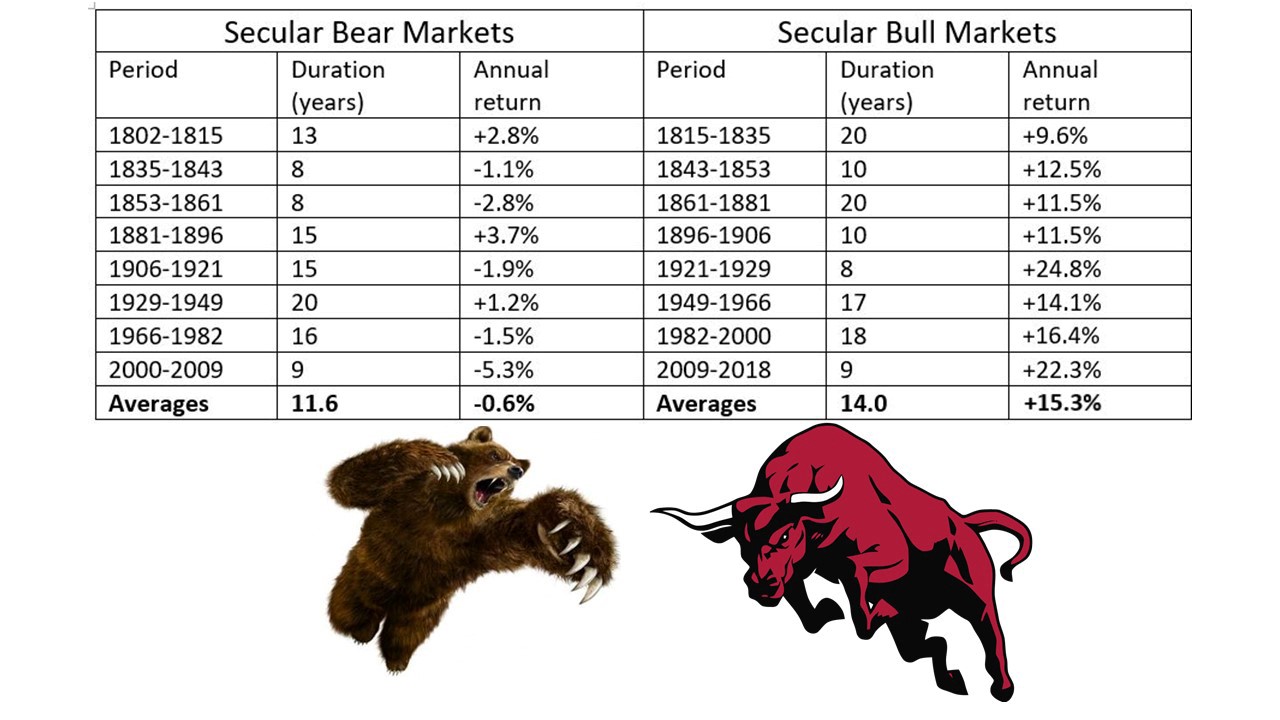

The seventh follows Facebook’s nail. See “Sixth Nail in Deceased bull’s coffin is Facebook”. Each additional nail increases the probability that the market will not get back to its January 2018 all-time high for at least eight years. This is because it’s likely the new secular bear market was born in January 2018. The table below which includes the eight secular bulls and bears since 1802 depicts that the recently departed bull had run its course based on its age and performance.

