Predictions are difficult, especially those about the future. That old proverb (often attributed to Yogi Berra) is right but you can’t live without making certain presumptions. You presume your car will start, your refrigerator will stay cold, the lights will turn on when you flip the switch.

In fact, you could argue this “predictability” separates advanced economies from primitive ones. Most of us don’t have to worry about being attacked in our sleep or having food tomorrow. That security frees us to do other things.

Right now, some basic assumptions are no longer safe. The economy will keep suffering until they are reliable again, or we replace them with new assumptions. We can’t travel or even go to a restaurant or visit friends without wondering about our health. Where does that leave us?

Today I’ll defy the proverb, consider what we know and don’t know, and try to tell you where I think we’re going. In the long run (after The Great Reset in the late 2020s), I still foresee a wonderful new world. But we have to get there first.

Economists use the word “recovery” to define a rebound from the previous time period. So if there was a 30% drop, a 10% increase would, for an economist, be a “recovery.” But in the real world, it still means you are 20% below where you started. Recovery doesn’t necessarily mean recovered. Even optimistic projections say we won’t see anything like 2019 GDP until late 2021. Many suggest it will be even longer.

Even then, the changes we will have to put into our operating business models, not to mention the massive amounts of capital that it will take to start new businesses or resupply old ones, will make the “recovered” economy look significantly different than that of 2019.

And just for the record, because I am not optimistic about the speed of economic recovery does not mean that I am necessarily bearish on the stock market. When the Federal Reserve pumps $5 trillion (or whatever) into the system it is going to find a home. While I think earnings will take a severe hit in 2021, the market could hold simply due to massive Fed support.

There have been numerous times when the economy and the stock market were out of sync. Don’t equate the two. The stock market doesn’t necessarily tell us anything about the economy, or vice versa.

Now on to the letter…

Highly Uncertain

Last week the Federal Reserve sent Congress its latest “Monetary Policy Report.” These are usually rather vague, dry documents on everything the Fed is doing right and what could possibly go wrong. This one is more interesting than usual because so many things have gone wrong and may get even worse. Not that the Fed has good answers, of course.

Anyway, my friend Mish Shedlock blogged about the report and particularly the six downside risks it identifies. Kudos to the Fed for actually giving a fairly transparent, coherent, and reasonable list of risks. Here they are.

- The future progression of the pandemic remains highly uncertain.

- The collapse in demand may ultimately bankrupt many businesses.

- Unlike past recessions, services activity has dropped more sharply than manufacturing—with restrictions on movement severely curtailing expenditures on travel, tourism, restaurants, and recreation. Social-distancing requirements and attitudes may further weigh on the recovery in these sectors.

- Disruptions to global trade may result in a costly reconfiguration of global supply chains.

- Persistently weak consumer and firm demand may push medium- and longer-term inflation expectations well below central bank targets.

- Additional expansionary fiscal policies—possibly in response to future large-scale outbreaks of COVID-19—could significantly increase government debt and add to sovereign risk.

I could write an entire letter on any one of these risks, but let’s start at the beginning: “The future progression of the pandemic remains highly uncertain.”

Here’s what we know. Many of the first countries the virus struck—China, South Korea, Japan, New Zealand, Italy, Spain—brought it under control with aggressive lockdowns, testing, contact tracing, social distancing, and isolation of confirmed cases. Yet little outbreaks keep popping up. Life is still far from normal in those places. Read this Financial Times account of conditions in South Korea to see what I mean.

Here in the US, the national numbers are much improved since March and early April. That’s not the case everywhere, though. Look deeper and you’ll see the New York/New Jersey crisis is easing but cases are rising elsewhere. Testing numbers are up but that’s not the full explanation. Hospitalizations are also up in some states, as is the testing “positivity rate.” Those indicate actual virus spread. This was expected as more people circulate in public but could get out of hand if not handled well.

Former Food and Drug Administration head Dr. Scott Gottlieb said the states hardest hit by the latest coronavirus surge are “on the cusp of losing control.” Ten states, most of them concentrated in the South and West, have recently seen new record-high, seven-day averages of new coronavirus cases. Those states are Alabama, Arizona, California, Florida, Nevada, North Carolina, Oklahoma, Oregon, South Carolina, and Texas. Gottlieb is a serious medical professional and not prone to wild statements. We should pay attention.

