If I had to describe my last 500 letters in one word, it would be “complexity.” The older I get, the more I realize problems I once thought had reasonably straightforward solutions are, in fact, hideously complicated. That doesn’t make them unsolvable but it reduces the odds they will be. Often we start with good intentions and end up with unintended consequences, not all of which are good.

One such problem: supplying sufficient energy to maintain global economic growth while also raising living standards for billions in China, India, the entire continent of Africa, and other developing countries. And doing so in a sustainable way that doesn’t cause permanent environmental harm for everyone.

Energy prices affect everything. They are a necessary input to all other production. Some things are more energy-intensive than others, but without it we are all back in the stone age. The price matters for the same reason tax rates matter. Both are unavoidable costs, so we can produce more of everything if they’re low or at least stable.

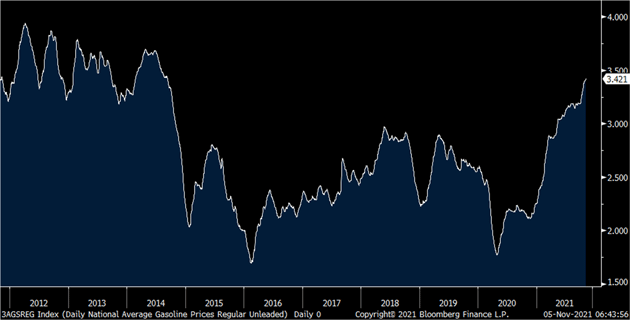

This problem is both intensifying and interacting with other challenges. Fuel prices have been rising worldwide, and may soon rise further. This week Bank of America raised its Brent crude oil forecast to $120 by mid-2022. That would be a price unseen since 2012. Natural gas is similarly spiking, as was coal until a recent retreat. The average US gasoline price is now $3.42 per gallon.

Source: Bloomberg

We have plenty of other problems and don’t need more, especially rising energy prices as the economy slows. Nonetheless, that seems to be what we will get. Today I’ll dig into what’s happening and what I think would be better.

Inflexible, Fragile, and Vulnerable

Like the Logistical Sandpiles problem I described last month, energy is actually a series of interrelated crises. We all feel the effects in different ways but the particular causes vary widely. They also defy simple solutions.

Gavekal’s Tom Holland captured the situation’s breadth well in a recent report, so I’ll just quote him.

“The rise in US gasoline prices has been driven by local refinery disruptions and climbing international prices for oil. However, gasoline prices are only part of the US energy story. Prices for the natural gas used to generate 40% of US electricity show wild distortions, with three-month forward prices for New England almost four times the benchmark price for Louisiana.

“China’s electricity shortages are all the result of Beijing’s ban on imports of Australian coal coupled with controls on domestic mining. India’s impending power cuts stem from a reluctance to pay international market prices for coal imports and capacity constraints on domestic production. Brazil’s troubles can be blamed on low water levels at the country’s hydroelectricity plants. And in Europe the finger is being pointed at Russia, which has not stepped up natural gas deliveries in response to depleted inventories and rising demand.

“But although the causes of these crises may appear to differ widely, there is a common thread: around the world shortages and price rises are typically the result of market distortions caused by deliberate policies.”

This is inarguably right. The original 1974 “Peak Oil” theory was as wrong as I always said. The world has plenty of oil, natural gas, and coal. We know where it is and how to extract it. If the available supply is small enough to raise prices unusually high, it is because humans made choices that led to that outcome. The choices may be defensible. Maybe they have other benefits, or they’re the least-bad alternative. But they are still choices. But as with many things human and political, the choices are often based on emotion, not logic.

In the report quoted above, Tom Holland attributes current problems to varying government and corporate policies. Then he zeroes in on the common threads.

“The motives behind these decisions vary, but two stand out. First, there is the desire to go green: to shift to less polluting energy sources with fewer greenhouse gas emissions. Second, there is the urge to improve efficiency: to provide the energy needed with the smallest possible capital investment.

“Both aims are in tune with the spirit of recent years. Viewed in isolation, both are laudable. But together, they have led to the creation of inflexible and fragile systems, highly vulnerable to disruptions in the supply of single energy sources…

“Politicians are maintaining that the price rises are the result of Covid-induced disruptions and that they will be short-lived. Therefore, they are sticking to their longer-term policy agendas. Few appear to worry that those very agendas are responsible for much of the rise in prices. Until they do, economies will remain exposed to similarly disruptive policy-induced energy crises.”