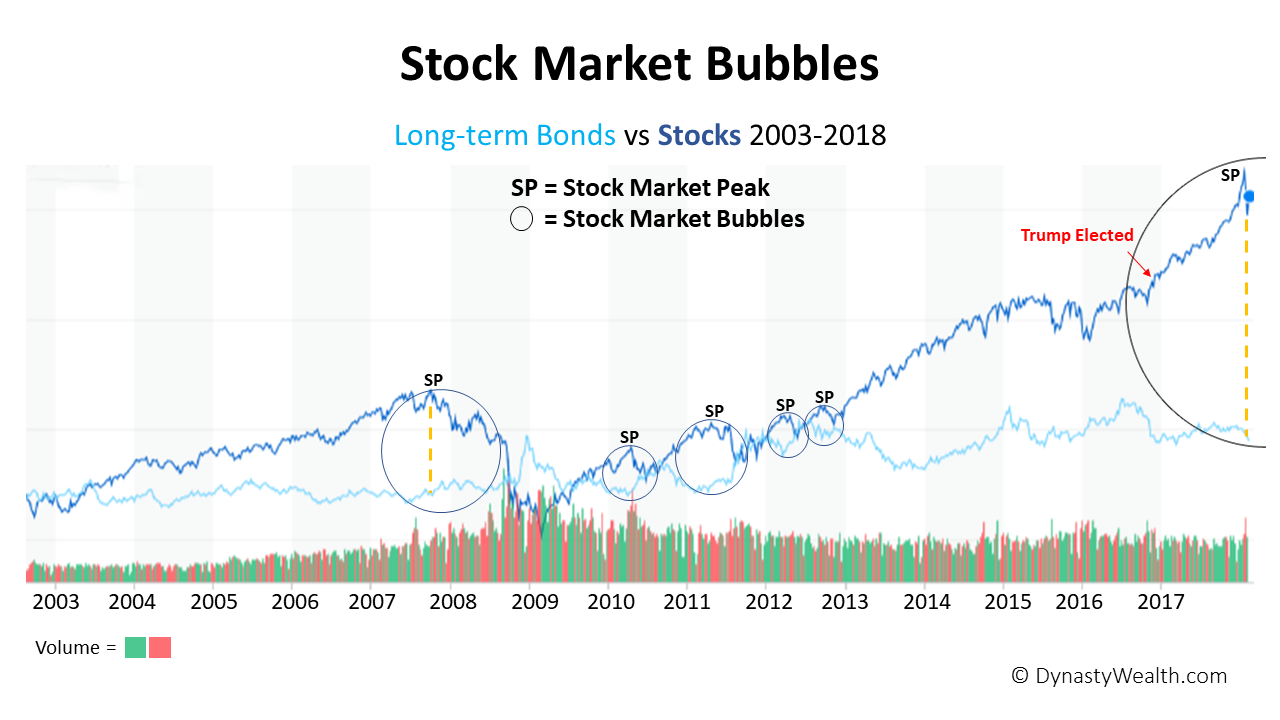

The chart below which depicts the stock market’s bubbles since 2007 is based on the price history of the S&P 500 versus long-term US government bonds for the period of 2003 through February 2018. The large bubble which had been in place prior to the election of Donald Trump as U.S. President has expanded significantly.

I have been monitoring this bubble since 2016. It was originally discovered from my crash research that I have been conducting since the Bank of Japan (BOJ) instituted a Negative Interest Rate Policy (NIRP) in February 2016. My research enabled me to find the bubble and other historical anomalies or distortions in the capital markets that have been present for the last several years. Watch the video below to view the charts and graphs for the anomalies and distortions which have put the markets on the precipice of a crash.

I am recommending the deployment of a 90/10 Crash Protection Strategy. For information on the strategy which is the only fail-safe strategy that one can utilize to protect their liquid assets from crashes, recessions and depressions view video below entitled “Crash! & 90/10 Crash Protection Strategy”.

My crash research that I began to conduct in 2016, resulted in my developing an algorithm that I utilized to issue market crash warnings during 2016 when negative interest rates posed great risks to the global economy. See equities.com article “NIRP Crash Indicator Signals Very Reliable for 2016”. Due to the ebbing of negative rates in 2017, after Mr. Trump’s election as President and the unprecedented low stock market and especially currency volatility, the NIRP Crash Indicator was disengaged in March of 2017. See equities.com article “No Longer a Need for NIRP Crash Indicator Signals”. Upon currencies volatility picking up the NIRP Crash Indicator will be re-engaged. Its warnings will be available to Trophy Investing’s members.

Disclaimer. Mr. Markowski’s predictions are frequently ahead of the curve. The September 2007 predictionsthat appeared in his EquitiesMagazine.com column stated that share-price collapses of the five major brokers, including Lehman and Bear Stearns, were imminent. While accurate, they proved to be premature. For this reason he had to advise readers to get out a second time in his January 2008 column entitled“Brokerages and the Sub-Prime Crash”. His third and final warning to get out, and stay out, occurred in October of 2008 after Lehman had filed for bankruptcy. In that article “The Carnage for Financials Isn’t Over”he reiterated that share prices for Goldman and Morgan Stanley were too high. By the end of November 2008, the share prices of both had fallen by an additional 60% and 70%, respectively — new all-time lows.