To be clear, I believe the initial closures were necessary, given what we knew at the time. They successfully flattened the curve. But they were a brute force strategy with very harmful economic side effects and needed to end quickly. Scientists have learned a lot in the last three months. We can now attack the problem more precisely, as Mike Roizen and I explained earlier this month.

But even then, we are not going back to normal until late this year, at best. More likely it will be 2021 before a vaccine can be successfully developed, tested, produced, and widely distributed. That means many more months with masks, social distancing, reduced travel, and no large gatherings, at least like we knew in the past. It also assumes no more large-scale outbreaks. So the best-case scenario is still disastrous for big parts of the economy.

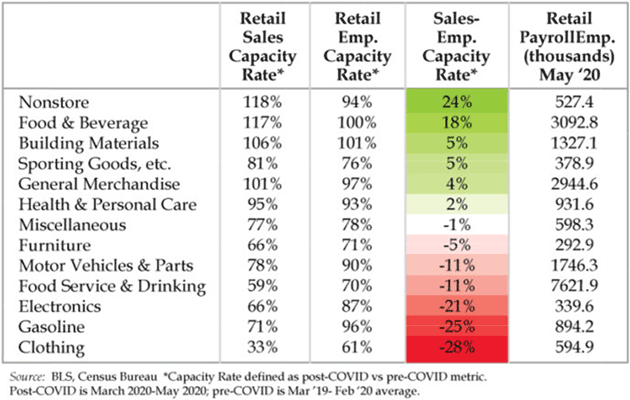

There was much celebration last week as retail sales showed a rather robust rise. Talk of a V-shaped recovery was in the air. Except that we have only roughly recovered to ~2015 in terms of GDP. The comments and table below come from Danielle DiMartino of Quill Intelligence (daily must-reading for me).

First, the good news. E-commerce and food are the big winners. Sales in the three months ended May are running well above their prior 12-month average while employment was relatively steady. This should open up short-run opportunities for job growth in these two areas. Anecdotes back this as we’ve seen job hiring announcements in these spaces.

Building materials and recreation, which includes sporting goods, hobby, book and music stores, also have moderately positive sales-to-employment capacity rates. Both sectors focus on DIY, at-home activities—endeavors rendered more attractive to millions of people working from home.

Unfortunately, losers outnumber winners. Clothing, gasoline, electronics, food service & drinking places and autos highlight the sectors at risk for future job cuts should the current sales levels be sustained in coming months. These five red categories represent 11.1 million payroll jobs, more than twice the 5.3 million of the four groups that are in the green.

Source: Quill Intelligence

It is certainly easy to see the restaurant businesses and their brethren are seeing extremely bad data. How soon before we go back to a movie theater? When we can watch from home, generally for less cost, even with a few friends for the human experience? How many other businesses have similar dynamics?

It is going to take several years for the employment situation to sort itself out. If your job is gone, what do you do now?