Hmm. Where else do we see fragile, inflexible, crisis-prone vulnerable systems persisting because bureaucrats stubbornly stick to their ill-considered agendas? That describes every major central bank.

This may surprise you, but I think the central bankers are mostly sincere. Their goals are usually right. The problem is they miscalculate the costs and side effects of reaching those goals. This is also the case for some energy policies. Sincere policymakers worldwide are putting constraints on the production of energy, increasing the risk on large capital investments in production, and not surprisingly, we get higher energy costs.

Imposing Pain

Today’s problems have roots in decisions year ago. You can see in the WTI chart how oil stayed above $80 and sometimes over $100 for about five years beginning in 2010. This encouraged capital investment and made many US shale fields profitable.

Source: tradingeconomics.com

In 2014 the Saudis, unhappy with the new competition, decided to defend their market share by producing more aggressively. This had a quick effect on prices, keeping crude below $70 and usually below $50 until recently. These low prices discouraged capital investment. Currently-operating fields have been depleted and here we are.

So part of the problem is purely economic, the normal boom-bust swings seen in any commodity market. But policy choices had a major effect, too, as governments around the world decided to fight climate change by discouraging fossil fuels and subsidizing cleaner energy sources, mainly solar and wind.

I realize climate change is a sensitive topic. Some think it is a civilization-ending threat, others think it is all a hoax. For my part, I just want clean air and water. Here in Puerto Rico we depend on unpleasant, unhealthy Bunker C oil-fueled electric plants. That is the same nasty fuel used to power oceangoing vessels. I would love to see us harvest the abundant sunshine and coastal breezes instead. They are better whether sea levels are rising or not. But it has to be economically feasible, which government-dictated changes often aren’t.

This is the problem I think policymakers all over the world aren’t facing. Clean energy technology is improving but is still a long way from replacing fossil fuels. Each alternative has limitations. Solar doesn’t produce at night. Wind depends on the weather. (Europe had the least wind on record last year.) We don’t yet have large-scale ways to store the power they produce, and won’t for quite a few years. In the meantime, we’ll still need reliable, 24/7/365 production from coal, natural gas, and nuclear power. Phasing them out too quickly invites the kind of shortages and high prices we are now seeing.

Some green energy advocates see high fossil fuel prices as good, thinking it will motivate faster adoption of their preferred solutions. This is the same flawed thought process that leads central bankers to punish savers with zero interest rates. They fixate on a goal and fail to think of the pain involved in reaching it.

My Camp Kotok friend and insightful thinker Megan Greene wrote an instructive Financial Times column on this point. She believes climate change creates real risks. But as an economist, she also sees the costs of controlling those risks.

“Most estimates for how we can achieve net zero over the next 30 years assume we will develop affordable technologies to capture carbon and can avoid suffering a major decline in real incomes and standards of living. That is a big assumption. Even if it’s right, the transition will inevitably create winners and losers.

“To be clear, the potential costs from transitioning and physical risk are less severe than those we’d incur by continuing to destroy the planet. I am not arguing that because there are costs, we shouldn’t do it. But politicians must be upfront about the price, financial or otherwise, and have concrete plans to support the losers.”

This is the real problem: Politicians think they can fight climate change without imposing pain on people who didn’t ask for it and aren’t prepared to handle it.

Megan observes this is remarkably similar to the globalization debacle. US and European leaders eagerly accepted China into the World Trade Organization but ignored the costs. They failed to protect those bearing the costs (Midwestern factory workers, for example), leading directly to today’s social divisions. We don’t need to repeat that failure.

Gradual Transition

So this leaves an important question: How do we secure a stable, low-cost energy supply without causing other problems?

You don’t have to believe in climate change to see that continued reliance on fossil fuels isn’t the best long-term solution. Among other problems, it empowers some of our geopolitical adversaries and harms poor countries that lack their own supply. The need to move fuel through pipelines and tankers makes it inherently expensive. The energy industry itself understands this, which is why the major producers are trying to diversify.