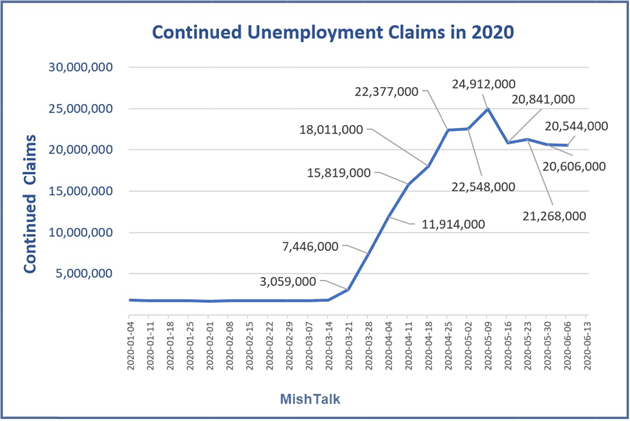

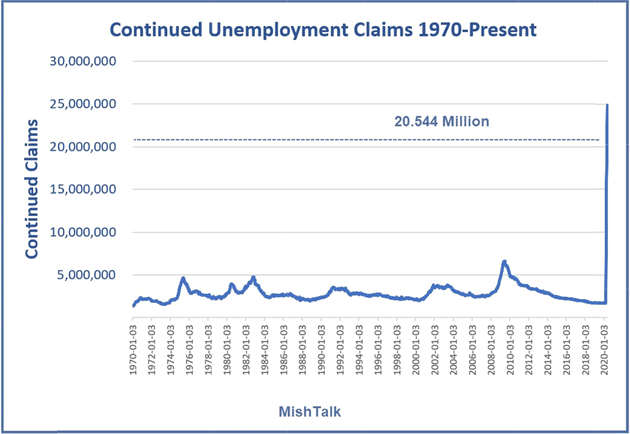

We can see that in continuing claims for jobless benefits. While off the highs, they have so far been stubbornly flat in June (H/T MishTalk).

Continuing claims are clearly at an all-time high. Only once before, in the middle of the Great Recession, did continuing claims even rise above 5 million.

The economy is currently being sustained by federal government largess. Those 20 million continuing benefit claimants are all getting at least $600 a week. Ironically, we have set the philosophical stage for Guaranteed Basic Income, at a much higher level than Andrew Yang’s $1,000 a month proposal. Furthermore, many businesses are staying alive only through the Paycheck Protection Program’s forgivable loans.

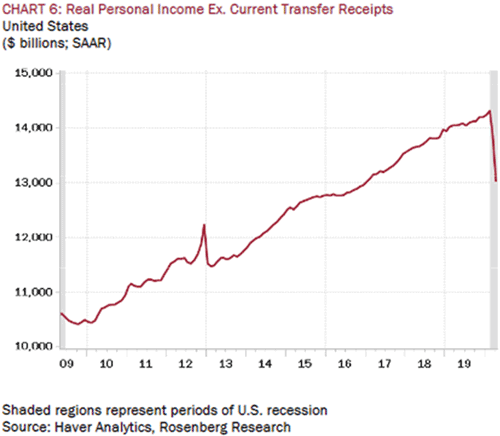

Let’s jump to an insight from David Rosenberg’s (Rosenberg Research) morning report.

There is nothing in the data, as of yet, to show that personal incomes are rising on their own—the story remains one of cash-flow support from Uncle Sam’s generosity and the ability (and willingness) of millions of Americans to skip their loan payments. Spending premised on such weak underpinnings does not constitute an official recovery. Not to mention the reality of historical data showing that recessions end when jobless claims get closer to 500K, not 1.5 million, which is where we are right now.

Source: Rosenberg Research

This isn’t something governors can easily reverse. They can let businesses open, but they can’t make consumers come back and spend freely. People have to feel safe; the economy can’t “recover” if even a small number don’t. As I’ve said, recovering even 90% of the previous consumer spending isn’t enough. We need it all, or close to all. We will get there, but it is going to take time.

Reallocation Shock

That brings us to the Fed’s second risk: collapsed demand could bankrupt many businesses. In fact, collapsed demand already bankrupted some businesses. More will surely follow. Nowhere is this more evident than restaurants.

I have a soft spot for independent restaurant owners. I enjoy great meals and appreciate the hard work that goes into them. Those who can actually do it consistently and profitably? They are among humanity’s best. They feed both our bodies and our souls. The tsunami that just hit them is indescribably painful. It hurts me to think of the places I’ve enjoyed wonderful evenings with friends, in dozens of different countries, that are now probably gone forever.

One recent survey of San Francisco restaurant owners found 60% lose money by staying open. They are low-margin even in normal times. Now capacity restrictions, combined with a general desire to stay home, make their prospects bleak indeed. Many won’t survive. The may hang on awhile, helped by PPP and other programs, but their challenge is deeper.

Nor is it just restaurants. The same or similar problems apply to bars, hotels, casinos, nightclubs, theaters, music venues—basically anywhere people gather in crowds. The crowds make them profitable. These businesses often can’t survive at 50% or even 80% capacity. They need to be full and now they can’t be. Can they change their model? Of course. But that will mean fewer employees and lower profits.

Which brings us to the real problem: These businesses employ millions of workers directly, and millions more depend on them indirectly. Many who lost their jobs in the last three months won’t get them back.

Here’s where it gets tough. I talk often about capitalism’s “creative destruction.” We go through times when the world changes. Businesses and workers must adapt. We don’t yet know how this will all develop, but COVID-19 seems likely to permanently change some industries. That could make many of these “temporary” job losses permanent.