But notice that word “diversify.” Shifting some of your resources to clean energy isn’t the same as abandoning fossil fuels, which are and will remain necessary for some time. Punishing producers and users of a critical resource for which adequate alternative supplies aren’t yet available is counterproductive.

I’m a bit sad to admit China is facing this situation more intelligently than the US. That may be surprising, since we know China is by far the world’s worst carbon emitter. The regime knows this can’t continue, but also that it must continue until something else can be arranged.

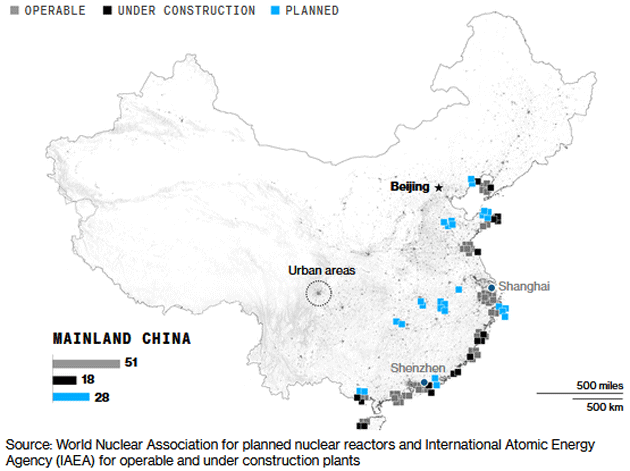

So, for the moment, China remains reliant on coal, oil, and natural gas, importing vast quantities of all three. But the government is also planning a gradual transition to cleaner power, which will include not just solar and wind but a massive nuclear power program, amounting to $440 billion over the next 15 years.

According to Bloomberg, China presently has 51 nuclear plants in operation, with 46 more planned or under construction. The US has 93 operating plants, many of them decades old, and only two under construction.

Source: Bloomberg

I’m a big nuclear energy proponent. I’m convinced it is the best way we have to produce clean, reliable, round-the-clock electricity regardless of weather conditions. I certainly don’t want more Chernobyl or Fukushima disasters. New designs that don’t depend on externally powered water cooling systems eliminate much of that risk. Other technologies like thorium reactors and nuclear fusion are coming. Nuclear is the perfect bridge to move us from carbon to a world of clean, sustainable, abundant energy.

In the West, nuclear suffers from “not in my backyard” reservations. China doesn’t have that problem, and so can take advantage of this ideal alternative we are largely ignoring here.

I’m far from the only one saying this. Bill Gates founded a company called TerraPower to develop advanced nuclear power technology. Their “Natrium” design uses liquid sodium rather than water to cool the reactor chamber. The high pressure that causes explosions simply doesn’t build up. The sodium doesn’t need pumps that can fail in an emergency, as happened in Fukushima. It circulates passively via hot air. It can even store heat in tanks of molten salt, which act as a giant battery that further increases power output.

TerraPower’s plant designs are smaller and much less expensive than conventional nuclear power plants. This lowers the capital cost for utilities, as well as the risk. They produce much smaller quantities of hazardous waste, too.

Chinese companies are developing similar technologies and Chinese state banks are financing about 70% of the costs for the reactors at much lower cost than we see in the West. Quoting from the Bloomberg article:

“That makes a huge difference because most of the cost of atomic energy is in upfront construction. At 1.4% interest, about the minimum for infrastructure projects in places like China or Russia, nuclear power costs about $42 per megawatt-hour, far cheaper than coal and natural gas in many places. At a 10% rate, at the high end of the spectrum in developed economies, the cost of nuclear power shoots up to $97, more expensive than everything else.”

At the current pace, China will deploy their technology far faster than the US does. I should point out that this is going to give the Chinese an enormous edge in nuclear facility production. They will be able to drive costs down because of the sheer quantity they are producing internally along with the enormous amount of research and development that must accompany such an effort. The West will rapidly fall behind and it will be hard to catch up.

This is really about national security as well as economics. A world in which China is energy-independent while the US grid gets less reliable every year is not going to work well.

As I said, this is a complex problem. Nuclear alone isn’t the answer, nor are solar and wind, nor are oil, gas, or coal. We haven’t even talked about the technologies that may help us keep using fossil fuels while greatly reducing harmful emissions. A lot is happening on that front.