Economists call this a “reallocation shock.” Affected workers have no good choices. They can either change careers, which might require expensive and time-consuming education, or move someplace that has jobs matching their skills. Neither is easy. It is similar to the way outsourcing and technology eliminated US manufacturing jobs in recent decades. This time, service industry workers are the unlucky ones, except the shock is happening much faster.

This has important social and political consequences but let’s stick with the economic ones. They are also bad.

Demand Shock

From a US perspective, this crisis began as a “supply shock” back in January/February, when China’s shutdowns threatened global supply chains. Now we have a demand shock, too. The millions who are staying home demand different goods, and their net spending is less. Others who have lost jobs or taken pay cuts or who are just concerned about the future are also spending less. That’s probably wise individually, but in a consumer-led economy it is devastating in the aggregate.

University of Texas economist James Galbraith explained it well in a recent Project Syndicate note. As he says, consumer incentives are to save, not spend.

Faced with radical uncertainty, US consumers will save more and spend less. Even if the government replaces their lost incomes for a time, people know that stimulus is short term. What they do not know is when the next job offer—or layoff—will come along.

Moreover, people do distinguish between needs and wants. Americans need to eat, but they mostly don’t need to eat out. They don’t need to travel. Restaurant owners and airlines therefore have two problems: They can’t cover costs while their capacity is limited for public-health reasons, and demand would be down even if the coronavirus disappeared. This explains why many businesses are not reopening even though they legally can. Others are reopening, but fear they cannot hold out for long. And the many millions of workers in America’s vast services sector are realizing that their jobs are simply not essential.

Meanwhile, US household debts—rent, mortgage, and utility arrears, as well as interest on education and car loans—have continued to mount. True, stimulus checks have helped: Defaults have so far been modest, and many landlords have been accommodating. But as people face long periods with lower incomes, they will continue to hoard funds to ensure that they can repay their fixed debts. As if all this were not enough, falling sales- and income-tax revenues are prompting US state and local governments to cut spending, compounding the loss of jobs and incomes.

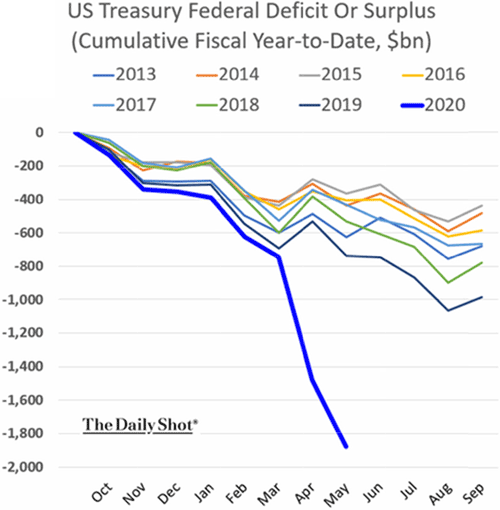

These household debt problems eventually become government debt problems. I have argued for years we are on an unsustainable fiscal path. This year it suddenly got much worse.

Chart: The Daily Shot

Note, this doesn’t include the Federal Reserve’s massive loan programs, through which it is transferring money to businesses that may or may not need it, and may or may not use the money productively. The resulting capital misallocations will further depress economic growth and reduce tax revenue.

State and local governments were already a problem, too. Many were over their heads in pension debt and now the crisis is decimating their tax revenue. This, too, may turn into federal debt.

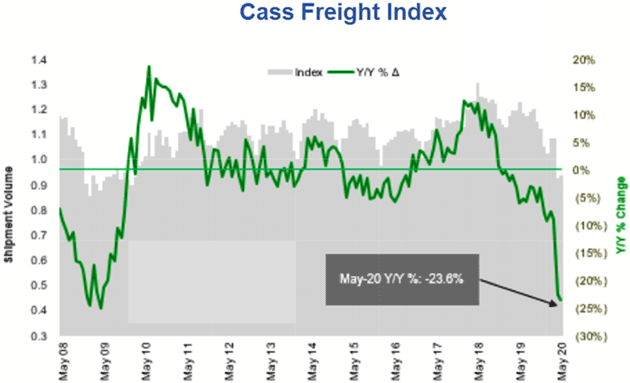

The demand shock is aggravating a sharp decline in freight volumes, which was already in progress before the pandemic. Here’s the latest Cass Freight Index, which I’ve referenced before.