Whichever course we take needs to be done in ways that protect innocent bystanders. Creating solar jobs in Florida while eliminating West Virginia coal mining jobs simply repeats the globalization mistake. Those on the losing end won’t be happy, nor should they be.

Climate warriors like to talk about the “externalities” of fossil fuels. They’re not wrong, but their solutions have externalities, too. Admitting it, and making sincere efforts to help the victims, would go a long way to getting what they want.

Would you really like to see carbon-free electricity? Then why not create the equivalent of Fannie Mae to fund low-interest loans to utility companies to install nuclear? Launching 10 or 15 plants a year would not only help the environment, it would create large numbers of high-paying jobs. If China can figure out how to switch existing facilities from coal to nuclear, as is doing the switchover on existing coal plants in situ, surely the West can figure it out. (I keep saying the West and not just the US, as Europe has some formidable nuclear technology and developers.)

Reliable Energy Needs Reliable Financing

The COP26 is meeting this week, and we did the usual feel-good proclamations, plus scary warnings, mixed in with a rather alarming note. This from the Financial Times:

“The Glasgow Financial Alliance for Net Zero (Gfanz)—which is made up of more than 450 banks, insurers, and asset managers across 45 countries—said it could deliver as much as $100tn of financing to help economies transition to net zero over the next three decades.”

That sounds nice, except buried in it is pressure from within the group and outside the group to commit to not funding new oil and coal projects. Somehow the magical thinking goes that if we don’t fund new coal, oil, and natural gas plants, renewable energy can somehow make up the slack and we won’t run out of energy on the way to being carbon free.

Remember the difference between 1.4% interest rates and 10% interest rates on the cost of nuclear power? I am not worried that oil and utility companies will lose access to financing. But that financing may increasingly come from private sources at higher costs. Higher interest costs for utilities means higher energy costs for consumers.

Bank of America’s $120 oil forecast is not all that outrageous. If we keep discouraging capital investment in oil and gas production, not just in the US but everywhere, while we are in the process of transition, we will see the same kind of high energy prices which cause riots in France and countries all over the world.

I am as much an environmentalist as anybody. I don’t want to see the air I breathe and I want nothing in my dark rum other than a crystal-clear ice cube. I recognize the need for transition to a more sustainable clean(er) energy production. China plans to replace every one of its coal plants by 2060. That is a long time, but they have massive energy needs and they are rationally planning the transition. I haven’t seen a lot about rational transition planning at COP26. Energy is going to be the ultimate reality check.

Failing to plan and finance a realistic transition will mean much higher and more volatile energy prices. We may one day wish for the good old days of $120 oil.

New York, Dallas, and Lake Granbury

I will be flying to New York while many of you are reading this letter. Next week’s schedule is full with lunches and dinners and meetings. I am really excited about it. Right now we are planning a dinner with some of the usual suspects along with Art Cashin. It has been too long since I’ve seen Art and many other of my New York friends. Then Shane and I will be in Dallas for a few days and end up on Lake Granbury to actually celebrate Thanksgiving with my family.

It is clear I will be flying more in the coming year. There are so many people I need to see where a video call just doesn’t cut it. And I actually got a live speaking gig offered to me in March. There was a point in my life were speaking fees actually were a nontrivial portion of my income. For the last two years it has been nonexistent. But significantly more than the fees, I miss speaking in front of a live audience.

So with that let me hit the send button and encourage you to, follow me on Twitter. John Mauldin unplugged and some might say a little unhinged. But we have fun and maybe learn something on the trip. Have a great week and spend some time with friends!

Your looking forward to live meetings analyst,

John Mauldin

BullsNBears.com was founded to educate investors about the eight secular bear markets which have occurred in the US since 1802. The site publishes bear market investing recommendations, strategies and articles by its analysts and unaffiliated third-party and qualified expert contributors.

No Solicitation or Investment Advice: The material contained in this article or report is for informational purposes only and is not a solicitation for any action to be taken based upon such material. The material is not to be construed as an offer or a recommendation to buy or sell a security nor is it to be construed as investment advice. Additionally, the material accessible through this article or report does not constitute a representation that the investments or the investable markets described herein are suitable or appropriate for any person or entity.