Source: Cass Information Systems

Cass said in its commentary it doesn’t expect freight will return to 2019 levels until 2021 at the earliest. Note this isn’t just international freight. It is about goods and materials being shipped within the US.

Add all this up and we are already in a deep recession and, barring some miraculous COVID-19 cure, not going to recover this year. That will have serious effects that are more than economic. More on that later.

A Most Troubling Dilemma

US federal debt is over $26 trillion and rising rapidly. There will likely be at least a $1 trillion additional stimulus package before July 31 that extends the additional unemployment benefits for some period. There is some debate on the amount. I expect a further multi-trillion stimulus/infrastructure bill before the election.

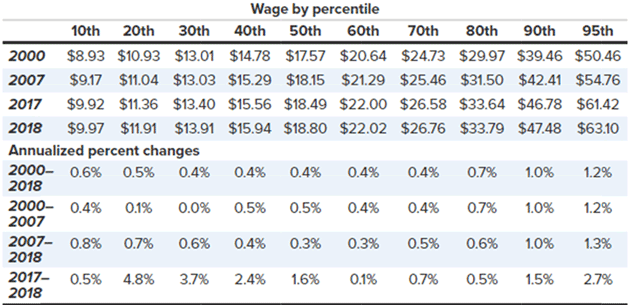

This table from the Economic Policy Institute shows hourly wages of all workers, by wage percentile, for 2000–2018 (in 2018 dollars).

Source: Economic Policy Institute

Current federal unemployment benefits of $600 per week, assuming a 40-hour week, equal $15 an hour (plus the state portion, which varies). That means the bottom 30% of US workers are better off keeping unemployment as long as they can. Especially the bottom 20%. Even the 40th percentile might be better off taking the unemployment benefit as they have no cost of getting to and from work.

I have no idea what the next level of benefits will be or how long they will last. But as I said earlier, we are moving toward a Guaranteed Basic Income which, added to other entitlement spending, would push us closer to $2 trillion-plus annual deficits.

The world will not come to an end with a $30 trillion US debt. How far will future US Congresses push that number? Explaining to the average politician that debt is a drag on future growth is futile. Spending money today helps them get reelected tomorrow. They will worry about the future later. Or at least most of them. Sigh.

This, along with Federal Reserve policy, is going to push us to a very uncomfortable place towards the end of this decade. Stay tuned…

How You Can Help

For now, what can we do? Our immediate problem stems from two sources.

- The coronavirus is continuing to spread.

- Concerned consumers are spending less money.

One simple thing we can all do will help attack both problems: Wear a mask in public. We can live with the virus risk, but not when a noticeable part of the population acts in ways others perceive as reckless. Walking around in public without a mask is like wearing an “I want a deeper recession” sign.

Note, it doesn’t matter whether you believe the mask really helps, or the virus is really dangerous. Perception is what counts. As long as substantial numbers believe normal life is too risky, the economy can’t recover. It is really that simple.

I’ll go further. Near-universal mask usage would help the economy more than another multi-trillion-dollar stimulus package would—a lot more, and faster, too. And without adding a penny to the national debt. You can see that in other countries.

Puerto Rico and Final Thoughts

First, you should be following me on Twitter @johnfmauldin. I find Twitter useful for news and information, depending of course on whom you follow.

My local gym has opened, sort of. You have to wear a mask, bring your own face towel, and half the air conditioning is down, so it’s kind of like working out in a sauna. But then again, a little sweat never hurt anyone.

I spend a lot of time considering how to find a semblance of certainty for investors in these times. There are opportunities. Progress has not stopped. It just looks different, especially in a world where everything is being repriced. But for now, it’s time to hit the send button. Have a great week!

Your dealing with uncertainty analyst,

John Mauldin

subscribers@mauldineconomics.com

The BullsNBears.com website was founded by market crash expert, Michael Markowski. BullsNBears.com publishes articles by Mr. Markowski and other qualified authors. These articles pertain to bear markets, market crashes, bottoms, recessions and depressions. Register below to be alerted when a new article is published on BullsNBears.com.